Tax Forms & Surprise Income

1099-C Cancelled Debt Taxes: What You Owe and How to Fix It in 2026

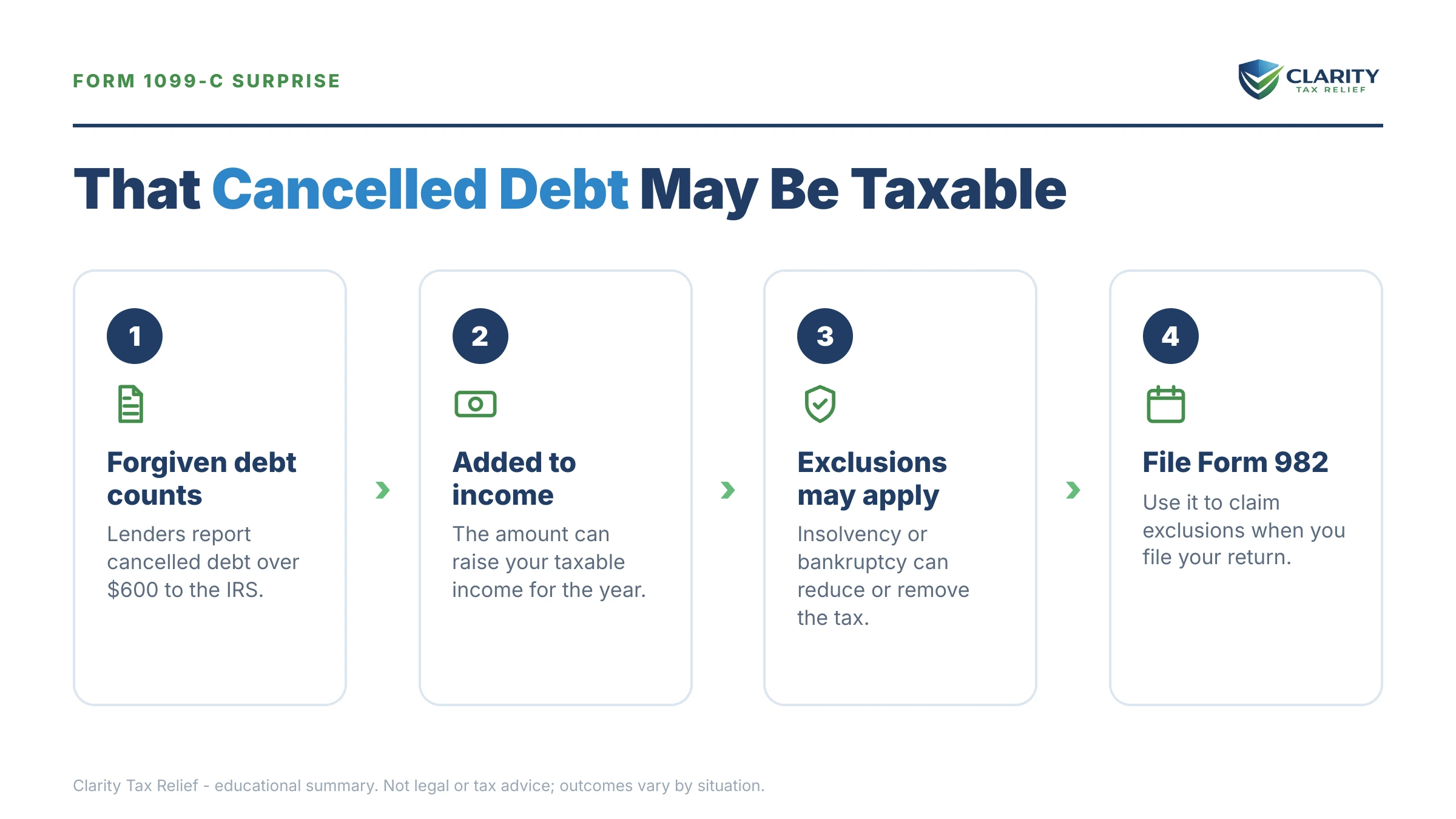

The short answer: 1099-C cancelled debt taxes work like this — when a creditor forgives $600 or more of your debt, the forgiven amount generally counts as taxable income for that year. But if you were insolvent when it was cancelled, Form 982 can legally exclude some or all of it, often cutting the tax to zero.

