IRS Penalties

IRS Civil Fraud Penalty: What the 75% Penalty Means and How to Fight It (2026)

The short answer: the IRS civil fraud penalty is 75% of any tax underpayment caused by intentional wrongdoing, under IRC §6663. Unlike most penalties, the IRS — not you — bears the burden of proof, and must show fraud by clear and convincing evidence. You can challenge it at Appeals or in Tax Court before paying a dollar.

You're looking at an audit report, and buried below the adjustments is a line you had to read twice: "Civil fraud penalty — IRC §6663 — 75%." The word "fraud," in writing, from the federal government, aimed at your return. That word is designed to be alarming — but a proposed fraud penalty is a position the IRS must prove, not a verdict, and it gets defeated or reduced regularly by people who respond correctly and on time.

This guide covers what makes the civil fraud penalty different from every other IRS penalty: the 75% rate, the reversed burden of proof, the unlimited lookback, the joint-return spouse rule, and the exact deadlines that decide whether you fight it before paying or after. The image below shows exactly what a fraud-penalty proposal looks like on an exam report and where to find the section that matters most.

⏱ Your deadline: if the penalty arrived in a notice of deficiency (90-day letter), you have 90 days from the notice date to petition the U.S. Tax Court — your last chance to fight the penalty before paying it. If it came in an exam report with a 30-day letter (such as Letter 950), you typically have 30 days to file a written protest with IRS Appeals. Check the date printed on your letter; it controls.

Why the IRS proposed a civil fraud penalty on your return

The civil fraud penalty under IRC §6663 equals 75% of the portion of an underpayment attributable to fraud — the harshest percentage penalty in the civil tax code. Examiners don't propose it casually. It usually surfaces at the end of an audit where the examiner believes the errors weren't errors at all: income deliberately left off, deductions invented, records altered or withheld.

Two procedural facts work in your favor from day one. First, the penalty requires written supervisory approval under IRC §6751(b) before it's formally communicated to you — a missing or late approval has sunk real fraud penalties in court. Second, the penalty rides deficiency procedures, meaning you get Appeals and Tax Court review before you ever have to pay.

One trap to understand early: once the IRS establishes that any part of the underpayment is due to fraud, the law presumes the entire underpayment is fraudulent — unless you prove, item by item, which portions weren't. That's why a fraud response is built adjustment by adjustment, not as one blanket denial.

How the IRS proves civil fraud: the badges of fraud

To sustain the civil fraud penalty, the IRS must prove fraud by clear and convincing evidence — a standard far above the one used for ordinary penalties, where the burden usually sits on you. Fraud means intent to evade tax. Sloppy bookkeeping, a misunderstood rule, or a preparer's mistake doesn't reach it.

Because no one confesses intent, examiners build circumstantial cases from what courts call the "badges of fraud":

- A pattern of understated income across multiple years — not a single miss

- Two sets of books, altered documents, or false invoices

- Concealing assets or income — nominee accounts, an undisclosed foreign account, unexplained cash

- Dealing extensively in cash to avoid a paper trail

- False or inconsistent statements to the examiner during the audit

- Destroying records, or "losing" only the records that would answer the key question

- Implausible or shifting explanations for the discrepancies

One badge alone rarely carries the case; a cluster does. That's also why what you say during the audit matters so much — statements made to "clear things up" often become the false-statement badge that completes the pattern. If your audit has this undercurrent, read our guide to the eggshell audit, where civil questions sit on top of criminal exposure.

