IRS Collections

What Extends the IRS Collection Statute? Every Event That Pauses the 10-Year Clock (2026)

The short answer: what extends the IRS collection statute is any event that legally freezes collection — a pending Offer in Compromise, bankruptcy's automatic stay (plus six months), a Collection Due Process hearing request, an innocent spouse claim, or living outside the U.S. for six-plus months. The clock stops while each runs, and that time is added back at the end.

You counted on the 10-year rule. You did the math from the year you fell behind, figured the finish line, and then your transcript — or a letter — showed the IRS still collecting well past year ten. The date didn't move by accident: something you filed, or something that happened to you, paused the clock.

This guide lists every tolling event, how much time each one adds, and how to calculate your real expiration date. Every pause leaves a fingerprint on your IRS account transcript — the image below shows exactly what those entries look like and where to find them.

⏱ The real clock: there is no response deadline on the CSED itself — it runs (or pauses) automatically based on what's on your account. But interest compounds daily whether the clock is running or stopped, and every tolling event you trigger pushes your expiration date further out.

Why your CSED is later than year ten

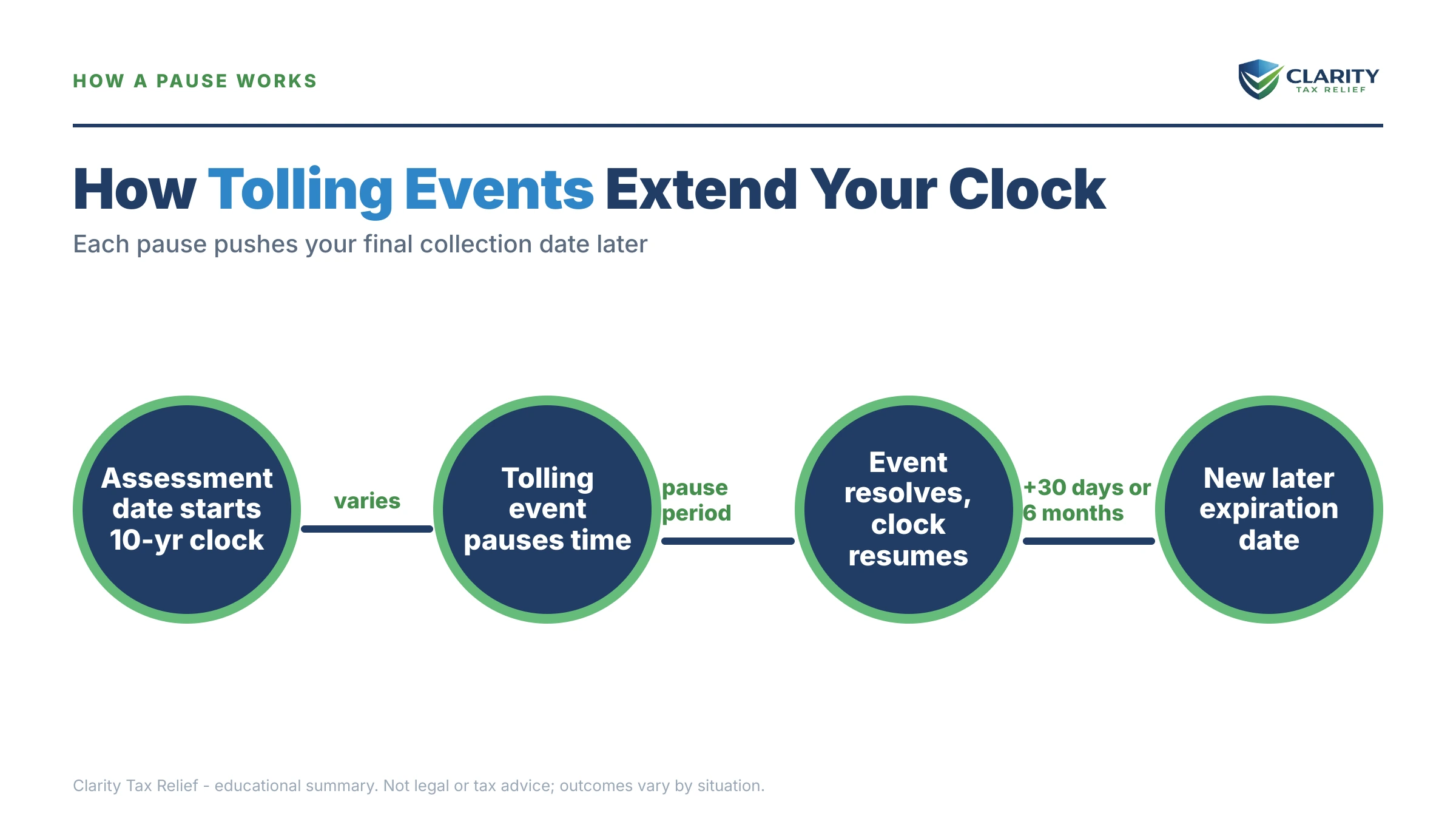

The IRS gets 10 years from the date of assessment to collect — but federal law suspends that clock whenever the IRS is legally barred from collecting. The logic is simple: if you file something that forces the IRS to stand down (an offer, a bankruptcy, an appeal), Congress doesn't let that stand-down time count against the IRS. The clock pauses, then resumes where it left off — often with extra days tacked on.

Two things trip people up. First, the clock starts at assessment, not the tax year — a 2019 return filed late in 2021 starts its 10 years in 2021. Second, tolling is per assessment: an audit that adds tax creates a second, later clock on the same year. The baseline rule is covered in our guide to how long the IRS can collect back taxes; this page covers everything that stretches it.

Just as important is what does not pause the clock: Currently Not Collectible status, an active payment plan you're making payments on, annual CP71 reminder notices, and a filed tax lien all leave the CSED running. Only the events below stop it.

