IRS Levies

IRS Taking 15 Percent of Social Security? How to Stop the FPLP Levy (2026)

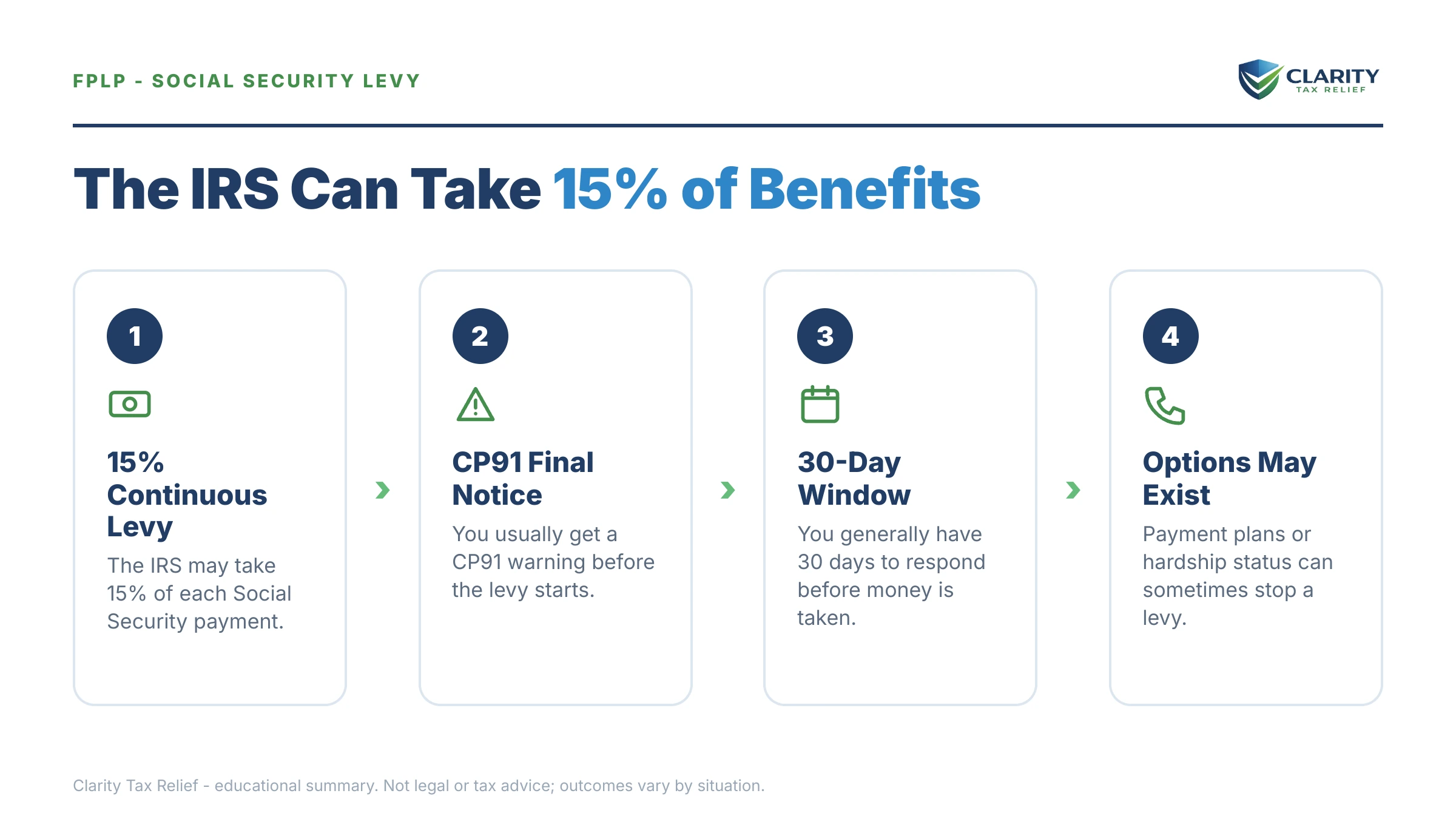

The short answer: if the IRS is taking 15 percent of your Social Security, that's the Federal Payment Levy Program (FPLP) — an automated, continuous levy that deducts 15% of every monthly benefit until the debt is paid, released, or expires. A payment plan, hardship release, or accepted settlement can turn it off, usually within a payment cycle or two.

Your benefit deposit posted short this month, and the letter from Social Security says the Treasury withheld part of it for a federal tax debt. Maybe you ran a business for decades and the tax years from winding it down finally caught up with the retirement check you were counting on. The deduction will repeat every single month until you act — but every path to turning it off is on this page.