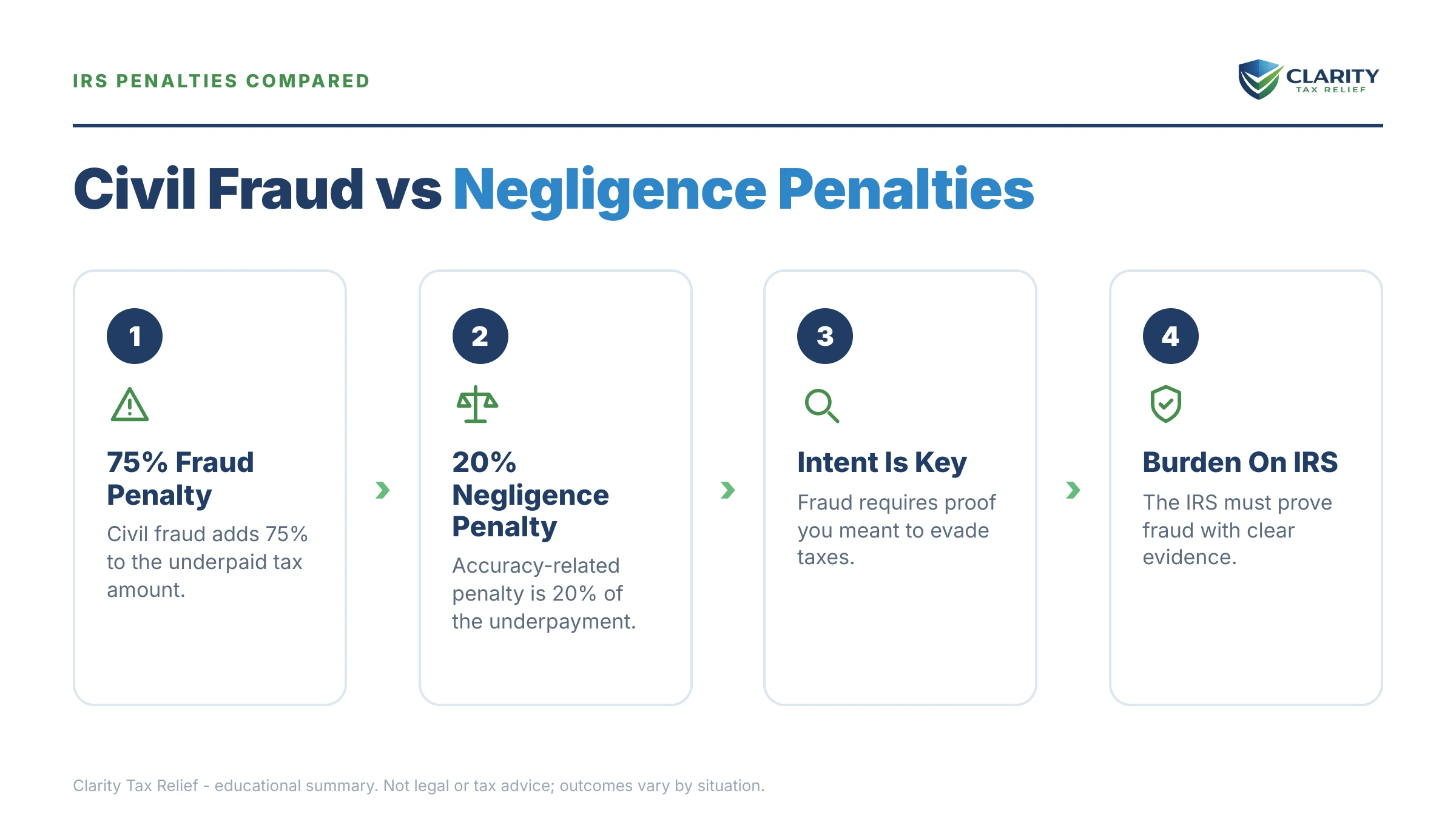

Civil fraud vs. negligence: the 20% line and the 75% line

The same understatement of tax can cost 20% as negligence or 75% as fraud — the difference is intent, and the two penalties cannot be stacked on the same dollars. When an examiner can't carry the fraud burden, the fallback is the accuracy-related penalty under §6662, which is both cheaper and easier for the IRS to sustain. A large share of successful fraud-penalty defenses end exactly there: fraud dropped, 20% conceded.

Here is how the fraud penalty compares to its neighbors:

| Penalty | Rate | Who must prove what |

|---|---|---|

| Civil fraud (IRC §6663) | 75% of the underpayment due to fraud | IRS must prove fraud by clear and convincing evidence |

| Fraudulent failure to file (IRC §6651(f)) | 15% per month, up to 75% of unpaid tax | IRS must prove the non-filing itself was fraudulent |

| Accuracy-related (IRC §6662) | 20% of the underpayment | You defend by showing reasonable cause and good faith |

| Criminal tax evasion (IRC §7201) | Fines and possible prison — separate prosecution | Government must prove guilt beyond a reasonable doubt |

That last row deserves a plain word. The civil fraud penalty is money, not prison — but it grows from the same facts as criminal tax evasion, and the two can run in parallel. A civil fraud proposal doesn't mean you're being prosecuted, and most never become criminal cases. But if your facts involve large unreported income, false documents, or several years, understand when the IRS refers a case to criminal investigation and what an IRS criminal investigation contact looks like — before you say anything else to the examiner.

