IRS Collections

Can the IRS Garnish Social Security? Yes — Here's the 15% Levy Rule (2026)

The short answer: yes — the IRS can garnish Social Security. Through the Federal Payment Levy Program, it takes up to 15% of your monthly retirement or SSDI benefit, every month, until the debt is resolved. SSI is exempt. You get a written warning first — typically a CP91 — with roughly 30 days to act.

Maybe your deposit already came in short this month, or maybe a letter just told you it's about to. Either way, discovering that the government can reach the benefit you spent forty years earning is a jolt — especially when that check is most of what you and your spouse live on. Here's the honest picture: the levy is real, it's capped, it's announced in advance, and every one of the paths that stops it is still open to you.

The warning letter that matters most here is the CP91 — the image below shows exactly what that notice looks like and where to find the date that controls your deadline.

⏱ Your deadline: the response date printed on your CP91 or final levy notice — typically 30 days from the notice date. If that window passes without a payment arrangement or hardship request, the Federal Payment Levy Program can begin taking 15% of every check until the debt is resolved.

How the IRS garnishes Social Security: the Federal Payment Levy Program

The IRS takes Social Security through an automated system called the Federal Payment Levy Program (FPLP), which levies up to 15% of each monthly benefit. There's no IRS employee deciding your case — the program electronically matches tax debts against federal payment files at the Treasury and diverts the money before it ever reaches your bank account.

Two features make this levy different from an ordinary wage garnishment. First, it's continuous: once it attaches, it takes 15% of every check until the debt is paid, an arrangement is in place, or the collection statute expires. Second, there's no dollar floor. When the IRS garnishes a paycheck, a formula protects an exempt amount of wages — that's the math covered in how much can the IRS garnish from my paycheck. Under FPLP, the 15% comes out whether or not the remaining 85% covers your rent.

The legal footing matters too. Federal law shields Social Security from private creditors, but the tax code carves out an exception for the IRS — so the "Social Security can't be garnished" rule you may have heard applies to credit card companies, not to federal tax debt.

Two guardrails work in your favor. The IRS runs a low-income screen that filters some taxpayers with poverty-level income out of FPLP — helpful, but not something to count on, because it doesn't catch every account. And in 2026, with the IRS workforce down roughly 27% after the 2025 cuts, it's harder than ever to reach a human to fix a levy after it starts — while the automated program that issues them never paused. Acting inside the notice window is worth far more than it used to be.

One more distinction: in rarer cases, a revenue officer assigned to a larger or older debt can issue a manual paper levy on Social Security. That version isn't capped at 15%, but it must leave you an exempt amount based on your filing status and dependents. For most retirees with a garden-variety balance, the automated 15% FPLP levy is what actually happens.

Which Social Security benefits the IRS can and can't take

The FPLP reaches retirement and disability insurance benefits, but it does not touch SSI. Here's the breakdown most readers are searching for:

- Retirement benefits — yes, up to 15% per month.

- SSDI (Social Security Disability Insurance) — yes, treated the same as retirement benefits. If disability is your situation, the full picture — including why many SSDI recipients qualify for hardship relief — is in can the IRS garnish SSDI.

- Survivor benefits — generally reachable the same way, since they run through the same payment system.

- SSI (Supplemental Security Income) — no. SSI is a needs-based program and is excluded from FPLP entirely.

- Benefits paid to children and lump-sum death benefits — excluded from the automated levy.

For a married couple, each spouse's benefit is its own federal payment. On a joint tax debt, both checks are exposed — the levy isn't limited to whichever spouse earned the income that created the balance. That's exactly the scenario in the worked example below.

And Social Security isn't the only income stream at risk while a balance sits unresolved. If you or your spouse still does contract or consulting work, the IRS can separately levy that pay — see can the IRS garnish 1099 income. Tax refunds get offset automatically throughout.

