Paying the IRS

The Best Way to Pay the IRS in 2026 (Every Option Compared)

The short answer: the best way to pay the IRS is IRS Direct Pay — a free bank transfer at IRS.gov with no processing fee and no registration. If you can't pay in full, a short-term plan (up to 180 days, $0 setup) or an installment agreement almost always beats a credit card or a retirement withdrawal.

You know the number you owe. What you haven't settled is the mechanics: which button to click, whether the card fee is worth it, whether a payment plan quietly costs more than borrowing. That choice is worth ten minutes of thought — because the best way to pay the IRS can differ from the worst by hundreds or even thousands of dollars on the exact same balance.

⏱ The running clock: there's no letter-driven deadline on how you pay — but there is a meter. The failure-to-pay penalty adds 0.5% of the unpaid balance every month, and interest compounds daily on top, until the day your payment actually posts.

Why how you pay the IRS matters as much as when

Every IRS payment channel posts at a different speed and costs a different amount — and the wrong channel can add real money to the same debt. A credit card adds a processor fee of roughly 2% before your card's APR even starts. A mailed check can float for days while another cycle of penalty accrues. A free bank transfer posts in days and costs nothing.

The structure matters even more than the channel. Paying in full stops all accrual immediately. A formal payment plan cuts the failure-to-pay penalty rate in half and switches off enforcement. Paying "when you can," with no agreement in place, does neither — the automated notice machine treats you exactly like someone who never paid at all.

One 2026 wrinkle worth knowing: the IRS workforce shrank by roughly 27% in 2025, so reaching a human by phone is harder than ever. The payment systems, though, are fully automated and work fine. Everything in this guide can be done online, without waiting on hold.

Best way to pay the IRS in full: six methods compared

IRS Direct Pay is free, requires no account, and pulls straight from checking or savings — for most people paying in full, it wins outright. Here's how every method stacks up on cost and speed:

| Payment method | Fee | Speed & best use |

|---|---|---|

| IRS Direct Pay (bank transfer) | $0 | Posts within days; instant confirmation number. Best for most one-time payments. |

| IRS online account payment | $0 | Same free bank pull, plus you see your live balance and payment history first. |

| EFTPS | $0 | Requires advance enrollment (a PIN arrives by mail). Best for scheduling recurring or quarterly payments. |

| Debit card | Small flat processor fee | Fast. Fine for small balances if you don't want to share bank details. |

| Credit card | Processor fee of roughly 2% | Fast but costly. Only sensible with a 0% promotional APR you're certain you'll pay off in time. |

| Check by mail / cash at retail partner | $0 (check) / small fee (cash) | Slowest — accrual continues until the payment posts. Check goes to "United States Treasury" with your SSN, tax year, and form written on it; cash has per-payment limits. |

Two details trip people up regardless of method. First, designate every payment — tell the IRS which tax year and which form it applies to, or the IRS will apply it in the government's best interest, which may not be yours. Second, keep every confirmation number. If a payment is ever misapplied, that number is your proof.

If you're deciding whether to send money now or wait until filing season, timing has its own math — see whether it makes sense to pay the IRS before the end of the year.

What happens if you don't pay at all

An unpaid IRS balance moves through a fixed, automated notice sequence that ends in levy power — no human has to decide to escalate it. Here is the order it runs in:

- CP14 — the first bill, with roughly 21 days to pay before the sequence advances (only 10 business days when the balance is $100,000 or more).

- CP501 / CP503 — reminder notices. Still just bills, but the balance grows every month they sit.

- CP504 — Notice of Intent to Levy under IRC §6331(d). The IRS can now take your state tax refund, and a federal tax lien becomes a live possibility.

- LT11 / Letter 1058 — the final notice. It starts a 30-day clock and your Collection Due Process rights (requested on Form 12153). After that window, the IRS can levy bank accounts (a 21-day hold before funds leave) and garnish wages continuously until released.

For self-employed and gig income there's no employer paycheck to garnish, but the IRS can levy bank accounts and send one-time levies to the companies that pay you. And for balances that climb past $66,000 (the 2026 threshold), the IRS can certify the debt to the State Department, which can deny or revoke your passport. The full endgame is mapped in what happens if you never pay the IRS.

Not sure which payment path is cheapest for your balance?

Tell us what you owe and what you earn. An experienced tax professional will map the lowest-cost way to pay — or the program that fits if full payment isn't realistic — free and confidential. Penalties and interest accrue every month the balance sits.