What extends the IRS collection statute: the complete list

Eight events reliably extend the IRS collection statute, and each adds a different amount of time. Here is the full reference, followed by the fine print on each:

| Tolling event | Clock stops while… | Extra time added at the end |

|---|---|---|

| Offer in Compromise pending | The IRS reviews the offer (can run up to 2 years) | +30 days after rejection, plus any appeal period |

| Bankruptcy | The automatic stay is in effect | +6 months |

| CDP hearing (Form 12153, timely) | The hearing and any court review are pending | Topped up to at least 90 days if less remains |

| Innocent spouse claim (Form 8857) | The claim and Tax Court window are open (requesting spouse only) | +60 days |

| Installment agreement request | The request is pending | +30 days after rejection or termination, plus appeal |

| Living outside the U.S. 6+ months | You're continuously abroad | Statute can't expire until at least 6 months after return |

| Combat zone service | You serve in the zone | +180 days |

| Taxpayer Assistance Order request (Form 911) | The TAS application is pending | None beyond the pending period |

Offer in Compromise. The single most common way small-balance taxpayers accidentally extend their own statute. The moment Form 656 is submitted and processable, the clock freezes for the entire review — and reviews routinely run a year or more. If the offer is rejected, add 30 more days, and more if you appeal. An accepted offer resolves the debt, so the extension only stings when the offer fails. A pending offer shows on your transcript as code 480.

Bankruptcy. The automatic stay bars IRS collection, so the statute suspends for the full stay — then six months more. A four-month Chapter 7 adds about ten months; a five-year Chapter 13 can add roughly five and a half years. For a small-business owner, note that trust-fund payroll liabilities generally survive bankruptcy, so you can emerge with the same debt and a longer clock.

A CDP hearing — but not a CAP appeal. A timely Form 12153 CDP hearing request suspends the statute from the request through the final determination, and if fewer than 90 days remain when it ends, the CSED is extended to a minimum of 90 days. A CAP appeal, by contrast, does not toll the CSED — one real reason to weigh which appeal route fits your case, especially in a debt's final years.