What happens if you ignore the warnings: the road to a Social Security levy

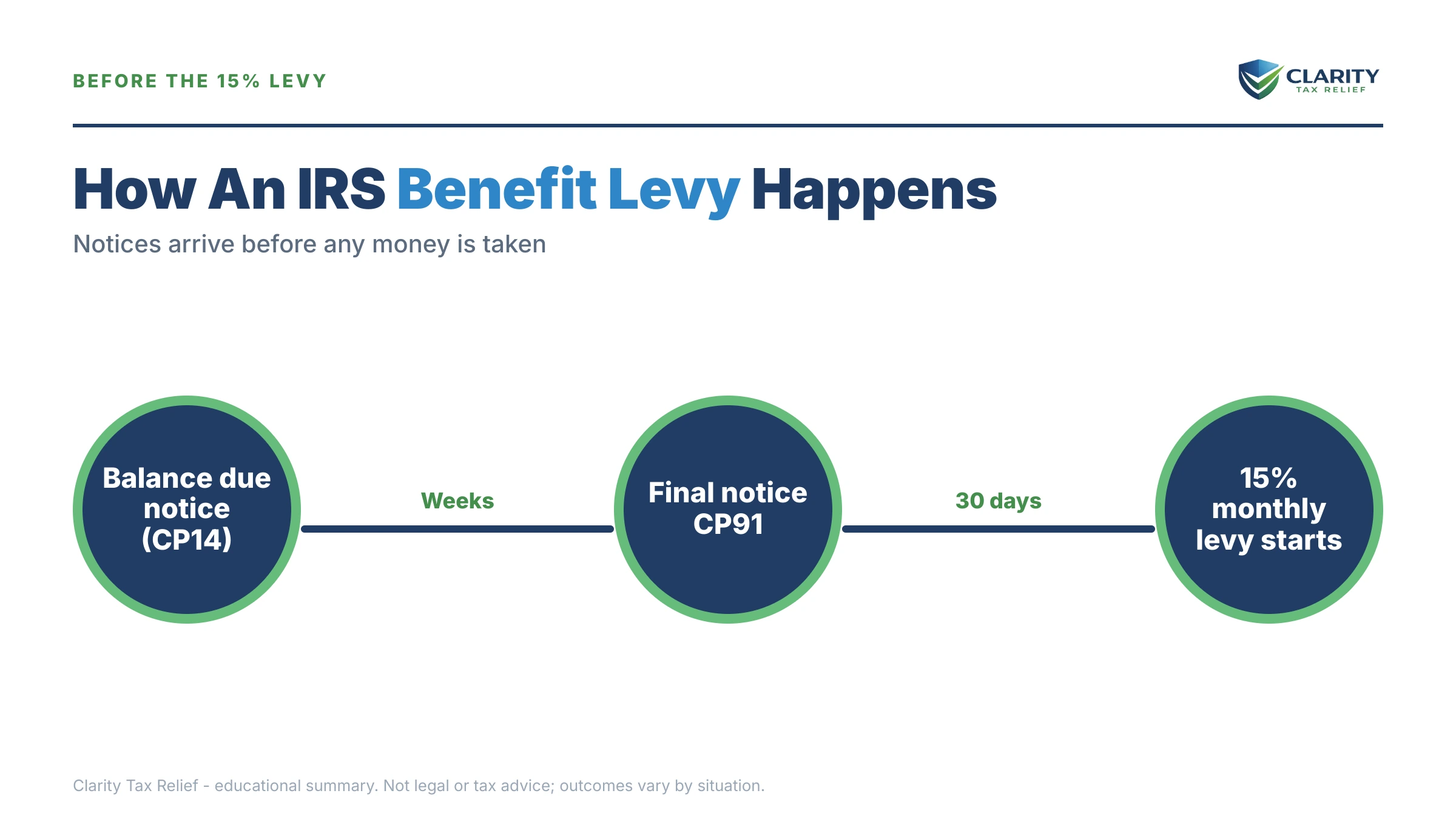

The IRS never takes Social Security by surprise — a fixed sequence of notices comes first, and each one you ignore removes an option. The sequence is automated, so it advances on schedule whether or not a human ever reviews your file:

- CP14 — the first bill. You have about 21 days before the system escalates. No enforcement yet; this is the cheapest moment to act.

