Can't Pay the IRS

401k Withdrawal Tax Bill You Can't Pay: What to Do in 2026

The short answer: you can't abate the 10% early-withdrawal tax — but you can stop everything else from growing. File any unfiled returns, then use an IRS short-term plan (180 days, $0 setup) or a monthly installment agreement (balances up to $50,000, up to 72 months online) while checking Form 5329 exceptions that may shrink the bill.

If you're staring at a 401k withdrawal tax bill you can't pay, you already know the cruel part: the money that created the bill is gone. You cashed out to survive a slow stretch — rent, the car, a gap between gigs — and now the return shows you owe thousands the withdrawal was supposed to solve.

This is fixable, in a specific order: shrink the bill where the law allows, get compliant, then pick the payment path that fits your numbers. Your Form 1099-R is where the whole bill was born — the image below shows exactly what that form looks like and which boxes explain why you owe more than you expected.

⏱ The real clock: there's no notice deadline yet, but the meter is running. The failure-to-pay penalty adds 0.5% of the unpaid balance every month, plus daily-compounding interest — and if the return itself is unfiled, the failure-to-file penalty runs 5% per month instead, ten times faster.

Why your 401k withdrawal tax bill is so much bigger than you expected

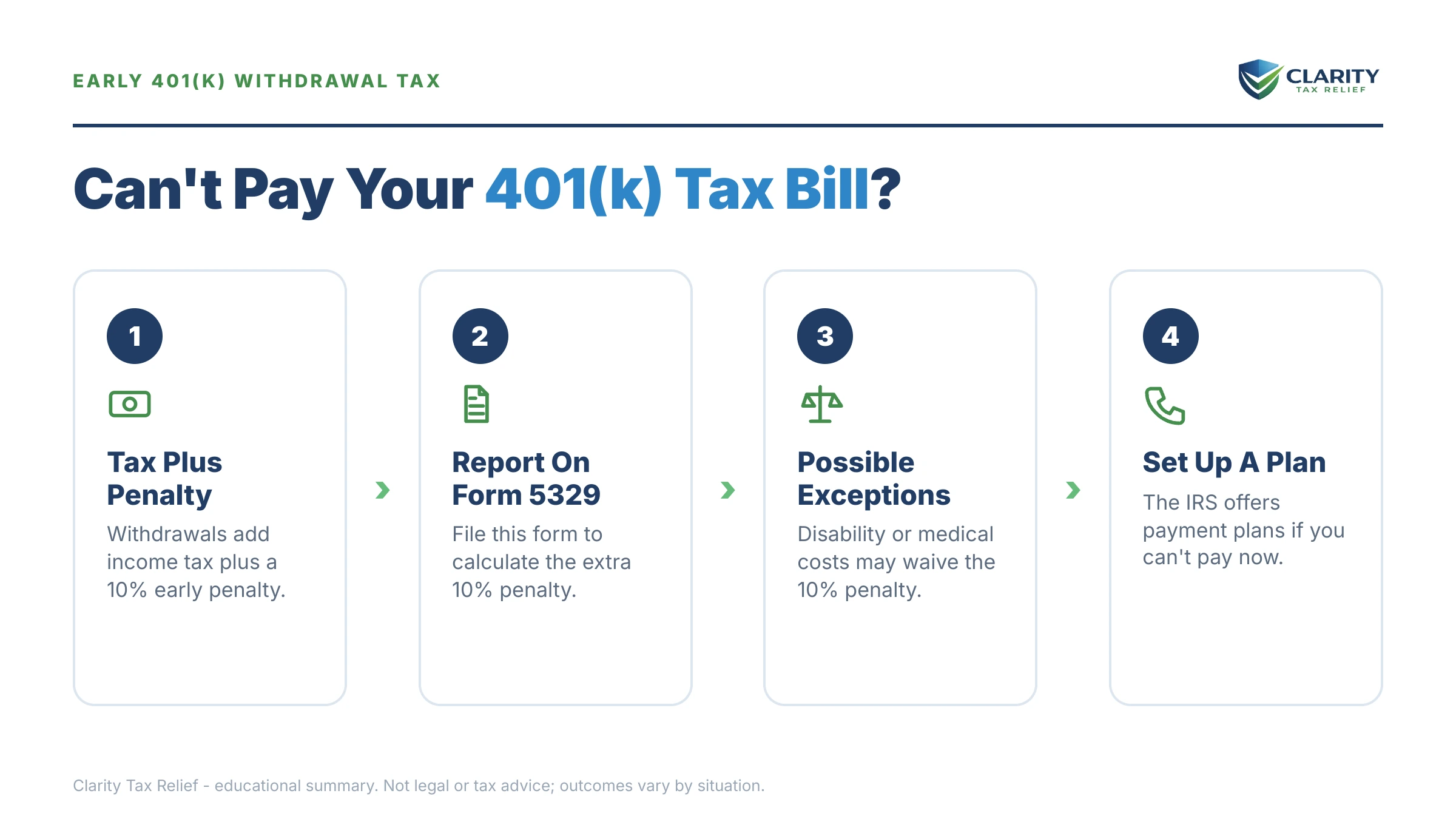

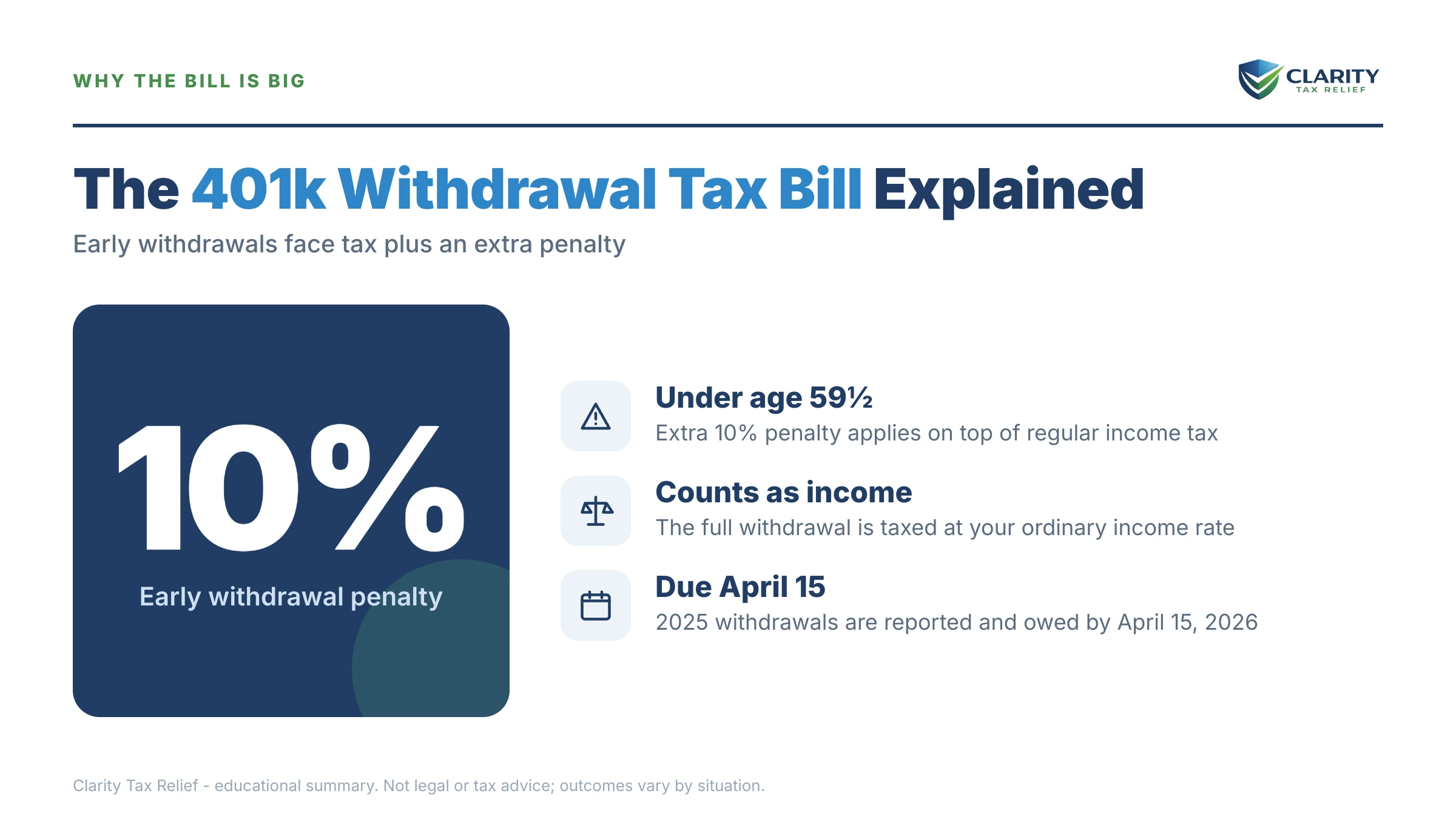

