IRS Transcripts

How to Read an IRS Account Transcript in 2026: Codes, Balances, and Dates

The short answer: to read an IRS account transcript, check the account balance and "as of" date in the header first, then read the transaction list below it: code 150 is your filed return, negative amounts are credits in your favor, and positive amounts are charges. The "as of" date is a computation date — not a deadline.

You logged in expecting a plain statement of what you owe and got a PDF full of three-digit codes, a −$15,000 that looks alarming until you learn it's good news, and an "as of" date sitting weeks in the future. It reads like it was written for IRS computers — because it was. But once you know the three rules above, the whole document decodes in about ten minutes, and this guide walks you through every section in order.

The image below shows exactly what a real account transcript looks like and where each section sits, so you can hold yours next to it and follow along line by line.

⏱ The ongoing clock: a transcript balance is only accurate through its "as of" date. Interest compounds daily and the failure-to-pay penalty adds 0.5% per month until the balance is resolved — the number you're reading today is the smallest it will ever be.

What an IRS account transcript is — and why you're staring at one

An IRS account transcript is the IRS's line-by-line ledger for one tax year: every assessment, payment, penalty, interest charge, hold, and notice, each recorded as a coded transaction. It is the closest thing to reading the IRS's internal file on you, which is why experienced tax professionals pull transcripts before touching any case.

People usually land on this document for one of five reasons: a refund is stuck, a notice arrived and they want to verify it, a lender asked for one, they're cleaning up back taxes, or they simply want to know what the IRS thinks they owe. Whatever brought you here, the account transcript answers a question no notice fully answers: what has actually happened on your account, in order, with dates and dollar amounts.

Be sure you pulled the right document. A return transcript only echoes the return you filed. A wage and income transcript lists the W-2s and 1099s reported about you — useful for reconstructing old returns; see our guide to IRS wage and income transcripts. If you haven't downloaded yours yet, start with how to get your IRS transcript online, then come back with the account transcript open.

The header: four numbers to read before any codes

The top of an account transcript tells you your entire position in four fields: account balance, accrued interest, accrued penalty, and the "as of" date. Read these before you touch a single transaction code.

- Account balance — what the IRS's system shows you owe for that year. A negative balance means the IRS owes you (an overpayment that hasn't been refunded or applied yet). Zero means the year is settled — as of the computation date.

- Accrued interest / accrued penalty — charges that have built up but may not yet appear as posted transaction lines below. Your real payoff is the account balance plus these accruals, not the balance alone.

- The "as of" date — the date through which those figures were computed. It is not a deadline, not a refund date, and a future "as of" date is normal. The full explanation lives in our guide to the "as of" date on an IRS transcript.

Below the money fields you'll see return information: filing status, adjusted gross income, taxable income, and the tax per your return. These simply restate what you filed and rarely need attention unless they don't match your copy of the return.

The transactions section: how to read each line

Every line in the transactions section has four parts: a three-digit code, a plain-English explanation, a date, and an amount — and the amount's sign is the single most misread thing on the page. Positive amounts are charges against you (tax, penalties, interest). Negative amounts are credits in your favor (withholding, payments, refundable credits).

The date on a line is the date the transaction posted or was assessed — not necessarily the date you acted. A payment you mailed April 12 may post weeks later; what matters legally is that payments are credited effectively as of the date received, and withholding is always credited as of the return due date.

Next to code 150 you'll also see a cycle code — an eight-digit number like 20262205 that tells you which weekly processing batch your return ran in. It matters mostly to refund-watchers; if yours is holding up a refund, our guide to the IRS cycle code meaning decodes it digit by digit.

Read the section top to bottom like a bank statement: the 150 line sets your tax, credit lines subtract from it, penalty and interest lines add to it, and administrative codes (holds, notices, status changes) tell you what the IRS is doing about the result.