Can't pay in full? Payment structures ranked by cost

A formal IRS payment plan cuts the failure-to-pay penalty rate in half — from 0.5% to 0.25% per month — while the agreement is in place. That single fact makes an installment agreement cheaper than almost any consumer borrowing, and far cheaper than doing nothing. The realistic structures, cheapest first:

| Option | Who it fits | Cost & catch |

|---|---|---|

| Pay in full now | You have the cash without gutting emergency savings | Cheapest by definition — all penalty and interest accrual stops the day it posts. |

| Short-term plan (up to 180 days) | You can clear the whole balance within six months | $0 setup fee. Interest and the failure-to-pay penalty continue, but enforcement stops. |

| Long-term installment agreement | Combined balance of $50,000 or less can be set up online, up to 72 months | Setup fee applies (lower with direct debit; reduced or waived for low-income taxpayers). Penalty rate drops to 0.25%/month; interest continues. |

| Guaranteed / streamlined agreements | $10,000 or less (guaranteed); $25,000 — or $50,000 with direct debit (streamlined) | No financial disclosure required. Approval of a guaranteed installment agreement is automatic by statute if you meet the conditions. |

| Currently Not Collectible | Any payment would prevent basic living expenses (shown on Form 433-F) | Collection pauses; the debt and interest remain, but the 10-year collection statute keeps running. |

| Offer in Compromise | Your assets and future income genuinely can't cover the debt — the IRS runs the math, not you | $205 fee plus 20% down on lump-sum offers (both waived with low-income certification). The IRS accepted roughly 1 in 5 offers in FY2024. |

CNC and the Offer in Compromise aren't really "ways to pay" — they're what replaces payment when payment genuinely isn't possible. The full decision tree for those programs lives in our guide on how to settle tax debt yourself; if the reason you can't pay is a job loss or a medical crisis, start with lost my job and can't pay the IRS instead, because hardship changes which program fits.

Two ways of "finding the money" deserve a warning. Draining retirement usually backfires — an early 401(k) withdrawal creates a tax bill you can't pay next April on top of the 10% penalty. And putting a five-figure balance on a card at a typical APR costs more per month than the IRS's combined accrual on a plan. You can estimate your own accrual with our IRS penalty and interest calculator; current rates are covered in IRS interest rates for 2026.

Worked example: paying $27,500 as a gig worker with unfiled years

Say you drive and deliver on 1099s, haven't filed for three years, and once the returns are prepared the combined damage — tax, failure-to-file and failure-to-pay penalties, and interest — comes to $27,500. This is hypothetical, but the arithmetic is real:

- Filing comes first, whatever you do. The failure-to-file penalty runs 5% per month (up to 25%) — ten times the 0.5% failure-to-pay rate, though in months where both penalties apply, the failure-to-file portion drops to 4.5% (5% combined) — so unfiled years bleed fastest. The IRS also won't approve any payment plan while required returns are missing. The catch-up sequence is covered in haven't filed in 3 years.

- Pay in full via Direct Pay: $27,500 sent, $0 in fees, all accrual stops. On a credit card, the processor fee alone at roughly 2% is about $550 — before a dollar of card interest.

- 180-day short-term plan: $27,500 ÷ 6 ≈ $4,583/month. $0 setup, and it works for a strong earner who just needs two good quarters.

- 72-month installment agreement: $27,500 is under the $50,000 online ceiling, so the whole thing can be set up in one sitting. The floor payment is about $27,500 ÷ 72 ≈ $382/month — but at the start, the reduced 0.25% penalty alone is about $69/month before interest, so a floor payment makes slow progress. Doubling to roughly $764/month (a 36-month pace) dramatically cuts the total accrual, and there's no prepayment penalty for paying faster.

- Stay current going forward, or the plan dies. A new unpaid balance defaults an existing agreement. For 1099 income that means starting quarterly payments now — here's how quarterly estimated taxes work.

One more lever in this scenario: with three late-filed years, penalty relief can shrink the balance itself before you pay a cent of it. First-time penalty abatement can remove penalties for the earliest year if the prior three were clean — and starting summer 2026, the IRS's new Automatic Exemption from Penalty (AEP) applies some of this relief automatically, with no request needed.

