IRS Forms & Appeals

Form 12153 CDP Hearing: How to Stop a Levy Before the 30-Day Deadline (2026)

The short answer: Form 12153 is the IRS form that requests a Collection Due Process (CDP) hearing. File it within 30 days of the date on your LT11, Letter 1058, CP90, or Letter 3172, and levy action generally pauses while the IRS Independent Office of Appeals reviews your case — with Tax Court review preserved.

You got a final notice of intent to levy — probably by certified mail — and buried in it was a line about your "right to a hearing." Someone said the words "Form 12153 CDP hearing," and now you need to know if it's real protection or paperwork. It's real: this two-page form is the strongest legal brake a taxpayer has on IRS collection, but only if it's postmarked in time.

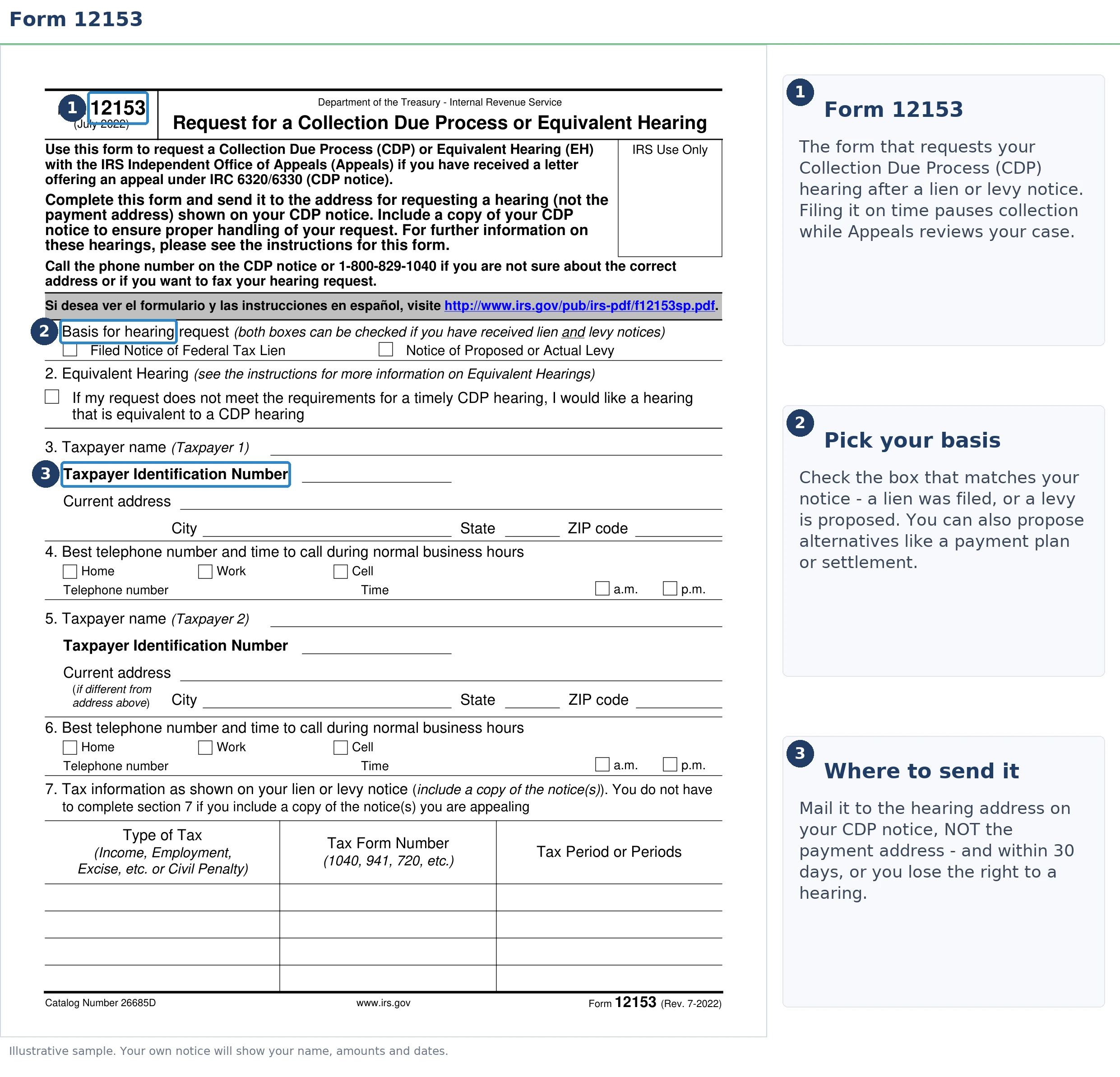

Form 12153 asks two questions that decide everything: which action you're appealing (levy, lien, or both) and what you want instead. The image below shows exactly what the form looks like and where those key sections sit, so keep reading before you fill anything in. If you're not even sure which letter you're holding, start with our guide to why did I get a letter from the IRS.

⏱ Your deadline: You have 30 days from the date printed on your final notice (LT11, Letter 1058, CP90, or Letter 3172) to file Form 12153 and keep full CDP rights. After day 30 you can still request an "equivalent hearing" for up to one year — but you lose the automatic levy pause and the right to Tax Court review. The clock runs from the notice date, not the day the mail arrived.

Which notices give you Form 12153 hearing rights — and why you got one

Only a handful of IRS letters trigger the right to file Form 12153: the final levy notices — LT11, Letter 1058, and CP90 — and the lien-filing notice, Letter 3172. Under IRC §6330, the IRS must offer you one independent hearing before it levies your wages, bank accounts, or federal benefits, and one after it files a Notice of Federal Tax Lien.

If you received one of these letters, it means the earlier bills in the collection sequence went unanswered — or, in the lien case, that the IRS has already recorded its claim against your property. Either way, the letter itself is the trigger: no other notice (not a CP14, not a CP504) starts CDP rights, and no other form invokes them.