IRS account transcript codes: what each one means and what to do

A handful of transaction codes account for nearly everything you'll see on an account transcript. Here's the working list:

| Code | What it means | What to do |

|---|---|---|

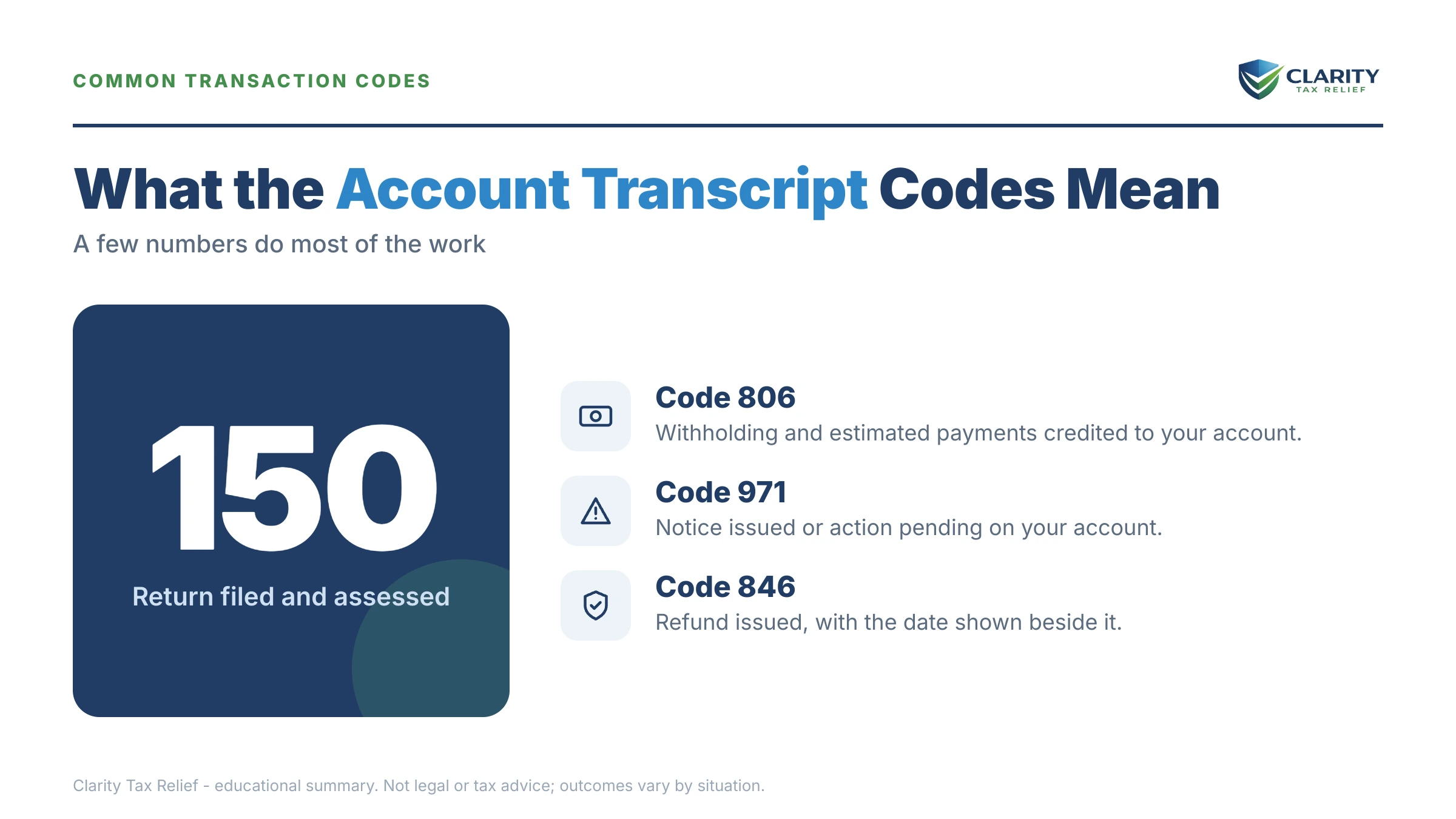

| 150 | Return filed; tax you reported is assessed | Nothing by itself — it's your starting tax, not an extra charge |