An early 401(k) withdrawal is taxed twice over: as ordinary income at your marginal rate, plus a 10% additional tax if you were under 59½ when you took it. The 20% your plan withheld — if it withheld anything — was a deposit toward your tax, not the tax itself.

Here's the stacking problem. The distribution lands on top of everything else you earned that year, so it gets taxed at your highest bracket, not your average rate. A gig worker in the 22% bracket pays 22% income tax plus the 10% additional tax — 32 cents per dollar withdrawn — before any state tax.

Two situations make the gap even worse. Hardship withdrawals aren't eligible rollover distributions, so the mandatory 20% withholding doesn't apply — many people waive withholding entirely and owe tax on every dollar. And if you're self-employed, the withdrawal stacks on gig income that already had zero withholding, so the shortfall compounds.

Check your 1099-R against this: Box 1 is the gross distribution the IRS taxes, Box 4 is what was actually withheld, and Box 7 carries the distribution code. Code 1 in Box 7 means "early distribution, no known exception" — which is exactly why the next section matters.

Check the 10% exception list before you accept the full bill

The 10% additional tax disappears entirely if one of the statutory exceptions fits — and you claim it on Form 5329, not by asking the IRS for abatement. Plans often issue code 1 by default because they don't know your circumstances, so a code-1 1099-R does not mean no exception applies to you.

| Exception | Who it covers | How to claim |

|---|---|---|

