IRS Payment Plans

Guaranteed Installment Agreement: The IRS Payment Plan It Must Accept in 2026

The short answer: a guaranteed installment agreement is a payment plan the IRS must accept by law — IRC §6159(c) — if you owe $10,000 or less in tax, have filed and paid on time for the past five years, haven't used an installment agreement in that window, and agree to pay the full balance within three years.

You've seen the balance — maybe on a CP14, maybe on your IRS online account — and you're trying to figure out whether a fixed income can absorb it without wrecking the budget you've built your retirement around. Here's the part almost nobody tells you: for tax debts of $10,000 or less, you don't have to hope the IRS says yes to a guaranteed installment agreement. Congress already said yes for them.

Two details in that sentence do most of the work, and they're worth pinning down before anything else. First, the $10,000 threshold counts tax only — penalties and interest are excluded, so a total balance a little over $10,000 can still qualify. Second, the guarantee is real but conditional: five specific tests, all of which are checkable in about ten minutes. The image below shows how the pieces of this program fit together at a glance.

⏱ The clock on this one isn't a letter date — it's accrual. The failure-to-pay penalty adds 0.5% of the unpaid tax every month (cut to 0.25% once an installment agreement is in effect), and interest compounds daily on top. Every month before you set up the plan costs real money; every month after costs half as much in penalty.

Why the guaranteed installment agreement exists — and the five conditions

The guaranteed installment agreement is the only IRS payment plan written directly into federal law: IRC §6159(c) says the IRS shall enter the agreement when five conditions are met. Every other plan — streamlined, non-streamlined, partial-pay — is administrative policy the IRS could tighten tomorrow. This one is a statutory right.

Congress created it in 1998 for exactly the situation most people with a small, first-time balance are in: an ordinary taxpayer with a clean history hit one bad year — an IRA withdrawal with no withholding, a pension that started mid-year, a side income surprise — and shouldn't have to open their entire financial life to the government to pay it back.

Here are the five conditions, in plain English:

| Condition | What it means | Common tripwire |

|---|---|---|

| Tax of $10,000 or less | Only the tax counts — penalties and interest are excluded from the test | Assuming a $10,800 total balance disqualifies you when the tax portion is $9,600 |

| Clean five-year filing and payment history | All returns filed on time and all tax paid for the prior five years | One late-filed return inside the window — even one you eventually paid |

| No installment agreement in the prior five years | You haven't used any IRS payment plan in that window | A short streamlined plan from a few years back that you forgot about |

| Full payment within 3 years | Your monthly payment must clear the whole balance in 36 months or less | Proposing a payment too small to finish inside the window |

| Stay compliant during the agreement | File and pay on time every year while the plan runs | Next April's new balance-due return, which defaults the plan |

Three nuances matter more than the ads ever mention. The program covers individual income tax only — business and payroll balances don't qualify. On a jointly filed debt, the five-year test applies to both spouses; one spouse's old payment plan sinks the guarantee for the couple. And the statute technically requires that you're financially unable to pay in full immediately — though for a qualifying balance, the IRS doesn't ask you to prove it with a financial statement.

That last point is the practical prize: no Form 433-F, no financial disclosure at all. The IRS never sees your bank balances, your home equity, or your retirement accounts. For a retiree with savings you'd rather not put on the government's radar, that alone can make this the right structure even when you could technically scrape together full payment.

One honest caution about the name. Tax-relief marketing loves the word "guaranteed," and some ads borrow it to imply everyone qualifies for everything. The guarantee here is narrow and specific: if you pass all five tests, the IRS must say yes. It is not a promise that you qualify — the five-year compliance test alone screens out most people with repeat balances.

What happens if you ignore the balance instead

A sub-$10,000 balance you ignore travels the same automated collection track as a $200,000 one — the machine doesn't scale its aggression down for small debts. The sequence runs in a fixed order, and each stage removes options the previous stage still offered:

- CP14 — the first bill. You typically have about 21 days from the notice date before the system escalates (10 business days when the balance is $100,000 or more). Nothing is being seized yet; this is the cheapest moment to act.

- CP501 / CP503 — reminders. Still just bills, but the failure-to-pay penalty and daily interest have been compounding the whole time.

- CP504 — intent to levy your state refund. The IRS can now take your state tax refund, and a federal tax lien becomes a live possibility — the lien protection a guaranteed agreement would have preserved is now at risk.

- LT11 / Letter 1058 — final notice of intent to levy. A 30-day clock starts, along with your Collection Due Process rights. After it runs, bank levies (with a 21-day hold before funds leave) and wage levies are on the table.