One form covers two very different appeals. The levy hearing happens before the IRS takes anything, so it can prevent the seizure entirely. The lien hearing happens after filing, so it's about getting the lien withdrawn, released, or made livable. Check the box that matches your letter — or both boxes if you received both letters.

What filing Form 12153 actually does

A timely Form 12153 generally suspends IRS levy action on the tax periods in your request while the hearing is pending. That's the headline benefit: the automated collection machine has to stand down on those years until the Independent Office of Appeals — a unit separate from Collection — issues a written determination. In 2026, with IRS staffing down roughly 27% but automated levies running uninterrupted, this legal pause is often the only reliable way to make the system stop and listen.

There's a trade-off you should understand before you file. A timely CDP request also suspends the 10-year collection statute (the CSED) while the hearing and any court review are pending — meaning the IRS gets that time back on the far end. If your debt is old, check how much collection time remains first; our guide to how long the IRS can collect back taxes explains the rules, and our CSED Calculator can help you estimate your own expiration date. For a debt with two years left on the clock, tolling it for a hearing may cost more than it protects.

One more nuance: the protection only covers the tax periods you list on the form. If your notice covers 2021, 2022, and 2023 and you write only "2023," the IRS can still levy for the other two years. List every period shown on the notice.

What happens if you miss the 30 days — or do nothing at all

Missing the 30-day Form 12153 deadline converts your full CDP hearing into an equivalent hearing and clears the IRS to levy. The stages unfold in a fixed order:

- Day 30 passes. Your right to a levy-pausing CDP hearing expires. The IRS is now legally authorized to levy for the periods on the notice, whether or not it acts immediately.

- Levies begin. A bank levy freezes the balance with a 21-day hold before the bank sends the money; a wage levy is continuous until released; and Social Security benefits can lose up to 15% per check through the Federal Payment Levy Program — see the 15% Social Security levy.

