IRS Collections

Can the IRS Take My House? When Home Seizure Really Happens (2026)

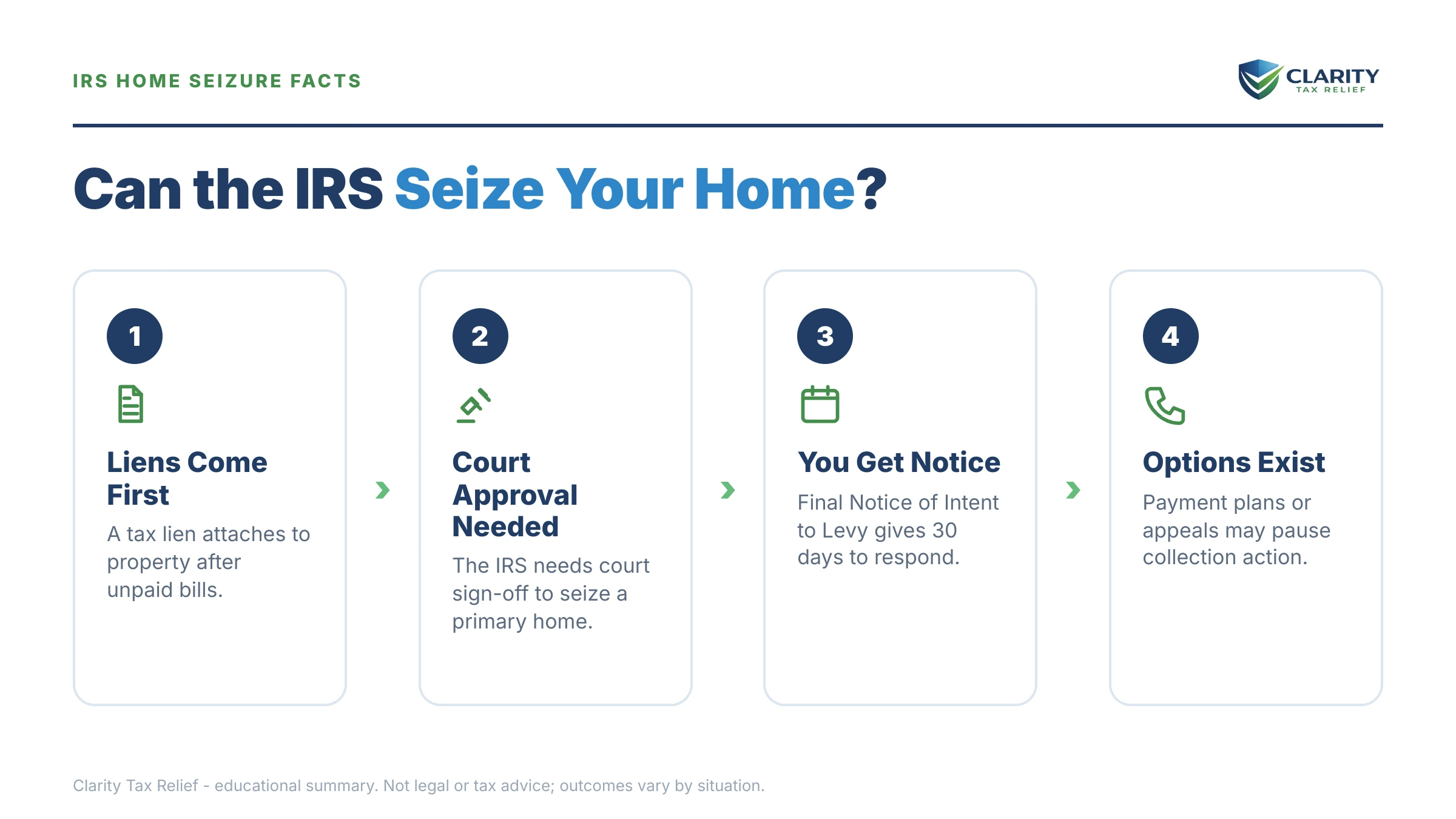

Can the IRS take my house? Legally, yes — but almost never in practice. Seizing a primary residence requires a federal district court judge's written approval, is prohibited for debts of $5,000 or less, and is treated as a last resort. The realistic threats are a tax lien on the title and levies on wages and bank accounts.