The debt was supposed to be behind you. You settled the account, the calls stopped — and then a form showed up saying the amount the creditor wrote off is income, and now the IRS wants tax on money you never actually held. If the letters have already escalated to a levy warning, the pressure feels backwards: you're being chased for taxes precisely because you couldn't pay a debt.

Here's the part almost nobody tells you: the same thin finances that forced the settlement are often exactly what erases the tax. If your debts outweighed what you owned when the debt was cancelled, the law says some or all of that "income" doesn't count. This page walks you through the test, the form, and every option if tax is genuinely owed. The image below shows exactly what a 1099-C looks like and where to find the two boxes that decide everything — the amount and the event code.

⏱ The real clocks: a 1099-C has no reply deadline of its own — it flows into your tax return for the year shown in Box 1. But once the IRS assesses tax on it, a 0.5% monthly failure-to-pay penalty plus interest accrue until resolved. And if you're holding an LT11 or Letter 1058 final notice, you have 30 days from the date on that letter to request a Collection Due Process hearing before a levy can proceed.

Why you got a 1099-C

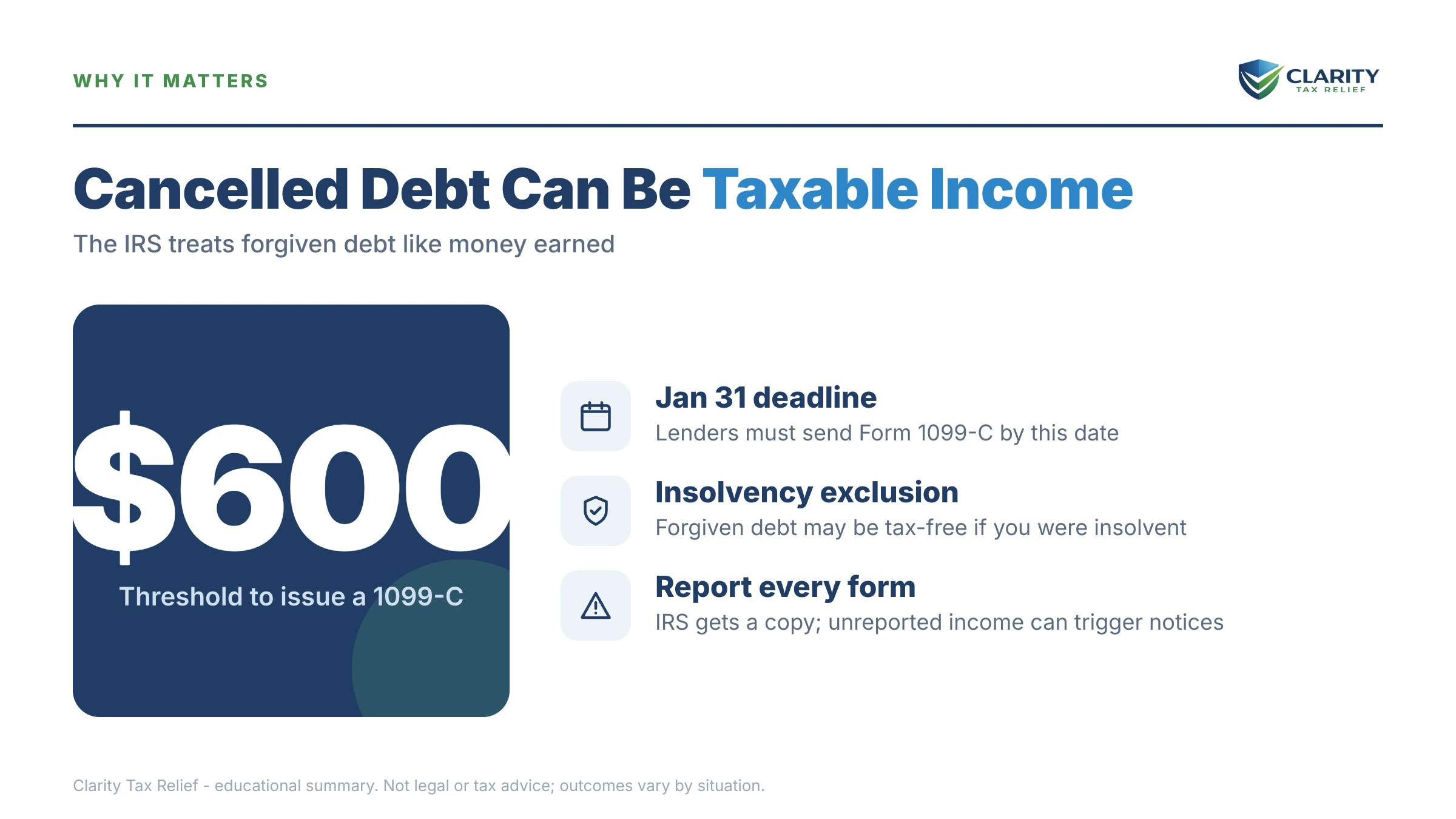

A creditor must file Form 1099-C with the IRS whenever it cancels $600 or more of your debt. The most common triggers: you settled a credit card or personal loan for less than the balance, a lender charged off an account and formally stopped collecting, a car was repossessed with a forgiven shortfall, or a home was foreclosed.

The creditor sends one copy to you and one to the IRS. That second copy is why this form can't simply be ignored — the IRS's matching system already expects to see the Box 2 amount on your return. If a 1099 of any kind landed that you didn't see coming, our guide to a surprise 1099 you weren't expecting covers how to verify any of them.