Innocent spouse claims. Filing Form 8857 suspends the statute — but only for the spouse who requested relief — until the 90-day Tax Court petition window closes (or the court's decision becomes final), plus 60 days. The non-requesting spouse's clock keeps running.

Installment agreement requests. This one is widely misunderstood. An active payment plan does not toll the statute. But the statute is suspended while a request is pending, for 30 days after a rejection, for 30 days after a termination, and during any appeal of either. Repeatedly requesting and abandoning plans quietly stretches your CSED.

Time abroad, military service, and TAS. Living outside the U.S. continuously for six months or more suspends the statute for the entire absence — and it can't expire until at least six months after you return, which matters if you're considering relocating with a balance. Combat zone service suspends collection during service plus 180 days; the details, including deferment rights, are in our guide to combat zone IRS collection relief. A pending Form 911 Taxpayer Assistance Order application also briefly suspends the clock.

Two extensions that aren't tolling. A signed Form 900 waiver voluntarily extends the CSED — since the 1998 IRS reform law, the IRS can generally only request one in connection with an installment agreement, and you can decline. And if the government sues to reduce the assessment to judgment before the CSED runs, the court judgment replaces the statute entirely. That's rare, and essentially unheard of at four-figure balances — it's a large-debt tool.

How tolling shows up on your account transcript

Every event that pauses the collection statute posts a transaction code to your IRS account transcript, so you can reconstruct your real CSED yourself. Pull the transcript, find the assessment date, then scan for these codes:

| Code | What it means for your CSED | What to do |

|---|---|---|

| 480 | OIC pending — clock frozen from this date | Measure the span from 480 to the 481/482 that closes it, then add 30 days |

| 481 / 482 | OIC rejected / withdrawn — clock resumes | Add the pending span plus 30 days (plus appeal time) to your CSED |

| 520 | Bankruptcy, litigation, or CDP freeze in effect | Note the date; pair it with the 521 that releases it — see code 520 |

| 521 | Freeze released | For bankruptcy spans, add the full 520→521 period plus 6 months |

| 550 | CSED extended or recalculated — a new date is on file | This is the IRS's own recalculation; verify its math before accepting it |

| 150 / 290 / 300 | Assessment dates — each starts its own 10-year clock | Compute a separate baseline CSED for each assessment |

If transcripts are new to you, start with our walkthrough on how to read an IRS account transcript. Once you have the assessment date and the tolling spans, you can estimate your own expiration date with our free CSED Calculator — it estimates the date; only the dated entries on your account settle it. And know this: the IRS miscalculates CSEDs often enough that its own figure is worth double-checking. A wrong TC 550 date can be challenged.

A worked example: how a $6,200 debt gains 19 extra months

This is hypothetical, but the math is exactly how the IRS runs it. Say you're a small-business owner and the IRS assessed $6,200 in unpaid payroll-related tax on August 15, 2020. Baseline CSED: August 15, 2030 — ten years later.

Then life happens:

- Chapter 7 bankruptcy, filed March 2022, closed July 2022. The stay ran 4 months; add the 6-month tack-on. 4 + 6 = 10 months added. The trust-fund portion of the payroll debt survived the discharge.

- Offer in Compromise, submitted January 2024, rejected September 2024, not appealed. Pending 8 months; add 30 days. 8 + 1 = 9 months added.

Total suspension: 10 + 9 = 19 months. The real CSED lands around March 2032 — a year and a half later than the date you'd get counting ten years on your fingers. And through every one of those paused months, interest kept compounding daily and the failure-to-pay penalty kept posting, so the $6,200 grew the whole time the clock stood still.

What happens if you try to run out the clock

Waiting out the CSED is a strategy the IRS knows well, and its systems are built to make the final years the hardest. The sequence typically unfolds like this:

- Early years: automated notices cycle, every tax refund you're owed gets offset to the balance, and a federal tax lien may be filed — it attaches to business assets and receivables, not just your home.

