IRS Notices

IRS LT11 Notice: Final Notice of Intent to Levy and Your 30-Day Deadline (2026)

The short answer: an LT11 notice is the IRS's final notice of intent to levy. You have 30 days from the date on the letter to pay, set up a resolution, or file Form 12153 for a Collection Due Process hearing — after that, the IRS can legally seize bank accounts, wages, and 1099 payments without further warning.

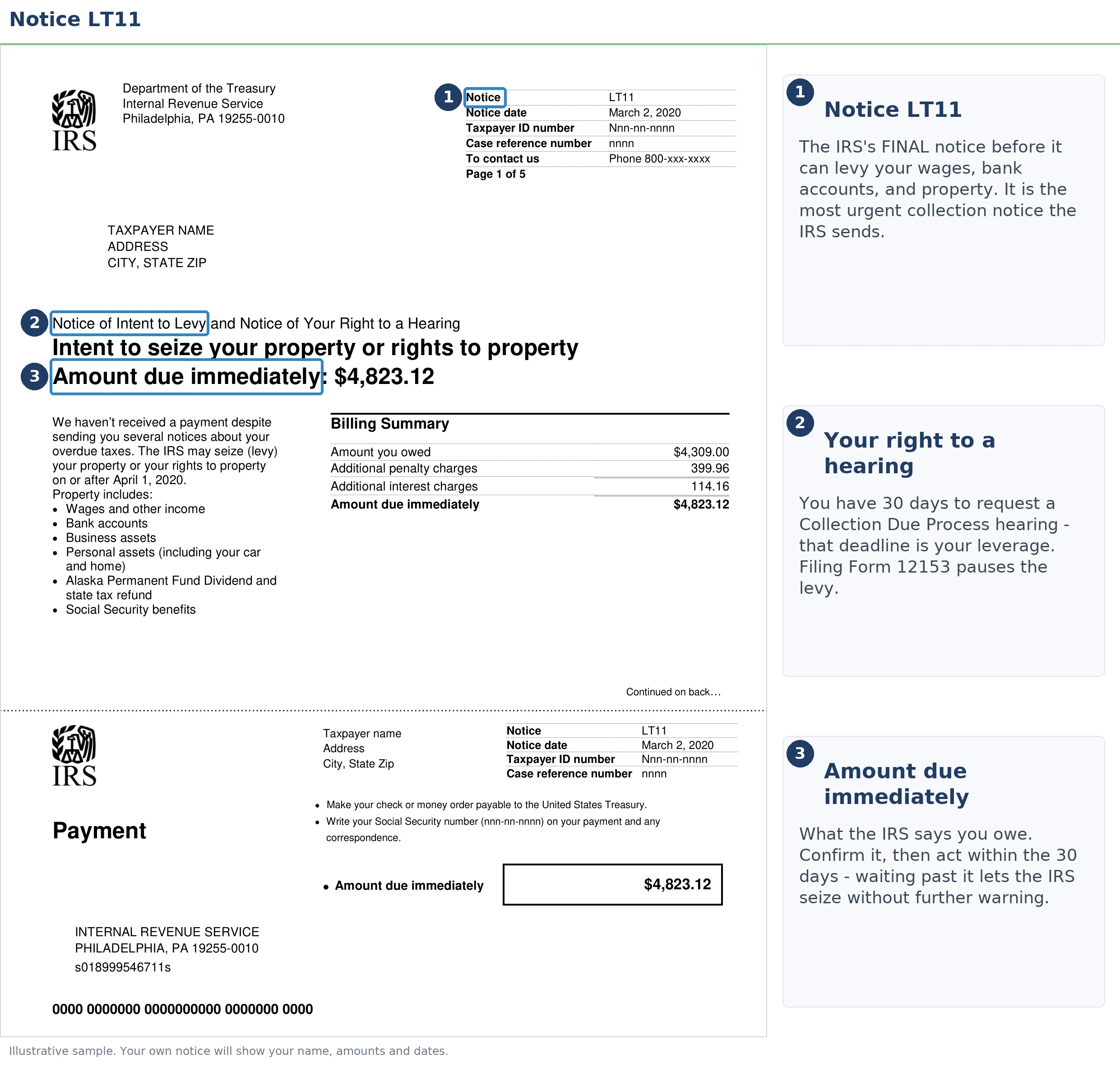

You signed for a certified letter, and the first line reads "Notice of intent to seize (levy) your property or rights to property." If you work for yourself, every dollar you're paid flows through accounts the IRS can now reach — which is exactly why this letter is sent certified. Here's the part the letter buries: the LT11 also hands you the single strongest appeal right in the entire IRS collection process, and the next 30 days are yours to use it.