- The lien follows (or precedes). If a Notice of Federal Tax Lien hasn't been filed yet, an unresolved balance at this stage makes one likely, attaching the government's claim to everything you own.

- One year passes. Even the equivalent-hearing window closes. You can still appeal specific collection actions through a CAP appeal or negotiate directly with Collection — but the independent-review-with-court-backstop moment is gone for those notices.

Nothing in that sequence requires a human at the IRS to decide anything. The escalation is automated; the pause is not. The pause only happens if you file.

Holding a final notice with the 30-day clock running?

Send us a photo of your LT11 or Letter 3172. An experienced tax professional will confirm your exact filing deadline, tell you whether Form 12153 is the right move for your CSED, and map what to ask for at the hearing — free, before the window closes.

CDP hearing vs. equivalent hearing: the rights you keep or lose

The filing date on your Form 12153 — not what you write on it — determines which of three very different outcomes you get.

| When you file Form 12153 | Hearing you get | Rights you keep — or lose |

|---|---|---|

| Within 30 days of the notice date | Collection Due Process (CDP) hearing | Levy action generally paused; CSED suspended; right to petition the U.S. Tax Court within 30 days of the determination |

| Day 31 through one year | Equivalent hearing | Same Appeals review and same alternatives — but no legal levy pause, no CSED suspension, and no Tax Court review; Appeals' decision is final |

| After one year | No hearing under Form 12153 | You can still pursue a CAP appeal, a payment plan, an offer, or hardship status through normal collection channels — without the independent-hearing protections |

One warning about what you write: Appeals can disregard a request built on frivolous arguments — "taxes are voluntary," "wages aren't income," and the like — and treat it as if you never filed. State a real dispute or a real alternative, in plain language.

What you can raise at the hearing: your options

A CDP hearing can end with a payment plan, hardship status, penalty relief, or a settlement in place of a levy — Appeals must consider any legitimate alternative you propose. The form has a section for exactly this, and what you write there frames the whole hearing.

| Alternative | Typically fits when | Cost / what it requires |

|---|---|---|

| Installment agreement | You can pay monthly. Balances of $10,000 or less that can be paid within 3 years may qualify for a guaranteed installment agreement; up to $50,000 can qualify for a streamlined plan over up to 72 months | Setup fee varies by type; interest and penalties keep accruing; all returns must be filed |

| Currently Not Collectible (CNC) | Paying anything would leave you unable to cover basic living expenses — common on fixed Social Security income | Financial disclosure (usually Form 433-F); debt remains and interest accrues, but levies stop |

| Offer in Compromise | Your assets and future income genuinely can't cover the debt before the CSED | $205 fee and 20% down on lump-sum offers — both waived with low-income certification (AGI ≤ 250% of poverty); the IRS accepted roughly 1 in 5 offers in FY2024 |

| Penalty abatement | Clean compliance history (first-time abatement, becoming automatic under AEP starting summer 2026) or reasonable cause like serious illness | No fee; removes penalties, not the underlying tax or interest |

| Innocent spouse relief | The debt traces to a spouse's or ex-spouse's income or errors on a joint return | Form 8857 and supporting facts; raised as a defense within the hearing |

| Liability dispute | You never had a prior chance to contest the amount — e.g., a deficiency notice mailed to an old address | Documentation of the correct figures; not available if you already had an appeal opportunity |

A worked example on Social Security income

Say you're retired, you owe $8,900 from a year you cashed out an investment, and your only income is a $1,900 monthly Social Security check. Do nothing after the LT11, and the Federal Payment Levy Program can take 15% of every check — $285 a month, involuntarily, until the balance plus growing penalties and interest is gone.

File Form 12153 on time instead, and the math changes. Because the tax is under $10,000, you may qualify for a guaranteed installment agreement if all your returns are filed and you can pay it off within three years: $8,900 ÷ 36 months ≈ $247 a month, on a date you choose, with no levy touching your benefit. Interest and a small monthly penalty keep accruing, so the true total will run somewhat higher — but you control the payment instead of losing it.