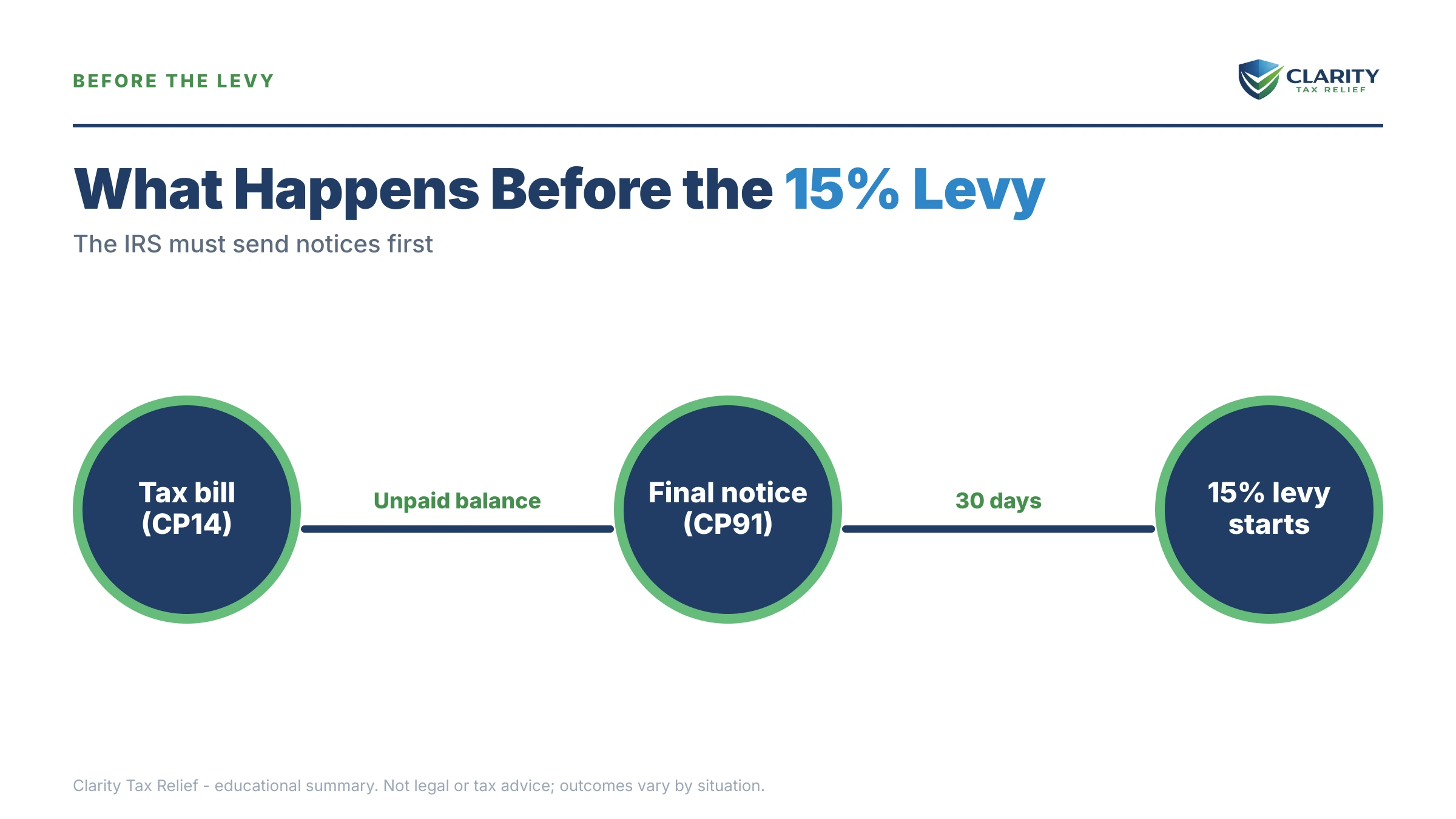

Before the withholding ever started, the IRS mailed a specific final warning — usually a CP91. The image below shows exactly what that warning looks like and where to find the date and balance that control your case.

⏱ Your clock: a CP91 gives you 30 days from the notice date before the 15% deduction begins. If the levy has already started, there is no new deadline to wait for — the clock is the levy itself: another 15% of your benefit leaves every month, while interest and penalties keep the balance growing behind it.

