Penalty Relief

First Time Penalty Abatement in 2026: How to Qualify, How to Ask, and What It's Worth

The short answer: first time penalty abatement (FTA) removes the IRS failure-to-file, failure-to-pay, or failure-to-deposit penalty for one tax period. You may qualify if you had no penalties in the prior three tax years, every required return is filed, and you've paid or arranged to pay. It's free to request — often one phone call does it.

The tax was hard enough to look at. Then you and your spouse read the notice a second time and realized a big slice of the total isn't tax at all — it's penalties, stacked on top of a number that already hurt. What no notice tells you is that the IRS's own manual contains a standing waiver that removes those penalties for people with a clean recent history. You just have to know it exists and ask.

This guide covers the three eligibility tests, which penalties FTA does and doesn't reach, the exact request process, and the biggest change to this program in decades: the Automatic Exemption from Penalty (AEP) rolling out in summer 2026. Farther down, the image shows you exactly where those penalty lines sit on an IRS bill and account transcript — so you'll know precisely which numbers you're asking the IRS to remove.

⏱ The clock that matters: first-time penalty abatement has no application deadline — but the failure-to-pay penalty adds another 0.5% of your unpaid tax every month until you pay or hit its 25% cap, and interest compounds on all of it. If you already paid the penalty, a refund claim is generally due within three years of filing the return or two years of paying, whichever is later.

Why your bill has penalty lines in the first place

The failure-to-file penalty runs at 5% of the unpaid tax per month — ten times the 0.5% monthly failure-to-pay rate. Those two charges, plus the failure-to-deposit penalty on business payroll accounts, are the penalties that FTA exists to remove. Everything else on the bill — the tax itself and the interest on that tax — stays even after a successful abatement.

Each penalty caps at 25% of the unpaid tax, which is how a five-figure balance quietly grows a five-figure penalty layer. For the full penalty math — how the two rates interact month by month and what interest does on top — see our guide to how much are IRS penalties on back taxes, and the breakdown of the failure to file penalty vs failure to pay penalty.

The important reframe: penalties are the one part of an IRS bill that has a built-in removal policy. The tax you owe. The interest follows the tax. The penalties are negotiable — through FTA, reasonable cause, or, starting this summer, automatically.