You're probably reading this with a levy notice on the table. Maybe your name is on a deed — or maybe you rent, and you're wondering whether the IRS can reach the roof over your head or the house you're saving toward. Either way, the honest answer comes with more built-in protections than the notice lets on, and every one of those protections has a deadline attached.

Home seizure sits at the very top of a long enforcement ladder. The image below shows you exactly where it sits — and how many rungs, notices, and legal checkpoints come before it.

⏱ The clock that matters: if you're holding an LT11 notice or Letter 1058, you have 30 days from the notice date to request a Collection Due Process hearing with Form 12153. That request pauses levy action while it's heard — it's the strongest legal brake between the IRS and your property.

When can the IRS take my house? The legal test

The IRS cannot seize a primary residence without the written approval of a federal district court judge or magistrate, and it cannot levy your home at all for a debt of $5,000 or less. Both protections are written directly into the tax code, at Internal Revenue Code Section 6334.

That court-approval requirement is not a rubber stamp. Before the government ever files, a revenue officer has to document that you had the ability to pay and refused, that less drastic collection was tried or wouldn't work, and that the seizure would actually produce money. Then you get notice of the court proceeding and a chance to object before a judge signs anything.

There's also an economics test the IRS applies to itself. A seizure must yield net proceeds after the mortgage and sale costs — a home with little equity isn't worth taking, no matter how large the debt. The IRS wants the fastest dollar, and a forced home sale is the slowest, most expensive dollar it can chase.

What the IRS does do routinely is file a Notice of Federal Tax Lien — a public claim that attaches to everything you own, including your home. A lien doesn't take your house; it takes a position in it, so the IRS gets paid when you sell or refinance. Our guide to the federal tax lien on your house covers that scenario in full, including how people sell a house with an IRS lien anyway.

Two caveats keep this honest. First, the judge-approval shield covers only your principal residence — a rental property, vacation home, or inherited house you don't live in can be seized through the ordinary administrative process. Second, the government can also file a lien-foreclosure lawsuit under IRC Section 7403 and ask a court to order a sale — rare, expensive for the government, and again reserved for large debts and uncooperative taxpayers.

What actually happens before any home seizure

Before the IRS could auction a house, it must send a sequence of escalating notices, offer you a formal hearing, and win a judge's sign-off — more exit ramps than any other debt collection process in America. The table below shows the sequence and the response window each stage gives you.

| Stage | What the IRS can reach | Your window |

|---|---|---|

| CP14 — first bill | Nothing yet; it's a bill | Typically 21 days from the notice date |

| CP501 / CP503 reminders | Nothing yet; the balance grows monthly | Weeks between notices |

| CP504 — intent to levy | Your state tax refund | Act before the final notice issues |

| LT11 / Letter 1058 — final notice | Wages, bank accounts, and property after 30 days | 30 days to request a CDP hearing (Form 12153) |

| Bank levy | Account funds, held 21 days before they're sent | 21 days to seek a release |

| Wage levy | A continuous slice of every paycheck until released | Release requires setting up a resolution |

| Notice of Federal Tax Lien | A recorded claim on all property, including your home | Appeal rights arrive with the lien-filing letter |

| Court-approved home seizure | A principal residence — only with a judge's approval | You can object in court before approval |

Notice what comes first at every stage: the liquid stuff. Paychecks, bank balances, and refunds are faster and cheaper to reach than real estate, which is why they get levied constantly while houses almost never do. If you rent, also notice what's missing from this list entirely — your landlord's house. The IRS cannot seize property you don't own. For a renter, the real exposure is your paycheck and your accounts; you can estimate how much of a paycheck a wage levy could reach with our IRS Wage Garnishment Calculator.

If every notice were ignored and the IRS decided a house was worth pursuing, the seizure pipeline itself runs like this:

- A revenue officer takes the case — home seizures aren't automated; a human collector must build the file.

- An equity analysis — the IRS confirms the sale would clear the mortgage and costs and still produce net proceeds.

- Management and IRS Counsel approval — multiple internal sign-offs are required for a residence.

- A petition in federal district court — the Department of Justice asks a judge to approve the levy on your principal residence.

- Your chance to object — you receive notice of the proceeding and can show the judge why the seizure shouldn't proceed or how you'll resolve the debt.

- Seizure, minimum-bid sale, and accounting — the home is sold at or above a set minimum bid; the mortgage and the tax debt are paid, and any surplus is returned to you. Federal law even gives you 180 days after the sale to redeem the property.

