IRS Penalties

Underpayment Penalty for Estimated Taxes: How It Works and How to Cut It (2026)

The short answer: the underpayment penalty for estimated taxes isn't a flat fine — it's daily interest, at the federal short-term rate plus 3 points, charged on each quarterly installment you shorted from its due date until you pay. You owe nothing if you paid in 90% of this year's tax, 100% of last year's, or owe under $1,000.

You made payroll every two weeks, kept your vendors current, and paid the IRS exactly what your return said you owed — and there's still a penalty at the bottom of the 1040 for not paying it during the year. That's the underpayment penalty for estimated taxes, and it's the most misunderstood — and most fixable — charge in the tax code. This page shows you exactly how it's computed, the three safe harbors that zero it out, and the one payroll trick that makes it nearly optional for business owners.

Whether the number came from your own software's Form 2210 or from a CP30 notice the IRS mailed you, the image below shows you exactly what this penalty looks like on paper and where to find the figures that control your options.

⏱ Your real clock: there's no response deadline printed on this penalty — but each underpaid installment keeps accruing penalty every day until you pay it, and the meter only shuts off for good at the April 15 filing deadline. After that, any unpaid balance switches to the failure-to-pay penalty plus daily-compounding interest.

Why you're being charged an underpayment penalty on estimated taxes

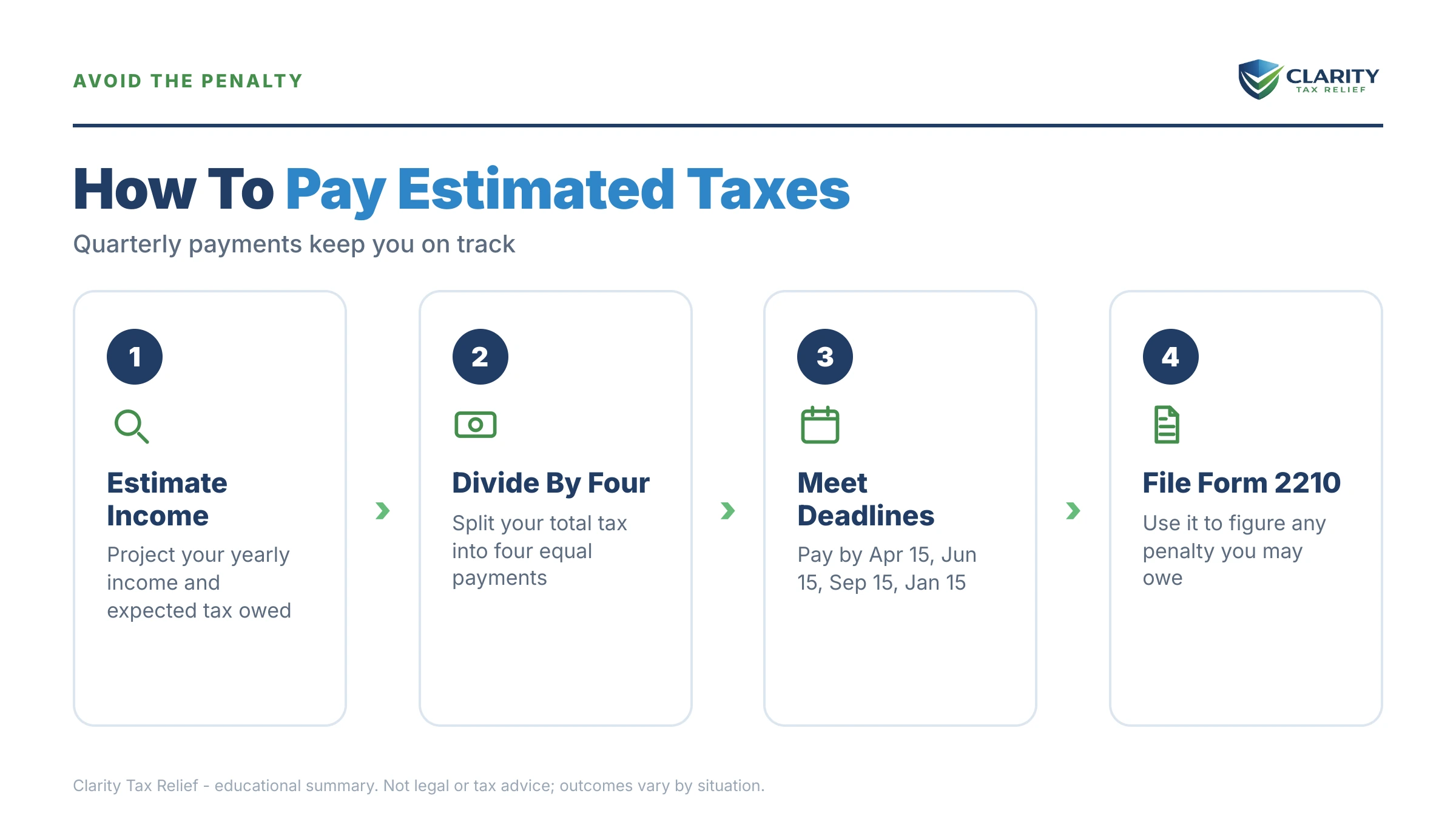

The IRS charges the underpayment penalty under IRC §6654 when you don't pay enough tax during the year — through withholding or quarterly estimated payments — even if you pay every dollar by April 15. The tax system is pay-as-you-go: the law expects roughly a quarter of your year's tax by each installment date (April 15, June 15, September 15, and January 15), and it charges you for the time the government waited on money that was due earlier.

That design produces two surprises that catch business owners constantly. First, you can owe this penalty even if you're getting a refund — if your payments arrived late in the year, the early quarters were still underpaid and the meter ran on each one. Second, paying in full at filing doesn't erase it; it only stops it from growing further.

W-2 employees rarely see this penalty because withholding covers them automatically. It lands on people whose income arrives without withholding: S-corp distributions, Schedule C profit, K-1 income, interest, and capital gains. If quarterlies are new territory for you, our primer on how quarterly estimated taxes work covers the system itself; this page covers the penalty for missing it.