The image below shows exactly what a real LT11 looks like and where to find the two lines that control everything — the notice date and the hearing-request deadline.

⏱ Your deadline: you have 30 days from the date printed on your LT11 to request a Collection Due Process hearing. File Form 12153 by that date and the IRS legally cannot levy while your case is heard. Let it pass, and full levy authority activates — with no further notice required.

Why you got an LT11 notice

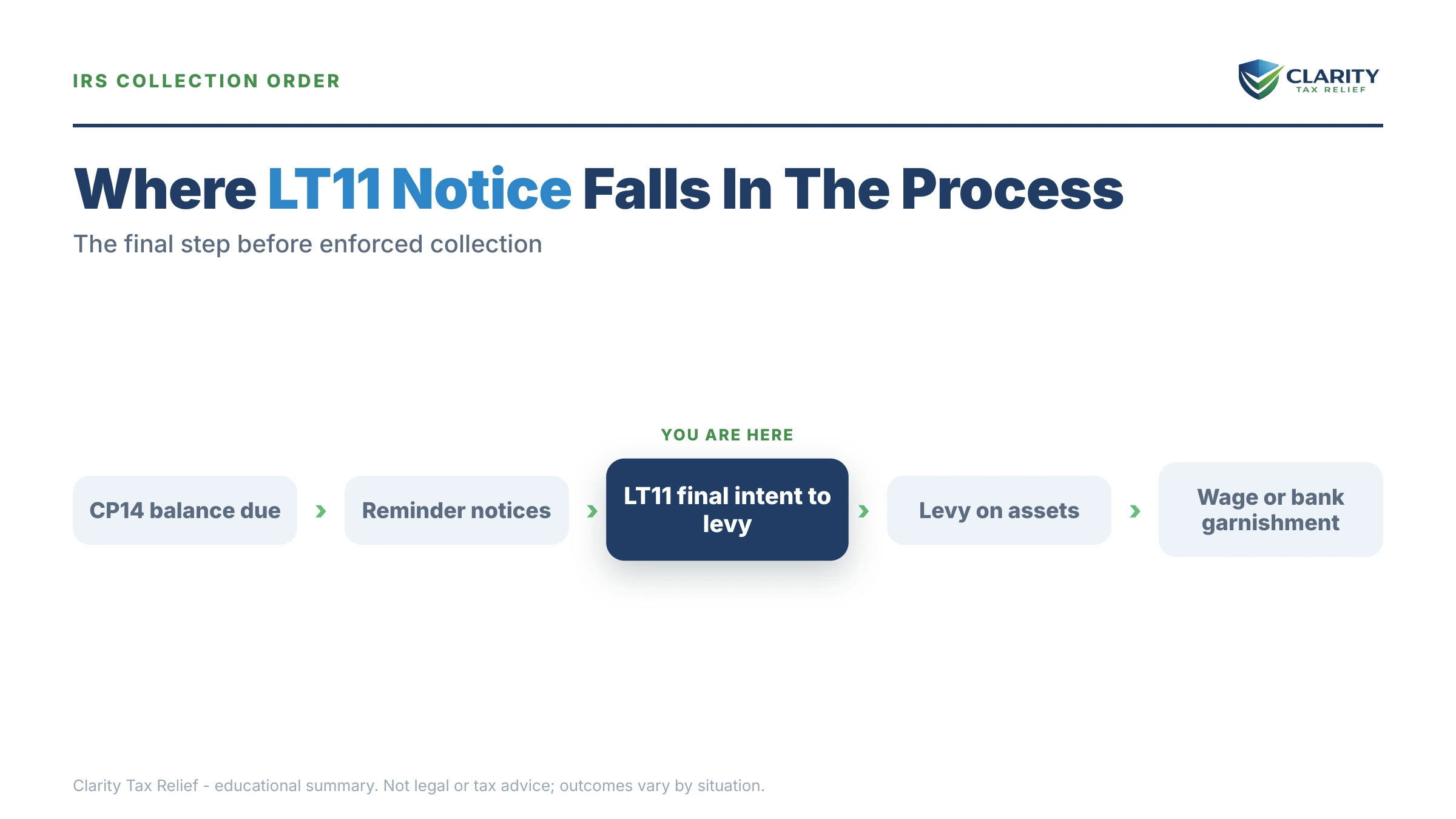

An LT11 is issued by the IRS Automated Collection System (ACS) when a tax balance has gone unpaid through the entire notice sequence — it is the last letter the law requires before a levy. Under IRC §6330, the IRS must give you written notice of its intent to levy and of your right to a hearing at least 30 days before seizing property. The LT11 is that notice.

By the time an LT11 arrives, you've usually already received a bill and reminders, then a CP504 notice threatening your state refund. Some taxpayers also get softer ACS letters first — an LT16 notice asking you to call, or an LT24 notice requesting financial information. The LT11 ends that conversation phase. (For the bigger picture of how IRS mail works, see why did I get a letter from the IRS.)

Three letters carry this same final-notice power, and which one you got tells you who's handling your case. The LT11 comes from ACS — a computer-driven queue with no individual assigned. Letter 1058 is the same notice issued by a revenue officer personally working your file, which means faster, more targeted enforcement. The CP90 notice is a third variant with identical rights. All three start the same 30-day Collection Due Process clock.

| Notice | What it authorizes | Response window |

|---|---|---|

| CP14 | First bill — no enforcement yet | ~21 days from the notice date |

| CP501 / CP503 | Reminder bills — balance grows monthly | The pay-by date printed on each notice |

| CP504 | Levy of your state tax refund only | The date printed on the notice |

| LT11 / Letter 1058 / CP90 | Full levy authority after the CDP window | 30 days (statutory) to file Form 12153 |

| Levy issued | Bank, wage, 1099, and Social Security seizures | Bank funds held 21 days before remitted |

Your 30-day Collection Due Process window: what Form 12153 actually does

Filing Form 12153 within 30 days of your LT11 date legally bars the IRS from levying while an independent Appeals officer reviews your case. That's not a courtesy — it's a statutory right that exists only because you received this specific notice. Our Form 12153 CDP hearing guide walks through the form line by line.