| Rule of 55 | You left that employer in or after the year you turned 55 — applies only to that employer's plan, not IRAs | Form 5329 with your return |

| Total and permanent disability | You can't engage in substantial gainful activity due to a condition expected to be long-term or fatal | Form 5329, keep medical proof |

| Medical expenses | Unreimbursed medical costs above 7.5% of your AGI that year — no itemizing required | Form 5329 |

| QDRO payout | Money paid to an ex-spouse under a qualified domestic relations order in a divorce | Form 5329 |

| IRS levy on the plan | The distribution happened because the IRS levied the account itself | Form 5329 |

| Emergency personal expense (SECURE 2.0) | One distribution of up to $1,000 per year for a personal emergency; repayable within 3 years | Form 5329 / plan reporting |

If an exception fits a return you already filed, you can amend and claim it — on a $15,000 withdrawal, that's $1,500 removed from the bill before you negotiate anything. What no exception ever removes: the ordinary income tax on the distribution. That part is real and needs a payment plan.

What happens if you ignore the bill

An unpaid balance from a 401(k) cash-out enters the same automated collection sequence as any other tax debt — and the sequence runs itself, whether or not a human at the IRS ever reads your file. With the IRS workforce down roughly 27% since 2025, humans are harder to reach, but the notices and levies never stopped. The stages, in order:

- Balance due at filing — interest and the 0.5%/month failure-to-pay penalty begin immediately. No notice needed.