- Middle years: quieter accounts get annual reminder notices and may be assigned to a contractor — see our guide to IRS private collection agency calls. The debt isn't forgotten; it's queued.

- Final years: the IRS prioritizes accounts approaching expiration. Levy activity and revenue officer attention increase precisely when you're closest to the finish line, and a levy served before the CSED can keep collecting after it.

- Large balances: the government can sue to reduce the debt to judgment, replacing the CSED with a court judgment. Rare — and effectively never worth the government's cost at a $6,200 balance — but it exists.

The full arc, notice by notice, is mapped in our IRS collection process step by step pillar. The takeaway: running the clock passively is very different from being levied in year nine because you never engaged.

Not sure when your debt actually expires?

Send us your transcript. An experienced tax professional will calculate your real CSED, map every tolling event on your account, and show you whether waiting or resolving costs less — free, confidential, no pressure. Interest and penalties accrue every day the balance sits.

Your options while the clock runs — and what each costs in time

Every resolution move has a tolling price tag, and smart strategy weighs both. Here's how the main paths interact with your CSED:

- Pay it off or set up a plan. An active installment agreement doesn't toll the statute, and at $6,200 a streamlined plan is available online with no financial disclosure. If the balance is small enough to clear within 180 days, a short-term plan costs $0 to set up. Compare methods in our guide to the best way to pay the IRS.

- Currently Not Collectible. CNC pauses collection but not the clock — which is why, for genuinely broke taxpayers, it's the one path where time works entirely in your favor. Eligibility is means-tested against IRS expense standards.

- Offer in Compromise. If your finances truly can't cover the debt, an OIC can resolve it for less — but a failed offer buys the IRS a year or more of extra collection time. With only a few years left on the statute, that trade often favors waiting; with eight years left, it often favors the offer.

- Appeals. Use CDP when you need its rights and court review; use CAP when speed matters and preserving the CSED matters more, since CAP doesn't suspend the statute.

The general playbook for choosing and executing these on your own lives in our hub on how to settle tax debt yourself — here, the point is narrower: never file anything without knowing what it does to your date.

How to check and protect your CSED, step by step

- Pull your account transcript for every year you owe — the assessment date next to code 150 (or 290/300) starts each 10-year clock.

- List every tolling event with dates: OICs, bankruptcies, CDP hearing requests, innocent spouse claims, and any stretch of six-plus months outside the U.S.

- Estimate your real CSED by adding each event's suspension period (plus its tack-on days) to the baseline date — our CSED Calculator can help you rough it out.

- Confirm the IRS's number by requesting your CSED in writing or having a professional pull it — the IRS miscalculates CSEDs often enough that its figure is worth challenging.

- Decide before you file anything new — every OIC, hearing request, or bankruptcy you submit from here changes the date, so choose your strategy with the full picture.

When you can handle this yourself

Plenty of CSED questions don't need professional help. If you owe one year, have never filed an offer or a bankruptcy, and just want your date, the transcript math is straightforward: assessment date plus ten years. If the balance is manageable — like the $6,200 in our example — setting up a plan online or paying through IRS.gov/payments before enforcement starts is usually cheaper than any strategy built around waiting.

Experienced help changes the outcome when the calculation itself is contested: multiple assessments across several years, an OIC-plus-bankruptcy history like the example above, a TC 550 date you think is wrong, a business with trust-fund exposure where personal and entity clocks differ, or a levy landing in the statute's final years. Those cases turn on getting dates corrected — and a corrected CSED has ended more than one collection case outright — but that only happens when the recalculated statute has already expired; in most cases a CSED review simply confirms (or slightly adjusts) the IRS's date, so treat this as a check, not an expected result. If the IRS won't fix a clearly wrong date, the Taxpayer Advocate Service exists for exactly that kind of stuck problem.