If a fraudulent return also went unfiled or was filed late, the §6651(f) fraudulent failure-to-file penalty can apply instead of the ordinary late-filing penalty — same 75% ceiling, reached at 15% per month. For how ordinary penalties compound on a balance, see our hub on how much IRS penalties on back taxes really cost.

What a fraud penalty costs: a worked example at $7,400

A civil fraud finding roughly doubles a tax bill before interest is even counted. Say a married couple filing jointly is audited, and the examiner finds $7,400 in additional tax from income one spouse's side business never reported — and proposes the full amount as fraudulent. The math:

- Additional tax: $7,400

- Civil fraud penalty: 75% × $7,400 = $5,550

- Total before interest: $12,950

- If the same $7,400 were negligence instead: 20% × $7,400 = $1,480 — a difference of $4,070 riding entirely on the fraud question

Interest compounds daily on both the tax and the penalty — and on fraud cases, interest on the penalty runs from the return's original due date, not from the audit. On a return three or four years old, that quietly adds thousands more. You can estimate how interest and penalties stack on your own numbers with our IRS Penalty & Interest Calculator.

Now the presumption trap in action: suppose the couple can document that $4,000 of the $7,400 came from an honest basis error, and only $3,400 traces to the concealed income. If they prove that split, the fraud penalty falls from $5,550 to 75% × $3,400 = $2,550 — a $3,000 swing won purely with paperwork. If they never make that showing, the law treats all $7,400 as fraudulent.

Married filing jointly: which spouse actually owes the penalty

On a joint return, the civil fraud penalty applies only to the spouse whose own fraud caused the underpayment. That's IRC §6663(c), and it's one of the most overlooked defenses in these cases. If one spouse ran the concealed side income and the other simply signed the return, the IRS cannot impose the 75% penalty on the non-fraudulent spouse unless it proves that spouse's own fraudulent conduct.

Two cautions. The underlying tax is still a joint liability — §6663(c) protects a spouse from the penalty, not the balance. And the protection isn't automatic: it has to be raised, with facts, during the exam or in the Appeals protest. For the underlying tax, a separate path exists — see how to qualify for innocent spouse relief under Form 8857, which runs on its own track and its own deadlines.

What happens if you ignore a proposed civil fraud penalty

A fraud penalty you don't contest becomes an assessed debt with interest backdated years — and fraud eliminates the normal audit time limit entirely. Under IRC §6501(c)(1), a fraudulent return has no statute of limitations on assessment: the IRS can reach back past the usual three- or six-year window (our guide to how far back the IRS can audit explains the tiers). Here's the sequence if you let each window close:

- The 30-day window passes. If the penalty came with a 30-day letter like Letter 950 and you don't protest, you lose the cheapest, fastest forum — a pre-assessment Appeals conference — and the file moves toward a statutory notice.

- Notice of deficiency issues. The 90-day letter and Tax Court petition window is your last chance to contest the fraud finding before paying. In Tax Court, the IRS still carries the clear-and-convincing burden.

- The 90 days pass. The tax and the 75% penalty are assessed together, and interest computed back to the return's original due date posts all at once. From here, removing the penalty generally means paying first and suing for a refund.

- Collection begins. The balance enters the ordinary collection machine — bills, then a final notice of intent to levy with 30 days to request a CDP hearing via Form 12153, then liens and levies. In 2026, that machine runs automated even with IRS staffing down sharply.

Facing a proposed 75% fraud penalty right now?

A civil fraud proposal is the most serious finding an examiner can make — and the response window on your letter is already running. Get the exam report reviewed free by an experienced tax professional before the 30-day protest or 90-day petition deadline closes. Confidential, no pressure.