One important distinction: a 1099-C reports debt that was forgiven, not money you were paid. If your form is actually a 1099-K reporting payments you received through an app or platform, that's a different problem with different rules — see the 1099-K $20,000 threshold guide instead.

What the boxes on Form 1099-C mean

Two boxes on the form control your entire tax outcome: Box 2 (the amount cancelled) and Box 6 (the reason it was cancelled). Box 1 gives the cancellation date — the date your insolvency is measured against — and Box 7 shows the property's fair market value when a foreclosure or repossession is involved. The image below shows you exactly where each of these sits on the form.

| Code | What it means | What to do |

|---|---|---|

| A | Discharge in bankruptcy | Excludable in full — check the bankruptcy box on Form 982 and keep your discharge order. |

| B | Other judicial debt relief | Gather the court paperwork; run the insolvency test for anything not covered by it. |

| C | Statute of limitations or deficiency period expired | Often disputable — the debt may have become uncollectible years earlier. Verify the Box 1 year. |

| D | Foreclosure election | Property rules apply; check Box 7 and any Form 1099-A you received for the same property. |

| E | Debt relief through probate or similar proceeding | Confirm whose return it belongs on — a decedent's debt may not be yours to report. |

| F | Cancellation by agreement (settlement) | The most common code. Run the insolvency test as of the settlement date. |

| G | Creditor's decision or policy to discontinue collection | Frequently issued years late — verify the year is right before accepting it as income. |

| H | Other actual discharge | Ask the creditor in writing what triggered it, then test for exclusions. |

The insolvency exclusion: why renters often owe far less than the form says

The insolvency exclusion lets you remove cancelled debt from income up to the amount your total debts exceeded your total assets immediately before the cancellation. You claim it on Form 982 using the insolvency exclusion, filed with the return for the year in Box 1.