At the hearing you can propose any collection alternative — a payment plan, hardship status, or an Offer in Compromise — and Appeals must consider it before levies resume. If you never had a prior chance to dispute the underlying tax (say, a CP2000 you never received), you can challenge the amount itself. If Appeals rules against you, you can take the decision to Tax Court — the only point in the collection process where a judge reviews an IRS levy decision.

Two trade-offs to know. First, the 10-year collection statute (CSED) pauses while your hearing is pending, so the IRS recovers that time later. Second, if you miss the 30 days, you can still request an "equivalent hearing" within one year — Appeals will listen, but levies aren't barred while it's pending and there's no Tax Court review after.

What happens if you ignore an LT11

Once the LT11's 30-day window closes, the IRS can seize your property without sending you anything else. The sequence from here isn't a series of warnings — it's a series of seizures, issued by automated systems that in 2026 keep running even though the IRS workforce was cut roughly 27% in 2025. The people who could help you answer the phone got scarcer; the computer that issues levies did not.

- Days 1–30: the window is open. No levy can issue. Every option — full CDP rights included — is still on the table.

- Day 31: levy authority activates. Your right to a levy-blocking CDP hearing expires. Only the weaker equivalent hearing remains, and it doesn't stop seizures.

- Bank levy. The IRS freezes whatever is in your account the day the levy lands. Your bank holds the funds for 21 days, then sends them to the Treasury — see IRS bank levy 21 days for how to use that hold.

- Wage and 1099 levies. A W-2 wage levy repeats every payday until released. For contractors, the IRS sends levies straight to your clients and can levy accounts receivable — often before you know it happened.

- Federal payments and state refunds. Up to 15% of Social Security checks through the Federal Payment Levy Program, plus interception of state tax refunds.

- Lien and passport consequences. A federal tax lien can be filed against everything you own, and if your debt tops $66,000 in 2026, the IRS can certify it to the State Department — see passport revoked tax debt.

Nothing in this sequence requires a human decision or another letter. That's what "final notice" means.