- Levy on federal payments. For retirees this is the stage that hurts most: through the Federal Payment Levy Program, the IRS can take up to 15% of every Social Security check — continuously, until the debt is resolved. Our guide to whether the IRS can garnish Social Security covers exactly how that works.

The bitter irony: someone who qualifies for a guaranteed installment agreement could have stopped this entire sequence with one online session. An active agreement halts levy action — including FPLP — for as long as it stays in good standing. In 2026, with IRS staffing down roughly 27% but the automated notice stream fully intact, the machine escalates on schedule whether or not a human ever reviews your file.

Owe under $10,000 and not sure you pass all five tests?

Send us the notice or your account balance. An experienced tax professional will check your compliance history, confirm whether the guaranteed agreement — or something better — fits, and map the exact payment before another month of penalties posts. Free and confidential.

Your options compared: guaranteed, streamlined, short-term, and hardship

The guaranteed installment agreement is one of four realistic structures for a balance in this range, and the right one depends on how fast you can pay and whether paying at all creates hardship. The full setup mechanics for each live in our walkthrough of the IRS payment plan online process — here's how they stack up:

| Option | Balance limit | Max term | Financial disclosure? |

|---|---|---|---|

| Short-term payment plan | Broad (individuals) | 180 days | No — and $0 setup fee |

| Guaranteed installment agreement | ≤ $10,000 in tax | 36 months | No — acceptance required by law |

| Streamlined installment agreement | ≤ $25,000 (≤ $50,000 with direct debit) | 72 months | No — but approval is discretionary |

| Currently Not Collectible | Hardship-based, any amount | Until finances improve | Yes — Form 433-F hardship math |

How to choose between them, honestly:

- If you can clear the balance in six months — say, a CD is maturing — the short-term plan beats everything: $0 setup fee, no monthly commitment, done. It's the cheapest structure the IRS offers.

- If you need one to three years, the guaranteed agreement is your lane. Statutory acceptance, no financials, and the IRS's general practice of not filing a lien on these plans.

- If 36 months is too tight, a streamlined installment agreement stretches the same sub-$10,000 debt over up to 72 months with no financial disclosure — a smaller payment in exchange for more total interest.

- If any payment would mean skipping medicine or utilities, a payment plan is the wrong tool. Compare a payment plan vs currently not collectible status, and see our guide to IRS hardship on Social Security — CNC pauses collection entirely while your situation stays tight.

Two add-ons worth stacking on top of whichever plan you pick. If your five-year history is clean enough to qualify for the guaranteed agreement, you very likely also qualify for first-time penalty abatement — the same clean-three-year test removes the failure-to-pay penalty already on your account. (Starting in summer 2026, the IRS's new Automatic Exemption from Penalty applies some of this relief automatically, with no request needed.) And skip the Offer in Compromise sales pitch at this balance level: an OIC costs $205 to apply, is means-tested against everything you own, and for a sub-$10,000 debt with any retirement savings behind it, the math almost never works.