This rule quietly favors people who rent. No home equity means the asset side of the test stays small — but be careful: the test counts everything you owned at fair market value, including retirement accounts, your car, and bank balances. Publication 4681 includes the worksheet the IRS expects you to keep as proof.

A worked example (hypothetical). Say a card issuer settled your $18,000 balance for $6,700 and cancelled the remaining $11,300. Reported as income in the 22% bracket, that adds roughly $2,486 of federal tax ($11,300 × 0.22).

Now run the insolvency test as of the day before the settlement. Assets: a car worth $6,500, $900 in checking, $2,400 in a 401(k), and about $1,700 in personal property — $11,500 total. Debts: the full $18,000 card balance, $5,300 on other cards, and $4,000 in medical bills — $27,300 total. You were insolvent by $15,800 ($27,300 − $11,500). Because $15,800 is more than the $11,300 cancelled, you can exclude the entire amount. Tax owed: $0.

If the numbers had shown you insolvent by only $7,000, you'd exclude $7,000 and report the remaining $4,300 — about $946 of tax at 22%. The exclusion is dollar-for-dollar up to your insolvency, never all-or-nothing.

What happens if you ignore cancelled debt income

Leaving a 1099-C off your return doesn't hide it — the IRS already has the creditor's copy, and the matching sequence that follows is automated. Here is the order of escalation:

- Document matching flags the gap. The IRS compares the Box 2 amount against your return, typically well after you filed.

- A CP2000 notice proposes the tax — plus, in many cases, a 20% accuracy-related penalty. The response deadline is printed on the notice; this is the cheapest place to fix it, because Form 982 can still be applied here.

- No response → assessment. After a statutory notice of deficiency, the balance becomes a legal debt and the collection bills begin (CP14, then reminders).

- A CP504 notice arrives — the IRS can now take your state tax refund, and a federal tax lien becomes a live risk.

- An LT11 notice or Letter 1058 starts a 30-day clock. After it runs, the IRS can levy your bank account (funds are held 21 days before they leave) or garnish wages continuously until the debt is resolved or released.

If you're already at that last stage, the math on a wage levy is brutal — the IRS leaves you an exempt amount and takes the rest. You can estimate what a levy would leave you with our IRS Wage Garnishment Calculator. And in 2026, with IRS staffing down sharply, these levies are issued by systems, not people — the escalation doesn't pause because nobody answers the phone.

Facing a levy over cancelled-debt tax?

If you were insolvent when the debt was cancelled, the assessment itself may be reducible — and if a final notice has arrived, the 30-day window on that letter is real. Send us your 1099-C and IRS letters for a free review before you agree to pay a number that may never have been right. Call (888) 825-7779 or use the 2-minute form.

Your options for 1099-C cancelled debt taxes you can't pay

Before choosing how to pay, always check whether the number is right — an exclusion filed late still beats a payment plan on tax you never owed. If tax genuinely remains, the IRS has several programs; the full DIY playbook is in our guide on how to settle tax debt yourself, and the table below shows which option fits which situation.

| Option | Typical eligibility | Cost & notes |

|---|---|---|

| Amended return / CP2000 response with Form 982 | You were insolvent (or in bankruptcy) at cancellation | No IRS fee. Reduces the tax itself — do this before any payment option. |

| Short-term payment plan | Can pay in full within 180 days | $0 setup. Interest and the 0.5%/month penalty continue, but enforcement stops. |

| Long-term installment agreement | Balance ≤ $50,000 (online), up to 72 months; balances ≤ $10,000 qualify for a guaranteed installment agreement | Setup fee varies (lower with direct debit). Interest and penalties keep accruing. |

| Currently Not Collectible status | Paying anything would leave you unable to cover basic living expenses | No fee; requires financial disclosure. Pauses levies — the debt and interest remain. |

| Offer in Compromise | Assets plus future income genuinely can't cover the debt before the collection statute runs | $205 fee and 20% down for lump-sum offers (both waived with low-income certification). The IRS accepted roughly 1 in 5 offers in FY2024 — real, but means-tested. |

| First-time penalty abatement | Clean compliance history for the prior 3 years | Free to request; removes penalties, not tax. From summer 2026, the new Automatic Exemption from Penalty (AEP) applies many of these removals automatically. |