And if $247 a month is genuinely impossible — if rent, medications, and utilities already consume the full $1,900 — the better request at the hearing is Currently Not Collectible status, which pauses collection entirely while your situation stands. Appeals weighs your actual budget against IRS living-expense standards, which is why the financial form matters so much (more on that below).

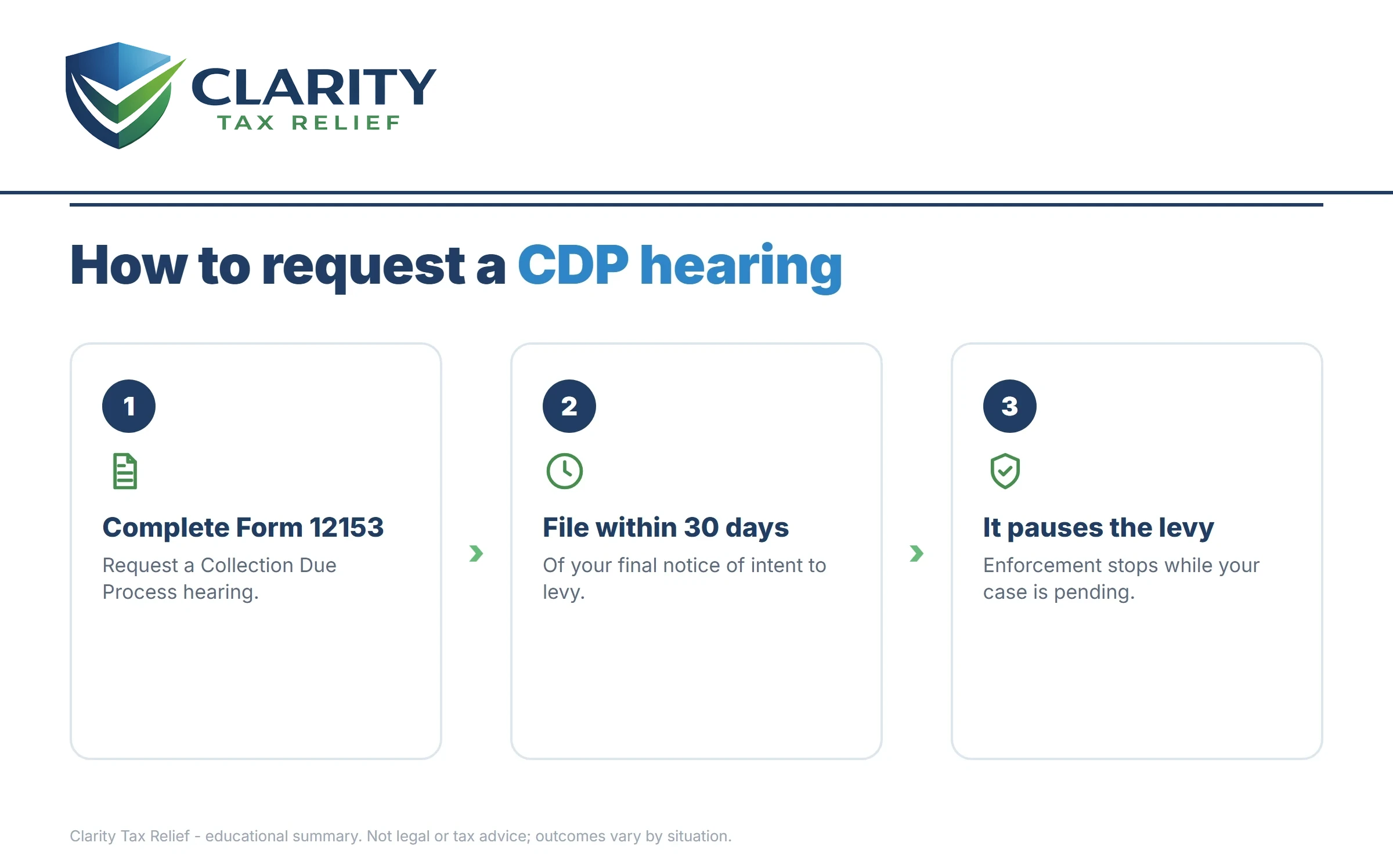

How to file Form 12153, step by step

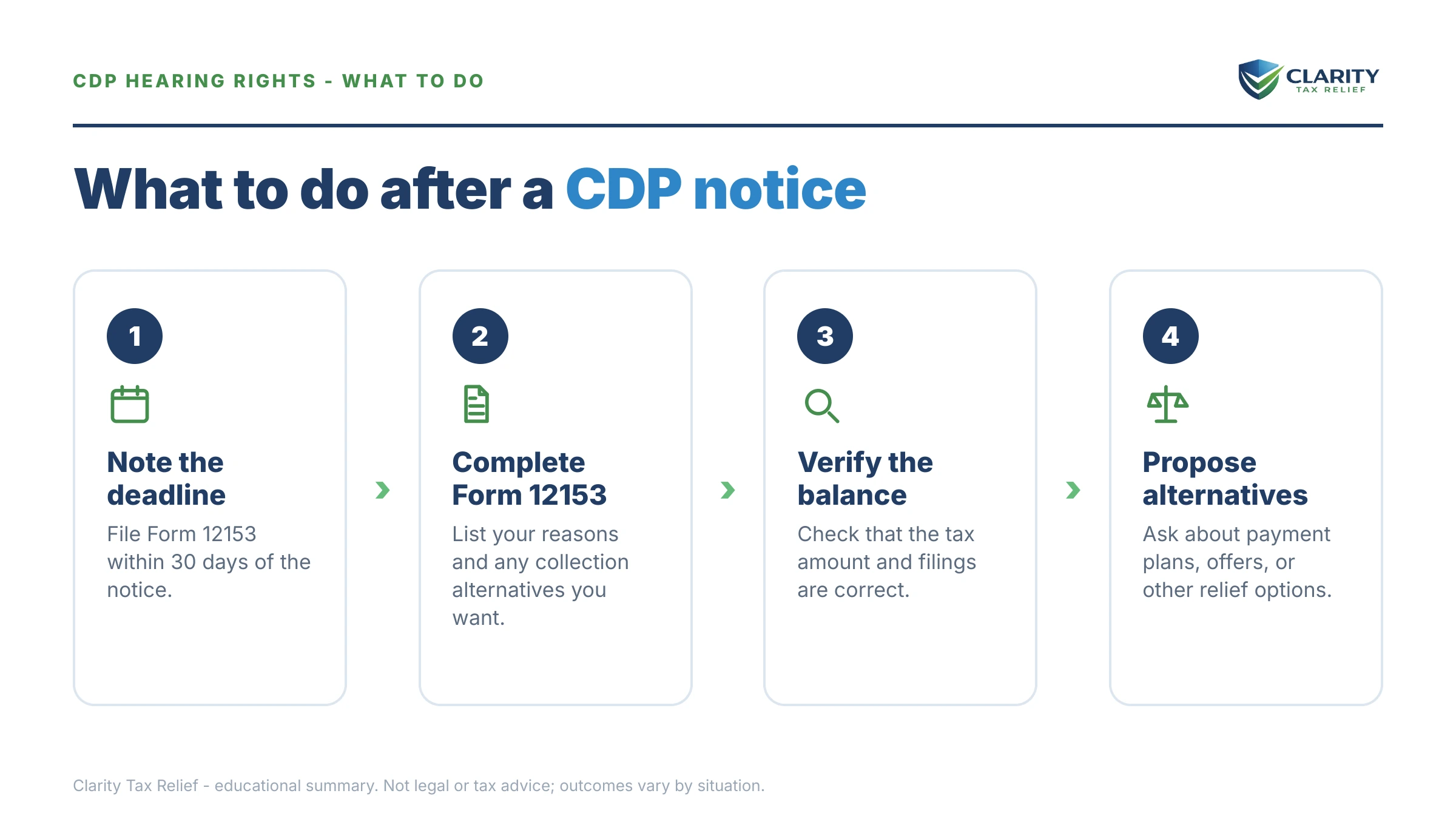

- Confirm the notice and count your 30 days — find the date printed on your LT11, Letter 1058, CP90, or Letter 3172 and count 30 calendar days forward; that is your filing deadline, regardless of when you opened the envelope.

