IRS Notices

IRS CP504 Notice: Intent to Levy — What It Means and What to Do (2026)

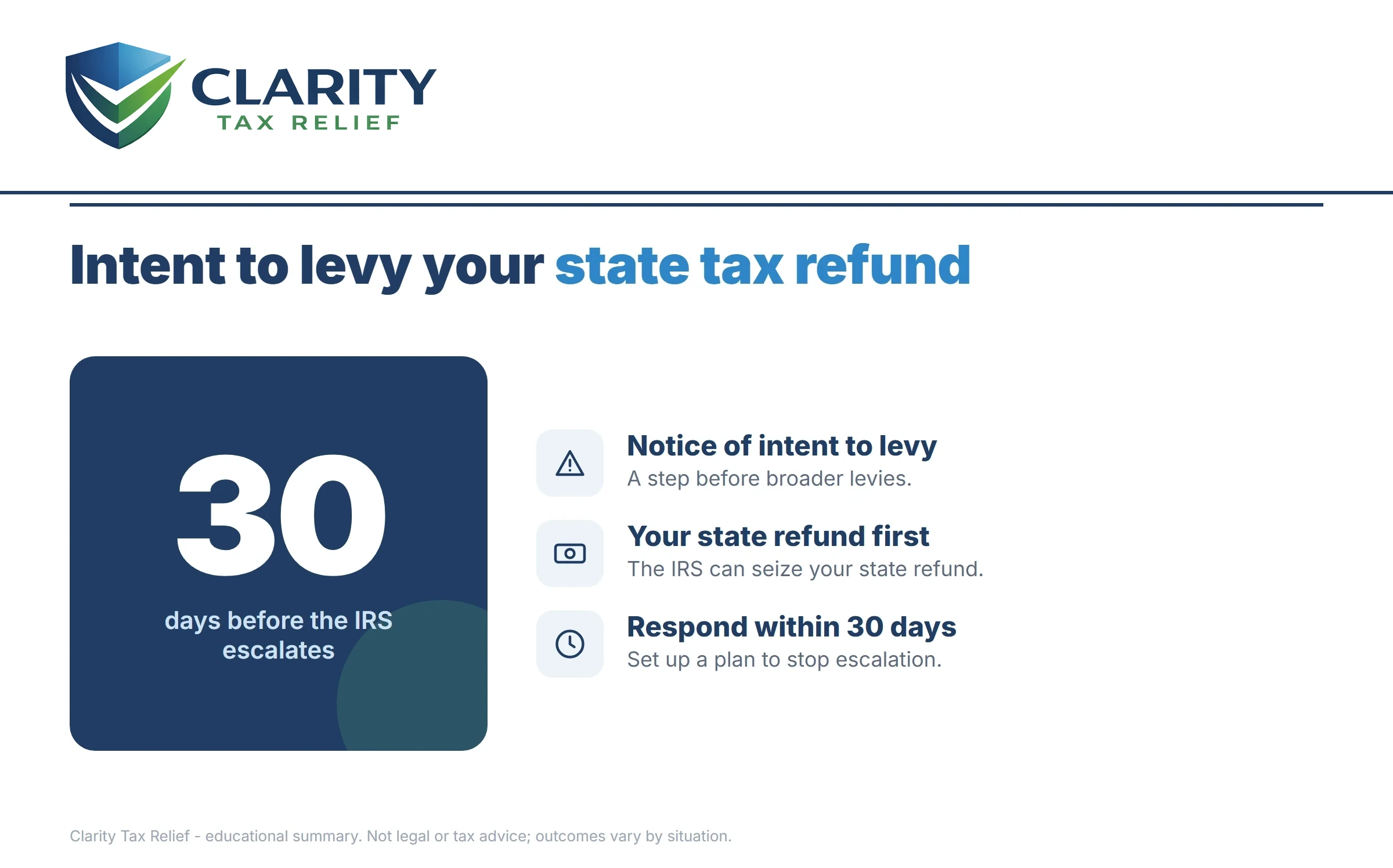

The short answer: a CP504 notice is the IRS's Notice of Intent to Levy under IRC §6331(d). It allows the IRS to seize exactly one thing — your state tax refund — and warns that a federal tax lien may follow. It is not the final levy notice, and you typically have 30 days to act.