Your LT11 clock is already running

A Form 12153 filed on day 29 blocks every levy on this list; the same form on day 31 blocks none of them. Get your LT11 reviewed free before the 30-day window closes — an experienced tax professional will confirm your deadline and map the option that fits your numbers.

What the IRS can levy after the 30 days end

After the LT11 window closes, the IRS can reach nearly every income stream and account you have — but each levy type works differently, and the differences decide your defense. A bank levy is a one-time snapshot; a wage levy is a faucet that stays open. If you're a contractor, the rules that protect a paycheck mostly don't protect you — no exempt-amount table applies to a one-time levy on 1099 pay. You can estimate what a wage levy would leave a W-2 earner with our IRS Wage Garnishment Calculator.

| Target | How the levy works | Key protection |

|---|---|---|

| Bank account | One-time snapshot of the balance the day it lands | Bank holds funds 21 days before remitting — release is possible in that window |

| Wages (W-2) | Continuous — repeats every payday until released | A small exempt amount based on filing status and dependents |

| 1099 / contractor pay | One-time; attaches to what the client owes you that day, and can be re-issued | No exempt-amount table — but each levy must be served fresh |

| Social Security | Automated 15% of each check via the Federal Payment Levy Program | Capped at 15% under FPLP |

| State tax refund | Intercepted in full | None once issued |

| Primary residence | Actual seizure of a home is rare | Requires federal court approval |

Your options after an LT11 notice

Every IRS resolution program is still available at the LT11 stage — the notice changes your deadline, not your menu. What matters is matching the option to your balance and your finances, then getting it in place (or getting Form 12153 filed) before day 30.

| Option | Eligibility | Cost | Stops the levy threat? |

|---|---|---|---|

| Pay in full | Anyone | No fee; stops all accrual | Yes — ends collection entirely |

| Short-term plan (up to 180 days) | Balance you can clear within 6 months | $0 setup; interest and penalties continue | Yes, once approved |

| Streamlined installment agreement | Individuals owing $50,000 or less — up to 72 months online | Setup fee applies; penalty drops to 0.25%/month while active | Yes, while you stay current |

| Currently Not Collectible | Income below IRS allowable living expenses (Form 433-F) | Free; balance keeps accruing | Yes, while the status holds |

| Offer in Compromise | Assets plus future income genuinely below the balance | $205 fee + 20% down (both waived with low-income certification) | Levies generally held while the offer is pending |

| CDP hearing (Form 12153) | Anyone, within 30 days of the LT11 date | Free | Yes — legally bars levy while pending |

| Penalty abatement | Clean 3-year history (first-time abate) or reasonable cause | Free to request | No — reduces the balance, pair it with another option |

Three notes on that table. A streamlined installment agreement requires no financial disclosure under $50,000, which makes it the fastest levy-proof fix for most LT11 balances. Currently Not Collectible status pauses collection but not the debt — interest keeps accruing while the 10-year statute keeps running. And an Offer in Compromise is real but means-tested: the IRS accepted roughly 1 in 5 offers in FY2024, so read how an offer in compromise works before anyone charges you to file one.

On penalties, one 2026 update: starting this summer, the IRS's new Automatic Exemption from Penalty (AEP) begins replacing first-time penalty abatement — qualifying penalties come off automatically, with no request needed. If your LT11 balance is padded with penalties, check whether relief applies before you agree to pay them.

Worked example: a 1099 contractor with $16,400 on an LT11

Say you're a self-employed contractor holding an LT11 for $16,400 — a year of underpaid quarterlies plus the penalties and interest that grew on top. Here's how the real options price out (hypothetical numbers, shown so you can run your own):

- Streamlined installment agreement. At $16,400 you're under the $50,000 online ceiling, so no financial statement is required. The 72-month minimum is $16,400 ÷ 72 ≈ $228/month. Interest still accrues, but the failure-to-pay penalty drops to 0.25% per month once the agreement is active — so budgeting $350/month instead retires the debt years sooner and cuts total accrual meaningfully.

- Offer in Compromise check. Suppose you net $4,600/month and IRS allowable expenses come to $4,350 — that's $250/month of "disposable" income. The lump-sum formula is disposable × 12 plus asset equity: ($250 × 12) + $1,500 in equity = $4,750. But the IRS also sees that $250/month over 72 months would full-pay $16,400 — exactly the profile that gets steered to a payment plan instead of a settlement. That's the honest reason acceptance runs about 1 in 5.

