IRS Payment Plans

Partial Payment Installment Agreement: How to Qualify and What You'll Pay (2026)

The short answer: a partial payment installment agreement (PPIA) is an IRS monthly payment plan deliberately set below what would pay your debt in full — whatever remains when the 10-year collection statute expires becomes legally uncollectible. To qualify, you disclose your finances on Form 433-F and prove you can't full-pay before that deadline.

You sat down with your spouse, plugged your balance into the IRS payment-plan tool, and the monthly number it demanded doesn't exist in your budget. That gap — able to pay something, unable to pay everything — is exactly what the partial payment installment agreement was built for, and most people who qualify have never heard of it.

The IRS won't volunteer this option on any notice. You have to ask for it, and you have to prove you fit it. The image below shows how the three moving pieces fit together — your monthly payment, the collection clock counting down, and the slice of the balance the IRS never collects.

⏱ The real clock: there's no notice deadline attached to a PPIA, but two clocks are running right now. Penalties and interest accrue on your full balance every month you wait, while the 10-year collection statute quietly counts down in your favor. Getting an agreement approved stops enforcement — and cuts the monthly failure-to-pay penalty rate in half while it's in place.

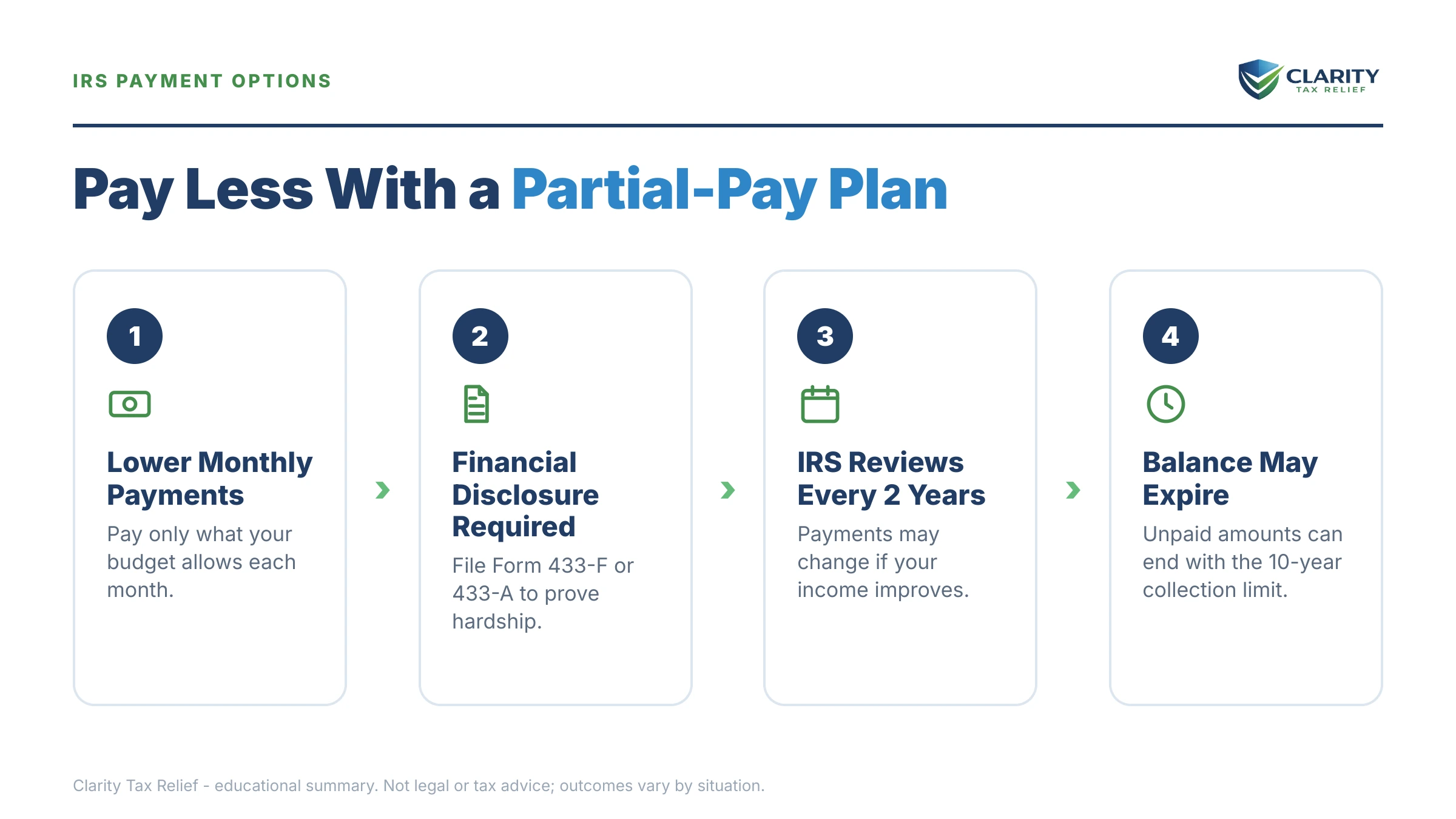

What a partial payment installment agreement actually is

A partial payment installment agreement is the only IRS payment plan designed from the start to collect less than the full balance. Every other installment agreement — guaranteed installment agreement, streamlined installment agreement, non-streamlined — is built to pay the debt off completely, with interest. A PPIA is built to pay what your documented budget allows until the debt legally dies.