One 2026 reality check: the IRS workforce shrank roughly 27% in 2025, so reaching a human is harder than ever — but the notices, liens, and wage and bank levies in the table above are issued by automated systems that never stopped running. The rarity of home seizure is not a reason to ignore the machine that's escalating toward your paycheck right now.

Worried the IRS is moving toward your home — or your paycheck?

If an LT11 or Letter 1058 is in your hands, the 30-day Collection Due Process window is the strongest brake you have. Get your notice reviewed free before it closes — an experienced tax professional will tell you exactly where you sit on the ladder and which exit fits.

Your options to stop a levy and protect your home

Every resolution option — from a 180-day extension to an Offer in Compromise — takes home seizure off the table while it's pending or in good standing. The step-by-step mechanics of each program live in our guide to how to settle tax debt yourself; here is how each one maps to protecting your property.

| Option | Typically fits when | Effect on enforcement |

|---|---|---|

| Short-term payment plan | You can pay in full within 180 days; $0 setup fee | Collection generally holds while you pay it down |

| Guaranteed installment agreement | You owe $10,000 or less and meet basic filing conditions | The IRS must accept it when the conditions are met |

| Streamlined installment agreement | You owe $50,000 or less; up to 72 months, set up online | The IRS generally doesn't levy while an agreement is pending or in good standing |

| Currently Not Collectible | Paying anything would leave you unable to cover basic living costs | Levies pause; the debt and any lien remain, and interest accrues |

| Offer in Compromise | Assets plus future income genuinely can't cover the debt; $205 fee, waived with low-income certification | Levy action generally pauses during review; roughly 1 in 5 offers were accepted in FY2024 |

| CDP hearing (Form 12153) | Filed within 30 days of an LT11 or Letter 1058 | Levy action pauses while heard; note it also pauses the 10-year collection clock |

Interest and penalties keep accruing under every option except full payment, so the cheapest path is always the fastest one your budget can actually sustain. And because the 10-year collection statute pauses during appeals, offers, and bankruptcy, "waiting it out" is rarely the shortcut it looks like.

Say you owe $41,800 and rent: the realistic math

Here's a clearly hypothetical example. Say you rent an apartment, owe $41,800, and an LT11 just arrived. There's no house to seize — but there is a paycheck, a bank account, and a 30-day clock.

Because $41,800 is under the $50,000 streamlined ceiling, you could set up a 72-month installment agreement online without submitting a full financial statement: $41,800 ÷ 72 = about $581 per month, with penalties and interest continuing to accrue on the shrinking balance — so paying more than the minimum whenever possible saves real money. It's also below the $66,000 passport-certification threshold for 2026, so your passport isn't in play at this balance.

The house angle still matters even as a renter: if the IRS files a Notice of Federal Tax Lien before you resolve the debt, that lien attaches to any home you buy later and complicates the mortgage — the full picture is in can I buy a house if I owe the IRS. And if rent and basics genuinely consume your income, run the other math first: when the IRS's own collection formulas show it could never recover the full $41,800 from your income and assets, Currently Not Collectible status or an Offer in Compromise may fit better than a plan you'll default on. An OIC is means-tested, not a discount program — which is exactly why the honest arithmetic matters before you file one.

How to respond, step by step

- Identify the exact notice you're holding. Find the notice number in the top corner. A CP504 threatens your state refund; an LT11 or Letter 1058 is the final notice that starts the 30-day levy clock.

- Calendar your 30-day deadline. If you have an LT11 or Letter 1058, count 30 days from the notice date and file Form 12153 before it passes to preserve your Collection Due Process hearing.

- Verify what you owe. Log into your IRS online account and confirm the balance, the tax years, and that every required return is filed — every resolution option requires filing compliance.

- Set up a resolution before the window closes. Pick the option that fits your finances — a payment plan, hardship status, or an offer — and submit it; a pending arrangement generally halts levy action.

- Get experienced help if enforcement is in motion. If a levy has already hit, a revenue officer is assigned, or you own a home with significant equity, have an experienced tax professional review your case before you respond.

When you can handle this yourself — and when help changes the outcome

Plenty of people in this situation don't need professional help. If you owe under $50,000, every return is filed, no levy has landed, and a streamlined monthly payment fits your budget, you can set up the agreement yourself online in under an hour — the IRS's own payment plans page walks through it. The same is true if you can simply pay within 180 days.