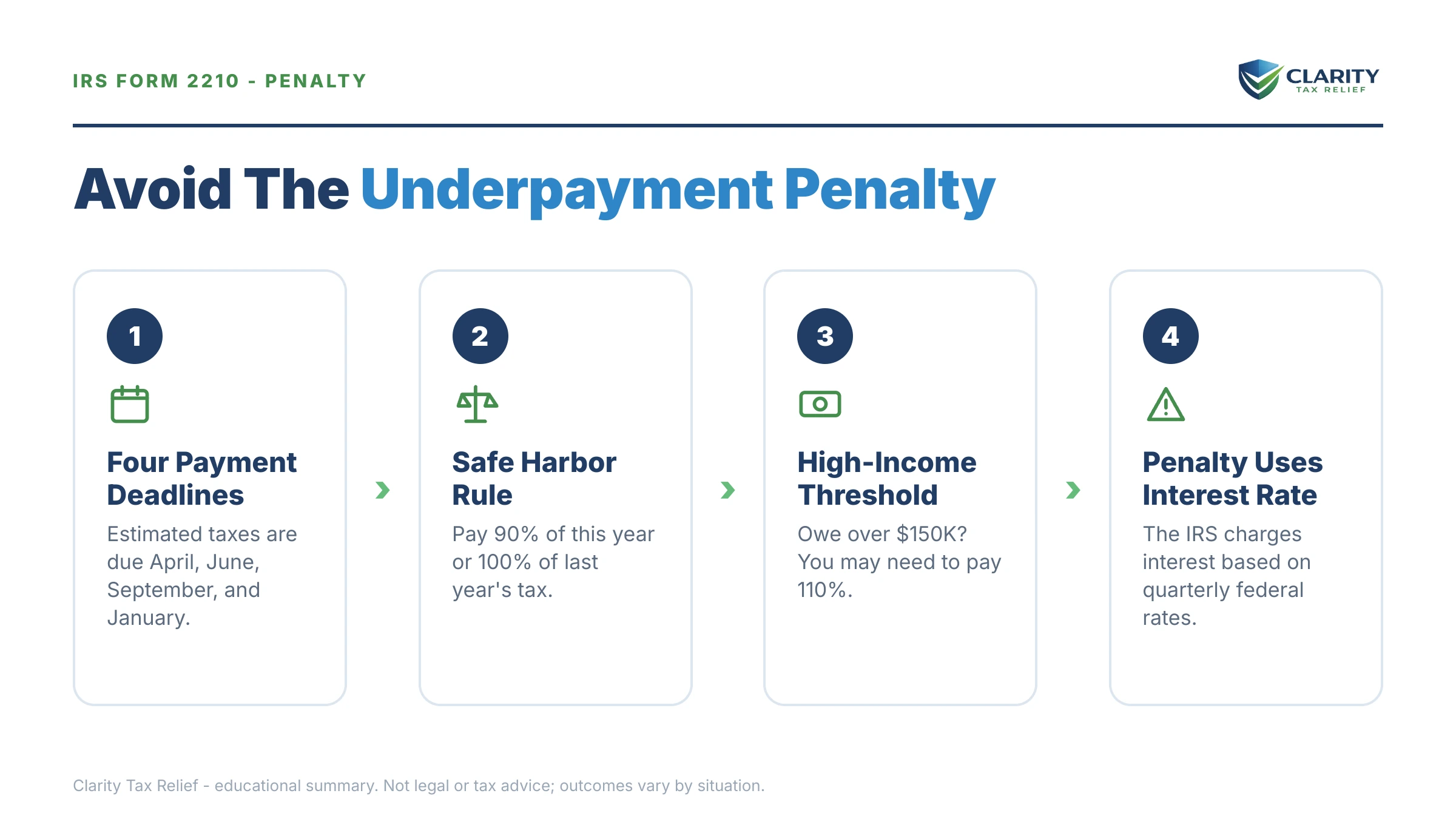

The safe harbors that decide whether you owe it at all

You owe zero underpayment penalty if your withholding plus timely quarterly payments reached 90% of this year's tax or 100% of last year's total tax — 110% if your prior-year AGI topped $150,000. Before you accept any penalty figure, test yourself against every row of this table, because meeting any single one makes the penalty disappear:

| Safe harbor | What you must have paid in during the year | Who it usually fits |

|---|---|---|

| 90% of current-year tax | At least 90% of this year's total tax, in timely installments | Income dropped from last year — pay to the lower number |

| 100% of prior-year tax | Last year's total tax, in four equal timely installments | Income rose — lock the penalty out with a known number |

| 110% of prior-year tax | 110% of last year's tax if prior-year AGI exceeded $150,000 ($75,000 married filing separately) | Higher earners, including most profitable owners |

| Under-$1,000 rule | Balance due after withholding and refundable credits is below $1,000 | Mostly-W-2 filers with a small side balance |

| Farmers & fishermen | 66⅔% of current-year tax, with a single January installment allowed | Two-thirds of gross income from farming or fishing |

Two traps inside the fine print. The married-filing-separately threshold for the 110% rule is $75,000, not half of whatever you assume. And the under-$1,000 test counts withholding but not estimated payments — so a self-employed filer with no withholding can trip the penalty on a surprisingly small balance.

How the estimated-tax underpayment penalty is calculated in 2026

The penalty accrues daily at the IRS underpayment rate — the federal short-term rate plus 3 percentage points, reset each calendar quarter. Form 2210 splits your year into four required installments, measures the shortfall in each, and charges the rate on each shortfall for the exact number of days it stayed unpaid. Later payments are applied to the oldest underpayment first.

Because the rate resets quarterly, the same shortfall costs different amounts in different years — the current figure and recent history are in our estimated tax penalty rate 2026 guide, and you can estimate your own number with our Penalty & Interest Calculator. Three properties of the math matter more than the rate itself:

- It's per-quarter, not per-year. An April underpayment can run the meter for a full 12 months; a January one runs it for only three.

- Paying early cuts it. Every day sooner you pay a shorted installment, the penalty on it stops — you don't have to wait for the return.

- It caps at April 15. The §6654 penalty can't grow past the original filing deadline. The unpaid balance underneath it can, through other charges.