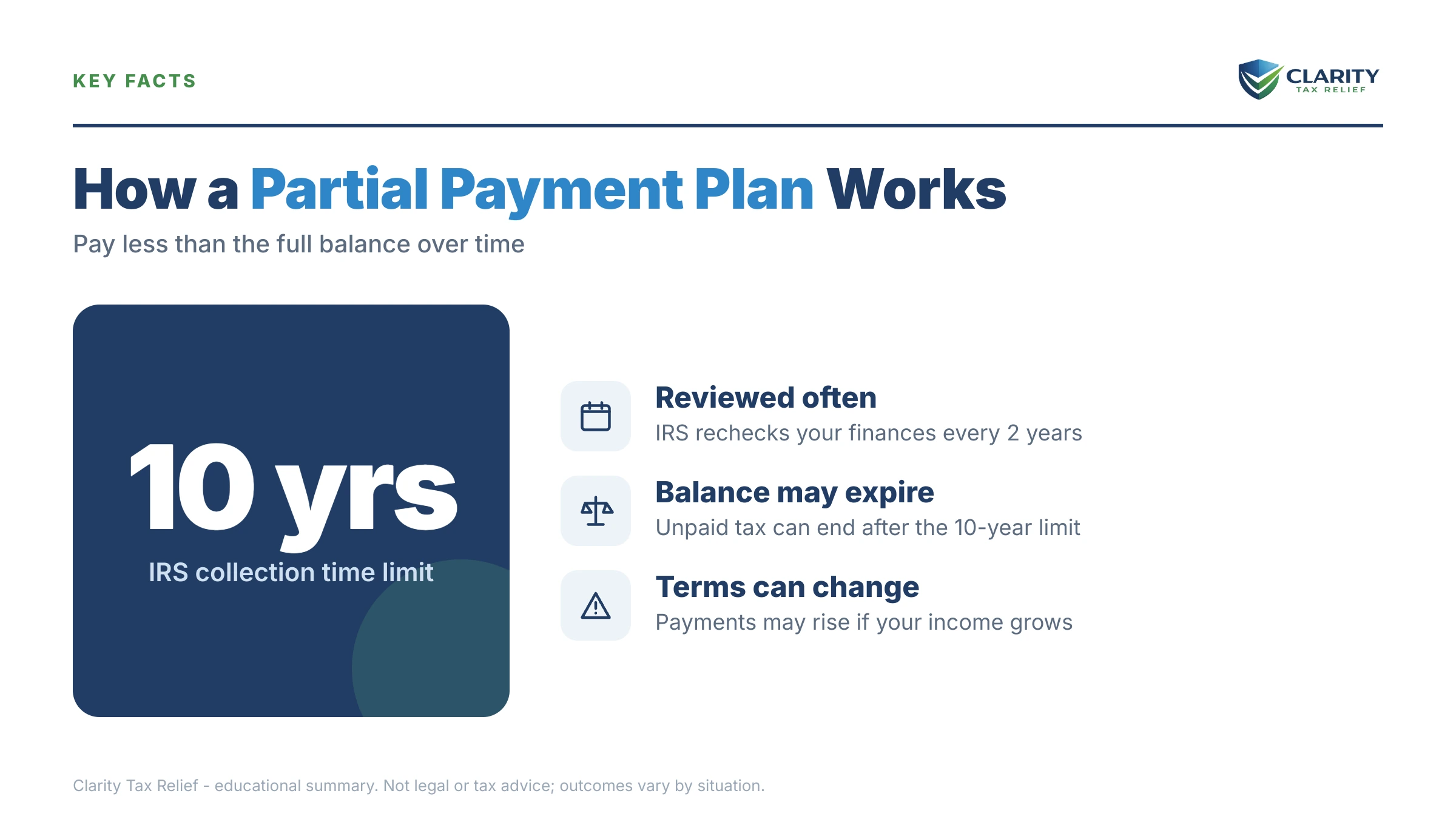

The mechanism is the collection statute. The IRS gets 10 years from the date each balance was assessed to collect it — the Collection Statute Expiration Date, or CSED (full explanation in our guide to how long the IRS can collect back taxes). On a PPIA, you make your monthly payment until the CSED arrives. Whatever your payments haven't covered by then becomes uncollectible under the law — no forgiveness application, no negotiation, no separate approval.

Two honest caveats before you build a plan around that. First, the clock can be paused: bankruptcy, a pending offer in compromise, collection appeals, and certain other events all toll the statute — our guide to what extends the IRS collection statute lists every one. A pending installment-agreement request itself can briefly pause the clock while the IRS considers it. Second, the IRS re-checks your finances during the agreement, so a PPIA is not a set-it-and-forget-it deal — more on the two-year review below.

If you just need the basics of setting up an ordinary full-pay plan, that lives in our step-by-step guide to setting up an IRS payment plan online. This page covers what that guide can't: the plan you request when the ordinary plan's math doesn't work.

How to qualify for a partial payment installment agreement in 2026

To qualify for a PPIA, you must prove on a collection information statement that your monthly budget cannot full-pay the debt before your collection statute runs out. That proof has several parts, and the IRS checks each one:

- All required returns filed. No installment agreement of any kind gets approved with unfiled years outstanding.

- Full financial disclosure. For most people that means Form 433-F, the shorter collection information statement, with roughly three months of pay stubs, bank statements, and bills to back it up. If a revenue officer holds your case, expect the longer Form 433-A instead.

- The disposable-income test. Here's the part that surprises people: the IRS measures your budget against its national and local allowable living expense standards, not your actual bills. If you spend $900 a month on car payments in a county where the standard allows $600, the IRS may count only $600 — which raises the "disposable income" it expects as your payment. This one calculation decides your PPIA amount, so it's worth getting right the first time.