- CP14 — the first bill, typically giving about 21 days before the next notice queues up. If you've got a CP14 and can't pay, this is still the cheapest stage to act.

- CP501 / CP503 — reminder notices. Still just bills, but the balance grows every month they sit.

- CP504 — intent to levy your state tax refund; a federal tax lien becomes a live possibility.

- LT11 / Letter 1058 — final notice. A 30-day clock starts on your Collection Due Process rights, and after it runs, the IRS can levy bank accounts, garnish wages, and levy 1099 payments owed to you by gig platforms.

- Levy — including, in flagrant cases, what's left in your retirement accounts. See can the IRS take my 401k for how far that reach goes.

The bitter irony of this topic: people who cashed out a 401(k) and then ignored the bill can eventually watch the IRS reach the rest of the account for a debt the first withdrawal created. You can estimate how fast your balance grows with our IRS Penalty & Interest Calculator.

Owe the IRS on a 401(k) cash-out — with returns still unfiled?

The order you fix this in changes what you pay: exceptions first, returns second, payment plan third. Interest and penalties accrue every month you wait. Get a free review of your 1099-R and your options from an experienced tax professional — no pressure, no obligation.

Your options when you can't pay taxes on a 401k withdrawal

The IRS has five real paths for a balance you can't pay at once, and eligibility is mostly mechanical — thresholds and compliance, not persuasion. (For the full walkthrough of negotiating any balance on your own, see our guide to how to settle tax debt yourself; here's how each path applies to a withdrawal bill specifically.)

| Option | Who qualifies | What it does |

|---|---|---|

| Short-term payment plan | Balances generally under $100,000; all required returns filed | Up to 180 extra days, $0 setup, enforcement paused |

| Guaranteed installment agreement | Tax of $10,000 or less, last 5 years filed and paid on time, payoff within 3 years | The IRS must accept it |

| Streamlined installment agreement | $25,000 or less — or up to $50,000 with direct debit; all returns filed | Up to 72 months, no financial disclosure |

| Currently Not Collectible | Paying anything would leave you unable to cover basic living expenses (Form 433-F math) | Collection pauses; the debt and interest remain |

| Offer in Compromise | Assets plus future income genuinely can't cover the debt; the IRS accepted roughly 1 in 5 offers in FY2024 | Settles for less than the full balance |

| Penalty relief (FTA / AEP) | Clean compliance history for the prior 3 years | Removes failure-to-file/failure-to-pay penalties — never the 10% additional tax |

Three notes specific to withdrawal bills. First, penalty abatement cannot remove the 10% early-distribution tax — it's an additional tax, not a penalty, so first-time penalty abatement applies only to the late-payment and late-filing penalties stacked on top. (Starting summer 2026, the new Automatic Exemption from Penalty applies that relief automatically — no request needed.)

Second, if you're weighing an Offer in Compromise, understand that the IRS can treat cashed-out retirement money as a dissipated asset — counted in your offer as if you still had it, depending on when and how it was spent. That single issue sinks more post-cash-out offers than the math itself.

Third, every option in the table above requires filed returns first. For a gig worker with unfiled years, that's the gate — more on it below.

| Option | Upfront cost | Ongoing cost | Typical timeline |

|---|---|---|---|

| Pay in full | The balance | None — accrual stops | Immediate |

| Short-term plan | $0 setup | Interest + 0.5%/mo failure-to-pay continue | Up to 180 days |

| Installment agreement | Modest setup fee — lowest online with direct debit, reduced or waived for low income | Interest continues; failure-to-pay drops to 0.25%/mo while the plan is active | Up to 72 months |

| Currently Not Collectible | $0 | Interest and penalties keep accruing; refunds are offset | Until finances improve — reviewed periodically |

| Offer in Compromise | $205 fee + 20% down on lump-sum offers (both waived with low-income certification, AGI ≤ 250% of poverty) | Offer payments per your terms | Often many months; auto-accepted if the IRS doesn't decide within 2 years, with narrow exceptions - a returned or rejected offer stops the clock, and time during court disputes does not count |

Say you owe $4,800: the worked math

Here's a clearly hypothetical example built on a common gig-economy pattern. Say you're 34, you drove and delivered on 1099s all year, and last winter you took a $15,000 hardship withdrawal from an old employer's 401(k) — waiving withholding, because you needed every dollar.