- Complete Form 12153 carefully — check the correct box (levy, lien, or both), list every tax period shown on your notice, and state the collection alternative you want: a payment plan, hardship status, an offer, or penalty relief. If you want help wording the request, see our CDP hearing request letter guide.

- Send it to the address or fax number on your notice — file with the office that sent the letter, not a generic IRS address, by certified mail with return receipt so the postmark proves you filed within the window.

- Prepare your financials and file missing returns — complete Form 433-F (or Form 433-A if a revenue officer is assigned), gather proof of income and expenses, and file any unfiled returns; Appeals cannot approve most alternatives while returns are missing.

- Attend the Appeals conference and present your alternative — most CDP hearings are a phone call with a settlement officer; walk through your numbers, propose your alternative, and send requested documents promptly.

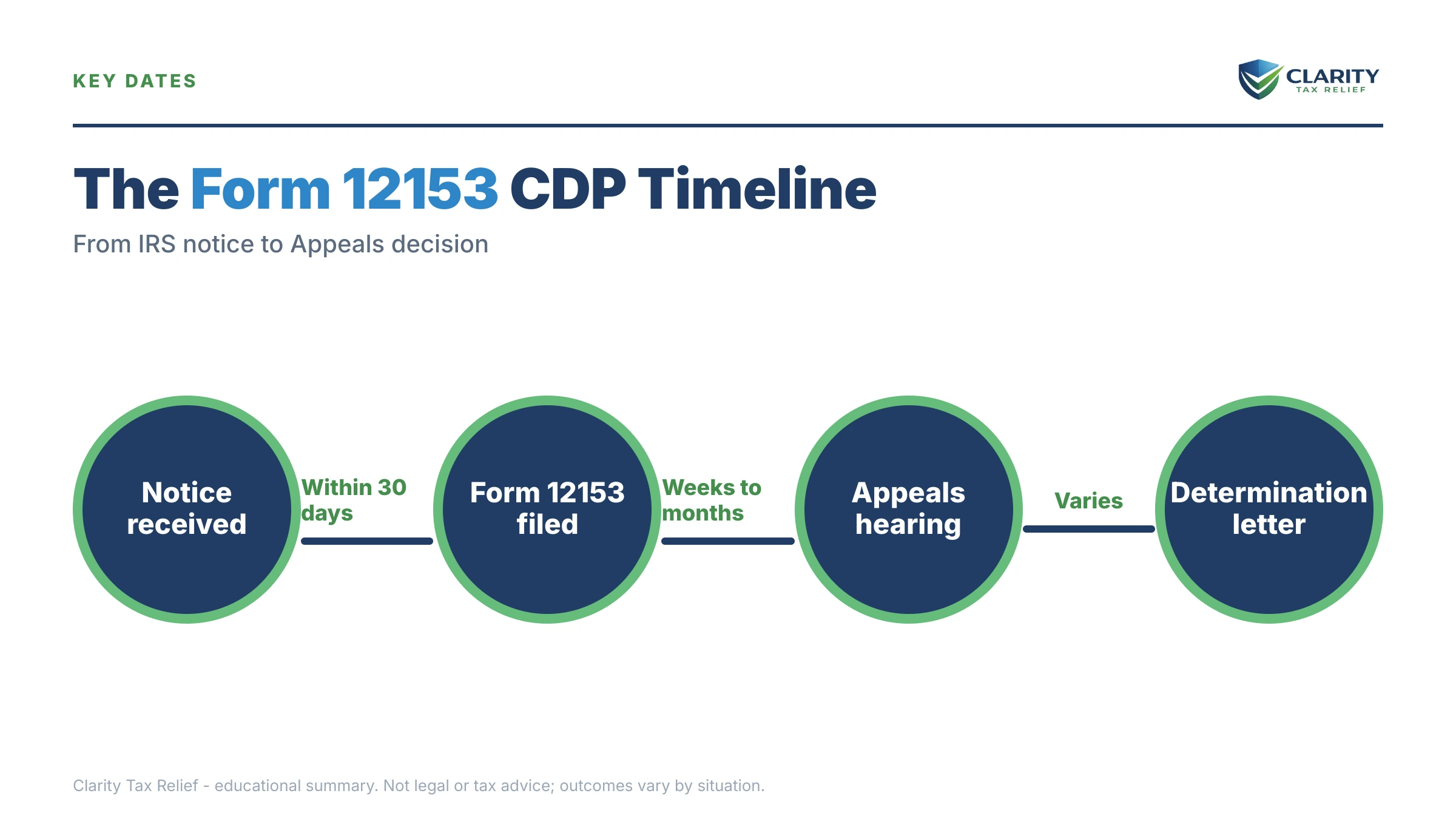

- Read the Notice of Determination and watch the 30-day court window — Appeals closes the case in writing, and if you disagree, you have 30 days from that letter to petition the U.S. Tax Court.

What happens after you file: tracking the hearing on your transcript

Every CDP case ends with a written Notice of Determination — and you have 30 days from that letter to go to Tax Court. Between filing and determination, expect a wait of several months for a settlement-officer assignment, then a scheduled phone conference. While you wait, your IRS account transcript tells you whether the request actually registered:

| Code | What it means during a CDP case | What to do |

|---|---|---|

| 971 | A notice or action posted — including issuance of your final notice and receipt of your CDP request | Match the 971 dates against your notice date and your certified-mail receipt |

| 520 | Collection freeze posted — the account is held while the hearing (or other litigation) is pending | Verify a 520 posted for every tax year you listed on Form 12153; call about any missing year |