- The asset-equity test. Before approving a plan that leaves debt unpaid, the IRS asks whether you can borrow against or sell what you own. You don't automatically lose your house or car — but you must document why the equity is unreachable: a loan denial letter, a vehicle you need for work, home equity no lender will lend against, or retirement funds whose liquidation would create hardship.

- Current-year compliance. Your withholding or estimated payments must cover this year's taxes. A new balance during the agreement puts it in default.

Two logistics to know. A PPIA cannot be set up through the IRS Online Payment Agreement tool — the online system only offers full-pay plans, so you'll request a PPIA by phone, by mail, or through your assigned revenue officer. And the setup fee follows the same tiers as other installment agreements, with reductions and waivers for low-income taxpayers — the current numbers are in our IRS payment plan setup fee guide.

One more expectation to set: because a PPIA leaves part of the debt permanently unpaid, the IRS commonly files a Notice of Federal Tax Lien to protect its claim before approving one, particularly on balances over $10,000. The lien no longer appears on consumer credit reports, but it's a public record and attaches to your property — a real consideration if you plan to sell or refinance a home during the agreement.

The PPIA math: what a couple owing $13,600 would actually pay

On a PPIA, your monthly payment equals your documented disposable income — and your total cost is capped by the months left on your collection statute. Here's a clearly hypothetical example with the arithmetic shown.

Say you and your spouse file jointly and owe $13,600 from your 2020 return, assessed in June 2021. Ten years from assessment puts the CSED at June 2031 — about 59 months away as of July 2026. To full-pay within the statute, the IRS would want roughly $13,600 ÷ 59 ≈ $231 per month, plus enough extra to cover the interest still accruing — realistically closer to $260.