- Federal income tax at a 22% marginal rate: 22% × $15,000 = $3,300

- 10% additional tax on the early distribution: 10% × $15,000 = $1,500

- Total: $4,800 — on top of whatever self-employment tax the gig income created.

Now the payment paths. On a short-term plan, $4,800 over six months is $800/month with $0 setup — the cheapest route if your income can carry it. On a 72-month streamlined agreement, the arithmetic minimum is about $67/month ($4,800 ÷ 72), but interest plus the reduced 0.25%/month penalty keep accruing, so paying $100–$150/month retires it years sooner and far cheaper.

The guaranteed installment agreement looks perfect at under $10,000 — but it requires the last five years filed and paid on time. With three years unfiled, that door is closed until the returns go in, and those returns may add balances that change which plan you need. Which brings us to the real first step.

Three years unfiled? File before you negotiate anything

The IRS will not approve a payment plan, hardship status, or an offer while required returns are missing — filing is the gate to every option on this page. If you haven't filed taxes in 3 years, that's the first project, and it usually works in your favor.

Why it's urgent for the withdrawal year specifically: the plan already sent the IRS your 1099-R. Left unfiled long enough, the IRS can build a substitute return from it — treating the entire distribution as fully taxable, adding the 10% additional tax with no exceptions considered, and skipping the mileage and expense deductions that shrink a gig worker's real bill. Your own return is almost always smaller than the IRS's version of it.

Filing also swaps the penalty rate. The failure-to-file penalty runs 5% per month — ten times the 0.5% failure-to-pay rate — so filing today, even with zero payment attached, cuts the monthly bleed by roughly 90% on that year.