- Do nothing. One levy served on your biggest client the week they owe you a $6,000 invoice takes all $6,000 — no exempt amount, no 21-day hold, and a client who now knows you have an IRS problem.

For this contractor, the winning move is usually the installment agreement set up inside the 30-day window — or Form 12153 filed with the agreement proposed at the hearing if the numbers need negotiating.

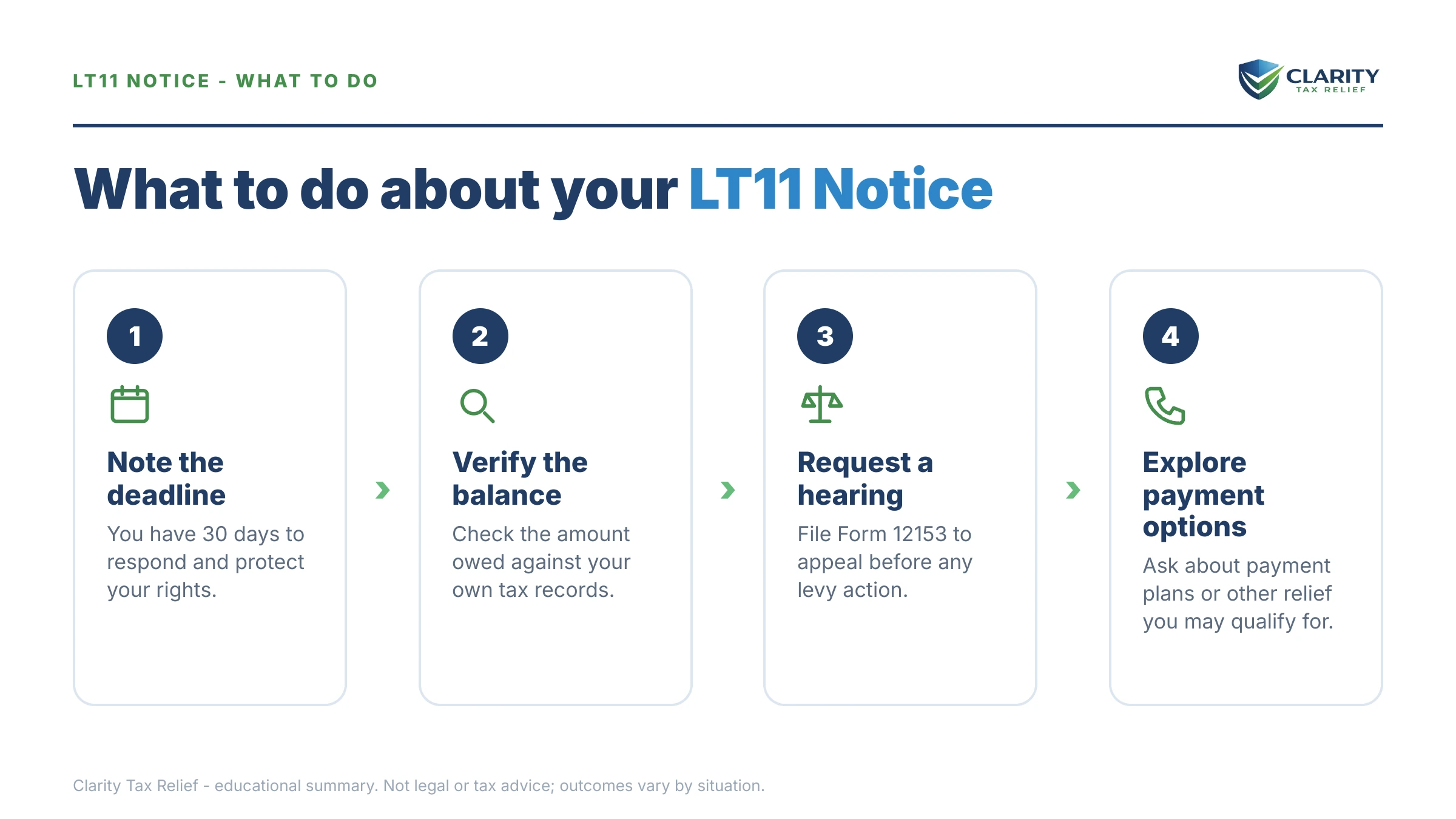

How to respond to an LT11 notice, step by step

- Find your deadline. Locate the date printed on your LT11 and count 30 days forward — that is the last day to request a Collection Due Process hearing.