Why the IRS is taking 15 percent of your Social Security

The 15% deduction from your Social Security check comes from the Federal Payment Levy Program, a computer match between the IRS and the Treasury's payment system authorized by IRC §6331(h). No revenue officer chose you. The system matched your unpaid balance against the federal payments going out in your name, and Social Security is a federal payment.

What makes this levy different from a bank levy is that it's continuous — one levy attaches to every future benefit payment automatically. A bank levy grabs what's in the account on one day; the FPLP renews itself every month with no new paperwork and no new notice.

You didn't get here without warning, even if the warnings went to an old address. The FPLP only fires after a full notice sequence, ending with a CP91 Social Security levy notice — "Final Notice Before Levy on Social Security Benefits." Here is the trail that led to your shrunken deposit:

| Notice | What it means | Your window |

|---|---|---|

| CP14 | First bill for the balance due | Typically 21 days before escalation |

| CP501 / CP503 | Automated reminders; balance growing monthly | Weeks apart, no enforcement yet |

| CP504 | Intent to levy — your state refund is now reachable | Act before the final notice issues |

| CP90 / LT11 | Final notice of intent to levy, with appeal rights | 30 days to file Form 12153 |

| CP91 / CP298 | Final notice before levy on Social Security benefits | 30 days before the FPLP starts |

| FPLP levy active | 15% of each monthly benefit withheld | Continuous until released, paid, or expired |

What the 15% levy can and can't touch

The FPLP reaches Social Security retirement, survivor, and disability (SSDI) benefits — but it cannot touch SSI. Benefits paid under Title II of the Social Security Act are all fair game for the 15% deduction, which is why the IRS can garnish SSDI the same way it garnishes a retirement benefit. Supplemental Security Income, lump-sum death benefits, and benefits paid to children are excluded.

Two limits on the 15% figure matter more than most articles admit. First, there is no protected floor under the FPLP — unlike a wage levy, no exempt amount is carved out before the 15% is computed, even if the benefit is your only income. The safety valve is a hardship release you must request (more below), not an automatic exemption.

Second, 15% is the ceiling only for the automated program. A revenue officer working your case personally can issue a manual levy on Social Security that is not capped at 15% — it only has to leave you a modest exempt amount. If your case involves a revenue officer, treat the 15% as the mild version of what's possible. For the full map of what the IRS can reach in retirement income, see whether the IRS can garnish Social Security in your specific situation.

What happens if you do nothing

An active FPLP levy never pauses on its own — it renews every month until the account is resolved or the collection statute runs out. Here is the sequence you're living through if you wait:

- The deduction repeats. 15% of every benefit payment, automatically, with no new notice and no human review.

- The balance still grows behind it. Interest compounds and the 0.5% monthly failure-to-pay penalty keeps posting, so a large share of each deduction covers new charges, not old tax. (Interest is rarely removable, but penalties often are — see can IRS interest be waived.)

- Other enforcement stacks on top. The Social Security levy doesn't replace anything. The IRS can still levy your bank account (with a 21-day hold before the money leaves), file a federal tax lien, and take every tax refund until the debt is gone.

- Bigger balances trigger bigger consequences. If your total certified debt crosses $66,000 (the 2026 threshold), the IRS can certify you to the State Department and block passport renewal.

- It runs to the statute's end. The IRS generally has 10 years from assessment to collect, and the FPLP will run right up to that date — with the clock pausing during bankruptcy, a pending offer, or certain appeals.

One 2026 reality check: the IRS workforce shrank roughly 27% in 2025, so reaching a human is harder than ever — but the FPLP is exactly the kind of enforcement that never needed a human. The computer that started this levy will keep it running indefinitely unless someone affirmatively turns it off.

Losing 15% of your check every month?

There's no future deadline to wait for — each month the FPLP runs costs you another 15% of your benefit. An experienced tax professional will review your levy free, tell you which release path fits your income, and map the fastest way to a full deposit again.