The words "Notice of intent to levy — intent to seize your property or rights to property" are printed in bold near the top, and it probably arrived by certified mail. Here's the fact the letter buries: the IRS still cannot touch your paycheck or your bank account based on this notice. The CP504 is the last warning before the notice that can — which makes the next 30 days the cheapest window you'll ever have to fix this.

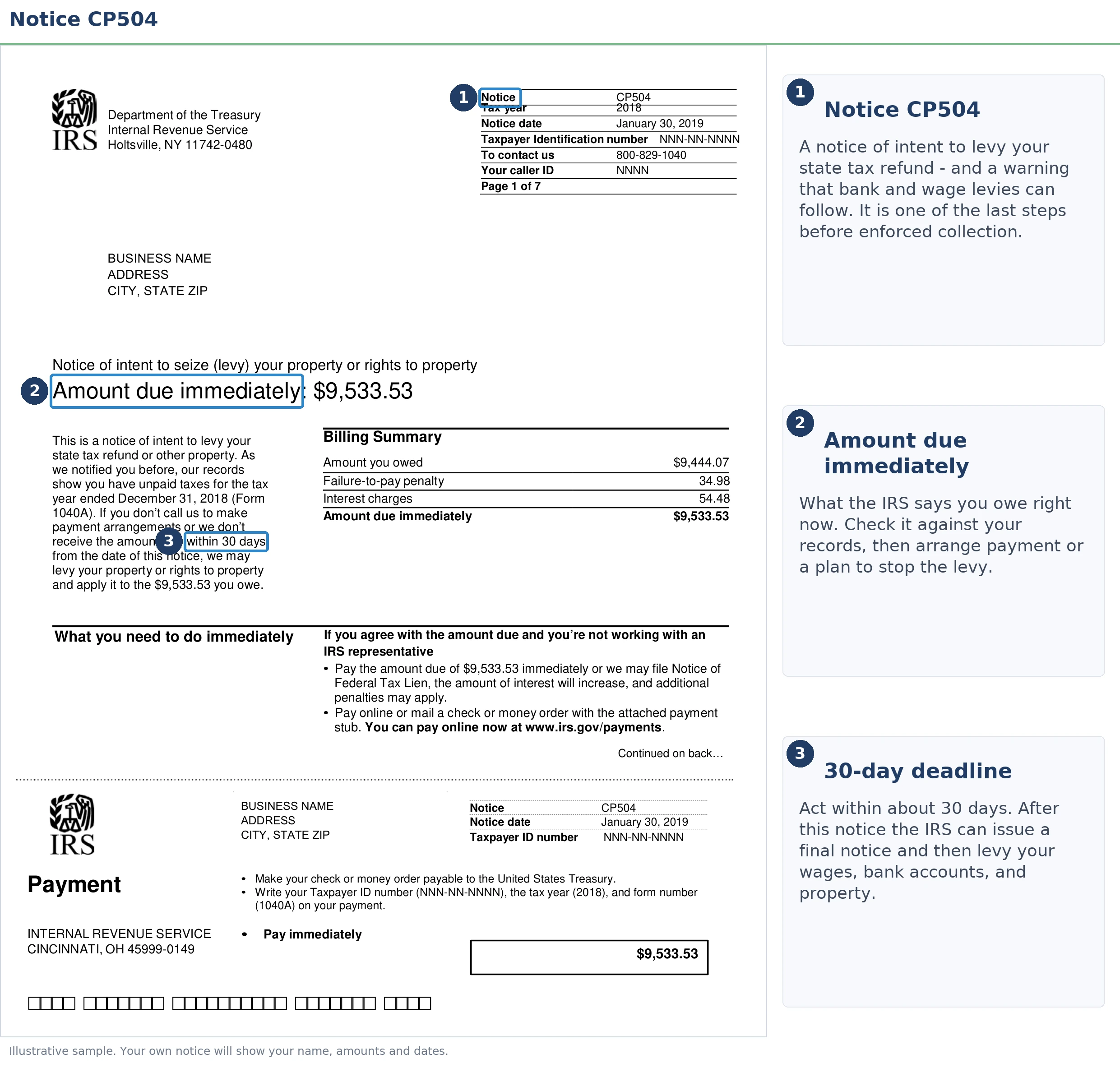

If you're not sure which of the IRS's similar-sounding letters you're actually holding, the image below shows exactly what a CP504 looks like and where the controlling date and balance sit on the page.