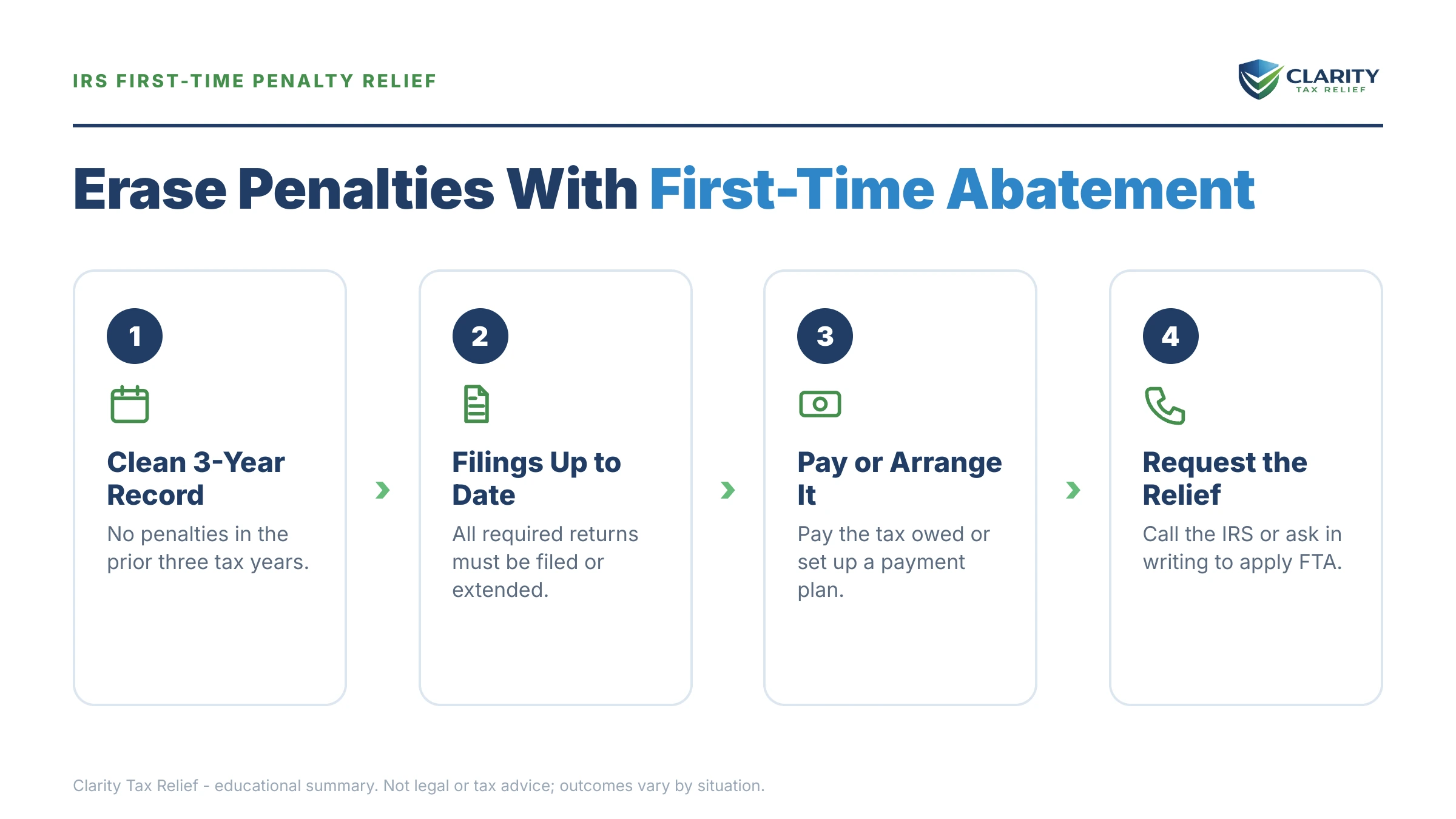

Do you qualify for first time penalty abatement? The three tests

FTA has exactly three requirements, and the IRS checks all three before granting it. There's no hardship test, no explanation required, and no fee — this is an administrative waiver, not a mercy plea.

Test 1 — clean compliance history. You had no penalties (other than the estimated-tax penalty) on the same type of return for the three tax years before the penalty year. A penalty the IRS previously removed for reasonable cause generally doesn't count against you. A first-time abatement granted within those three years does count — that's the disqualifier that surprises the most callers.

Test 2 — filing compliance. Every return you're required to file is filed, or on a valid extension. One unfiled year anywhere on your account fails this test, even if it's not the penalty year. Fix the filing gap first, then request.

Test 3 — payment compliance. You've paid the balance, or you've "arranged to pay" — an installment agreement in good standing satisfies this. If you have neither, setting up an IRS payment plan online before you call is usually the fastest way to pass.

Notice what's absent: no income limit, no dollar cap on the penalty, no requirement that this literally be your "first" penalty ever. If the three years before the penalty year are clean, a taxpayer who had penalties a decade ago may still qualify.

Which penalties first-time abatement covers — and which it can't touch

FTA reaches exactly three penalties: failure-to-file, failure-to-pay, and failure-to-deposit. If your notice shows a different penalty type, FTA is the wrong tool — but a different one usually exists, and asking for the wrong relief wastes the request.

| Penalty | How it's charged | FTA covers it? | If not, your path |

|---|---|---|---|

| Failure-to-file | 5%/month of unpaid tax, max 25% (4.5% in months where failure-to-pay also runs) | Yes | — |

| Failure-to-pay | 0.5%/month of unpaid tax, max 25% | Yes | — |

| Failure-to-deposit (payroll) | Tiered 2%–15% of the late deposit | Yes — business accounts | — |

| Estimated-tax penalty | Interest-style charge on underpaid quarterlies | No | Form 2210 waiver (casualty, disaster, retirement, disability) |

| Accuracy-related penalty | 20% of the understated tax | No | Reasonable cause or audit appeal |

| Civil fraud penalty | 75% of the underpayment | No | Representation — this is a legal defense, not a waiver request |

One more boundary: FTA applies to one tax period per request. If penalties span 2022, 2023, and 2024, a single FTA grant can clear one of those years — the strategy for the rest is covered below and in our guide to first time abatement multiple years.

What happens if you ignore the penalties

Unremoved penalties don't sit in a separate bucket — they're folded into the balance the IRS collects on, so the collection machine escalates against the whole number, penalties included. The sequence is automated and runs in a fixed order:

- First bill (CP14) — the balance with tax, penalties, and interest itemized. You typically have about 21 days from the notice date before the sequence moves — but only 10 business days if the balance is $100,000 or more.