- CP501 / CP503 — reminder notices. Still just bills, but interest and the 0.5%-per-month failure-to-pay penalty keep compounding.

- CP504 — Notice of Intent to Levy. The IRS can now seize your state tax refund, and a federal tax lien becomes a live possibility.

- CP90 / LT11 — final notice of intent to levy, opening a 30-day window to request a Collection Due Process hearing. For Social Security specifically, the IRS typically sends a CP91 Social Security levy notice announcing the 15% levy.

- The FPLP levy begins — 15% of every benefit check, continuously, until the debt is paid, an arrangement is accepted, a hardship release is granted, or the 10-year collection statute runs out.

Here's the same sequence as a reference table — including the specific right each deadline protects:

| Notice | What it means | Response window | Right you lose if it passes |

|---|---|---|---|

| CP14 | First bill for the balance | ~21 days from notice date | Resolving before penalties stack and notices escalate |

| CP504 | Intent to levy your state refund | Date printed on the notice | Keeping your state tax refund |

| CP90 / LT11 | Final notice of intent to levy | 30 days | Collection Due Process hearing (Form 12153) before levy |

| CP91 | Intent to take up to 15% of Social Security | Typically 30 days — check your notice | Stopping the levy before your check shrinks |

| Levy active | FPLP takes 15% of every benefit payment | Ongoing until resolved | Release now requires an arrangement or hardship showing |

Got a CP91 — or already seeing a smaller deposit?

Send us the notice. An experienced tax professional will confirm where you are in the sequence and which option protects your benefit — free, before the 30-day window on your notice closes.

How to stop the IRS from garnishing your Social Security: every option

Any accepted resolution — a payment plan, hardship status, or a settlement — generally keeps the 15% levy from starting, or gets it released once it has. The general playbook for releasing an IRS levy lives in our guide to how to stop IRS wage garnishment; what follows is how each option actually plays out on a fixed income:

- Short-term payment plan — up to 180 days to pay in full, with $0 setup fee. Right for a balance you can clear with savings or a one-time source of funds.

- Installment agreement — a monthly plan. Balances of $25,000 or less qualify for a streamlined agreement without detailed financial disclosure (up to $50,000 with direct debit), spread over as many as 72 months. Interest and penalties keep accruing, but the levy is generally released once the agreement is in place — and you pick a payment you can live with instead of losing a flat 15%.

- Currently Not Collectible status — if the IRS's own allowable-expense math shows your necessary living costs meet or exceed your income, collection is paused entirely. No monthly payment, levy released, and the 10-year collection clock keeps running. For retirees living check to check, this is often the honest answer — the fixed-income version is covered in IRS hardship while on Social Security.

- Economic-hardship levy release — if a levy is already running and it prevents you from paying basic living expenses, the IRS must release it under IRC §6343. This is the fastest route when medication, housing, or utilities are on the line — details in levy causing hardship.

- Offer in Compromise — settling for less than the full balance when your assets and future income genuinely can't cover the debt. It costs a $205 application fee and, for lump-sum offers, 20% down — both waived if your household income is at or below 250% of the federal poverty level, a threshold many Social Security-only households actually meet. The IRS accepted roughly 1 in 5 offers in FY2024, so this is a math test, not a discount program.