⏱ Your deadline: the due date printed on the front of your CP504 — typically 30 days from the notice date, the window IRC §6331(d) requires before the IRS can levy your state refund. The date on the notice controls, not the day you opened the envelope. Interest and the 0.5% monthly failure-to-pay penalty keep accruing throughout.

What a CP504 actually is — and what it isn't

A CP504 authorizes the IRS to levy only your state tax refund — not your wages, bank account, or property. That's the legal effect of the §6331(d) notice, despite the alarming "intent to seize your property" language on the front. Wage and bank levies require a later, different letter: the LT11 notice (or Letter 1058), which starts its own 30-day clock and carries formal hearing rights.

So the CP504 is dangerous for what it sets up, not what it does. It's the last routine notice in the collection sequence. Ignore it, and the next letter puts everything you own within the IRS's reach — while the CP504 stage still lets you resolve the balance on ordinary terms, usually online, with no seizure in motion.

One more distinction: a CP504 is not an audit and not a dispute about your return. The IRS considers the tax already assessed and final. This stage is purely about collection — which means your leverage comes from arranging payment, not arguing the numbers (with narrow exceptions covered below).

Why you got a CP504 notice

A CP504 is the fourth notice in the IRS collection sequence, not the first — it means a balance was assessed months ago and the earlier bills went unanswered. The chain runs CP14 notice (first bill) → CP501/CP503 (reminders) → CP504. If this is genuinely the first letter you've seen, something interrupted the chain, not the debt.

The common paths here:

- You filed but couldn't pay in full, planned to catch up, and the earlier notices piled up unopened.

- You moved and the CP14 and reminders went to an old address. They're still legally valid — the IRS only has to mail to your last known address.

- The IRS changed your return — a math-error adjustment like a CP11 notice created a balance you never agreed to or forgot about.

- A payment plan defaulted, quietly putting the account back into active collections.

- On a joint return, one spouse handled the mail and the other is seeing the problem for the first time. Both spouses are fully liable for the whole balance, regardless of whose income created it.

For the broader map of how IRS letters fit together, see why did I get a letter from the IRS — this page stays focused on the CP504 itself.

What the IRS can do right now with a CP504

After the CP504's 30-day window passes, the IRS can take your state income tax refund through the State Income Tax Levy Program — automatically, with no further warning. If you're expecting a state refund, it's already spoken for unless you resolve the balance first.

The notice also warns that the IRS may file a Notice of Federal Tax Lien. A lien doesn't take anything today, but it attaches to everything you own — including a home you co-own with your spouse — and becomes public record. It can stall a sale or refinance at the worst moment. If a lien gets filed, you'll receive Letter 3172, which carries its own appeal rights.

Just as important is what the IRS cannot do based on a CP504 alone: levy your wages, bank accounts, Social Security, or property. Every one of those requires the final notice and another 30 days. If someone — especially a company that cold-called you — tells you a CP504 means your paycheck is about to be garnished, they're wrong about the law or lying to scare you.

One threshold worth knowing: passport certification for "seriously delinquent" debt kicks in at $66,000 in 2026. A CP504 alone doesn't trigger it, but a lien filing on a large enough balance can put it in play.

What happens if you ignore a CP504

Nothing about a CP504 expires or gets forgotten — the sequence that follows is fully automated, and in 2026 that matters more than ever. The IRS workforce shrank roughly 27% in 2025, so reaching a human is harder, but the computers that issue levies never stopped. Ignored, your account moves through these stages:

- The 30-day window closes. The IRS can now intercept your state tax refund and may file a federal tax lien against everything you own.

- The final notice arrives — LT11 or Letter 1058. This one starts a 30-day clock on your Collection Due Process rights, your strongest procedural protection.

- That 30-day window closes too. The IRS gains full levy authority — and you lose the CDP hearing that comes with Tax Court review.

- Levies begin. A bank levy freezes funds for a 21-day hold before the money leaves. A wage levy is continuous — it hits every paycheck until released. Social Security can be levied at up to 15% through the Federal Payment Levy Program.