Worked example: a $7,400 shortfall, quarter by quarter

Say you run a small business with payroll, and between salary withholding and sporadic estimates you paid in $7,400 less than your safe-harbor number required — $1,850 short on each of the four installments. Using an illustrative 7% annual rate held constant all year (the real rate resets quarterly), here's what each quarter's meter reads by April 15:

- Q1 shortfall ($1,850, unpaid ~365 days): $1,850 × 7% ≈ $130

- Q2 shortfall ($1,850, ~304 days): $1,850 × 7% × 304/365 ≈ $108

- Q3 shortfall ($1,850, ~212 days): $1,850 × 7% × 212/365 ≈ $75

- Q4 shortfall ($1,850, ~90 days): $1,850 × 7% × 90/365 ≈ $32

Total penalty: roughly $345 on a $7,400 shortfall — about 4.7%. Painful, but modest. Now the version that stings: if that same owner had run themselves a December bonus through payroll with an extra $7,400 withheld, the penalty would have been approximately zero — because withholding is deemed paid evenly across all four quarters, no matter when it actually came out. Same dollars, same year, $345 difference. More shortfall scenarios and full-year math live in our companion guide on the didn't pay estimated taxes penalty.

What happens if you ignore it

The underpayment penalty stops growing at the April filing deadline — but the balance it's attached to does not, and an unpaid balance enters the IRS's automated collection sequence. The stages run in this order:

- Assessment. The penalty posts to your account — either from your own Form 2210 or via a CP30 notice when the IRS computes it for you and reduces your refund or bills the difference.

- CP14 bill. If a balance remains, the first bill arrives with roughly 21 days to pay before the sequence continues. The failure-to-pay penalty (0.5% per month) and daily interest are now running on the unpaid tax.

- CP501 / CP503 reminders. Still just bills — but each cycle adds another month of penalty and interest to the total.

- CP504 — intent to levy. The IRS can now take your state tax refund, and a federal tax lien becomes a live risk.

- LT11 / Letter 1058 — final notice. A 30-day clock starts on your Collection Due Process rights; after it, wage and bank levies are on the table.

In 2026, with the IRS workforce down roughly 27%, this ladder is climbed by software, not people — the notices keep printing whether or not a human ever reviews your account. A few-hundred-dollar penalty is never worth that ride; the unpaid tax underneath it is what fuels it.

Staring at a penalty you didn't expect?

Send us your Form 2210 or CP30. An experienced tax professional will re-test every safe harbor, check whether annualizing or a waiver erases the charge, and map the cheapest way to close out the balance — free, confidential, while penalties and interest on any unpaid tax are still accruing daily.