One nuance for the CP2000 stage specifically: if you agree the cancelled debt is taxable but can't pay, say so on the response — agreeing to the tax while requesting a payment arrangement prevents the accuracy penalty fight from dragging into assessment by default.

How to respond to a 1099-C, step by step

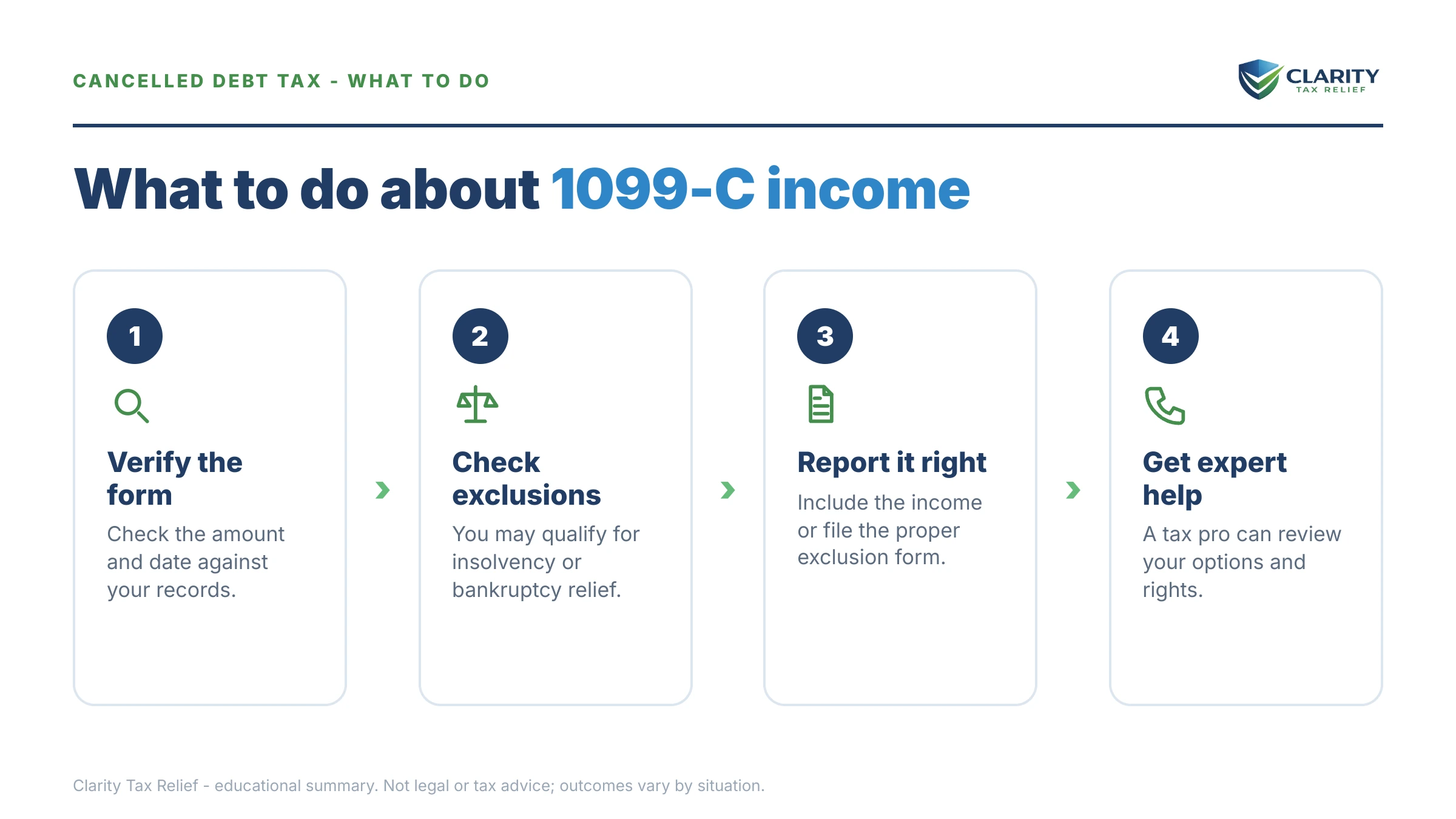

- Verify the form. Check Box 1 (cancellation date), Box 2 (amount cancelled), and Box 6 (event code) against your settlement paperwork. If the year or amount is wrong, dispute it with the creditor in writing and request a corrected form.

- Run the insolvency test. List every debt you owed and the fair market value of everything you owned immediately before the cancellation date. If debts exceeded assets, you can exclude cancelled debt up to that difference.

- File Form 982 with the right return. Attach Form 982 to the return for the year shown in Box 1 — or amend that return if you already filed without it. Keep your insolvency worksheet in case the IRS asks for proof.

- Arrange payment on any tax genuinely owed. If part of the cancelled debt is taxable, set up a short-term payment plan (up to 180 days) or an installment agreement at IRS.gov before the collection notices escalate.

- Protect yourself from a levy. If an LT11 or Letter 1058 final notice has arrived, request a Collection Due Process hearing with Form 12153 within 30 days of its date — and get an experienced tax professional involved if a levy is already in motion.

If you already filed without Form 982 and the IRS has assessed the tax, the fix runs through amending a return to lower a tax debt or audit reconsideration — and if a final notice is in hand, the CDP hearing via Form 12153 is the tool that legally pauses the levy while the numbers get corrected.

When you can handle this yourself

Many 1099-C situations don't need professional help. If you haven't filed yet, have one form, and are clearly solvent — pay the tax with the return or set up a plan online. If you're clearly and deeply insolvent with simple finances, the Publication 4681 worksheet plus Form 982 is genuinely a DIY job: one form, one worksheet, attached to one return.