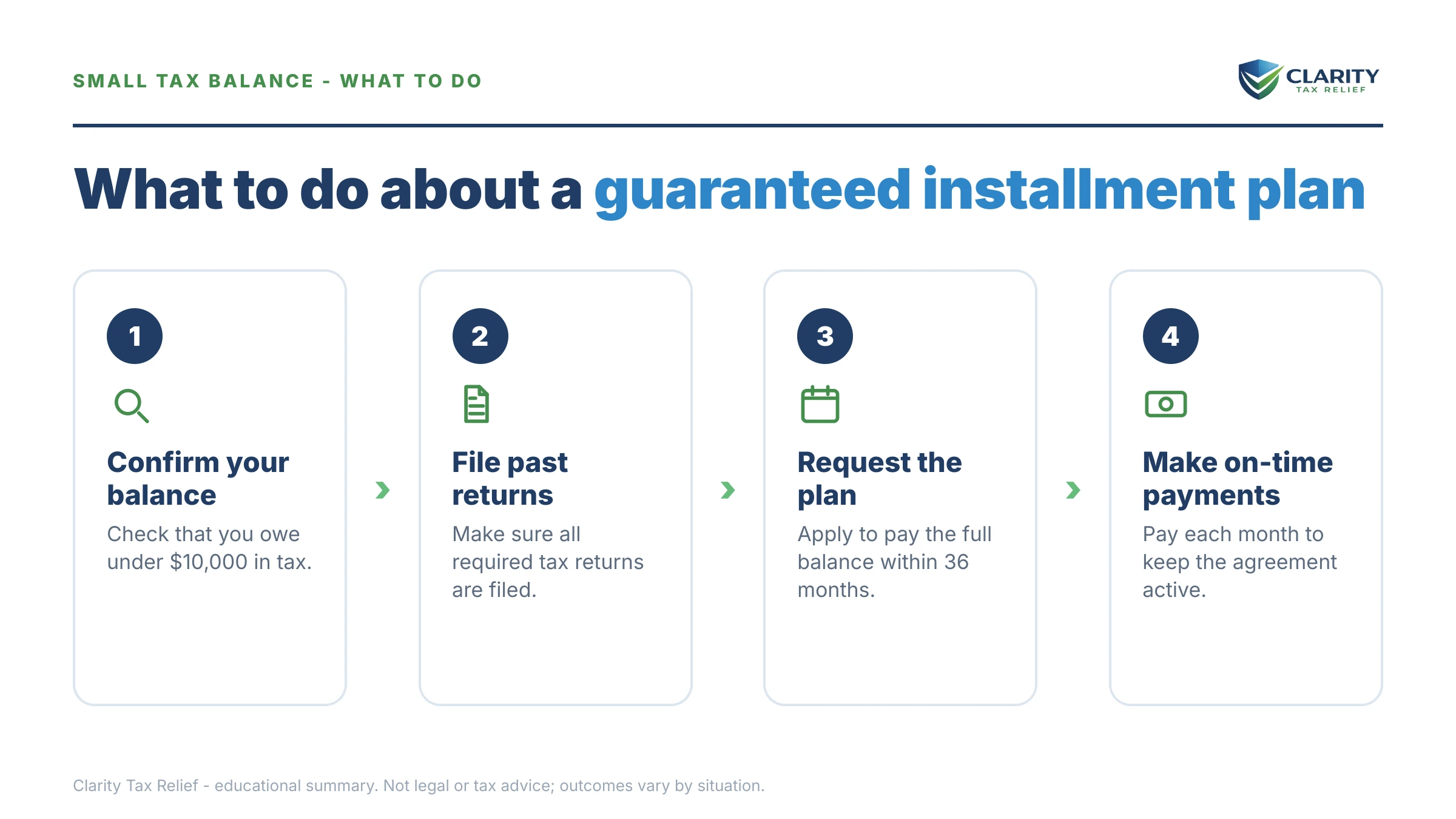

How to set up a guaranteed installment agreement, step by step

A qualifying taxpayer can have a guaranteed installment agreement in place in a single sitting. Here's the sequence:

- Pull your exact balance. Log in to your IRS online account and separate the tax from penalties and interest — the $10,000 test counts tax only.

- Verify your five-year history. Confirm all returns were filed and paid on time and that you haven't had an installment agreement in the past five years — on a joint balance, that goes for both spouses.

- Set a payment that clears the debt within 36 months. Divide your total balance by 36, then round up so accruing interest doesn't push you past the three-year line.

- Apply online, by Form 9465, or by phone. The IRS Online Payment Agreement tool is the fastest route and carries the lowest setup fee.

- Choose direct debit. Automatic bank payments cost less to set up and nearly eliminate accidental default from a forgotten check.

- Stay compliant while the plan runs. File every return on time and don't create a new balance — a fresh unpaid debt defaults the agreement.

On step 4: if you'd rather apply on paper, our Form 9465 walkthrough shows the line that lets you name your own payment amount and due date. On step 5, the fee difference and the default-proofing are both covered in our comparison of the direct debit installment agreement versus mailing checks. Setup fees vary by application method and are reduced, waived, or reimbursed for low-income taxpayers (income at or below 250% of the federal poverty level) — the exact tiers are in our guide to the IRS payment plan setup fee.

The math on a fixed income: a worked example

A guaranteed installment agreement's payment is simple arithmetic: total balance, divided by up to 36 months, rounded up for interest. Here's what that looks like in a clearly hypothetical case.

Say you're 68, retired, living on Social Security plus a small pension — about $2,900 a month total. Last year you pulled money from a traditional IRA to replace a roof, no withholding came out, and the return you filed in April shows $9,400 in tax due. By the time you deal with it, penalties and interest have pushed the account balance to roughly $10,100.

- Do you qualify? Yes — the test looks at the $9,400 of tax, not the $10,100 total. Clean filing history, no prior plan: all five conditions met, and the IRS must accept.

- The base payment: $10,100 ÷ 36 = about $281 a month. Because interest keeps accruing on the shrinking balance, budgeting around $305–$310 keeps you comfortably inside the three-year window.