Your options to stop the IRS taking 15% of Social Security

The FPLP levy is typically released once your account enters a resolution the IRS accepts — and there are more of those than the notice tells you. The general playbook for resolving a balance lives in our guide to how to settle tax debt yourself; what follows is how each option interacts with this specific levy.

| Option | Typical eligibility | Effect on the 15% levy |

|---|---|---|

| Pay in full | Anyone with the funds | Levy released; may take a payment cycle to reach SSA |

| Short-term payment plan | Balance payable within 180 days; $0 setup fee | Generally released once the plan is approved |

| Installment agreement | Up to $50,000 → up to 72 months, set up online | Generally released once the agreement is in place |

| Currently Not Collectible | Income doesn't cover allowable living expenses (Form 433-F) | Released on hardship grounds; debt remains |

| Offer in Compromise | Assets plus future income genuinely below the balance; ~1 in 5 accepted in FY2024 | Levy action generally pauses while a valid offer is pending |

| CDP hearing (Form 12153) | Within 30 days of a CP90 or LT11 | Holds new levy action while the hearing is pending |

| Penalty abatement | Clean 3-year history or reasonable cause | Shrinks the balance; doesn't release the levy by itself |

Payment plans are the workhorse. A balance under $50,000 qualifies for a streamlined agreement online — up to 72 months, no detailed financial disclosure — and approval is normally what triggers the levy release. Which payment method fits your cash flow (direct debit, payroll deduction, online) is compared in our guide to the best way to pay the IRS.

Hardship status matters most for readers of this page. If your benefit is your primary income and the 15% deduction leaves you short on rent, food, medicine, or utilities, the law — IRC §6343 — requires the IRS to release a levy that creates economic hardship. That's the levy causing hardship release, and it usually pairs with placing the whole account in Currently Not Collectible status. For fixed-income taxpayers specifically, the numbers and documentation are covered in IRS hardship while on Social Security.

An Offer in Compromise is real but math-driven: the IRS accepted roughly 1 in 5 offers in FY2024, and acceptance turns on whether your assets and future income truly can't cover the debt — a test many benefit-only households actually pass. The $205 application fee and 20% down payment are waived entirely if your AGI is at or below 250% of the federal poverty level.

Appeal rights may still be alive. If a CP90 or LT11 reached you within the last 30 days, filing a Form 12153 CDP hearing request preserves your right to propose alternatives before an appeals officer — and generally holds new levy action while it's pending.

One persona-specific note: if your balance traces back to a business — say the Trust Fund Recovery Penalty from unpaid payroll taxes assessed against you personally — the FPLP treats it exactly like any 1040 debt. Closing the company did not shield your benefit check.

What the math looks like: say you owe $23,800

Say you owe $23,800 — you closed your small business two years ago, the final payroll and income-tax years landed on you personally, and you now draw a $2,200 monthly Social Security benefit. The FPLP takes 15% of $2,200 = $330 a month, or $3,960 a year.

Here's the trap: the levy doesn't stop the meter. The failure-to-pay penalty alone is 0.5% per month — about $119 a month on a $23,800 balance at the start — and interest compounds on top of that. A large slice of each $330 the Treasury takes is covering new charges, so the real paydown crawls.

Now compare a streamlined installment agreement: $23,800 over the maximum 72 months is about $331 a month — essentially the same cash out of pocket as the levy. But the agreement releases the FPLP levy, restores your full benefit deposit, typically cuts the failure-to-pay rate roughly in half while it's in effect, and lets you pay more in good months to kill the interest sooner. Same dollars, dramatically better position.

And if $2,200 a month doesn't cover your actual living expenses in the first place, the right answer may be neither — a documented hardship release plus CNC status can reduce your required payment to zero while the debt sits (and the 10-year clock keeps running). You can estimate what a levy takes from your income with our IRS Wage Garnishment Calculator before you decide which path fits.

How to stop the 15% Social Security levy, step by step

- Confirm the levy source — check the letter Social Security sent about the withholding and log into your IRS online account to verify it is the FPLP, and note the exact balance and tax years involved.

- Gather your financials — pull your last filed return, your monthly benefit statement, and a list of basic monthly living expenses; every resolution path starts with these numbers.

- Pick your resolution — choose an installment agreement, Currently Not Collectible status, or an Offer in Compromise based on what your income can actually support, not on which one sounds best.

- Request the levy release — once the agreement is approved or the hardship is documented, ask the IRS to release the FPLP levy and confirm when Social Security will restore your full benefit.

- Appeal if you are still inside the window — if a CP90 or LT11 final notice arrived within the last 30 days, file Form 12153 to preserve your Collection Due Process rights before choosing anything else.

When you can handle this yourself

If your balance is under $50,000, your returns are all filed, and the benefit isn't your only income, you can likely fix this without paying anyone. Set up a payment plan on IRS.gov, then confirm the levy release — that's a same-week project for many people, and the honest truth is you don't need a firm for it.