- Reminder notices (CP501 / CP503) — same balance, larger, as failure-to-pay and interest post each month.

- CP504, Notice of Intent to Levy — the IRS gains the power to seize your state tax refund, and a federal tax lien becomes a live risk.

- LT11 / Letter 1058, Final Notice — a 30-day clock to a wage or bank levy, with Collection Due Process appeal rights you must invoke in time. Once a final intent-to-levy notice issues, the failure-to-pay rate also doubles to 1% per month.

The penalty layer has teeth beyond the notices, too. Penalties and interest count toward the $66,000 passport-certification threshold for 2026 — a tax debt that started under the line can be pushed over it by the penalties alone. And in 2026, with the IRS workforce down roughly 27%, the humans are harder to reach while the automated notices, liens, and levies never paused. The machine escalates whether or not anyone reads your file.

Conversely, acting has a rate benefit: while an installment agreement is in place, the failure-to-pay rate drops to 0.25% per month. Doing nothing is the single most expensive option on this page.

Penalties still compounding on your balance?

Every month adds another 0.5% failure-to-pay penalty plus interest — and one phone call may remove the whole penalty layer. Get your three-year penalty history reviewed free by an experienced tax professional, who'll tell you which years qualify for first-time abatement before the next month posts.

Your options for IRS penalty relief in 2026, compared

Every penalty-relief path the IRS offers is free to request — the differences are speed, evidence required, and which situations each one fits. FTA is the fastest because it's mechanical: the IRS checks three facts and decides. The others take longer but reach further.

| Option | Cost | Typical timeline | Best fit |

|---|---|---|---|

| FTA by phone | $0 | Often decided on the call; written confirmation follows by mail | Clean 3-year history, penalty on one period |

| FTA in writing / Form 843 | $0 | Typically several weeks to a few months | Larger penalties, already-paid penalties, or a stalled phone request |

| AEP (automatic, from summer 2026) | $0 | Applied by the IRS with no request | Qualifying penalties assessed after the rollout — verify it posted |

| Reasonable cause | $0 | Weeks to months; documentation required | Illness, death in the family, disaster, records genuinely unavailable |

| Interest abatement (§6404) | $0 | Months; rarely granted | Interest caused by IRS error or delay only |

| Appeal of a denial | $0 | Adds months to the process | Denials from the automated screening tool |

The 2026 change worth knowing: starting this summer, the IRS is replacing the request-based FTA process with the Automatic Exemption from Penalty (AEP) — the same style of relief, applied automatically with no phone call or letter. Two cautions. First, AEP covers qualifying penalties going forward; penalties already sitting on your account from earlier assessments may still need the traditional request. Second, "automatic" means verify, not assume — check your transcript for the abatement rather than trusting that the system caught you.

If your history isn't clean — a penalty two years ago knocks you out of FTA — reasonable cause penalty abatement is the fallback. It requires showing that circumstances beyond your control (serious illness, a death, a disaster, reliance on bad advice) caused the noncompliance, with dates and documentation. It's slower and more subjective, but it has no clean-history requirement and can cover multiple years at once.

The math on a $68,500 balance: what FTA is actually worth

Say you and your spouse owe $68,500 in tax on your joint 2024 return — a stock sale under-withheld, and the return went in five months late, in September 2025. Here's what the penalty layer looks like by mid-2026, with the arithmetic shown:

- Failure-to-file: 4.5% per month for the five late months (the rate drops from 5% because failure-to-pay runs at the same time). 4.5% × 5 = 22.5%. On $68,500, that's $15,412.50.

- Failure-to-pay: 0.5% per month since April 2025 — call it 15 months by July 2026. 0.5% × 15 = 7.5%. On $68,500, that's $4,795 rising toward $5,137.50 as the months post.

- Penalty layer total: roughly $20,500 — before counting the interest that compounds on the tax and on the penalties.

If 2021 through 2023 were penalty-free, all returns are filed, and a payment plan is in place, a single first-time abatement request on the 2024 period removes that entire penalty layer, plus the interest that accrued on those penalties. What stays: the $68,500 in tax and the interest on the tax itself. To run your own numbers, our IRS Penalty & Interest Calculator estimates both penalties month by month.