- The penalty drop: before the agreement, the failure-to-pay penalty on $9,400 runs about $47 a month (0.5%). Once the plan is in effect it falls to roughly $23.50 (0.25%) — the agreement literally cuts the penalty bleed in half from day one.

- The faster option: stretch to $425 a month and you're done in about 24 months, saving a year of interest and penalty. There's no prepayment penalty, ever.

You can estimate your own accrual — what waiting another three or six months would add — with our IRS Penalty & Interest Calculator, and the current quarterly rate itself is tracked in our guide to the installment agreement interest rate.

| Total balance | Base payment (÷ 36) | Suggested monthly budget |

|---|---|---|

| $3,000 | $84 | ~$95 |

| $6,000 | $167 | ~$185 |

| $10,000 | $278 | ~$310 |

Now flip the scenario: suppose the withdrawal was much larger and the balance is $48,300 instead. The guaranteed agreement is off the table — but you're not stuck. At $48,300 you're still under the $50,000 direct-debit ceiling for a streamlined agreement, which spreads the debt over up to 72 months: $48,300 ÷ 72 ≈ $671 a month before interest, with no financial statement required. The rules and tradeoffs at that level are covered in our guide to an IRS payment plan over $50,000.

After approval: what the agreement looks like month to month

An approved guaranteed installment agreement runs quietly in the background — as long as three things stay true. Here's the rhythm of the plan and the two mail items to know about:

- CP521 reminders. If you pay by check, the IRS mails a CP521 notice before each payment is due. On direct debit, the money simply moves — one more reason debit plans rarely default.

- Your tax refunds get kept. Every federal refund you're owed while the plan runs is applied to the balance automatically — it counts as extra principal, not as your monthly payment. Details in will the IRS take my refund on a payment plan.

- No lien, generally. The IRS's standing practice is not to file a Notice of Federal Tax Lien on guaranteed agreements — your credit applications, refinance, and public record stay clean while you pay.

- Miss a payment? One slip usually triggers a warning, not a termination — there's a cure window, explained in our guide to a missed IRS payment plan payment. If the IRS moves to terminate, it sends a CP523 notice first; respond inside that window and the plan is typically saved. Ignore it and levy powers — including the 15% Social Security levy — come back.

- The 10-year clock keeps running. Your payments chip at a balance that also has a legal expiration date (the CSED, ten years from assessment) — though a 36-month plan will finish long before that matters.

The default trigger people don't see coming isn't a missed payment — it's next year's return. File on time with a new balance you can't pay, and the agreement defaults even if you never missed a monthly payment. If a new balance is forming (say, another withholding-free IRA withdrawal), fix the withholding now: Form W-4V sets voluntary withholding on Social Security, and your IRA custodian can withhold on distributions.

When you can handle this yourself — and when to get help

Honest answer: the guaranteed installment agreement is the most DIY-friendly program the IRS runs. If your balance is under $10,000 in tax, your last five years are clean, and you agree with the amount, you can set this up yourself online in well under an hour — you do not need a tax relief firm for that, and anyone charging you four figures to do it is selling you your own statutory right.

Experienced help changes the outcome in a narrower set of situations:

- You dispute the balance. Locking a wrong number into a 36-month plan is the worst order of operations — the amount should be challenged or amended first.

- There are unfiled years in the window. An unfiled return kills the five-year test and can hide additional balances. The filing sequence determines which programs stay open.

- Multiple years of debt push the tax over $10,000. The choice between streamlined terms, penalty abatement first, or a hardship route becomes real strategy.

- A levy is already in motion — a CP504 or LT11 has arrived, or Social Security is already being clipped. Deadlines and appeal rights now interact with the plan request.

- Paying anything would break your budget. If the honest answer is that $280 a month means skipped prescriptions, CNC — not a payment plan — is likely the right ask, and that case has to be documented properly.

If any of those describes you, have an experienced tax professional review the file free — the two-minute form or (888) 825-7779 — before you lock in a plan, because the order you fix things in changes what you end up paying.

Terms on your plan, decoded

- IRC §6159(c): the statute that makes acceptance mandatory — the "guaranteed" in the program's name.

- Form 9465: the paper request for an installment agreement, used when you'd rather not apply online.

- Form 433-F: the financial statement the IRS demands for bigger or hardship cases — and that guaranteed applicants get to skip entirely.

- CP521: the routine monthly payment reminder — normal mail, not a warning.

- CP523: the default warning — notice of intent to terminate your agreement. This one has a deadline; act on it.