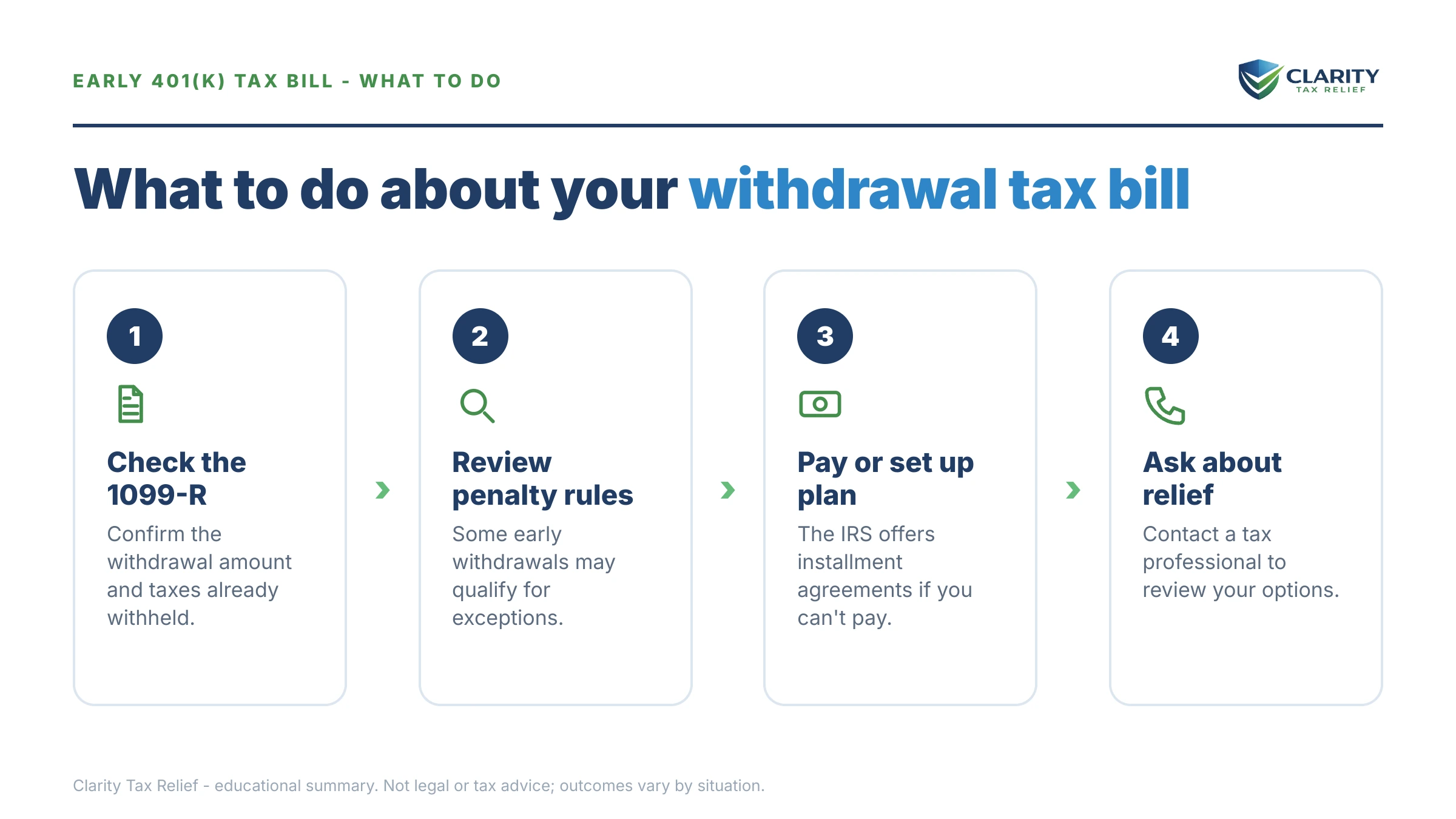

How to respond, step by step

- Pull your Form 1099-R. Confirm Box 1 (gross distribution), Box 4 (federal tax withheld), and the code in Box 7 — code 1 means early distribution with no known exception.

- Check the exception list. If the rule of 55, disability, medical expenses over 7.5% of AGI, or another exception fits, claim it on Form 5329 — it removes the 10% additional tax even when Box 7 shows code 1.

- File every unfiled return. The IRS will not approve any payment arrangement until required returns are in, and filing immediately stops the 5%-per-month failure-to-file penalty.

- Set up your payment path. Choose the short-term plan, an installment agreement, hardship status, or an offer based on the eligibility table above, and set it up at IRS.gov before the notice sequence escalates.

- Fix this year's estimates. Set aside tax on current gig income quarterly so next April doesn't stack a second balance on top of this one.

For the plan setup itself, our walkthrough on how to set up an IRS payment plan online covers the screens step by step, or go straight to the IRS's payment plans and installment agreements page. Payments of any kind go through IRS.gov/payments — never to anyone asking for gift cards or payment apps.

When you can handle this yourself — and when help changes the outcome

If this is a single filed year you agree with, the balance is a few thousand dollars, and you can clear it within 180 days, you don't need to hire anyone — the short-term plan takes ten minutes online and costs nothing to set up. Same for a straightforward streamlined agreement on one clean year.

Experienced help earns its cost in the messier versions: multiple unfiled years where income has to be reconstructed from platform records, a notice sequence already at CP504 or LT11, an exception claim the plan coded wrong, or Offer in Compromise math complicated by a cashed-out account the IRS may count as a dissipated asset. In those cases the sequencing — which year to file first, which penalties to fight, which plan to request — genuinely moves the final number.

Terms on your 1099-R and tax bill, decoded

- Form 1099-R — the form your plan sends you and the IRS reporting the distribution; it's why the IRS already knows about the withdrawal.

- Distribution code 1 — the Box 7 code meaning "early distribution, no known exception"; it triggers the 10% unless you claim an exception yourself.