| 806 | W-2/1099 withholding credited (negative) | Confirm it matches your actual withholding |

| 660 / 670 | Estimated tax payment / payment received (negative) | Verify every payment you made appears — and to the right year |

| 766 / 768 | Refundable credits posted (negative) | Confirm expected credits (CTC, EITC) landed |

| 276 | Failure-to-pay penalty assessed | Check penalty-relief eligibility before paying blindly |

| 196 | Interest charged on the unpaid balance | Interest can only rarely be removed — resolve the balance to stop it |

| 570 | Hold on the account; refund or processing frozen | Wait for the explaining notice; respond fast when it arrives |

| 971 | Notice issued to you | Match the date to the letter in your mail — this is your paper trail |

| 290 / 291 | Additional tax assessed / tax reduced | Find out why — audits, CP2000s, and amendments post here |

| 420 / 424 | Return pulled for examination / exam requested | Gather records for that year now, before the audit letter lands |

| 480 / 530 | Offer in compromise pending / currently not collectible | Confirms your resolution request is on the system |

| 582 | Federal tax lien indicator | A lien has been filed or is in motion — get advice promptly |

| 846 | Refund issued (negative) | Your refund is on the way as of that date |

Three of these generate the most confusion, and each has its own deep dive: code 150 on an IRS transcript (why a big number there isn't a bill), code 290 on an IRS transcript and its mirror code 291 on an IRS transcript (tax added versus tax removed), and code 420 on an IRS transcript (the audit indicator).

Worked example: decoding a $7,400 balance, line by line

Say you run a small S-corporation with a few employees, and your 2024 account transcript — pulled in July 2026 — shows this. (This is a hypothetical illustration, not a client case.)

| Code | Line description | Amount |

|---|---|---|

| 150 | Tax return filed | $21,500 |

| 806 | W-2 or 1099 withholding | −$15,000 |

| 276 | Penalty for late payment of tax | $455 |

| 196 | Interest charged for late payment | $445 |

| Account balance | $7,400 | |

Here's the story those four lines tell. You reported $21,500 in total tax (150). Your W-2 salary from your own company carried $15,000 of withholding (806) — but pass-through distributions pushed your tax above what payroll withholding covered, leaving $6,500 of tax unpaid. Roughly 14 months later, the failure-to-pay penalty has accrued at 0.5% per month: 14 × 0.5% = 7%, and 7% of $6,500 is $455 (the 276 line). Interest on the unpaid balance adds about $445 (the 196 line). Total: $6,500 + $455 + $445 = $7,400 — and it grows every month. You can estimate how fast your own penalties and interest are compounding with our IRS penalty and interest calculator.

Because the balance is under $10,000, this reader is likely eligible for a guaranteed installment agreement — full payment within 3 years, roughly $7,400 ÷ 36 ≈ $206 per month before continuing interest, set up online without financial disclosure.

One payroll-specific caution: this 1040 transcript shows only your personal account. Your company's 941 payroll balances live on separate business transcripts, pulled quarter by quarter under the EIN — a clean personal transcript says nothing about them. If the business is behind on deposits, start with our guide to 941 back taxes, because payroll debt escalates on a different and harsher track.

What happens if you ignore a balance your transcript shows

A balance on your account transcript is the front end of the IRS's automated collection sequence, and the transcript itself will record each escalation as a new 971 line. Ignored, the stages run in this order:

- The balance posts — your 150/276/196 lines, exactly like the example above. No enforcement yet, but daily interest has started.

- CP14 first bill — typically about 21 days to pay before the next notice queues up (10 business days when the balance is $100,000 or more). Each notice appears on the transcript as a code 971.

- CP501 / CP503 reminders — still bills, but the balance is compounding monthly while they cycle.

- CP504 intent to levy — the IRS can now seize your state tax refund under IRC §6331(d), and a federal tax lien (code 582 on the transcript) becomes realistic.

- LT11 / Letter 1058 final notice — a 30-day clock with Collection Due Process appeal rights (Form 12153). After it runs, bank levies (21-day hold before funds leave) and continuous wage levies are on the table.