Your options for fighting or resolving the penalty

Every path to defeating a civil fraud penalty runs through one fact: the IRS bears the burden of proof, and burdens that heavy create settlement leverage. Your realistic options, roughly in the order they arise:

- Appeals protest (free). A written protest within the 30-day window sends the case to the IRS Independent Office of Appeals, which settles based on "hazards of litigation" — the odds the IRS loses in court. Fraud penalties are hard to prove, so Appeals frequently trades the 75% penalty down to the 20% accuracy-related penalty, or drops it, in exchange for agreement on the tax.

- Tax Court petition (about a $60 filing fee). Filed within 90 days of a notice of deficiency, this contests the penalty before you pay. Most docketed cases still settle with Appeals before trial.

- The §6751(b) approval defense. If the examiner's supervisor didn't approve the penalty in writing before it was first communicated, the penalty can fail on procedure alone — regardless of the facts. Always worth checking.

- Shrink the fraudulent portion. Even where some fraud is conceded, proving which dollars weren't fraudulent cuts the penalty directly, as the worked example above shows.

- The §6663(c) spouse defense on joint returns, covered above — it removes the penalty from a non-fraudulent spouse entirely.

- Pay, then claim a refund. After assessment, the remaining route is paying the penalty and pursuing a refund claim, and suing if it's denied. Slower and costlier — which is why the pre-assessment windows matter so much.

- Resolve what stands. A sustained penalty becomes part of your total balance, which may be workable through an installment agreement or, if your finances genuinely qualify, an Offer in Compromise. Know what doesn't work: first-time abatement and reasonable-cause waivers don't remove a fraud penalty. Those tools — including a well-built IRS penalty abatement letter — apply to the ordinary penalties that may also sit on your account, and clearing those still shrinks the bill.

Keep the deadlines and the right each one protects in one place:

| Stage | Your window | The right at stake |

|---|---|---|

| Exam report + 30-day letter (e.g., Letter 950) | Typically 30 days from the letter date | Written protest → pre-assessment Appeals conference |

| Notice of deficiency (90-day letter) | 90 days from the notice date | Tax Court review before you pay anything |

| After assessment | Before collection notices escalate | Payment arrangement stops enforcement; refund claim remains for the penalty |

| Final notice of intent to levy (LT11/Letter 1058) | 30 days from the notice date | Collection Due Process hearing via Form 12153 before levy |