- CSED: the Collection Statute Expiration Date — the 10-year legal limit on collecting an assessed tax, which certain events can pause.

Guaranteed installment agreement questions, answered

Does the IRS have to accept a guaranteed installment agreement?

Yes — if you meet all five conditions, acceptance is a legal right under IRC §6159(c), not a discretionary favor. The IRS cannot reject you for owing "too much" relative to income and cannot demand a financial statement. The word "guaranteed" refers to this statutory obligation, not to a promise that every applicant qualifies; the five-year compliance test screens out most repeat balances.

Does the $10,000 limit include penalties and interest?

No. The statute counts only the tax itself — penalties, interest, and additions to tax are excluded from the $10,000 test. So a total account balance of $11,200 built on $9,500 of tax still qualifies. Check your IRS online account or account transcript to see the breakdown, because the notice you received shows only the combined total.

What is the difference between a guaranteed and a streamlined installment agreement?

The guaranteed agreement is a statutory right for tax debts of $10,000 or less, capped at 36 months. The streamlined agreement is an IRS administrative program for balances up to $25,000 — or $50,000 with direct debit — with terms up to 72 months. Streamlined approval is nearly automatic but still discretionary; a guaranteed installment agreement must be accepted by law when you meet all five conditions.

Will the IRS file a tax lien if I set up a guaranteed installment agreement?

As a matter of standing practice, the IRS generally does not file a Notice of Federal Tax Lien on guaranteed installment agreements. That protects your ability to refinance, sell property, or pass a background check while you pay. If you default and the agreement terminates, lien filing goes back on the table, so keeping the plan current preserves the protection.

Can the IRS take my Social Security while I'm on a payment plan?

Not while the agreement is in good standing — an active installment agreement stops levy action, including the Federal Payment Levy Program's 15% cut of Social Security benefits. If you never set up a plan, the IRS can take up to 15% of each monthly check through FPLP. That protection ends if the agreement defaults and isn't cured or reinstated.

How much does it cost to set up a guaranteed installment agreement?

The setup fee depends on how you apply: online with direct debit is the cheapest route, and applying by phone or mail costs more. Low-income taxpayers — income at or below 250% of the federal poverty level — can have the fee reduced, waived, or reimbursed. After setup, your only ongoing costs are interest and the reduced 0.25% monthly failure-to-pay penalty.

What happens if I miss a payment on a guaranteed installment agreement?

One missed payment doesn't instantly kill the plan — the IRS typically sends a CP523 notice of intent to terminate first, and you get a window to catch up or reinstate before enforcement resumes. Don't ignore that notice: once the agreement actually terminates, levy powers return and the "no lien" practice no longer protects you.

Do penalties and interest stop on a guaranteed installment agreement?

No — interest keeps compounding daily and the failure-to-pay penalty continues, though it drops from 0.5% to 0.25% per month once the agreement is in effect (for returns that were filed on time). That's why paying faster than the 36-month maximum always saves money. There is no prepayment penalty for finishing early.

Can I pay off a guaranteed installment agreement early?

Yes, anytime, with no prepayment penalty — and every month you shave off the schedule stops that month's interest and penalty accrual. You can also make extra payments on top of the fixed monthly amount whenever cash appears — an inheritance, a CD maturing, an RMD you don't need. The fixed payment is a floor, never a ceiling.

Do both spouses need a clean history for a joint tax debt?

Yes. On a jointly filed balance, the five-year compliance test — returns filed on time, tax paid, no installment agreement — applies to both spouses. If your spouse had a payment plan three years ago, the joint balance won't qualify for the guaranteed agreement, though a streamlined installment agreement will usually cover the same debt on similar terms.

Your next 24 hours

- Pull the two numbers that decide everything. Log in to your IRS online account (or grab your most recent notice) and write down the tax amount separately from the penalties and interest. If the tax is $10,000 or less, the guaranteed agreement is likely on the table.

- Gather your compliance picture. Your last five years of returns — or just the filing dates — plus your monthly income and the payment you can genuinely sustain for 36 months.

- Get it confirmed free. An experienced tax professional can verify all five conditions, check whether penalty abatement shrinks the balance first, and set the plan in motion — start with the 2-minute form or call (888) 825-7779. Interest and the failure-to-pay penalty post again every month you wait; the plan cuts that penalty in half the day it's approved.

Primary sources: the IRS's official payment plans and installment agreements page, the About Form 9465 page, and — if the IRS mishandles your agreement request — the Taxpayer Advocate Service.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.