In 2026 this sequence runs with almost no human involvement: the IRS workforce was cut roughly 27% in 2025, but the notice and levy systems are automated and never paused. And if combined assessed balances ever pass $66,000, passport certification enters the picture too. The upside of reading your transcript is that you can see exactly which stage you're at — and act while the cheap options are still open.

Not sure what your transcript is telling you?

Send it to us. An experienced tax professional will decode every line, tell you exactly where your account stands in the collection sequence, and map your options — free and confidential, before another month of penalties posts.

Your options when the transcript shows you owe

Every IRS balance has a resolution path, and which one fits depends on the amount and your finances — the full playbook is in our guide to how to settle tax debt yourself. Here's the field of options at a glance:

| Option | Upfront cost | Timeline | Watch out for |

|---|---|---|---|

| Pay in full | $0 | Same day online | Nothing — cheapest path; accruals stop when payment posts |

| Short-term plan (up to 180 days) | $0 setup | Minutes to set up online | Interest + 0.5%/month penalty continue until paid |

| Guaranteed installment agreement (≤ $10,000) | Setup fee (reduced online) | Approved online; pay within 3 years | Must stay current on filing and payments |

| Streamlined installment agreement (≤ $50,000) | Setup fee (reduced online; low-income waivers) | Up to 72 months, online approval | Missing a payment or a new balance can default it |

| Currently Not Collectible | $0, but requires financial disclosure (Form 433-F) | Weeks to months | Balance keeps growing; the IRS reviews it periodically |

| Offer in Compromise | $205 fee + 20% down on lump-sum offers (both waived with low-income certification) | Months to 2 years; auto-accepted if undecided at 2 years, with narrow exceptions — a returned or rejected offer stops the clock, and time during court disputes does not count | Strict means test — roughly 1 in 5 offers accepted in FY2024 |

| Penalty abatement | $0 | Phone call or letter; weeks | Removes penalties only — not the tax or most interest |

If your transcript shows a 276 line and your prior three years were clean, look at first-time penalty abatement before paying the penalty — and note that starting summer 2026, the IRS's new Automatic Exemption from Penalty (AEP) begins applying qualifying relief automatically, no request needed. Current plan mechanics and fees are on the IRS's payment plans and installment agreements page.

How to read an IRS account transcript, step by step

- Pull the right transcript: download the "account transcript" for the exact tax year in question from your IRS online account — not the return transcript or wage and income transcript.

- Read the header first: note the account balance, accrued interest, accrued penalty, and the "as of" date those figures run through — that is your true position in one glance.

- Find code 150: that line is your filed return and the total tax assessed on it — the starting point every other line adjusts up or down.

- Subtract the negative lines: withholding (806), estimated payments (660), and other payments (670) reduce what you owe — confirm every payment you actually made appears here.

- Flag the action codes: circle any 570 hold, 971 notice, 276 or 196 penalty and interest charge, and any 420, 480, 520, 530, or 582 line — these change what you should do next.

- Act on the bottom line: if a balance remains, choose a resolution path before the next monthly penalty posts; if the IRS's numbers are wrong, dispute them with documentation.

If you hit a wall pulling the document itself, the IRS's official Get Transcript page covers online, mail, and phone options.

When you can handle this yourself — and when to get help

Most transcript reading is genuinely DIY. If the header balance matches what you expected, the codes are the ordinary ones (150, 806, 971, 846), and any balance is under about $10,000 with the income to pay it within a few years, you can set up a payment plan online in an evening and never need to hire anyone.

Experienced help changes the outcome in specific situations: a 582 lien line or an LT11-stage 971 (enforcement is in motion), 290 assessments you don't recognize or disagree with, multiple years with balances or "N/A" years suggesting unfiled returns, business payroll transcripts alongside personal ones, or a balance large enough that Offer in Compromise math is worth running properly. In those cases the order you fix things — returns first, then penalties, then the balance — often determines what you ultimately pay.