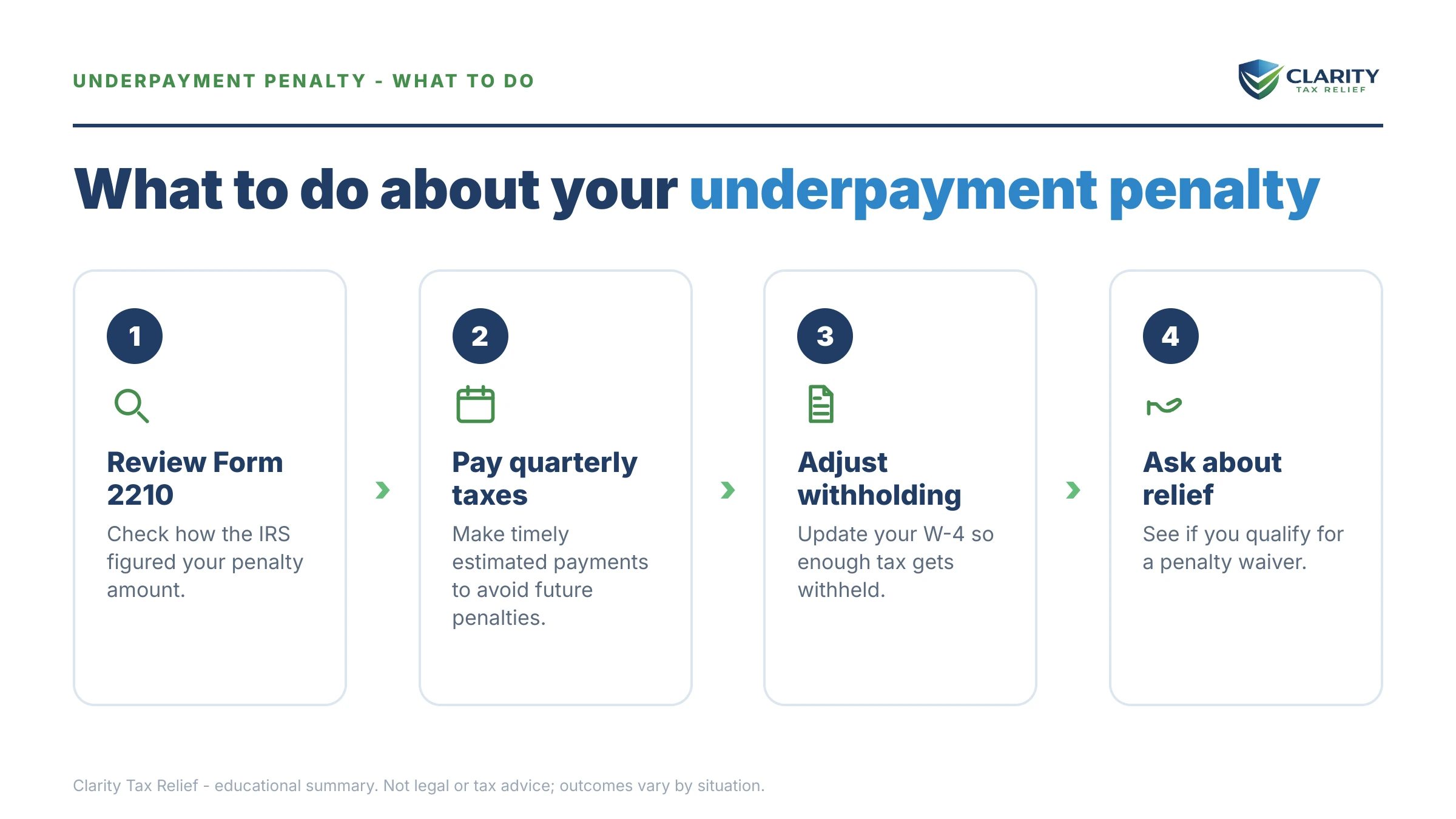

Your options to reduce or remove the penalty

Five moves can shrink or erase an estimated-tax underpayment penalty, and every one of them is free — the only cost is time and paperwork. One thing that does not work: first-time penalty abatement. FTA (and the Automatic Exemption from Penalty replacing it in summer 2026) covers failure-to-file and failure-to-pay penalties — the §6654 penalty has never been on that list. Its relief runs through Form 2210 instead:

| Option | What it can do | Cost & timeline |

|---|---|---|

| Annualized income method (Form 2210 Schedule AI) | Recomputes each installment based on when you actually earned the money — often erases the penalty for seasonal or back-loaded income | Free; 1–2 hours of math, filed with your return or an amended one |

| Form 2210 Part II waiver | Waives the penalty for casualty, disaster, or other unusual circumstance — or retirement after 62 / disability with reasonable cause | Free; short written statement, decided when the return processes |

| Recheck the withholding split | Withholding is deemed paid evenly by default, but you can elect actual dates if that's better — and confirm all W-2 boxes were counted | Free; minutes with your W-2s and Form 2210 |

| Pay the shortfall now | Stops the daily meter on each underpaid installment before April 15 — the earlier the payment, the smaller the final penalty | Free to do; savings depend on how many days you cut off |

| Respond to the CP30 | If the IRS computed the penalty without an exception you qualify for, a reply with a corrected Form 2210 gets it recomputed | Free; written response, typically resolved in one processing cycle |

For uneven income, Schedule AI is the workhorse. A landscaping company, a retailer with a fourth-quarter surge, or a consultant who landed one big contract in October is being penalized under the default method for not pre-paying tax on money that didn't exist yet. Annualizing matches each installment to actual year-to-date earnings — and for genuinely back-loaded income it routinely cuts the penalty to a fraction of the default figure. Full walkthrough of every exception in our estimated tax penalty waiver guide.