- Penalty relief — first-time abatement can strip penalties if your prior three years were clean, and starting summer 2026 the IRS's Automatic Exemption from Penalty (AEP) applies similar relief automatically, with no request needed. Less balance means a smaller plan payment.

| Option | Upfront cost | Effect on the 15% levy | Typical timeline |

|---|---|---|---|

| Pay in full | The balance | Levy never starts / released | Immediate |

| Short-term plan (≤180 days) | $0 setup | Enforcement paused while you pay | Same day online |

| Streamlined installment agreement | Modest setup fee (reduced or waived for low-income) | Generally released once accepted | Days to a few weeks |

| Currently Not Collectible | $0 (Form 433-F financials required) | Levy released; collection paused | Weeks, once financials are reviewed |

| Hardship levy release (§6343) | $0 | Active levy released on hardship showing | Fastest path when basic needs are at risk |

| Offer in Compromise | $205 + 20% down (waived for low-income) | Levies generally held while offer is pending | Months; auto-accepted if no decision in 2 years, with narrow exceptions - a returned or rejected offer stops the clock, and time during court disputes does not count |

A worked example: $19,700 owed, two Social Security checks

Say you and your spouse filed jointly and owe $19,700, and your combined benefits are $3,480 a month — $2,080 for one of you, $1,400 for the other. Here's how the paths compare:

- Do nothing: FPLP takes 15% of $3,480 = $522 every month. At that pace it would take about 38 months of levies ($522 × 38 ≈ $19,836) just to cover today's balance — and longer in practice, because interest and the 0.5%/month failure-to-pay penalty keep accruing while the levy runs.

- Streamlined installment agreement: $19,700 is under the $25,000 streamlined threshold. Spread over 72 months, the minimum is roughly $274/month ($19,700 ÷ 72) before accruing interest — nearly half the levy amount, on a schedule you chose, with your full checks arriving intact.

- Currently Not Collectible: if your allowable living expenses — housing, utilities, food, out-of-pocket medical — run $3,600 a month against $3,480 of income, you're a genuine CNC candidate. Collection pauses, the levy releases, and the 10-year clock keeps ticking toward expiration.

This is hypothetical math, but it's the exact comparison the IRS runs on your Form 433-F. You can estimate what a levy could take from your own household with our IRS Wage Garnishment Calculator.

How to respond to a Social Security levy notice, step by step

- Find your deadline — locate the response date printed on your CP91 or final levy notice; that date, not a general rule, controls how long you have.

- Verify the balance — log into your IRS online account and confirm the amount, the tax years involved, and whether past payments posted correctly.

- Run the hardship math — compare your household's monthly income against the IRS allowable living expense standards; if expenses exceed income, you're a candidate for Currently Not Collectible status instead of a payment plan.

- Set up a resolution before the deadline — establish a payment plan online, request CNC status, or start an Offer in Compromise; any accepted arrangement generally keeps the 15% levy from starting or gets it released.

- Preserve your appeal rights — if you received an LT11 or CP90 final notice, file Form 12153 within 30 days to request a Collection Due Process hearing; it pauses levy action while your case is heard.

When you can handle this yourself — and when help changes the outcome

Plenty of Social Security levy situations don't need professional help. If your balance is one you can clear within 180 days, if you agree with the amount and a ~$274/month streamlined plan fits your budget, or if you're still at the CP14 stage with time on the clock, setting up a plan yourself at IRS.gov's payment plans page is straightforward and cheap.

Experienced help earns its cost in a narrower set of situations: the levy is already taking money you need for medication or housing and you need a hardship release argued now; you have unfiled years blocking any agreement; the debt is joint and only one spouse's income created it; or your finances genuinely fit the Offer in Compromise profile and the 433 math needs to be built correctly the first time — with a 1-in-5 acceptance rate, a sloppy offer is an expensive way to lose a year. In 2026's understaffed IRS, having someone who knows which unit to reach — and what to file so the automated system stands down — is often the difference between a release in weeks and a levy that grinds on for months.

If your case fits that second list, an experienced tax professional can review your notice and your numbers free — start with the 2-minute form before the next benefit payment goes out short.

Terms on your notice, decoded

- FPLP (Federal Payment Levy Program) — the automated Treasury matching system that diverts up to 15% of federal payments, including Social Security, toward tax debt.

- Continuous levy — a levy that attaches to every future payment until released, unlike a one-time bank levy that grabs a single snapshot.

- CP91 — the IRS notice announcing its intent to take up to 15% of your Social Security benefit, typically giving 30 days to respond.