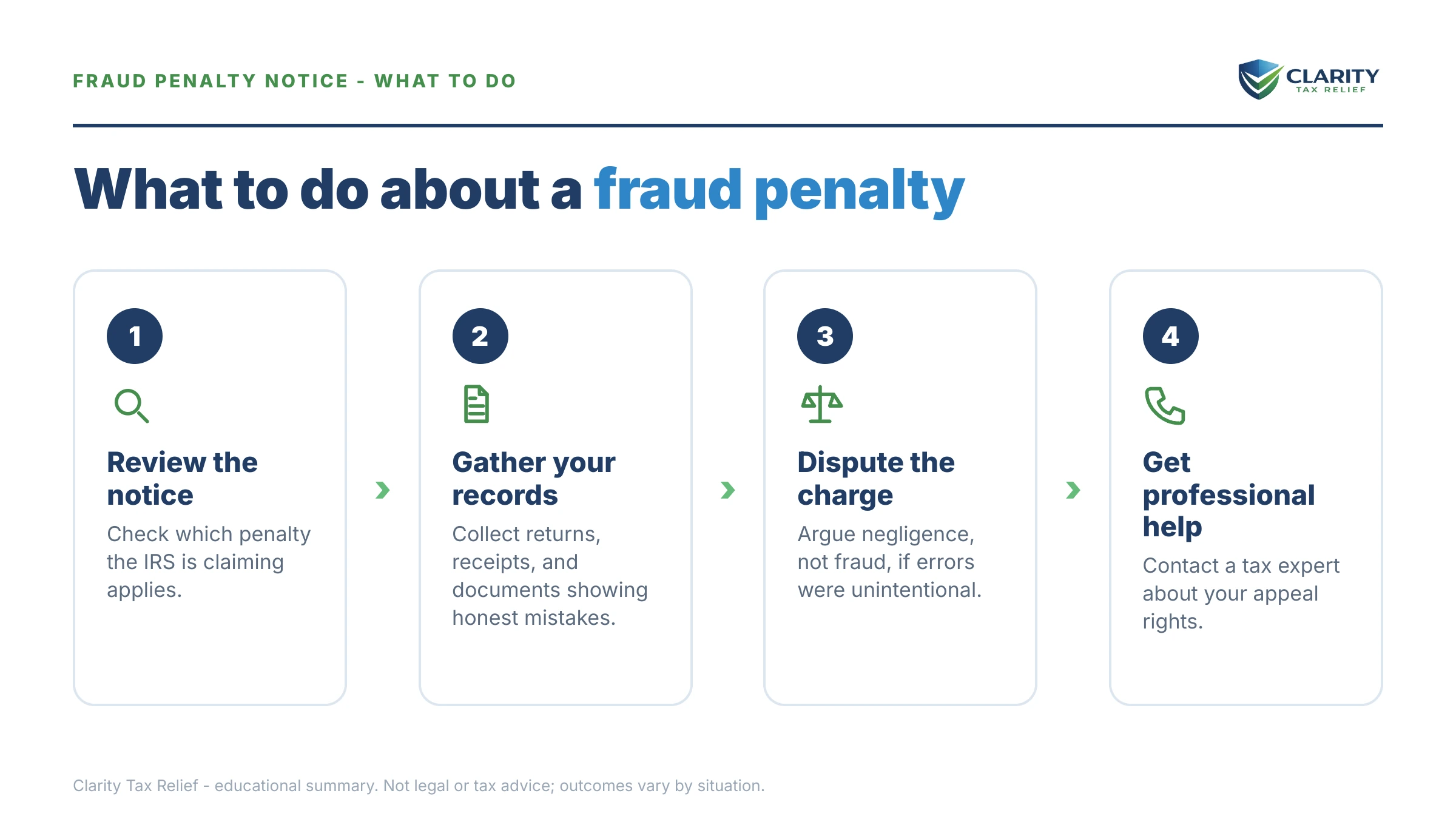

How to respond to a civil fraud penalty, step by step

- Find the penalty on your report. Open the exam report or notice and locate the line citing IRC §6663 or "civil fraud penalty." Note which adjustments it attaches to and the response deadline printed on the letter.

- Stop volunteering information. Don't call the examiner to "explain" before you understand your exposure. Statements you make now can be used in both the civil case and any criminal referral.

- Gather your records. Pull the audited return, the full exam report, and every document behind the adjusted items — bank statements, invoices, correspondence. Gaps you can fill honestly weaken the fraud case.

- Meet the deadline in writing. File a written protest with IRS Appeals within the 30-day window, or petition the U.S. Tax Court within 90 days of a notice of deficiency. Missing both converts the proposal into an assessed debt.

- Resolve the remaining balance. Once the penalty fight is decided, set up a payment plan or explore other resolution for whatever balance stands, before collection notices escalate.

When you can handle this yourself — and when you shouldn't

Honest answer: the civil fraud penalty is the one IRS penalty we almost never suggest handling alone. Where a CP14 or a late-filing penalty is often a DIY fix, a fraud proposal means an examiner has already built an intent case against you, every statement you make can feed it, and the money at stake is 75 cents on every disputed dollar plus backdated interest.

You can reasonably self-handle the aftermath: if the penalty was withdrawn or reduced at exam and you agree with the remaining tax, setting up your own payment plan is straightforward. And if your notice actually shows a 20% §6662 penalty — not §6663 — the stakes and the playbook are different, and a documented reasonable-cause response is realistic on your own.

Experienced help changes outcomes when: the penalty spans multiple years; the audit involves unreported cash, offshore accounts, or false documents; you're weighing what to say to an examiner who is still asking questions; a spouse's conduct — not yours — created the problem; or a 30-day or 90-day clock is already running. Those are exactly the cases where the burden-of-proof leverage gets won or lost in the protest.

Terms on your notice, decoded

- IRC §6663: the tax-code section imposing the 75% civil fraud penalty on underpayments caused by fraud.

- Underpayment: the gap between the tax you should have reported and the tax you did — the base the 75% is computed on.

- Badges of fraud: the circumstantial patterns (hidden income, false records, cash dealings) courts accept as proof of intent.