How to respond, step by step

- Verify the math. Pull your Form 2210 (or the CP30 the IRS sent) and check the penalty against your actual payment dates and amounts — IRS records occasionally miss a payment or post it to the wrong year.

- Re-test every safe harbor. Confirm last year's total tax, your total withholding, and the $1,000 rule. If any safe harbor is met, the penalty is zero — respond with the corrected Form 2210.

- Annualize if your income was uneven. If most of your profit landed late in the year, complete Form 2210 Schedule AI to match each installment to when you actually earned the money.

- Request a waiver if one fits. Casualty, disaster, retirement after age 62, or disability with reasonable cause — check the waiver box in Form 2210 Part II and attach a short statement.

- Pay the underlying balance or set up a plan. The penalty caps at the filing deadline, but the failure-to-pay penalty and daily interest on the unpaid tax do not.

- Fix the current year today. Raise your W-2 withholding or start this quarter's estimated payment now so next April doesn't repeat this one.

The payroll advantage: why business owners have the best fix in the code

Withholding is treated as paid evenly across all four quarters no matter when it actually comes out of your paycheck — and if you run payroll, you control your own withholding. That single rule turns your December payroll run into a time machine: extra tax withheld from a year-end paycheck or bonus retroactively cures underpayments from April, June, and September. Estimated payments can never do that; they count only on the day they're paid.

The practical playbook for an owner on payroll: each fall, project your full-year tax, compare it to your safe-harbor number, and close any gap through withholding on your remaining paychecks rather than a catch-up estimate. This year's installment dates are in our quarterly estimated tax deadlines 2026 calendar.

One hard warning that belongs on this page and nowhere else: never cover personal estimates by delaying your payroll tax deposits. That trades a mild interest-style penalty for the failure-to-deposit cascade and potential personal trust-fund liability — a categorically worse problem. If deposits have already slipped, start with our guides on a missed payroll tax deposit and 941 penalty abatement.

What the penalty looks like on your IRS transcript

On an IRS account transcript, the estimated-tax penalty posts as transaction code 170 or 176. If you're checking your account to confirm what was assessed — or whether a correction went through — these are the codes to read:

| Code | What it means | What to do |

|---|---|---|

| 170 / 176 | Estimated-tax penalty assessed (170 manually, 176 by computer) | Match the amount to your Form 2210 or CP30; if a safe harbor or exception applies, respond with a corrected 2210 |

| 196 | Interest charged on the unpaid balance | Grows daily until the balance is paid — see our code 196 transcript guide |

| 276 | Failure-to-pay penalty — a separate charge on tax unpaid after April 15 | Different penalty, different relief rules — see code 276 transcript |

| 971 | Notice issued — often the CP30 or a collection notice | Watch the mail and match the date to the notice you received |

A negative (credit) entry against code 170/176 after you respond means the recomputation worked. State penalties never appear on an IRS transcript — if you also underpaid California, the FTB estimated tax penalty is a separate charge under separate rules, tracked only in your FTB account.

When you can handle this yourself — and when help changes the outcome

Most people can resolve a standalone underpayment penalty themselves with Form 2210 and an hour of quarter-by-quarter math. If the penalty is a few hundred dollars, your income was steady, and no safe harbor applies, the honest answer is often to pay it, adjust withholding, and move on — hiring anyone to fight a $345 charge is bad economics.

Experienced help earns its cost in specific situations: multiple years of penalties stacked on unpaid balances that have already drawn collection notices; a business year messy enough that Schedule AI requires reconstructing month-by-month income; a disaster or disability waiver that needs a persuasive statement; or an underpayment penalty that's the visible tip of a larger debt — where sequencing the fix (returns first, then penalties, then the balance) changes the total you pay. For how this penalty compares to everything else the IRS charges, the full picture with math is in how big do IRS penalties get.

Terms on your Form 2210 or CP30, decoded

- Safe harbor — a payment threshold (90% current-year, 100%/110% prior-year) that, once met, makes the underpayment penalty zero regardless of what you still owe at filing.