How much calendar time that takes varies by account — we break down the realistic gaps in CP504: how long before levy — but the order never changes, and each stage removes options the previous one still offered.

| Notice | What it is | What the IRS can do at this stage |

|---|---|---|

| CP14 | First bill (about 21 days to pay) | Nothing yet — penalties and interest accrue |

| CP501 / CP503 | Reminder notices | No new powers — balance keeps growing |

| CP504 — you are here | Intent to levy under IRC §6331(d) | Seize your state tax refund; may file a federal tax lien |

| LT11 / Letter 1058 | Final notice of intent to levy (30-day clock) | After 30 days: levy wages, bank accounts, property |

| Active levy | Enforcement | Bank funds held 21 days then taken; continuous wage levy; up to 15% of Social Security |

Holding a CP504 with the clock running?

Get it reviewed free before your 30-day window closes. An experienced tax professional will confirm where you are in the sequence, what the IRS can actually take, and which resolution fits your numbers — no pressure, no obligation.

Your options after a CP504 notice

Any arrangement approved before the notice date stops the escalation — a CP504 doesn't disqualify you from a single IRS program. The notice presents two choices, pay or be levied; the real menu is longer:

| Option | Who typically qualifies | Cost & effect on the CP504 clock |

|---|---|---|

| Pay in full | Anyone with the funds | No fee; stops all notices, penalties stop growing immediately |

| Short-term plan (up to 180 days) | You can raise the full amount within 6 months | $0 setup; enforcement pauses while approved; interest continues |

| Streamlined installment agreement | Balance ≤ $50,000, all returns filed | Setup fee varies (lowest with direct debit); up to 72 months online; halts escalation |

| Currently Not Collectible | Paying would leave you unable to cover basic living expenses | No fee; requires financial disclosure; collection pauses, debt and interest remain, lien likely |

| Offer in Compromise | Assets + future income genuinely can't cover the debt | $205 fee + 20% down on lump-sum offers (both waived for low-income filers); roughly 1 in 5 accepted in FY2024 |

| Penalty abatement | Clean 3-year compliance history, or reasonable cause | Free to request; removes failure-to-pay penalties and their interest, shrinking the balance |

A few specifics the table can't hold:

- The streamlined installment agreement is the workhorse at this stage: balances of $50,000 or less qualify for up to 72 months online with no financial disclosure. A bonus most people miss — while an approved agreement is in effect for a timely-filed return, the failure-to-pay penalty typically drops from 0.5% to 0.25% per month.

- Currently Not Collectible status pauses collection when your budget genuinely can't support payments. Interest still accrues and a lien usually gets filed, but the 10-year collection statute keeps running while you're protected.

- An Offer in Compromise settles for less than you owe only when the IRS's own math shows it could never collect the full amount — see how an offer in compromise works before anyone charges you to pursue one. Unfiled returns disqualify you, and offers are auto-accepted if the IRS doesn't decide within 2 years, with narrow exceptions - a returned or rejected offer stops the clock, and time during court disputes does not count.

- First-time penalty abatement requires a clean prior three years. Starting summer 2026, the IRS's new Automatic Exemption from Penalty (AEP) begins applying similar relief automatically — but on a CP504 balance that's been growing for months, it's worth requesting affirmatively rather than waiting.

What resolving $41,800 actually looks like: a worked example

Say you and your spouse filed jointly and the CP504 shows $41,800 — a big self-employment year for one of you, no estimated payments, and three unopened notices later, here you are. This is hypothetical, but the arithmetic is real:

- The cost of waiting: the 0.5% monthly failure-to-pay penalty alone adds about $209 every month ($41,800 × 0.005) — before interest, which compounds on top. You can estimate your own balance's growth with our IRS penalty & interest calculator.

- Streamlined installment agreement: at $41,800 you're under the $50,000 line, so you can set this up online without submitting financials. The floor payment is roughly $41,800 ÷ 72 ≈ $581/month; because interest keeps accruing, budgeting closer to $650–$700 pays it off inside the window and cuts total interest meaningfully.

- Short-term plan: 180 days means roughly $6,970/month equivalent — realistic only if a bonus, home-equity draw, or asset sale is coming. If it is, this is the cheapest structured option: $0 setup and the shortest accrual period.

- Offer in Compromise: both spouses' income and assets count on a joint liability. If you own a home with, say, $60,000 of reachable equity, the IRS sees more than $41,800 of collection potential and an offer is effectively off the table. If you rent, have minimal assets, and only a few hundred dollars of monthly disposable income under IRS expense standards, an offer built on that math may genuinely fit — but it's the exception, not the default.