One timing note at this dollar level: $68,500 is above the $50,000 line for the streamlined online installment agreement, so the payment plan that satisfies Test 3 will likely require financial disclosure or a partial paydown first. And because failure-to-pay keeps accruing on the unpaid tax after an abatement, some filers deliberately request FTA near the end of the payoff so one request captures the maximum penalty. That's a judgment call worth making with real numbers in front of you.

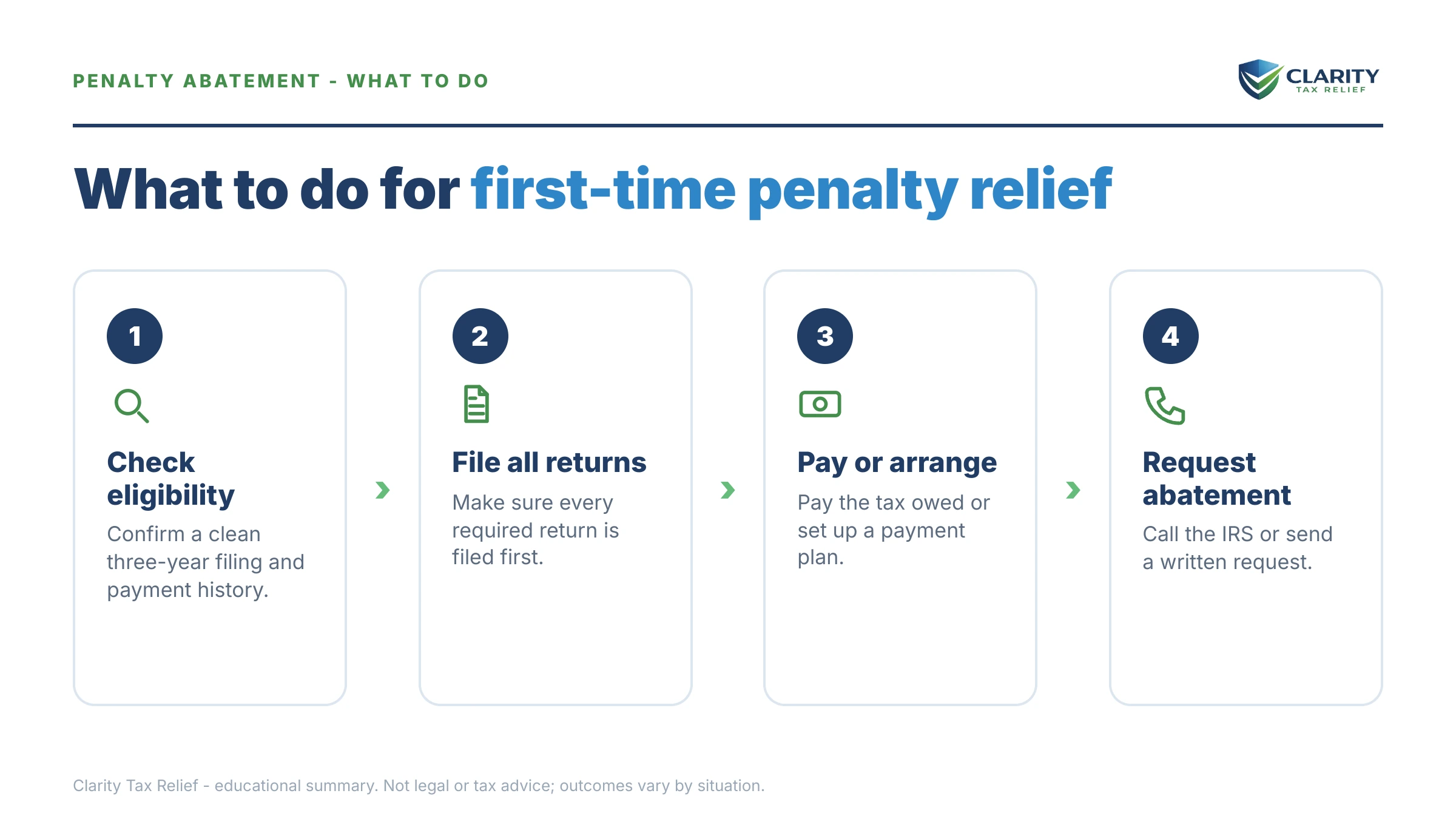

How to request first-time penalty abatement, step by step

- Pull your IRS account transcript. Download the account transcript for each penalty year from your IRS online account and confirm which penalties posted, in what amounts, and for which tax periods.