- Verify the balance. Log into your IRS online account and confirm the amount and tax years on the notice match the IRS's records and your own.

- Choose your path. Decide between paying at IRS.gov/payments, a payment plan, hardship status, an Offer in Compromise, or disputing the debt — the options table above shows what each requires.

- File Form 12153 if you need protection. If you can't resolve the balance before day 30 or you dispute it, send the CDP request before the deadline — it legally blocks levies while Appeals reviews your case.

- Set up the resolution. Establish your agreement online or by phone, get written confirmation, and keep copies of everything you send, including proof of mailing for Form 12153.

- Get experienced help for the hard cases. If a levy is already out, returns are unfiled, or the balance is large, have an experienced tax professional review the case before the window closes.

The official request form and instructions are at the IRS's About Form 12153 page. Mail it to the address on your LT11 — not a generic IRS address — and use certified mail so you can prove the date.

Situations that change your LT11 playbook

You're self-employed or paid on 1099

Levies on contractor income don't follow paycheck rules — each levy grabs 100% of what a client owes you that day. The IRS can also levy your accounts receivable and your business bank account, which can end a contracting business faster than any wage garnishment. See IRS levy independent contractor for the mechanics, and know that any resolution will require you to be current on this year's estimated taxes.

You have unfiled returns

The IRS generally won't approve a payment plan or offer — and Appeals won't grant a collection alternative at a CDP hearing — while required returns are missing. If you also received an LT26 notice demanding overdue returns, filing them is step one; it often shrinks the balance too, especially if the IRS estimated your income without your deductions.

You dispute the amount

If you never had a prior opportunity to contest the tax — a CP2000 or audit notice that went to an old address, for example — the CDP hearing lets you challenge the liability itself, not just how it's collected. That's a right you lose if the 30 days pass, so a disputed balance is the strongest reason of all to file Form 12153 on time.

The debt is from a joint return

Both spouses are fully liable for a joint balance, and each spouse must receive their own final notice. If the debt traces to your spouse's income or errors, innocent-spouse relief can be raised at the CDP hearing — another issue that's easier to assert inside the window than after a levy lands.

You genuinely can't pay anything

If paying the IRS would leave you unable to cover basic living expenses, Currently Not Collectible status stops levies while the hardship lasts. And if your AGI is at or below 250% of the federal poverty level, the OIC low-income certification waives the $205 fee, the 20% down payment, and payments during review — which can put a settlement within reach for taxpayers who assumed they couldn't afford to apply.

When you can handle an LT11 yourself — and when help changes the outcome

You can likely handle this alone if the balance is accurate, your returns are filed, and you can either pay within 180 days or qualify for a streamlined agreement online — that setup takes under an hour and immediately neutralizes the levy threat. A single tax year, an amount you agree with, and steady income is a DIY case.

Experienced help changes outcomes in the harder fact patterns: the 30-day window is nearly gone, a levy has already hit a bank account or client, multiple years are unfiled, the debt involves a business or payroll taxes, you dispute the liability, or the OIC math is genuinely close. In those cases the sequence you fix things in — returns, then penalties, then the balance — often determines what you ultimately pay, and a CDP hearing argued well is very different from one argued blind. If the IRS itself is the obstacle (lost paperwork, a levy causing verified hardship you can't get released), the Taxpayer Advocate Service is a free, independent escalation path.

If your window is already short or a levy is in motion, a free LT11 case review with an experienced tax professional — (888) 825-7779 or the 2-minute form — can map the fastest release path before your next payday or invoice.

Terms on your LT11, decoded

- Levy vs. lien: a levy takes your property; a lien is a legal claim against it that secures the debt without taking anything yet.

- Collection Due Process (CDP) hearing: the independent Appeals review your LT11 entitles you to — request it within 30 days and levies are barred while it's pending.

- Equivalent hearing: the backup version available up to one year after the notice date; Appeals still listens, but levies aren't blocked and there's no Tax Court review.

- Form 12153: the one-page form that requests either hearing — the deadline is measured by the date on your notice, not the day you opened it.