Now run the Form 433-F math. Your combined monthly take-home is $6,100. After the IRS's allowable expense standards for housing, vehicles, food, health care, and taxes, your allowed expenses total $5,960. Disposable income: $140 per month — nowhere near $260. That gap is your PPIA case.

On an approved PPIA at $140/month, you'd pay $140 × 59 = $8,260 over the remaining life of the statute. Because interest keeps accruing on the unpaid balance, part of each payment goes to interest rather than principal — so at the CSED, likely $6,000 or more of the combined balance remains. That remainder expires with the statute and is never collected.

Compare the offer in compromise route for the same couple. Under the IRS's lump-sum formula, an offer generally starts at 12 months of disposable income plus asset equity: $140 × 12 = $1,680, plus (say) $8,000 of equity in a paid-off car ≈ a $9,680 offer — due largely up front, which is cash this couple doesn't have. The PPIA reaches a similar total outcome with no lump sum and no acceptance gamble. The pivot point in every case is the statute: estimate how many months remain on your own clock with our CSED Calculator before deciding which path fits.

What happens if you do nothing instead

If you set up nothing, the IRS's automated collection stream escalates from bills to levies without a human ever reviewing your file. The sequence runs in a fixed order:

- CP14 — the first bill, with a pay-by date typically about 21 days out. See our CP14 notice guide if this is where you are.

- CP501 / CP503 — reminder notices. Still just bills, but the balance grows every month.

- CP504 — Notice of Intent to Levy. The IRS can now seize your state tax refund, and a federal tax lien becomes a live possibility.

- LT11 / Letter 1058 — the final notice, starting a 30-day clock and your Collection Due Process rights.

- Levy — after that window, bank accounts (funds held 21 days before they leave) and wages (a continuous levy until released) are both fair game.

The 2025 workforce cuts made the IRS harder to reach by phone — but the notice stream, lien filings, and levies are issued by systems that never got smaller. Meanwhile the failure-to-pay penalty runs at 0.5% per month on the full balance, plus quarterly-adjusted interest. Once any installment agreement — including a PPIA — is approved, that penalty rate drops to 0.25% per month. Waiting costs money on both ends: more accrual now, and more months burned that could have been PPIA months.

Can't full-pay what you owe?

You already know your budget can't produce the full-pay number — the real question is what the IRS's own Form 433-F math says your payment should be, and whether a PPIA, hardship status, or an offer wins for your figures. An experienced tax professional will run all three in a free, confidential review. Penalties and interest accrue on the full balance every month this stays unresolved.

PPIA vs. your other options when you can't pay in full

A PPIA is one of five realistic paths for a balance you can't pay off, and the right one turns on three numbers: your disposable income, your asset equity, and the months left on your statute. Here's how the options compare on cost and how each one ends:

| Option | Upfront cost | What you pay monthly | How it ends |

|---|---|---|---|

| Short-term payment plan | $0 setup fee | Anything you choose — full balance due within 180 days | Debt paid in full |

| Streamlined installment agreement | Setup fee (reduced or waived for low-income) | Balance spread over up to 72 months (or the CSED, if sooner) | Debt paid in full, with interest |

| Partial payment installment agreement | Setup fee + Form 433-F disclosure | Your documented disposable income | Unpaid remainder expires at the CSED |

| Currently Not Collectible | $0 (Form 433-F disclosure) | $0 — collection paused | Debt expires at the CSED if finances never improve |

| Offer in Compromise | $205 fee + 20% down on lump-sum offers (both waived with low-income certification) | Offer amount, lump sum or over a short schedule | Debt resolved for the accepted offer amount |

Eligibility is where these options really separate. Each has a different gate, and the financial-disclosure burden rises as the potential savings rise:

| Option | Core eligibility test | Financial disclosure required |

|---|---|---|

| Guaranteed installment agreement | Owe $10,000 or less and can full-pay within 3 years | None |

| Streamlined installment agreement | Owe $50,000 or less and can full-pay within 72 months or by the CSED | None (set up online) |

| Partial payment installment agreement | Can pay something monthly, but not enough to full-pay before the CSED | Form 433-F (Form 433-A with a revenue officer) |

| Currently Not Collectible | Allowable expenses equal or exceed income — any payment creates hardship | Form 433-F |

| Offer in Compromise | Assets plus future income total less than the balance owed | Form 433-A (OIC) + Form 656 |

Two comparisons come up constantly. PPIA vs. Currently Not Collectible: both end at the CSED, but Currently Not Collectible status requires showing you can't pay anything — if your Form 433-F shows even $100 of monthly disposable income, the IRS will steer you to a PPIA instead. PPIA vs. Offer in Compromise: an offer in compromise ends the debt faster and needs no biennial review, but it demands cash up front and acceptance is far from certain — the IRS accepted roughly 1 in 5 offers in FY2024.