- Fix any compliance gaps first. File every required return that is missing and pay the balance or set up a payment plan — the IRS checks filing and payment compliance before it grants first-time abatement.

- Call the number on your notice and ask for first-time abatement by name. The agent runs your three-year history while you are on the line, and smaller penalties are often removed during the call. Write down the agent's ID number and the outcome.

- Put the request in writing if needed. If the phone request stalls, the penalty is large, or you already paid it, send a short letter or Form 843 to the address on your notice and keep a copy of everything.

- Verify the abatement on your transcript and appeal a denial. Watch for the abatement codes to post, confirm the recalculated balance, and use your appeal rights within the window stated on any denial letter.

For the written route, our Form 843 penalty abatement request walkthrough covers each box, and we publish a free first time penalty abatement letter sample you can adapt in minutes. If the request is denied, a penalty abatement appeal gets a human reviewer instead of the automated tool — and reversals are common when the denial rested on a stale compliance record. The IRS's own overview of these programs is at IRS.gov penalty relief, with the form itself at About Form 843.

Reading the penalty codes on your IRS account transcript

Your account transcript — not the notice — is the authoritative record of what was charged and what was removed. The image below shows you exactly what these lines look like and where to find them; here's what each code means when you get there:

| Transcript code | What it means | What to do |

|---|---|---|

| 166 | Failure-to-file penalty assessed | A primary FTA target — note the amount and tax period |

| 276 | Failure-to-pay penalty assessed | Also FTA-eligible; it keeps accruing until the tax is paid |

| 196 | Interest charged | Interest on the tax survives abatement; interest on an abated penalty comes off with it |

| 167 / 277 / 197 | Penalty or interest abated | Proof your request worked — confirm the amounts match your grant |

| 971 | Notice issued | Match the date to the letter in your hand to track where you are in the sequence |

If your transcript shows a 276 but you're not sure why, our guide to code 276 transcript lines explains how that penalty posts and recalculates as you pay.

Situations that change the answer

Married filing jointly

On a joint return, the IRS checks both spouses' compliance histories — a penalty on either spouse's account within the three-year window can break the clean-history test for the couple. If one of you filed separately or ran a business in those years, pull transcripts for both before you call, so a surprise on your spouse's record doesn't torpedo the request mid-conversation.

Penalties across multiple years

FTA clears one period, so the standard play is FTA on the earliest eligible year, then reasonable cause — with documentation — for the years after it. Sequencing matters, because a penalty left standing on an early year blocks FTA on the later ones. The full strategy is in first time abatement multiple years.

Business and payroll penalties

FTA covers the failure-to-deposit penalty on payroll accounts, and each 941 quarter is its own period with its own history test — which cuts both ways when several quarters slipped. Payroll penalties also escalate into personal-liability territory faster than income-tax penalties do, so treat them with more urgency; see 941 penalty abatement for the payroll-specific rules.

You already paid the penalty

Paid penalties aren't gone — they're refundable if you would have qualified. The request becomes a refund claim on Form 843, and the claim window (generally the later of three years from filing or two years from payment) is a hard cutoff. If you're anywhere near it, file the claim now and refine later.

State penalties are a different system

None of the IRS rules on this page apply to state penalties. California's Franchise Tax Board, for example, runs its own separate one-time abatement program with its own eligibility rules — covered in our FTB penalty abatement guide. For other states, check with that state's tax agency directly rather than assuming an IRS-style waiver exists.

When you can handle this yourself — and when help changes the outcome

Most single-year FTA requests are genuinely do-it-yourself. If you have one penalty year, a clean prior three years, all returns filed, and a balance you can pay or put on a plan, one phone call with your transcript in front of you will usually resolve it — no professional needed, and anyone who tells you otherwise is selling.

Experienced help changes outcomes in the harder patterns: penalties spread across multiple years where the FTA-then-reasonable-cause sequencing determines how much comes off; business or payroll penalties where personal liability may be lurking behind the abatement question; five-figure penalty layers where a denied request is worth appealing properly; already-paid penalties near the refund-claim cutoff; and any case where the compliance record itself is wrong and has to be corrected before the automated tool will say yes. In those cases, the fee for help is usually small against the penalty dollars at stake — and a candid review will tell you if it isn't.

Two free resources worth knowing either way: the Taxpayer Advocate Service for cases stuck in IRS processing, and your own IRS online account for real-time balance and transcript access — especially valuable in 2026, when reaching a human by phone takes longer than it used to.