| 521 | The freeze was released — the hearing closed and normal collection can resume | Locate your Notice of Determination and calendar the 30-day Tax Court deadline immediately |

If a year you listed never shows the freeze, don't assume it's protected — that's exactly the gap where an automated levy slips through while everyone thinks the case is on hold.

When you can handle Form 12153 yourself — and when help changes the outcome

You can reasonably file Form 12153 on your own when the facts are simple: one tax year, a balance you agree with, returns all filed, and a straightforward ask like a monthly payment plan you can clearly afford. The form is short, the deadline is the only trap, and Appeals officers work with self-represented taxpayers every day.

Experienced help tends to change outcomes in four situations. First, when a levy is already in motion — an FPLP offset on Social Security or a bank freeze — because release requests and hearing rights run on parallel tracks that are easy to mishandle. Second, when multiple years are involved, especially with unfiled returns, since Appeals won't approve alternatives until compliance is fixed and the order you fix things changes the total. Third, when you'll propose an Offer in Compromise or CNC, because those live or die on how the financial statement presents your budget against IRS expense standards. Fourth, when the CSED is short — filing a CDP request that tolls a nearly-expired debt can be a genuine mistake, and that judgment call is worth a professional look. A representative files Form 2848 and can attend the hearing so you never have to.

Terms on your notice and Form 12153, decoded

- Collection Due Process (CDP): your legal right to one independent Appeals review before the IRS levies (and after it files a lien), created by IRC §§6320 and 6330.

- Equivalent hearing: the late-filed version of a CDP hearing — same Appeals review, but no levy pause, no CSED suspension, and no court review.

- Notice of Determination: the written decision that closes a CDP hearing and starts your 30-day window to petition the U.S. Tax Court.

- CSED: the Collection Statute Expiration Date — the end of the IRS's 10-year window to collect, which a timely CDP request pauses.