- Required annual payment — the smaller of the 90% and 100%/110% figures; Form 2210 divides it into four installments.

- Underpayment rate — the federal short-term rate plus 3 percentage points, reset quarterly; the "interest rate" behind this penalty.

- Annualized income installment method — the Schedule AI election that sizes each installment to income actually earned by that date instead of a flat one-quarter split.

- CP30 — the notice the IRS sends when it computes this penalty for you and reduces your refund or bills the difference.

- Deemed-even withholding — the default rule treating all W-2 withholding as paid in four equal quarterly pieces, whenever it actually came out.

Underpayment penalty questions, answered

How is the underpayment penalty for estimated taxes calculated?

It's calculated like daily interest, not a flat fine. The IRS applies its quarterly underpayment rate — the federal short-term rate plus 3 percentage points — to each installment you missed or shorted, for every day from that installment's due date until you pay it or until the April filing deadline, whichever comes first. Form 2210 walks through the math quarter by quarter.

Can the underpayment penalty for estimated taxes be waived?

Yes, but only through the waivers built into Form 2210 — first-time penalty abatement does not apply to this penalty. The IRS can waive it if you underpaid because of a casualty, disaster, or other unusual circumstance, or if you retired after turning 62 or became disabled and had reasonable cause. You request the waiver in Part II of Form 2210 with a short written statement.

What is the safe harbor for estimated taxes?

Pay in at least 90% of this year's tax or 100% of last year's total tax — 110% if your prior-year adjusted gross income was over $150,000 ($75,000 married filing separately) — through withholding and timely quarterly payments, and you owe no underpayment penalty. You're also exempt if your balance after withholding is under $1,000. Farmers and fishermen have a lower 66⅔% threshold.

Do I owe an underpayment penalty if I owe less than $1,000?

No. If your total tax minus your withholding and refundable credits is under $1,000, the underpayment penalty doesn't apply at all — no Form 2210 needed. Watch the fine print, though: the $1,000 test is measured after withholding but before estimated payments, so a self-employed person with no withholding can still owe the penalty on a fairly small balance.

Does increasing withholding at the end of the year avoid the underpayment penalty?

Usually, yes — and it's the most powerful fix available to anyone on a payroll. Tax withheld from wages is treated as paid evenly across all four quarters by default, even if it all came out of a December paycheck. A business owner who runs their own payroll can raise withholding late in the year and retroactively cure earlier quarters. Estimated payments never get that treatment — they count only when actually paid.

What is a CP30 notice?

A CP30 is the notice the IRS sends when it calculates the estimated-tax penalty for you and either reduces your refund or bills you for it. It shows the tax year, the penalty amount, and how it was applied. If a Form 2210 exception the IRS didn't apply fits your facts — like the annualized income method or a waiver — you can respond and have the penalty recomputed.

Does the underpayment penalty keep growing after I file?

No — this specific penalty stops accruing at the original April filing deadline for each tax year. But if you leave the balance itself unpaid, two other charges take over: the failure-to-pay penalty at 0.5% per month and interest that compounds daily. That's why paying the underlying tax matters far more than the penalty line itself.

Is the California FTB estimated tax penalty the same as the IRS penalty?

No. California's Franchise Tax Board runs its own version with its own rates, its own safe-harbor limits, and a weighted installment schedule that front-loads payments instead of splitting them into four equal quarters. If you underpaid both, you owe two separate penalties to two separate agencies, and fixing one does nothing for the other.

Your next 24 hours

- Find your number. Pull the penalty line from your Form 2210 or the amount box on your CP30, and note the tax year it covers — everything else depends on those two facts.

- Gather three documents: last year's return (for the prior-year tax figure), this year's payment confirmations and W-2 withholding totals, and — if your income was uneven — anything showing when the money actually arrived.

- Get it reviewed free. Use the 2-minute form or call (888) 825-7779. We'll re-test the safe harbors, check Schedule AI and the waivers, and map the cheapest close-out — while interest on any unpaid balance is still accruing every day.

Primary sources: the IRS overview of estimated taxes for individuals and small businesses, the official Form 2210 page, and the IRS explainer Understanding your CP30 notice.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.