The cleanest rule of thumb: the further you are from your CSED, the more a PPIA costs in total — and the more an OIC tends to win; the closer you are, the harder a PPIA is to beat. A couple 2 years from their CSED paying $140/month sends the IRS $3,360 total. The same couple 9 years out sends $15,120 — likely more than a well-built offer.

How to set up a partial payment installment agreement, step by step

The IRS explains its general plan options at IRS.gov payment plans and installment agreements, but a PPIA request follows its own path:

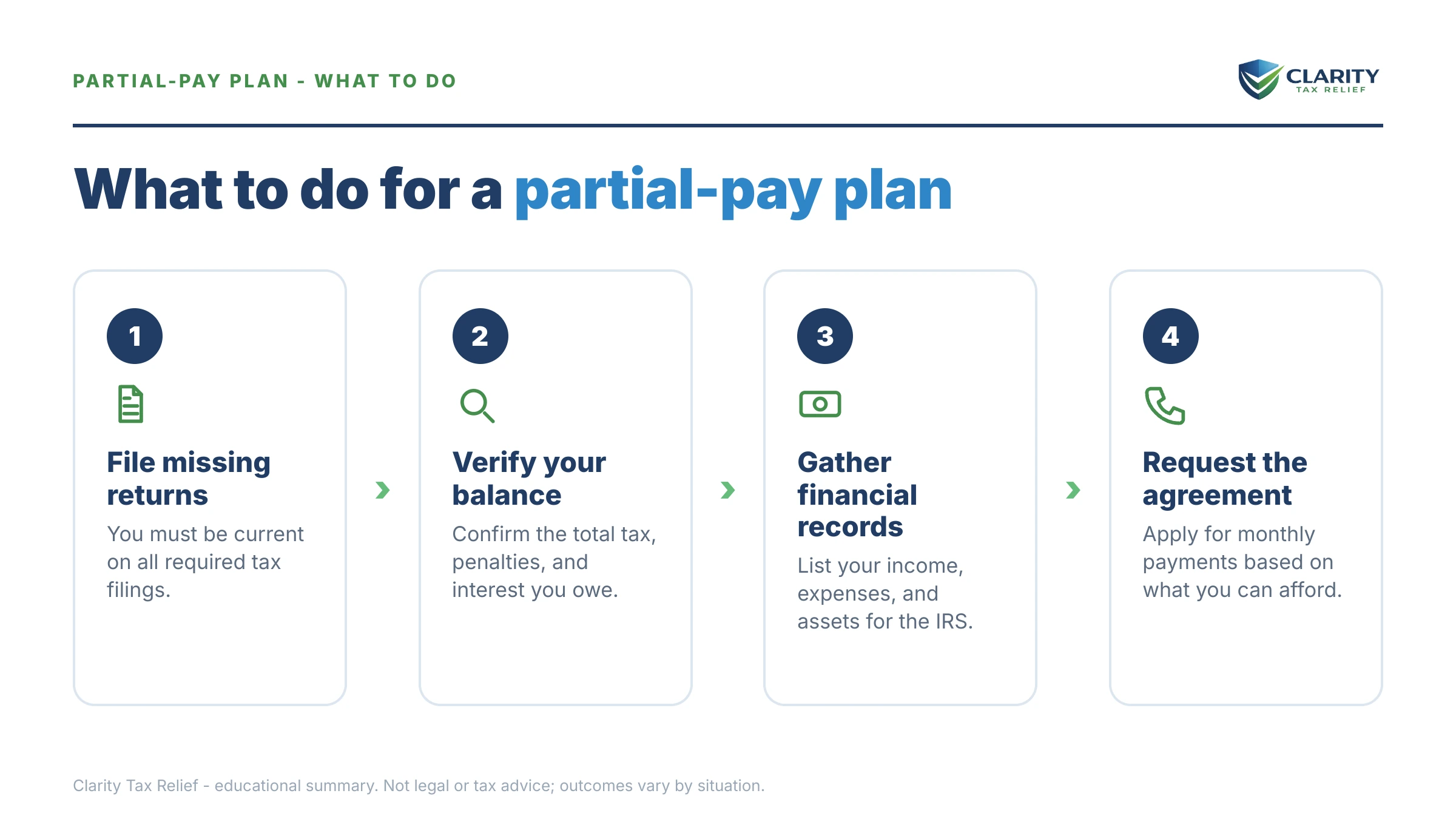

- File any missing returns. The IRS will not approve a PPIA — or any installment agreement — while required returns are unfiled, so filing compliance comes first.