- CSED: the Collection Statute Expiration Date — the IRS generally has 10 years from assessment to collect, paused by CDP hearings, offers, and bankruptcy.

- Continuous levy: a levy that repeats automatically (wages, Social Security) until released, unlike the one-time snapshot levies on bank accounts and 1099 pay.

The IRS's own explanation of this notice is at Understanding your LT11 notice or Letter 1058.

LT11 questions, answered

How serious is an LT11 notice from the IRS?

An LT11 is the most serious collection notice most taxpayers ever receive — it is the legal prerequisite the IRS must send before levying your bank account or wages. Once the 30-day window printed on it passes, no further warning is required before money is taken. It is also the notice that grants your strongest appeal right, a Collection Due Process hearing, so it opens a door at the same moment it closes one.

What is the difference between an LT11 and Letter 1058?

They carry identical legal force — both are the final notice of intent to levy with the same 30-day Collection Due Process rights. The difference is who sent it: an LT11 comes from the IRS's Automated Collection System, while Letter 1058 comes from a specific revenue officer assigned to your case. A Letter 1058 signals a human is actively working your file, which usually means faster enforcement if you don't respond.

What is the difference between an LT11 and a CP504?

A CP504 authorizes the IRS to seize only your state tax refund; an LT11 is the final notice that authorizes levies on bank accounts, wages, and most other income. The CP504 comes earlier in the sequence and does not carry Collection Due Process rights — the LT11 does. If you received a CP504 and did nothing, the LT11 is the escalation that follows.

Does filing Form 12153 stop the IRS from levying?

Yes — a Collection Due Process request filed within the 30-day window legally bars the IRS from levying while your hearing is pending, with narrow exceptions such as jeopardy situations. Collection stays on hold through the Appeals hearing and, if you disagree with the result, through Tax Court review. The trade-off is that the 10-year collection statute pauses during the hearing, so the IRS gets that time back on the far end.

What happens if I miss the 30-day deadline on my LT11?

You lose the levy-blocking version of the hearing, but not every option. Within one year of the notice date you can still request an "equivalent hearing" on the same Form 12153 — Appeals will hear your case, but the IRS may levy while it's pending and you can't take the result to Tax Court. Payment plans, hardship status, and an Offer in Compromise all remain available at any point.

Can the IRS levy my bank account right after the 30 days end?

Legally, yes — once the 30-day window closes, the IRS can issue a levy without any further notice to you. In practice, a bank levy freezes whatever is in the account on the day it lands, and the bank holds the funds for 21 days before sending them to the IRS — that hold is your last realistic window to get the levy released. Wage levies have no such hold; they run every payday until released.

Will an LT11 lead to losing my passport?

Not by itself — passport certification is a separate process triggered by "seriously delinquent" tax debt, which in 2026 means more than $66,000 with a levy issued or lien filed. If your balance is under that threshold, the LT11 doesn't touch your passport. If you're over it, the levy authority the LT11 creates is often the step that makes certification possible, so resolving before the window closes matters even more.

Can the IRS garnish my 1099 income after an LT11?

Yes. Once the LT11 window passes, the IRS can send levies directly to your clients and payers — but a levy on contractor pay only attaches to money the client owes you on the day the levy is served, unlike a W-2 wage levy that repeats every payday. The IRS can re-issue those levies, and it can also levy accounts receivable, which for many contractors is more damaging than a wage garnishment.

Does requesting a CDP hearing extend the 10-year collection statute?

Yes — the collection statute (CSED) is suspended while your CDP hearing and any Tax Court review are pending, then the clock resumes. For most people the trade is worth it: the hearing stops levies and forces the IRS to consider your payment plan, hardship, or settlement proposal before taking anything. But if your debt is close to expiring, pausing the clock can work against you — check your CSED before filing.

Your next 24 hours

- Find the notice date at the top of your LT11 and count 30 days forward. Write that date somewhere you'll see it — it's the last day Form 12153 can block a levy.

- Gather three things: the LT11 itself, your most recent filed return, and your income records (1099s and bank statements for the last few months) — everything any option requires is in that stack.

- Get the free case review — the 2-minute form or (888) 825-7779 — while the full 30 days are still on the clock, so an experienced tax professional can confirm your deadline and lock in the right move before levy authority activates.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.