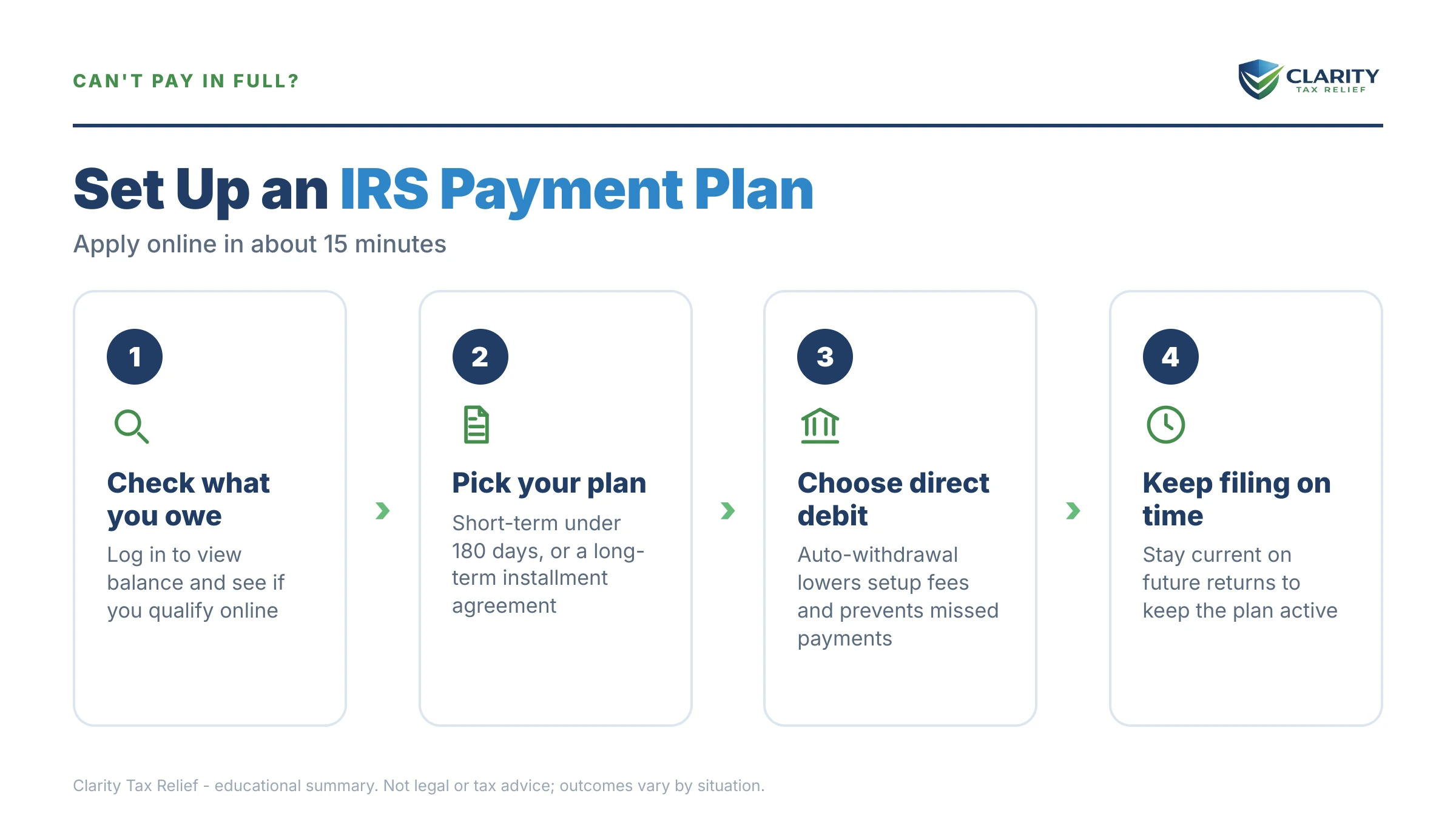

How to pay the IRS, step by step

- Confirm your exact balance. Log into your IRS online account and write down the payoff amount for each year separately. Any notice in your hand is already out of date the day it prints, because interest accrues daily.

- File every missing return. The IRS will not approve a payment plan while required returns are unfiled, and filing stops the 5%-per-month failure-to-file penalty from growing on those years.

- Choose the cheapest method you can sustain. Pay in full through Direct Pay at IRS.gov/payments if you can. If you can't, pick the shortest plan your budget genuinely supports — not the smallest payment the calculator allows.

- Set the plan up before the notices escalate. Combined balances of $50,000 or less can usually be arranged through the IRS Online Payment Agreement tool in one sitting, with no financial disclosure and no phone call.

- Designate and document every payment. Apply each payment to a specific tax year and form, and save every confirmation number. If a payment is ever misapplied, that confirmation is how you fix it.

The click-by-click version of step 4 — screens, direct-debit setup, and fee tiers — is in how to set up an IRS payment plan online. The official starting points are the IRS's own payments page and its payment plans and installment agreements page.

When you can handle this yourself — and when help changes the outcome

Most people searching for the best way to pay the IRS can do this alone. If you're filed and current, the balance is under $50,000, and you agree with the amount, the online tools were built for you: Direct Pay for full payment, the Online Payment Agreement for a plan. There's nothing a firm can add to a streamlined installment agreement or a guaranteed installment agreement that you can't click through yourself in an evening.