- Pull your transcripts and estimate your CSEDs. Your account transcripts show each year's assessment date, which drives the collection-statute math that makes a PPIA worth pursuing.

- Complete Form 433-F with documentation. Report income, expenses, and assets accurately, and gather roughly three months of pay stubs, bank statements, and bills to back it up.

- Propose your payment with Form 9465. Request the monthly amount your Form 433-F disposable income supports — the number your documents prove, not a number you hope for. Our Form 9465 walkthrough covers the request line by line.

- Address your asset equity in writing. Be ready to show why you can't borrow against or sell assets — loan denials, work-vehicle needs, or home equity a lender won't touch.

- Set up direct debit and stay current. Automatic payments prevent accidental default, and staying current on this year's taxes keeps the agreement alive through its reviews.

When the IRS approves the agreement, it typically confirms the terms on Form 433-D — read it before signing, because that document sets your payment date, amount, and banking details.

Life on a PPIA: the two-year review, refunds, and missed payments

The IRS re-examines every partial payment installment agreement's finances roughly every two years, and your payment can move in either direction. This is the trade-off for paying less than you owe — the IRS reserves the right to check whether "less" is still justified:

| Your situation at review | What typically happens |

|---|---|

| Income and expenses roughly unchanged | Payment continues as-is until the next review or the CSED |

| Disposable income has grown | Payment is increased, or the agreement is restructured toward full payment |

| Finances got worse | You can request a lower payment or conversion to Currently Not Collectible |

| You added a new unpaid tax year | The agreement is at risk of default; the new balance must be addressed |

| You ignore the review request | The IRS can default the PPIA and send a CP523 termination notice |

Three more realities of the agreement's life span. Your federal refunds don't survive it: the IRS keeps and applies any refund to the back balance each year, which on a PPIA actually accelerates the payoff of the interest-bearing balance — details in our guide to whether the IRS takes your refund on a payment plan. A single missed IRS payment plan payment usually gets a short cure window before anything drastic happens — but a true default triggers a CP523 notice of intent to terminate, and termination puts you back in the levy pipeline. That's why we push almost every PPIA client onto a direct debit installment agreement: automatic payments are the single cheapest insurance a PPIA has against accidental default.

If a review outcome seems wrong — the IRS insists on a payment your real budget can't survive — you can push back through the IRS's own channels, and the Taxpayer Advocate Service exists for exactly the cases where the normal process is creating hardship.

When you can handle this yourself — and when help changes the outcome

Plenty of tax debts don't need a PPIA or a professional. If you can pay in full within 180 days, the free short-term plan wins — no fee, no financial disclosure. If your balance is under $50,000 and the 72-month payment fits your budget, set up a streamlined agreement yourself online in twenty minutes and skip everything on this page. Small, affordable, first-time balances are genuinely a DIY situation.

A PPIA is different, for one structural reason: your monthly payment for years to come is set by how your Form 433-F is prepared and argued — which expenses get allowed, how asset equity is presented, whether the IRS's standards or your documented specials apply. The same household can come out at $140/month or $320/month depending on that presentation. Experienced help earns its cost when a levy is already in motion, when multiple years have different CSEDs (each year's remainder expires on its own schedule), when there's business or payroll debt in the mix, or when the PPIA-vs-OIC math is close enough that picking wrong costs thousands.

Not sure whether the PPIA math or the offer math wins on your numbers? An experienced tax professional can run both side by side in a free partial-pay case review — or call (888) 825-7779 — before you commit to either path.

Terms on your PPIA paperwork, decoded

- CSED — Collection Statute Expiration Date: the day, 10 years after assessment, when the IRS's legal right to collect a given balance ends.

- Form 433-F — the collection information statement listing your income, expenses, assets, and debts; it's the evidence your PPIA payment is built on.