- 10% additional tax — the early-distribution charge under the tax code; legally a tax, not a penalty, which is why abatement can't remove it.

- Form 5329 — the form where you report the additional tax or claim an exception to it (see the IRS's About Form 5329 page).

- Hardship withdrawal — a plan distribution for immediate financial need; it skips the plan's withdrawal restrictions but not the tax, and it can never be rolled back in.

- Failure-to-pay penalty — 0.5% of the unpaid balance per month (0.25% while an installment agreement is active), separate from interest.

401k withdrawal tax bill questions, answered

Can the IRS waive the 10% early withdrawal penalty on a 401k?

Not through penalty abatement — the 10% is legally an additional tax, not a penalty, so first-time abatement and reasonable-cause relief can't touch it. The only way off is a statutory exception (rule of 55, disability, medical expenses over 7.5% of AGI, and others) claimed on Form 5329. If your 1099-R shows code 1 but an exception genuinely fits, you can still claim it on your return or by amending.

Why do I owe the IRS when my 401k already withheld 20%?

The 20% withholding is a deposit toward your tax, not the tax itself. The withdrawal stacks on top of your other income and is taxed at your marginal rate — often 22% or higher — plus the 10% additional tax if you were under 59½. That means the true cost can run 32% or more, leaving a gap of 12 cents or more on every dollar you withdrew.

Can I set up a payment plan for a 401k withdrawal tax bill?

Yes — the IRS treats it like any other balance due. A short-term plan gives you up to 180 days with no setup fee, and balances of $50,000 or less can qualify for a monthly installment agreement of up to 72 months set up online. The catch for gig workers: the IRS requires all overdue returns to be filed before it approves any plan.

Can I put the money back into my 401k to undo the tax?

Usually only within 60 days of the distribution, by rolling it into an IRA or another plan — after that window closes, the tax generally stands. Narrow exceptions exist: certain SECURE 2.0 distributions, like the $1,000 emergency personal expense withdrawal and qualified disaster distributions, can be repaid within three years to reverse the tax. Hardship withdrawals cannot be rolled over at all.

Will the IRS take the rest of my 401k if I don't pay the bill?

It can — retirement accounts are not off-limits to a levy — but seizing retirement money is a last-resort step generally reserved for cases the IRS considers flagrant, and it comes only after the full notice sequence and a final notice with appeal rights. Setting up even a modest payment plan before that point takes a retirement levy off the table.

What happens if I never filed the return for the year I cashed out?

The IRS already has your 1099-R, so it can eventually file a substitute return for you — treating the entire distribution as fully taxable, adding the 10% additional tax with no exceptions, and allowing no deductions you could have claimed. Filing your own return almost always produces a smaller balance, and it stops the 5%-per-month failure-to-file penalty, which runs ten times the failure-to-pay rate.

Does cashing out my 401k hurt my chances at an Offer in Compromise?

It can. If you spent retirement money instead of paying the tax it created, the IRS may treat it as a dissipated asset and add the amount back into your offer calculation — as if you still had it. The impact depends on when the money was spent and what it went to; necessary living expenses are viewed very differently than discretionary spending.

Do I owe state taxes on a 401k withdrawal too?

In most states with an income tax, yes — the withdrawal counts as taxable income there as well, and a few states add their own early-distribution charge on top (California adds 2.5%). No-income-tax states like Florida and Texas take nothing. State agencies bill separately and run their own collection timelines, so a federal payment plan does nothing for a state balance.

Your next 24 hours

- Find your 1099-R and write down three numbers: Box 1 (what the IRS taxes), Box 4 (what was withheld), and the Box 7 code. If Box 7 says 1, run the exception table above before accepting the 10%.

- Gather what filing takes: your last filed return, platform earnings summaries or 1099s for every unfiled year, and any mileage or expense records — even partial ones.

- Get a free case review. An experienced tax professional can map the exception, the filings, and the right payment plan in one conversation — before another month of penalties and interest lands. Use the 2-minute form or call (888) 825-7779.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.