Terms on your transcript, decoded

- CSED — Collection Statute Expiration Date: the day an assessment legally dies, ten years after assessment plus all tolling.

- Tolling — a legal pause of the statute; the clock stops, then resumes, and the paused time is added to the end.

- Assessment date — the day the IRS formally records the tax on its books; each assessment starts its own 10-year clock.

- Automatic stay — the bankruptcy-court order that halts IRS collection while the case is open, suspending the statute plus six months.

- Form 900 waiver — a signed, voluntary extension of the CSED, now generally requested only alongside an installment agreement.

- Suit to reduce to judgment — a government lawsuit that converts the tax debt to a court judgment, replacing the CSED with the judgment's own life.

Collection statute questions, answered

Does an installment agreement extend the IRS collection statute?

An active installment agreement does not pause the 10-year clock — payments continue and the CSED keeps running. But the request itself tolls the statute while the IRS considers it, plus 30 days after a rejection or termination, and any appeal of that decision adds more. If you sign a CSED waiver as a condition of the agreement, that extension is separate and voluntary.

Does Currently Not Collectible status extend the CSED?

No. CNC (hardship) status pauses collection but not the statute — the 10-year clock keeps running the entire time you're in it. That's why CNC can be a legitimate long-term strategy for some taxpayers: if your finances never recover, the debt can expire while you're protected. The IRS reviews your income periodically and can reactivate collection if it improves.

How do I find out my exact CSED date?

Start with your IRS account transcript: your assessment date appears next to code 150 (or 290/300 for later assessments), and the baseline CSED is 10 years later. Then add time for any 480, 520, or 550 entries. You can also ask the IRS directly for the CSED in writing, or have an experienced tax professional pull and calculate it — the IRS's own figure is sometimes wrong and can be challenged.

Can the IRS extend the 10 years without my consent?

Not by simply choosing to. Statutory tolling happens automatically when you take certain actions — an OIC, bankruptcy, a CDP hearing — but the IRS can't unilaterally add time. Voluntary extensions (Form 900 waivers) require your signature and, since the 1998 reform law, can generally only be requested in connection with an installment agreement. The one big exception: a court judgment on the debt replaces the CSED entirely.

Does bankruptcy really add time to the collection statute?

Yes — the clock stops for the entire automatic stay plus six additional months. A Chapter 7 that runs four months adds roughly ten months to your CSED; a five-year Chapter 13 can add five and a half years. Whether the underlying tax was discharged matters too: payroll trust-fund taxes and recent income taxes typically survive, so the extended clock applies to a debt you still owe.

What happens when the CSED finally expires?

The IRS writes off the balance, and any federal tax lien tied to it self-releases. It cannot legally levy, garnish, or sue on an expired assessment. But nothing 'resets' early — expiration only helps if you actually reach it, and offsets of refunds and payments made before the date are kept. Verify the write-off on your transcript rather than assuming it happened.

Does filing an amended return or an audit restart the 10-year clock?

Not for the original balance — but any additional tax assessed gets its own, new 10-year clock starting from that new assessment date. So a 2019 return audited in 2023 can carry two CSEDs: one for the tax you self-reported in 2020, another for the audit assessment in 2023. Each expires separately, which is why per-assessment dates matter more than tax years.

One caution for anyone comparing federal and state clocks: state statutes are completely different animals. California's FTB, for example, gets 20 years — see California's 20-year collection statute — so never assume an IRS timeline applies to a state balance.

Your next 24 hours

- Pull your account transcript from your IRS online account and write down the date next to code 150 (and any 290/300) for every year you owe — that's where each clock starts.

- Make a dated list of every tolling event in your history: offers, bankruptcies, hearing requests, innocent spouse claims, long stretches abroad. Dates, not guesses.

- Get the calculation verified free. Use the form at claritytaxrelief.com/#consult or call (888) 825-7779 — an experienced tax professional will compute your real CSED and map the cheapest path from here, while interest keeps compounding on the balance either way.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.