- Disposable income — your monthly income minus IRS-allowed expenses; on a PPIA, this number becomes your payment.

- Allowable living expenses — the IRS's national and local standards for housing, vehicles, food, and health care that cap what your budget can claim.

- Notice of Federal Tax Lien — a public filing that attaches the government's claim to your property; commonly filed alongside a PPIA.

- Two-year review — the IRS's periodic re-check of your finances during a PPIA, which can raise, lower, or restructure the payment.

Partial payment installment agreement FAQs

What is a partial payment installment agreement with the IRS?

A partial payment installment agreement (PPIA) is a monthly IRS payment plan set below the amount needed to pay your debt in full before the 10-year collection statute expires. You pay what your documented budget allows, and whatever remains when the statute runs out is legally uncollectible. Qualifying requires Form 433-F financial disclosure and all required returns filed.

Is the rest of my tax debt really forgiven at the end of a PPIA?

Yes — once the collection statute expiration date (CSED) passes, the IRS can no longer collect the remaining balance. The catch is tolling: bankruptcy, a pending offer in compromise, collection appeals, and certain other events pause the 10-year clock and push your CSED later. Before counting on a specific date, confirm your CSEDs from account transcripts, because each tax year has its own.

Can I set up a partial payment installment agreement online?

No. The IRS Online Payment Agreement tool only offers plans that pay the balance in full, so a PPIA has to be requested by phone, by mail with Form 9465 and Form 433-F, or through a revenue officer if one is assigned to your case. Expect the IRS to verify your income, expenses, and asset equity before approving it.

Will the IRS file a tax lien if I get a PPIA?

Often, yes. Because a PPIA leaves part of the debt unpaid, the IRS commonly files a Notice of Federal Tax Lien to protect its claim before approving the agreement, especially on balances over $10,000. The lien no longer appears on consumer credit reports, but it is a public record and attaches to property you own, which matters if you plan to sell or refinance.

What happens at the PPIA two-year review?

The IRS asks for updated financial information — typically a new Form 433-F with current pay stubs and expenses — roughly every two years. If your disposable income has grown, your payment can be raised, or the agreement can be restructured toward full payment. If your finances are unchanged or worse, the payment usually stays the same or can be lowered. Ignoring the review request can default the agreement.

Do I have to sell my house or car to qualify for a PPIA?

Not automatically, but you must address your equity. Before approving a PPIA, the IRS asks whether you can borrow against or liquidate assets to pay the debt. You can keep them if you document why the equity is unreachable — a loan denial, a car you need for work, or home equity a lender won't touch. Retirement accounts get the same analysis.

Is a PPIA better than an offer in compromise?

It depends mostly on your CSED and your access to cash. An OIC resolves the debt faster, but it requires a lump sum or short payment schedule, and the IRS accepted roughly 1 in 5 offers in FY2024. A PPIA needs no lump sum and no acceptance gamble — but the further away your CSED is, the more a PPIA costs in total, and the more an OIC tends to win.

Will the IRS keep my tax refund while I'm on a PPIA?

Yes. The IRS applies any federal tax refund to your back balance every year the agreement is in place — the offset does not count as your monthly payment, and it does not default the plan. On a PPIA this can actually work in your favor, since each offset shrinks the balance that interest accrues on. Adjust your withholding if you'd rather keep the money during the year.

What happens if I miss a partial payment installment agreement payment?

One missed payment usually doesn't terminate a PPIA on the spot — the IRS generally allows a short cure period and sends a CP523 notice of intent to terminate before ending the agreement. Contact the IRS before the termination date on that notice to reinstate the plan, and set up direct debit so a forgotten due date never puts the deal at risk. A defaulted agreement puts you back in the levy pipeline.

Your next 24 hours

- Find your assessment dates. Log into your IRS online account or pull account transcripts and note the assessment date for each year you owe — those dates set the CSEDs that make or break the PPIA math. (You can also verify balances and pay anything small directly at IRS.gov/payments.)

- Gather your financial proof. Last year's return, three months of pay stubs and bank statements for both spouses, and your major monthly bills — everything Form 433-F will ask for.

- Get the numbers run before you propose anything. The payment you request is the payment you'll live with — get a free case review at the 2-minute form or (888) 825-7779 so the Form 433-F math is argued in your favor from the start. Interest and penalties accrue on the full balance until an agreement is in place.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.