Experienced help earns its cost in a narrower set of situations: multiple unfiled years (transcripts have to be pulled and income reconstructed before anyone knows the true balance — and if the IRS filed substitute returns for you, professionally prepared originals often shrink the debt itself), a levy or lien already in motion, business or payroll tax debt, balances over $50,000 that require financial disclosure, or Offer in Compromise math where one wrong number on the forms sinks the application. In those cases the order you fix things — returns, penalties, then the balance — changes what you ultimately pay.

Payment terms, decoded

- Direct Pay — the IRS's free bank-transfer tool for individuals; no registration, instant confirmation number.

- EFTPS — the Electronic Federal Tax Payment System at EFTPS.gov; free, but you enroll in advance and receive a PIN by mail. Built for scheduled and recurring payments.

- Failure-to-pay penalty — 0.5% of the unpaid tax per month (capped at 25% total), cut to 0.25% per month while an approved installment agreement is in place.

- Designated payment — a payment you've instructed the IRS to apply to a specific year and form; undesignated payments are applied in the government's best interest.

- Streamlined installment agreement — a payment plan approved without full financial disclosure when the balance is under the streamlined dollar thresholds.

Best way to pay the IRS: your questions answered

What is the cheapest way to pay the IRS?

IRS Direct Pay is the cheapest way to pay: it pulls directly from your checking or savings account with no fee and no registration. EFTPS is also free but requires enrollment in advance. Every other channel costs something — credit cards add a processing fee of roughly 2%, and mailed checks risk posting delays that let another month of penalty accrue. If you can't pay in full, a $0-setup short-term plan of up to 180 days is the cheapest structure.

Should I pay the IRS with a credit card?

Usually not. The IRS's card processors charge a fee of roughly 2% on top of your balance, and typical card APRs are far higher than the combined interest-plus-penalty cost of an IRS installment agreement. The narrow exception is a 0% introductory-APR card you are certain you can pay off before the promotional window ends — the processing fee then buys you interest-free months. Run the math before you swipe.

Can I pay the IRS in cash?

Yes — the IRS accepts cash through participating retail partners, and some IRS Taxpayer Assistance Centers take cash by appointment. Retail cash payments carry a small fee, have per-payment dollar limits, and can take several days to post to your account. Never use cash against a tight deadline, and never hand cash to anyone who calls claiming to be the IRS — that is always a scam.

Is it better to pay the IRS in full or set up a payment plan?

Paying in full is always cheaper, because interest and the failure-to-pay penalty stop the day the balance hits zero. A payment plan makes sense when paying in full would wipe out your emergency fund or force you onto high-interest debt. On an approved installment agreement the failure-to-pay penalty drops from 0.5% to 0.25% per month, which softens — but does not eliminate — the cost of paying over time.

Does an IRS payment plan stop penalties and interest?

No. Interest keeps compounding daily and the failure-to-pay penalty keeps accruing — at a reduced 0.25% monthly rate — until the balance is paid. What a payment plan stops is enforcement: as long as you stay current, the IRS won't levy your bank account or garnish your wages over that balance. You can also pay more than your required monthly amount at any time, with no prepayment penalty, to cut the total cost.

Should I withdraw from my 401(k) to pay the IRS?

Rarely. An early withdrawal before age 59½ typically triggers a 10% penalty plus ordinary income tax on the amount, which can cost more than years of accruals on an IRS payment plan — and it creates a brand-new tax bill next April. The IRS rarely levies retirement accounts, so voluntarily pulling money out can hand over an asset that was relatively protected. Compare the true cost of both paths before touching retirement funds.

How do I make sure my payment goes to the right tax year?

Designate every payment with the tax year and form it applies to — the online tools ask for this, and a mailed check needs it written on the memo line along with your SSN. If you don't designate a payment, the IRS applies it in the government's best interest, which may not match your plan. Misapplied payments are one of the most common reasons people get a bill for a year they thought was paid.

Can I pay off an IRS payment plan early?

Yes, and you should if you can — there is no prepayment penalty, and every extra dollar stops future interest and failure-to-pay penalty on the amount paid. You can make extra payments through IRS Direct Pay or your online account at any time without changing your agreement's terms. A windfall — a refund, a bonus, one strong 1099 quarter — is often best aimed straight at the balance.

Your next 24 hours

- Pull your real number. Log into (or create) your IRS online account and write down the exact payoff balance for each tax year — that figure, not the one on any letter, is what every option above is priced against.

- Gather the paperwork. Your last filed return, any IRS notices, 1099s or income records for unfiled years, and your bank routing details so a plan or payment can be set up on the spot.

- Get the plan priced before you commit. If anything here is murky — unfiled years, a balance over $50,000, or a payment you're not sure you can sustain — get a free case review at the form or (888) 825-7779. Every month without a payment or a plan in place, penalty and interest accrue on the full balance.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.