Terms on your transcript, decoded

- Transaction code (TC): the three-digit label the IRS's master file assigns to every event on your account.

- Assessment: the formal recording of a tax debt — the legal step that starts collection (and the 10-year collection clock).

- "As of" date: the date through which interest and penalties in the header were computed; a moving target, not a deadline.

- Cycle code: the eight-digit stamp showing which weekly IRS processing batch handled your return.

- Accrued vs. assessed: assessed amounts have posted as transaction lines; accrued amounts are building daily but not yet posted — your payoff includes both.

- CSED: the Collection Statute Expiration Date — generally 10 years from each assessment, pausable by appeals, offers, and bankruptcy; see how long the IRS can collect back taxes.

- Freeze code: a code (like 570 or 810) that stops refunds or processing until a condition clears.

If a transcript problem is stalling a refund you urgently need and normal channels aren't moving, the independent Taxpayer Advocate Service can intervene in hardship cases.

Account transcript questions, answered

What do the negative numbers on my IRS account transcript mean?

Negative amounts are credits — money in your favor, such as withholding (code 806), estimated payments, or refundable credits. Positive amounts are charges against you: tax assessed, penalties, and interest. This convention trips up almost everyone: a line reading −$15,000 means the IRS credited you $15,000, not that you owe it. Add the positives, subtract the negatives, and you should land near the account balance in the header.

What does the "as of" date on an IRS account transcript mean?

It is the date through which the IRS computed the interest and penalty figures shown — not a deadline, and not the date anything is scheduled to happen to you. The balance is only accurate through that date; interest compounds daily afterward, so a payoff a month later will be higher. A future "as of" date is normal and usually just means the system has scheduled a recalculation of your account.

What is the difference between an account transcript and a return transcript?

A return transcript shows the line items from the return you filed — and nothing that happened afterward. An account transcript shows everything that happened to the account: assessments, payments, penalties, interest, holds, and notices, each as a coded line. If you are checking a balance, a refund delay, or collection activity, the account transcript is the one you want. A record of account combines both for recent years.

Does code 150 on my account transcript mean I owe money?

Not by itself. Code 150 means your return was filed and the tax you reported was assessed — the amount next to it is your total tax liability before any withholding or payments are subtracted. You only owe if the positive lines exceed the negative credit lines. Many people see 150 with a large figure and panic, when the withholding line right below it covers most of the amount.

Why doesn't my account transcript balance match my IRS notice?

Usually timing. The transcript header shows the balance as of its computation date, while notices are printed on different dates — and interest accrues daily and the failure-to-pay penalty monthly in between. Also check the accrued interest and accrued penalty lines: some transcript balances exclude accruals that have not yet been formally assessed. If the gap is large or a payment you made is missing entirely, investigate rather than assume.

Can my IRS account transcript tell me if I'm being audited?

Often, yes — before any letter arrives. Code 424 means an examination request; code 420 means your return was pulled for audit. Code 922 signals an underreporter review (the CP2000 process), which is document matching rather than a full audit. If you see 420 or 424, start gathering your records for that year now; the notice explaining what the IRS wants typically follows as a code 971 line.

How many years of account transcripts can I get?

Through your IRS online account you can generally view account transcripts for the current tax year and up to nine prior years. Older years usually require Form 4506-T by mail, and very old years may only be available as literal account printouts requested by phone or through a tax professional. If a year shows N/A, the IRS may have no return on file for it — a separate problem worth fixing quickly.

Your next 24 hours

- Find three things on your transcript: the account balance, the "as of" date, and any 570, 971, 420, or 582 lines. Those four data points tell you exactly where your account stands.

- Gather your side of the ledger: your copy of the return for that year, proof of every payment you made, and any IRS letters you've received — you'll need them whether you pay, set up a plan, or dispute.

- Get a free transcript review: if the lines don't add up, a balance is growing, or enforcement codes are posting, send the transcript through the 2-minute form or call (888) 825-7779. Penalties and interest accrue monthly — reading the transcript today and acting on it are two different wins.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.