Experienced help changes outcomes in four situations: a levy is already in motion or a final notice clock is running; the IRS has assessed tax on a year that needs to be reopened with Form 982 after the fact; the insolvency math is close or complicated (retirement accounts, a co-signed debt, a vehicle worth more than you think); or the form involves foreclosed or repossessed property, where recourse-versus-nonrecourse rules and a companion 1099-A change the answer entirely. In those cases, the order you fix things in — assessment first, penalties second, payment terms last — usually determines what you end up paying.

The primary sources are worth bookmarking: the IRS pages for Form 1099-C and Form 982, and the official IRS payment plan page for setting up an agreement directly.

Terms on your 1099-C, decoded

- Cancellation of debt (COD) income: the tax law's name for forgiven debt treated as income — you're taxed because you received value (the loan) you no longer have to repay.

- Identifiable event: the specific trigger (settlement, charge-off policy, statute expiration) that legally required the creditor to file the form, coded in Box 6.

- Insolvency: owing more than you own — measured at fair market value, immediately before the cancellation, counting every asset including retirement accounts.

- Form 982: the one-page form that tells the IRS which exclusion (bankruptcy, insolvency, and others) removes the Box 2 amount from your income.

- Fair market value (FMV): what an asset would actually sell for today — not what you paid for it — and the number Box 7 reports for property in a foreclosure.

- Recourse vs. nonrecourse debt: whether the lender could pursue you personally beyond the collateral; it determines whether a foreclosure produces COD income at all.

1099-C questions, answered

Do you have to pay taxes on a 1099-C?