If your transcript shows penalties across several years or a payroll return in the mix, get a free penalty review or call (888) 825-7779 — an experienced tax professional can map which years first-time abatement reaches and which need reasonable cause, before another month of failure-to-pay posts.

Terms on your notice, decoded

- Abatement — the IRS removing a charge it already assessed; the reversal posts to your transcript as its own line.

- First-Time Abate (FTA) — the administrative waiver in the IRS manual that removes one period's failure-to-file, failure-to-pay, or failure-to-deposit penalty based on a clean three-year history.

- Automatic Exemption from Penalty (AEP) — the successor program rolling out from summer 2026 that applies the same relief automatically, with no request.

- Reasonable cause — penalty relief based on circumstances beyond your control (illness, death, disaster), proven with documentation rather than a clean history.

- Clean compliance history — no penalties (other than estimated-tax) on the same return type in the three years before the penalty year.

- Form 843 — the IRS form used to request abatement in writing or to claim a refund of a penalty you already paid.

First time penalty abatement: your questions, answered

How do I ask the IRS for first-time penalty abatement?

Call the number on your penalty notice and ask for first-time abatement by name — the agent runs an eligibility check while you are on the line. Smaller penalties are often removed during the call; larger penalties, or penalties you already paid, usually need a written request or Form 843. Either way, note the agent's ID number and ask for written confirmation of the decision.

Does first-time abatement remove interest too?

Not on the tax itself. When a penalty is abated, the interest that accrued on that penalty comes off automatically, but interest on the underlying tax keeps running until the balance is paid. The IRS only abates interest on the tax in narrow situations involving its own errors or delays, which is a separate request from first-time abatement.

Can I get first-time abatement if I still owe the balance?

Yes — the payment test is paid or arranged to pay, so an installment agreement in good standing counts. One timing caveat: the failure-to-pay penalty keeps accruing on whatever tax remains unpaid, so an abatement granted today only removes what has posted so far. Many people wait until the balance is nearly paid so a single request captures the full penalty amount.

How many times can you use first-time penalty abatement?

More than once — the name is misleading. FTA is not a once-per-lifetime waiver; you can qualify again any time you have three clean years since your last penalty. What you cannot do is use it for two back-to-back years, because the penalty on the earlier year breaks the clean-history test for the later one.

Does an estimated-tax penalty in a prior year disqualify me?

No. The clean-history test ignores the estimated-tax penalty when the IRS reviews your prior three years, and a penalty that was previously removed for reasonable cause generally does not count against you either. A first-time abatement granted within the last three years does count, though — that is the most common hidden disqualifier people discover on the call.

Can I get first-time abatement for multiple years at once?

No — FTA applies to a single tax period. When several years carry penalties, the usual strategy is to apply FTA to the earliest eligible year, then request reasonable-cause relief for the remaining years with documentation of what went wrong. The order matters, because a penalty left standing on an early year can block FTA on a later one.

Is first-time abatement going away in 2026?

It is being replaced by something more generous. Starting in summer 2026, the IRS is rolling out Automatic Exemption from Penalty (AEP), which applies the same style of relief automatically, with no request needed. Penalties assessed before the rollout, or outside AEP's reach, still require the traditional request — so verify on your transcript rather than assuming relief was applied.

What if my first-time abatement request is denied?

You can appeal, and denials get reversed regularly. Many denials come from the IRS's automated screening tool misreading a compliance record — an unfiled return that was actually filed, or a payment plan that had not posted yet. Fix the underlying record, re-request, and if the denial stands, file a written appeal within the window stated on the denial letter.

Can I get back a penalty I already paid?

Yes, as a refund claim on Form 843 rather than a phone request. Refund claims are generally due within three years of when you filed the return or two years of when you paid the penalty, whichever is later. If you are near the end of that window, file the claim first and sort out the details after — a late claim is gone for good.

Your next 24 hours

- Find the penalty breakdown. On your notice or account transcript, locate the failure-to-file and failure-to-pay lines — the exact dollar amounts, by tax year, that a successful request would remove.

- Gather three things: the notice itself, your last three years of returns (to confirm the clean-history window), and proof of any payment plan or payments made.

- Get the free penalty review. Use the 2-minute form or call (888) 825-7779 — an experienced tax professional will check which years qualify for first-time abatement and which need reasonable cause, while the failure-to-pay penalty and interest are still accruing on every month you wait.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.