- Passport check: $41,800 sits below the $66,000 certification threshold for 2026 — but add a second unresolved year plus accruals, and a couple can cross it faster than they expect.

The takeaway for this couple: an online payment plan set up this week costs about $581–$700 a month and ends the escalation entirely. Doing nothing costs $209+ a month, a likely lien, and eventually a levy — for the same debt.

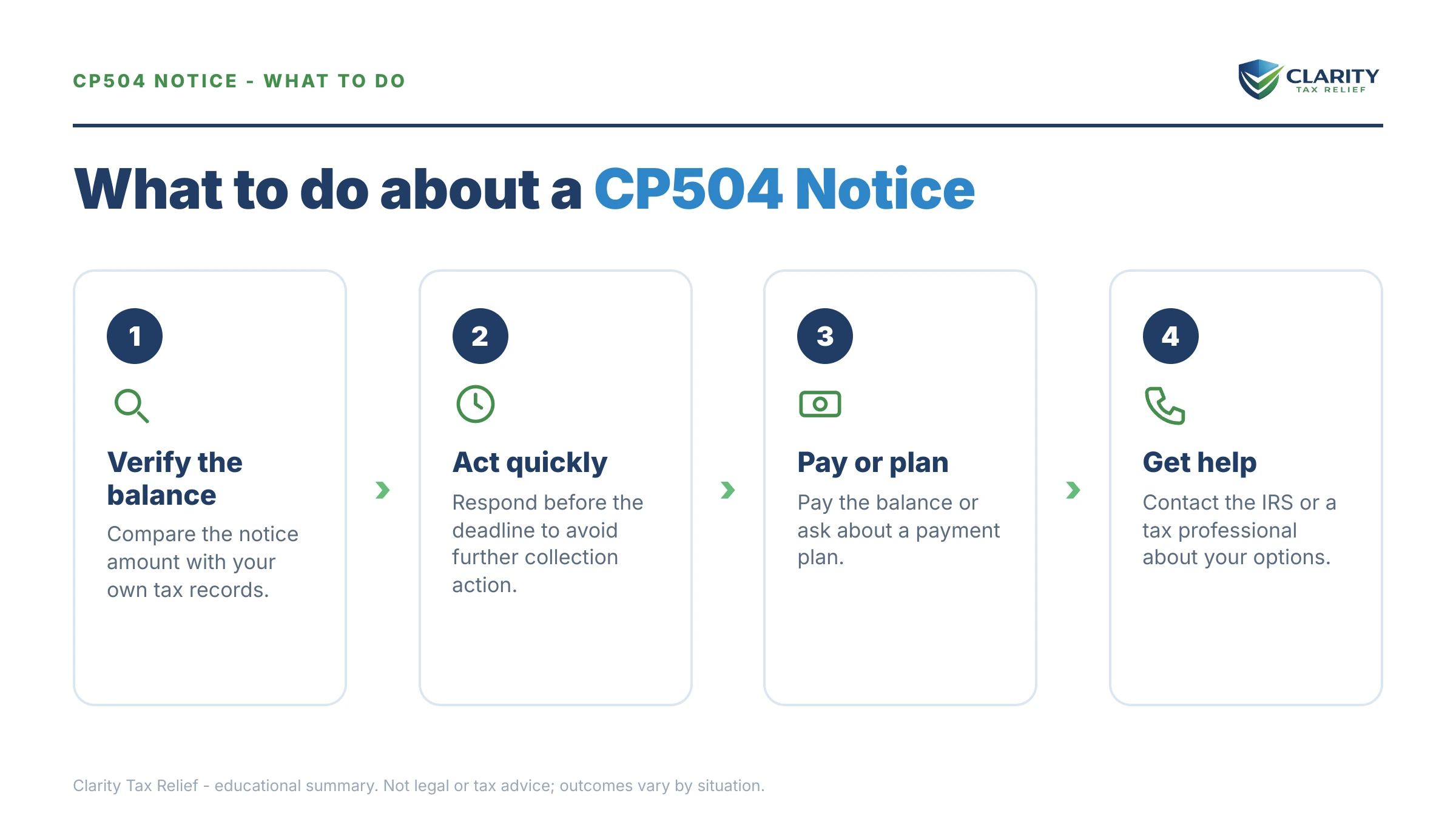

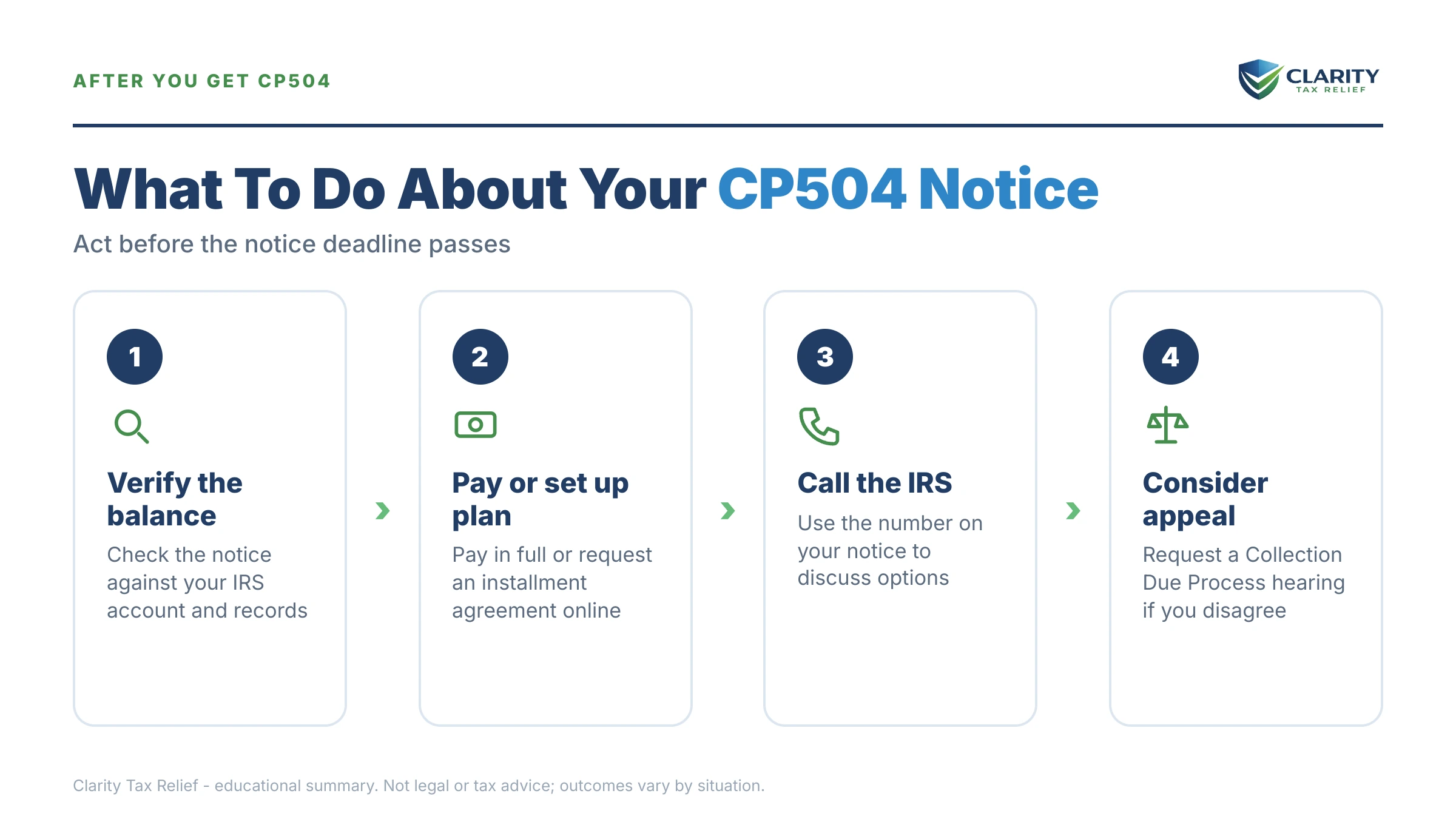

How to respond to a CP504, step by step

- Verify the balance. Log into your IRS online account and compare the balance, tax year, and posted payments against your CP504 before paying anything.