- CDP hearing (Form 12153) — your Collection Due Process right to an independent appeal, available for 30 days after a final notice of intent to levy.

- Currently Not Collectible (CNC) — hardship status that pauses IRS collection when your necessary living expenses meet or exceed your income.

- CSED — the Collection Statute Expiration Date: generally 10 years from assessment, after which the IRS must stop collecting and release any levy — though appeals, offers, and bankruptcy pause the clock.

Can the IRS garnish Social Security: your questions answered

How much of my Social Security can the IRS take?

Up to 15% of your monthly benefit through the Federal Payment Levy Program, taken automatically from every check until the debt is resolved. Unlike garnishments by private creditors, there is no dollar floor under FPLP — the 15% comes out even if what's left doesn't cover your bills. If the levy leaves you unable to pay basic living expenses, you can request a hardship release.

Can the IRS take my entire Social Security check?

No — through the automated Federal Payment Levy Program, the IRS is capped at 15% of your benefit. In rarer cases, a revenue officer can issue a manual levy that isn't capped at 15%, but it must leave you an exempt amount based on your filing status and dependents. Either way, you always receive written notice before any money is taken.

Does the IRS garnish SSI?

No. Supplemental Security Income is excluded from the Federal Payment Levy Program, so SSI payments are not garnished for federal tax debt. Lump-sum death benefits and benefits paid to children are also excluded. If money was taken from an SSI payment, that points to a different debt or an error worth investigating right away.

Can the IRS garnish SSDI?

Yes. Social Security Disability Insurance is treated the same as retirement benefits under the Federal Payment Levy Program, so the IRS can take up to 15% of an SSDI check. SSI — the needs-based program — is exempt. Many SSDI recipients qualify for hardship status or a levy release because their income already falls below the IRS's allowable living expense standards.

Will the IRS warn me before garnishing my Social Security?

Yes. Before the 15% levy starts, the IRS sends a series of balance-due notices and then a final warning — typically a CP91 for Social Security — giving you about 30 days to respond. The exact deadline is printed on your notice. If you act inside that window with a payment plan or hardship request, the levy never has to start.

How do I stop the IRS from taking my Social Security?

Set up a resolution before the levy starts, or request a release once it has: an installment agreement, Currently Not Collectible status, an economic-hardship levy release, or — if your finances qualify — an Offer in Compromise. A payment plan on a balance under $25,000 can usually be set up without detailed financial disclosure, and the levy is generally released once the agreement is in place.

Does the Social Security levy stop when the 10-year collection statute expires?

Yes — the IRS generally has 10 years from assessment to collect, and a levy must be released when that collection statute (CSED) expires. But the clock pauses during bankruptcy, a pending Offer in Compromise, and certain appeals, so your real expiration date may be later than ten calendar years. Check your CSED before deciding to wait it out — for many retirees, resolving the debt costs less than years of 15% levies.

Isn't Social Security protected from garnishment?

From most creditors, yes — federal law shields Social Security from private debt collectors and most court judgments. But that protection has exceptions for the federal government itself: the IRS, other federal agencies, child support, and alimony can all reach benefits. For federal tax debt, the tax code specifically authorizes the 15% continuous levy on Social Security.

Your next 24 hours

- Find the date. Pull out your CP91 or most recent IRS notice and circle the response deadline printed near the top — that date decides how much room you have before the 15% levy starts or continues.

- Gather three things. The notice itself, your last filed tax return, and a simple list of your household's monthly income and expenses — both spouses' benefits included. That's everything a resolution requires.

- Get the free case review. Call (888) 825-7779 or use the 2-minute form and an experienced tax professional will map your fastest route to protecting your benefit — before the deadline on your notice passes.

For primary-source reading: the IRS explains the levy program on its Federal Payment Levy Program page, payment options live at IRS.gov/payments, and the independent Taxpayer Advocate Service can intervene when a levy creates hardship the normal channels won't fix.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.