- Levy vs. lien: a levy takes property (wages, bank funds, benefits); a lien is a recorded legal claim against property you keep. Form 12153 covers both, with separate checkboxes.

- Collection alternative: anything you propose instead of the levy — an installment agreement, CNC status, an offer, or penalty relief. (Disputes over an audit's tax amount use a different route — see Form 12203.)

Form 12153 and CDP hearing questions, answered

What is the deadline to file Form 12153?

You have 30 days from the date printed on your final notice — LT11, Letter 1058, CP90, or Letter 3172 — to file Form 12153 and keep full CDP rights, including Tax Court review. Miss it and you can still request an equivalent hearing for up to one year, but you lose the Tax Court backstop and the automatic levy pause. The clock runs from the notice date, not the day you opened the envelope.

Does filing Form 12153 stop an IRS levy?

A timely CDP request generally requires the IRS to hold levy action on the tax periods in the hearing while Appeals reviews your case. That protection lasts through the hearing and, if you petition, through Tax Court review. It does not undo a levy that already took your money, and it does not protect tax periods you left off the form — list every year shown on the notice.

What is the difference between a CDP hearing and an equivalent hearing?

Both are reviews by the IRS Independent Office of Appeals, and you can propose the same collection alternatives at either. The difference is what you keep: a timely CDP hearing legally pauses levy action, suspends the 10-year collection statute, and ends with a Notice of Determination you can take to Tax Court. An equivalent hearing carries none of those three protections — Appeals' decision is final.

Can I dispute the amount I owe at a CDP hearing?

Only if you never had a prior opportunity to dispute it — for example, a Notice of Deficiency that went to an old address you never received. If you already had that chance, the hearing is limited to how the debt is collected, not whether it exists. Audit reconsideration or a doubt-as-to-liability offer may still be available through separate channels.

Where do I send Form 12153?

Mail or fax it to the address or fax number printed on the notice that gave you hearing rights — not to a generic IRS address. Send it certified mail with return receipt so you can prove it was postmarked within the 30-day window. Keep a copy of the completed form and the notice together; the postmark date is what preserves your rights.

Does a CDP hearing pause the 10-year collection statute?

Yes. A timely CDP request suspends the CSED — the 10-year collection deadline — while the hearing and any court review are pending. That is the real trade-off of filing: you gain a levy pause and appeal rights, but you give the IRS more total time to collect. If your debt is close to expiring, run the math before you file; an equivalent hearing does not suspend the CSED.

What happens after the CDP hearing?

Appeals issues a Notice of Determination stating whether it sustains the levy or lien and whether it accepts your proposed alternative. If you disagree, you have 30 days from that determination to petition the U.S. Tax Court. If you agree — say Appeals approved your installment agreement — the case closes and collection follows the agreed terms instead of a levy.

Can the IRS levy my Social Security while my CDP request is pending?

Generally no — a timely CDP request suspends levy action, including the 15% Federal Payment Levy Program offset against Social Security, for the periods in your hearing. If an FPLP levy is already taking 15% of your benefit when you file, Appeals can release it, especially where it creates economic hardship. An equivalent hearing does not carry the same legal bar, though the IRS often holds voluntarily.

Your next 24 hours

- Find the date on your final notice — the notice date in the upper corner of your LT11, Letter 1058, CP90, or Letter 3172 — and count 30 days forward. Write that deadline where you'll see it.

- Gather three things: the notice itself, your most recent tax return, and a simple list of monthly income and expenses (your Social Security award letter or bank statement works for income).

- Get a free case review before the window closes — call (888) 825-7779 or use the 2-minute form. An experienced tax professional will confirm your exact deadline, check your CSED, and help you decide what to ask Appeals for.

The IRS's own resources are worth bookmarking: the official About Form 12153 page has the current form and instructions, the IRS Independent Office of Appeals page explains the hearing process, and the Taxpayer Advocate Service can step in if a levy is causing hardship while your case sits in a queue.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.