- Confirm every return is filed. Unfiled years block payment plans and offers alike — file any missing returns first, even if you can't pay what they show.

- Choose your resolution. Pick full payment, a 180-day short-term plan, a monthly installment agreement, hardship status, or an Offer in Compromise based on what your budget genuinely supports.

- Set it up before the notice date. Arrange the plan online at IRS.gov or by phone before the date printed on your CP504 — an approved arrangement stops the escalation to the final levy notice.

- Request penalty relief. If you have a clean three-year compliance history, ask for first-time abatement of the failure-to-pay penalty when you set up your plan.

- Get a professional review if anything is complicated. Multiple years, business taxes, or a possible offer are situations where an experienced tax professional changes the outcome — start with a free case review.

Payments and plan setup both live at the IRS's official payment plans and installment agreements page — never pay a tax balance through anyone who contacted you first.

CP504 vs. LT11: the appeal rights you have at each stage

A CP504 does not carry Collection Due Process rights — that stronger protection only attaches to the final notice that follows. What you have now is the Collection Appeals Program (CAP), requested on Form 9423, which can pause a specific action like a state refund levy or a lien filing. It's faster than CDP but narrower: no Tax Court review, and you generally can't contest the underlying tax. Details in our CAP appeals guide.

If the LT11 arrives, the calculus changes. You'd have 30 days to file Form 12153 for a CDP hearing — which freezes levies on the years at issue while the hearing is pending and preserves your right to Tax Court review. Missing that window is the single most expensive procedural mistake in IRS collections.

| Notice | Response window | Appeal right | What you lose if it passes |

|---|---|---|---|

| CP504 | Date printed on the notice (typically 30 days) | CAP (Form 9423) — no Tax Court review | State refund can be seized; federal tax lien may be filed |

| LT11 / Letter 1058 | 30 days from the notice date | CDP hearing (Form 12153) with Tax Court review | Full levy power over wages, bank accounts, and property; strongest hearing right downgraded |

Situations that change the CP504 playbook

Married filing jointly. Both spouses are liable for the entire balance, both state refunds are exposed, and both incomes count in any plan or offer calculation. If the debt traces to income one spouse hid from the other, innocent spouse relief may exist — but it's a separate application, and the CP504 clock doesn't wait for it.

Self-employed or 1099. Payment plans and offers require you to be current on this year's estimated taxes, not just the old balance. Fix the quarterly problem in parallel, or the agreement you set up defaults the moment next April's return posts a new balance.

Business balances. Businesses get the CP504B notice instead — same §6331(d) authority, but higher stakes: unpaid payroll taxes can become the owners' and check-signers' personal debt through the Trust Fund Recovery Penalty, and business accounts escalate to revenue officers faster.

Multiple years. Thresholds run on your aggregate assessed balance. Two years of $28,000 each puts you over the $50,000 streamlined line and within sight of the $66,000 passport threshold — resolving all years in one arrangement almost always beats handling them piecemeal.

You dispute the amount. The CP504 stage assumes the tax is final, so "I don't owe this" needs a different track: proof of a misapplied payment, an amended return, or audit reconsideration — while you protect yourself from levy in the meantime, often with a plan you can later adjust.

Genuine hardship. If any payment means skipping rent or medication, Currently Not Collectible exists for exactly this, and the Taxpayer Advocate Service can intervene when the process itself is causing harm.

When you can handle a CP504 yourself — and when help changes the outcome

Honestly: many CP504s don't need professional help. If you agree with the balance, it's a single year under $50,000, and your budget supports a monthly payment, the online streamlined agreement takes about 20 minutes and stops the escalation cold. Add a first-time abatement request and you've likely done everything a pro would do.

Experienced help changes outcomes in specific situations: multiple years with some unfiled (the filing order affects what you owe), business or payroll tax exposure, a balance you dispute, offer-in-compromise math where one wrong figure means rejection after months of waiting, or an LT11 already in the mail behind this notice — where the 30-day CDP window becomes the whole game. In those cases the fee is buying a materially different result, not convenience.

If you're not sure which camp your CP504 falls in, that's precisely what a free case review settles in one call — before the window on your notice closes.

Terms on your CP504, decoded

The official IRS explainer lives at Understanding your CP504 notice; here's the plain-English version of the language you're staring at:

- Levy — the actual taking of money or property: a bank account, a paycheck, a refund.