Usually yes — cancelled debt of $600 or more generally counts as taxable income for the year in Box 1 of the form. But the tax code carves out real exceptions: debt discharged in bankruptcy is excluded in full, and debt cancelled while you were insolvent can be excluded up to the amount of your insolvency using Form 982. Many people who run the insolvency math correctly owe far less than the form suggests — sometimes nothing.

How much tax will I owe on cancelled debt?

The cancelled amount is added to your ordinary income and taxed at your marginal rate. For example, $11,300 of cancelled debt in the 22% bracket adds roughly $2,486 of federal tax, before any state tax. The extra income can also shrink income-based credits like the Earned Income Tax Credit, so the true cost can be higher than the bracket math alone — unless an exclusion removes some or all of it.

What if I was insolvent when the debt was cancelled?

You can exclude cancelled debt from income up to the amount your total debts exceeded the fair market value of your total assets immediately before the cancellation. You claim it by filing Form 982 with the return for that year and keeping an insolvency worksheet (Publication 4681 includes one) as proof. Retirement accounts count as assets in this test, which surprises many people — run the numbers before assuming you qualify or don't.

What happens if I don't report a 1099-C?

The creditor sent the same form to the IRS, so its document-matching system flags the missing income — usually well after you filed. You'll typically receive a CP2000 notice proposing the extra tax plus a possible 20% accuracy-related penalty, and if you don't respond, the amount is assessed and moves into the collection notice stream, which ends at levies. Responding to the CP2000 with Form 982 at that stage can still reduce or remove the proposed tax.

I got a 1099-C years after I stopped paying the debt — is that allowed?

It happens often, especially with Box 6 Code G (creditor's decision to stop collection), and the year the creditor picks matters enormously. Your insolvency is measured on the cancellation date shown on the form — you may have been deeply insolvent when you defaulted but solvent by the year the creditor finally filed. If the date or amount looks wrong, dispute it with the creditor in writing and ask for a corrected form before the IRS assesses tax on the wrong year.

Does a 1099-C mean the creditor can no longer collect the debt?

Not automatically. The form is a tax-reporting document, and whether the underlying debt is still legally collectible depends on your state's law and the facts of the discharge. A Code F settlement agreement usually means the debt is contractually resolved; a Code G policy decision is murkier. If a collector contacts you about a debt that was already reported on a 1099-C, get the form and your settlement paperwork in front of them before paying anything.

Can I claim insolvency after the IRS has already billed me?

Yes. If you're inside a CP2000 window, respond with Form 982 and your insolvency worksheet before the deadline on the notice. If the tax was already assessed, you can file an amended return for that year, or request audit reconsideration with the same documentation. Reducing the assessment itself is almost always better than negotiating payment terms on a number that was never right — do this step before you agree to a payment plan.

Is a 1099-C from a foreclosure or repossession treated differently?

Yes — property changes the math. With recourse debt, the foreclosure is treated as a sale at fair market value (often shown in Box 7), and only the forgiven shortfall is cancellation-of-debt income; with nonrecourse debt, there is generally no COD income at all. You may also receive a Form 1099-A for the property transfer itself. These cases mix capital-gain rules with COD rules, so they're worth a professional review before you file.

Your next 24 hours

- Find three things on your 1099-C: the date in Box 1, the amount in Box 2, and the code in Box 6. If an IRS letter came with a levy warning, find the notice date and the deadline printed on it — if it's an LT11 or Letter 1058, the 30-day hearing window runs from that date.

- Gather your numbers: a list of everything you owed and everything you owned around the Box 1 date, your settlement letter, the tax return for that year, and every IRS notice you've received.

- Get the free case review. Interest and the monthly failure-to-pay penalty keep accruing on any assessed balance while you wait — send your 1099-C and letters through the 2-minute form or call (888) 825-7779 and an experienced tax professional will tell you whether the tax itself can be reduced before you pay a dime of it.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.