- Clear and convincing evidence: the elevated proof standard the IRS must meet — well above the "more likely than not" standard used for most civil issues.

- Notice of deficiency: the "90-day letter" that formally proposes the tax and penalty and opens your Tax Court window.

- §6751(b) approval: the required written supervisor sign-off; if it's missing or late, the penalty can fail on procedure alone.

Civil fraud penalty questions, answered

What is the IRS civil fraud penalty rate?

The civil fraud penalty is 75% of the portion of your tax underpayment that's attributable to fraud, under IRC §6663. It's the largest percentage penalty in the civil tax code — nearly four times the 20% accuracy-related penalty. Interest also accrues on the penalty itself from the return's original due date, so on older years the true cost runs well past 75%.

Can the IRS civil fraud penalty lead to jail time?

No — the civil fraud penalty is purely financial and cannot itself result in jail. But civil fraud and criminal tax evasion grow from the same facts, and a fraud proposal during an audit can signal that an examiner considered a criminal referral. If your case involves large unreported income, false documents, or multiple years, talk to an experienced tax professional before making any further statements to the IRS.

How does the IRS prove civil fraud?

The IRS must prove fraud by clear and convincing evidence — a higher standard than almost any other civil penalty, where the burden usually sits on you. Examiners build the case from 'badges of fraud': a pattern of understated income, concealed accounts, false records, cash dealings, or implausible explanations. One honest mistake, even a large one, doesn't meet that standard.

Is there a statute of limitations on the civil fraud penalty?

There is no statute of limitations on assessment when a return is fraudulent — under IRC §6501(c)(1), the IRS can audit and assess a fraudulent year forever. Once the penalty is actually assessed, though, the normal 10-year collection statute (CSED) applies to collecting it. That's why fraud proposals sometimes reach back much further than the usual three- or six-year audit window.

Does first-time penalty abatement apply to the civil fraud penalty?

No. First-time abatement covers only failure-to-file, failure-to-pay, and failure-to-deposit penalties, and the automatic AEP relief rolling out in summer 2026 follows the same lines. There is no administrative waiver for a fraud penalty — the only way to remove it is to defeat the fraud finding itself at Appeals, in Tax Court, or through a refund claim after paying.

My spouse committed the fraud on our joint return — do I owe the 75% penalty?

Not automatically. Under IRC §6663(c), the fraud penalty on a joint return applies to a spouse only if some part of the underpayment is due to that spouse's own fraud. You may still be jointly liable for the underlying tax, but innocent spouse relief under Form 8857 can address that separately. Raising §6663(c) early — in the audit or the Appeals protest — matters.

Can I settle or negotiate an IRS civil fraud penalty?

Yes, in two ways. Before assessment, the IRS Independent Office of Appeals can reduce or drop the penalty based on 'hazards of litigation' — how likely the IRS is to lose in court. After assessment, the penalty becomes part of your total balance, which may be resolvable through a payment plan or, if your finances qualify, an Offer in Compromise — though fraud-penalty accounts get close scrutiny.

What's the difference between civil fraud and negligence?

Intent. Negligence — carelessness, sloppy records, misunderstanding a rule — draws the 20% accuracy-related penalty, and you can defend it by showing reasonable cause. Civil fraud requires intentional wrongdoing: deliberately hiding income or faking deductions. The same $10,000 understatement costs $2,000 as negligence but $7,500 as fraud, and the two penalties can't be stacked on the same dollars.

Your next 24 hours

- Find the controlling date. On your exam report or notice, locate the line citing §6663 and the response deadline printed near the top of the letter — that date decides whether your forum is Appeals (30 days) or Tax Court (90 days).

- Gather the file. Pull the audited return, the complete exam report, and the records behind each adjusted item — bank statements, invoices, anything that shows where the numbers came from. If you're unrepresented and overwhelmed, the Taxpayer Advocate Service exists for exactly that; if you agree with the tax and just need to pay it, IRS.gov/payments handles that part.

- Get the proposal reviewed free — before the window closes. Send us the report and an experienced tax professional will tell you whether the fraud case is actually provable, what a realistic outcome looks like, and what to file first: the 2-minute form or (888) 825-7779.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.