Experienced help earns its cost when the stakes or the math get complicated: an LT11 with days left on the CDP window, a wage or bank levy already in motion, a revenue officer assigned to your case, multiple unfiled years that block every program, a home with substantial equity that makes you a rare genuine seizure candidate, or a jointly owned property where a non-liable spouse's interest is tangled in the lien — a scenario covered in IRS lien on jointly owned property. In those cases, the order you fix things in changes what you ultimately pay and what the IRS can touch while you fix it.

One related worry worth defusing: if someone knocks on your door claiming to be the IRS, that has its own rules and its own scams — see will the IRS come to my house before you open the door or hand over anything.

Terms on your notice, decoded

- Lien — a recorded legal claim securing the debt against everything you own; it doesn't take property, it takes a position in it. The IRS's own primer is at Understanding a Federal Tax Lien.

- Levy — the actual taking of property to pay the debt: wages, bank funds, or, rarely, physical assets.

- Seizure — a levy on physical property like a car or house, followed by a government sale.

- CDP (Collection Due Process) — your statutory right to a hearing before levy action, requested on Form 12153 within 30 days of the final notice.

- CSED (Collection Statute Expiration Date) — the end of the IRS's 10-year window to collect, though appeals, offers, and bankruptcy pause the clock.

- Right of redemption — your federal right to buy back seized real estate within 180 days after the government sells it.

If a levy would leave you unable to pay basic living expenses, the Taxpayer Advocate Service is an independent, free channel inside the IRS that can intervene in hardship cases.

Can the IRS take your house? Questions people actually ask

How often does the IRS actually seize houses?

Rarely. In a typical year the IRS conducts only a few hundred seizures of all property types combined — vehicles, business assets, and real estate — against millions of liens and levies. A principal-residence seizure also requires a federal judge's written approval, so it is reserved for large debts where the taxpayer has refused every other resolution.

How much do you have to owe before the IRS takes your house?

There is no dollar amount that automatically triggers a home seizure, but federal law bars the IRS from levying a principal residence for a debt of $5,000 or less. In practice, seizures target large balances with substantial home equity after the taxpayer has ignored repeated notices and refused payment arrangements. Setting up a payment plan or hardship status at any balance takes seizure off the table.

Can the IRS take a house I'm renting?

No. The IRS can only seize property you own, so your landlord's house is never at risk for your tax debt. As a renter, your real exposure is a wage levy, a bank account levy, and offsets of your tax refunds. A lien filed now can also attach to a home you buy later, which is why resolving the balance before a purchase matters.

Can the IRS take my house if only my spouse owes the taxes?

The federal tax lien attaches to your spouse's interest in the property, not yours. Courts have, in rare cases, allowed the government to force the sale of a jointly owned home and pay the non-liable spouse their share of the proceeds — but that requires a full court case. If a lien has been filed against a home you co-own, get advice before selling or refinancing.

Does a federal tax lien mean the IRS is taking my house?

No. A lien is a legal claim that attaches to your property and secures the debt; a levy or seizure is the act of actually taking property. The lien mostly matters when you sell or refinance, because the IRS gets paid from the proceeds. Many taxpayers carry liens for years; only a tiny fraction ever face an actual seizure.

Can I sell my house if the IRS has a lien on it?

Yes. Homes with federal tax liens are sold regularly — the lien is paid from your proceeds at closing. If your equity can't cover the full lien, the IRS can discharge the property from the lien using Form 14135 so the sale can still close. Start that paperwork early; it typically takes weeks, not days.

Does a state homestead exemption protect my house from the IRS?

No. State homestead exemptions protect your home from most private creditors, but they do not defeat a federal tax lien or a court-approved federal seizure. Your real protections are federal ones: the $5,000 minimum for a residence levy, the required court approval for a principal residence, and your Collection Due Process rights before any levy.

Your next 24 hours

- Find the notice number and date in the top corner of the letter you're holding — that single line tells you whether you're at the CP504 stage or inside the final 30-day LT11 window.

- Gather three things: the notice itself, your most recent filed tax return, and a rough monthly income-and-rent (or mortgage) figure. That's everything needed to match you to the right option.

- Get a free case review — call (888) 825-7779 or use the 2-minute form. If a final notice of intent to levy is in your hands, do it before the 30-day Collection Due Process window on that notice closes.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.