- Lien — a legal claim attached to everything you own; it takes nothing today but clouds any sale or refinance.

- IRC §6331(d) — the law requiring the IRS to give 30 days' notice before levying; the CP504 is that notice for your state refund.

- Collection Due Process (CDP) — the formal hearing right, with Tax Court review, that attaches to the final notice (LT11/1058), not to the CP504.

- Collection Appeals Program (CAP) — the faster, narrower appeal available at the CP504 stage; it can pause a specific action but can't contest the tax itself.

- CSED — the Collection Statute Expiration Date: the IRS generally has 10 years from assessment to collect, though appeals, offers, and bankruptcy pause that clock.

CP504 notice questions, answered

Is a CP504 the final notice before the IRS levies?

No. The final notice is the LT11 or Letter 1058, which must arrive and sit for 30 days before the IRS can levy wages or bank accounts. The CP504 is the step right before it — it authorizes only a levy of your state tax refund. Treat it as your last low-stakes window: everything after it carries real seizure power.

How long do I have to respond to a CP504 notice?

You typically have 30 days from the date printed on the notice — that exact date is on the front page, and it controls, not the day you opened the envelope. After it passes, the IRS can take your state tax refund and may file a federal tax lien. Interest and the monthly failure-to-pay penalty keep accruing the whole time.

Can the IRS take money from my bank account after a CP504?

Not based on the CP504 alone. A bank or wage levy requires a final notice — the LT11 or Letter 1058 — plus another 30 days for you to request a hearing. What the CP504 does allow is seizure of your state tax refund, and it typically precedes a federal tax lien filing. If you do nothing, the final notice usually follows.

What exactly can the IRS seize after a CP504?

At this stage: your state income tax refund, through the State Income Tax Levy Program. The IRS can also file a Notice of Federal Tax Lien against everything you own. Wages, bank accounts, Social Security, and property require the later final notice and its 30-day window before they're at risk.

Can I still set up a payment plan after getting a CP504?

Yes — a CP504 does not disqualify you from any resolution program. Balances of $50,000 or less generally qualify for an online streamlined installment agreement of up to 72 months, and a short-term plan gives you up to 180 days with no setup fee. Setting one up before the notice date stops the escalation to the final levy notice.

Does a CP504 mean a tax lien has been filed?

Not automatically. The CP504 warns that the IRS may file a Notice of Federal Tax Lien if the balance stays unresolved. Liens no longer appear on consumer credit reports, but they are public record and can block a home sale or refinance. If a lien has already been filed, you'd receive Letter 3172 with its own appeal rights.

Can I appeal a CP504?

Yes, through the Collection Appeals Program (CAP), which can pause a specific action like a state refund levy. What a CP504 does not give you is a Collection Due Process hearing — that stronger right, with possible Tax Court review, only attaches to the later LT11 or Letter 1058. Most people resolve a CP504 by arranging payment rather than appealing.

What is the difference between a CP504 and a CP504B?

They carry the same legal weight — intent to levy under IRC §6331(d) — but the CP504 goes to individuals and the CP504B goes to businesses, typically for payroll or other business tax balances. Business balances escalate faster in practice because unpaid payroll taxes can trigger personal liability for owners and officers.

Will a CP504 affect my passport?

Not by itself. Passport certification applies only to 'seriously delinquent' tax debt — $66,000 or more in 2026 — after a lien or levy notice has been issued. If you owe less than that, your passport isn't at risk yet, but penalties and interest on multiple years can push a balance across the threshold over time.

What if I never got the CP14 or reminder notices before this CP504?

The notices are still legally valid — the IRS only has to mail them to your last known address, which comes from your most recent return. If you moved, file Form 8822 to update your address and check your IRS online account for the full notice history. Missing mail doesn't reset the clock, so act on the CP504 you have.

Your next 24 hours

- Find the notice date and total balance on the front page of your CP504 — top right corner. That date, not today's, is your 30-day anchor for everything else.

- Gather three things: the notice itself, your last filed return, and a quick snapshot of monthly income and expenses. Then log into your IRS online account to confirm the balance and see whether an LT11 is already queued behind it.

- Get your CP504 reviewed free before the date on your notice — the 2-minute form or (888) 825-7779. One call tells you whether a 20-minute online plan solves this or whether your situation needs more.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.