Experienced help changes outcomes in a few specific situations: the benefit is your only income and you need a hardship case built and documented correctly the first time; the debt comes from business or payroll years (the Trust Fund Recovery Penalty adds traps a DIY plan can trip); multiple years are unfiled, which blocks every resolution until they're in; or the Offer in Compromise math is close and the presentation decides it. If the levy is causing immediate hardship and you can't get traction with the IRS, the Taxpayer Advocate Service is a free, independent channel that can also intervene.

Terms on your notice, decoded

- FPLP (Federal Payment Levy Program): the automated Treasury–IRS match that withholds up to 15% of federal payments, including Social Security — the IRS explains it on its Federal Payment Levy Program page.

- Continuous levy: a levy that attaches to future payments automatically, month after month, until it's released — unlike a one-time bank levy.

- CP91 / CP298: the "Final Notice Before Levy on Social Security Benefits" — CP91 for individuals, CP298 for businesses — mailed 30 days before the deduction starts.

- Economic hardship (IRC §6343): the law requiring the IRS to release a levy that prevents you from paying reasonable basic living expenses.

- Currently Not Collectible (CNC): a status where the IRS shelves active collection because your income doesn't cover allowable expenses; the debt remains, but levies stop.

- CSED: the Collection Statute Expiration Date — generally 10 years from assessment, after which the IRS can no longer collect; the full rules are in our guide to how long the IRS can collect back taxes.

15% Social Security levy questions, answered

Can the IRS take more than 15 percent of my Social Security?

Yes, but not through the automated program. The FPLP is capped at 15% of each monthly benefit, but a revenue officer can issue a manual levy on Social Security that is not limited to 15% — it only has to leave you an exempt amount based on your filing status and dependents. Manual levies are far less common and usually show up in larger or long-ignored cases.

Does the 15% levy apply to SSDI and SSI?

SSDI yes, SSI no. Disability insurance benefits (SSDI) are paid under Title II of the Social Security Act and are subject to the FPLP the same way retirement and survivor benefits are. Supplemental Security Income (SSI) is a needs-based program and is excluded from the levy entirely, as are lump-sum death benefits and benefits paid to children.

How do I stop the IRS from taking 15 percent of my Social Security check?

Get the account into a resolution the IRS accepts — the levy is typically released once an installment agreement is approved, the account is placed in Currently Not Collectible status, or a valid Offer in Compromise is pending. If the deduction leaves you unable to pay basic living expenses, you can request an economic hardship release under IRC §6343 without waiting for a full agreement. Releases are not instant; it can take a payment cycle or two for the change to reach Social Security.

How long will the IRS take 15 percent of my Social Security?

Until the debt is paid, a resolution releases the levy, or the 10-year collection statute (CSED) expires — whichever comes first. The FPLP levy is continuous, meaning it renews automatically every month with no new notice. The 10-year clock also pauses during bankruptcy, a pending Offer in Compromise, and certain appeals, so the expiration date may be later than you expect.

Did the IRS have to warn me before levying my Social Security?

Yes. Before the deduction starts, the IRS must send a final notice of intent to levy with appeal rights, and for Social Security it typically also mails a CP91, Final Notice Before Levy on Social Security Benefits, giving you 30 days to respond. If you moved and never saw the notices, the levy is still valid as long as they went to your last known address — but you may still be able to raise your case through an equivalent hearing or a collection appeal.

Is any part of my Social Security automatically protected from the FPLP?

No — unlike a wage levy, the FPLP has no built-in exempt floor, so the 15% comes out even if the benefit is your only income. The protection is a hardship release you have to ask for: if the levy prevents you from paying reasonable basic living expenses, the IRS can release it under IRC §6343. That requires documenting your income and expenses, usually on Form 433-F.

Will the 15 percent levy eventually pay off my tax debt?

Slowly, and on larger balances sometimes barely at all. Interest and the 0.5% monthly failure-to-pay penalty keep accruing while the levy runs, so much of each 15% deduction goes to new charges rather than the original tax. On a $23,800 balance with a $2,200 monthly benefit, the $330 levy is roughly what a 72-month payment plan would cost — but the plan releases the levy and puts you back in control of the account.

Your next 24 hours

- Find the notice. Locate your CP91 — or the letter from Social Security showing the withholding — and note the date, the balance, and the tax years listed.

- Gather three things. Your last filed tax return, your monthly benefit statement, and a rough list of your basic monthly expenses. Every release path starts with those numbers.

- Get the levy reviewed free. Send it through the 2-minute form at claritytaxrelief.com/#consult or call (888) 825-7779. There's no future deadline coming to save you here — the only clock is the 15% that leaves your check again next month.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.