Penalty Relief

Business Penalty Abatement: 941, 1120 & 1065 Penalty Relief (2025)

The short answer: business penalty abatement is the IRS process for removing late-filing and late-payment penalties on business returns — payroll (Form 941), corporate (Form 1120), and partnership (Form 1065). There are two main paths: first-time abatement for a clean prior record, or reasonable-cause relief when events outside your control caused the delay.

Got a business penalty notice?

Send us a photo of it. An experienced tax professional will tell you whether your business qualifies for first-time or reasonable-cause abatement — and which payroll, corporate, or partnership penalties can come off. Free, confidential, no pressure.

⏱ Timing matters: there's no single deadline to ask, but penalties grow until the balance is paid. If you already paid a penalty, you generally must request a refund within 3 years of filing the return or 2 years of paying — whichever is later. The sooner you act, the less the late-payment penalty (0.5% per month) adds up.

Why your business got hit with a penalty

If you're reading this, the IRS sent a notice showing a penalty on a business return. Business penalty abatement exists because the system that adds these penalties is automated — it doesn't know your bookkeeper quit in March or that a flood destroyed your records. The most common business penalties are:

- Failure to file — filing a 941, 1120, or 1065 late. For partnerships and S corporations, this penalty is charged per partner or shareholder, per month, so it adds up fast even when no tax is due.

- Failure to pay — 0.5% of the unpaid tax per month, up to 25%.

- Failure to deposit — for payroll taxes that weren't deposited on the right schedule. The rate climbs from 2% to as high as 15% depending on how late.

A penalty notice is not an audit and not a criminal matter. It's a bill — and a meaningful share of it can often be removed if your business qualifies. The IRS explains the relief options at Penalty relief on IRS.gov.

What happens if you ignore a business penalty

Penalties don't sit still. With payroll (941) debt in particular, ignoring the notices is the most expensive mistake a business owner can make. Here's the typical escalation:

- Balance due notice — the first bill showing tax plus penalty and interest. No enforcement yet.

- Reminder notices — the balance grows monthly; the late-payment penalty keeps stacking.

- Notice of Intent to Levy — the IRS can move to seize business bank accounts and receivables.

- Trust Fund Recovery Penalty — for unpaid payroll taxes, the IRS can pursue owners, officers, and other "responsible persons" personally, piercing the business shield. Learn how this works in our guide to the Trust Fund Recovery Penalty.

The lesson: the longer a 941 balance sits, the closer it gets to becoming a personal debt you can't walk away from by closing the company.

Path 1: First-time penalty abatement for businesses

First-time abatement (FTA) is the simplest relief, and yes — it applies to businesses, not just individuals. The IRS grants it based on a clean compliance history, not a sad story. Your business generally qualifies if all three are true:

- Clean prior record — no penalties in the three tax years before the year you're asking about (a small estimated-tax penalty doesn't disqualify you).

- Filing compliant — all currently required returns are filed, or you have a valid extension.

- Paying compliant — any tax owed is paid, or you've set up an installment agreement that's in good standing.

FTA covers failure-to-file, failure-to-pay, and (for payroll) failure-to-deposit penalties. The big advantage: you don't have to prove a reason. If you qualify, you ask, and the IRS removes it. Our full first-time penalty abatement guide walks through the exact wording and the order to do things in.

Path 2: Reasonable-cause relief

If your business doesn't qualify for FTA — say you had a penalty two years ago — you can still ask for relief based on reasonable cause. This means circumstances beyond your control kept you from meeting your obligations even though you used ordinary business care. Examples the IRS accepts:

- Serious illness, injury, or death of the owner or the person responsible for the taxes

- A fire, flood, hurricane, or other disaster that destroyed records

- Inability to get records you needed despite reasonable efforts

- Reliance on incorrect written advice from a tax professional or the IRS

What usually doesn't work: "we didn't have the cash," "we forgot the deadline," or "our accountant dropped the ball" (you're responsible for filing, even when you delegate). Reasonable cause is fact-specific and documentation wins — dates, records, and a clear timeline. See our deeper walkthrough on reasonable-cause penalty abatement.

A worked example: a late 1065 partnership return

Say a three-partner LLC files its Form 1065 partnership return four months late, with no tax due. The late-filing penalty is charged per partner, per month. At roughly $245 per partner per month (the figure adjusts for inflation each year), that's:

3 partners × 4 months × ~$245 = roughly $2,940 in penalties — on a return that owed zero tax.

If the partnership has a clean three-year history, first-time abatement could remove that penalty entirely. If it had a small penalty two years ago, reasonable cause — say the managing partner was hospitalized during filing season — might still get it removed with the right documentation. Either way, the penalty is worth fighting because none of it reflects actual tax owed.

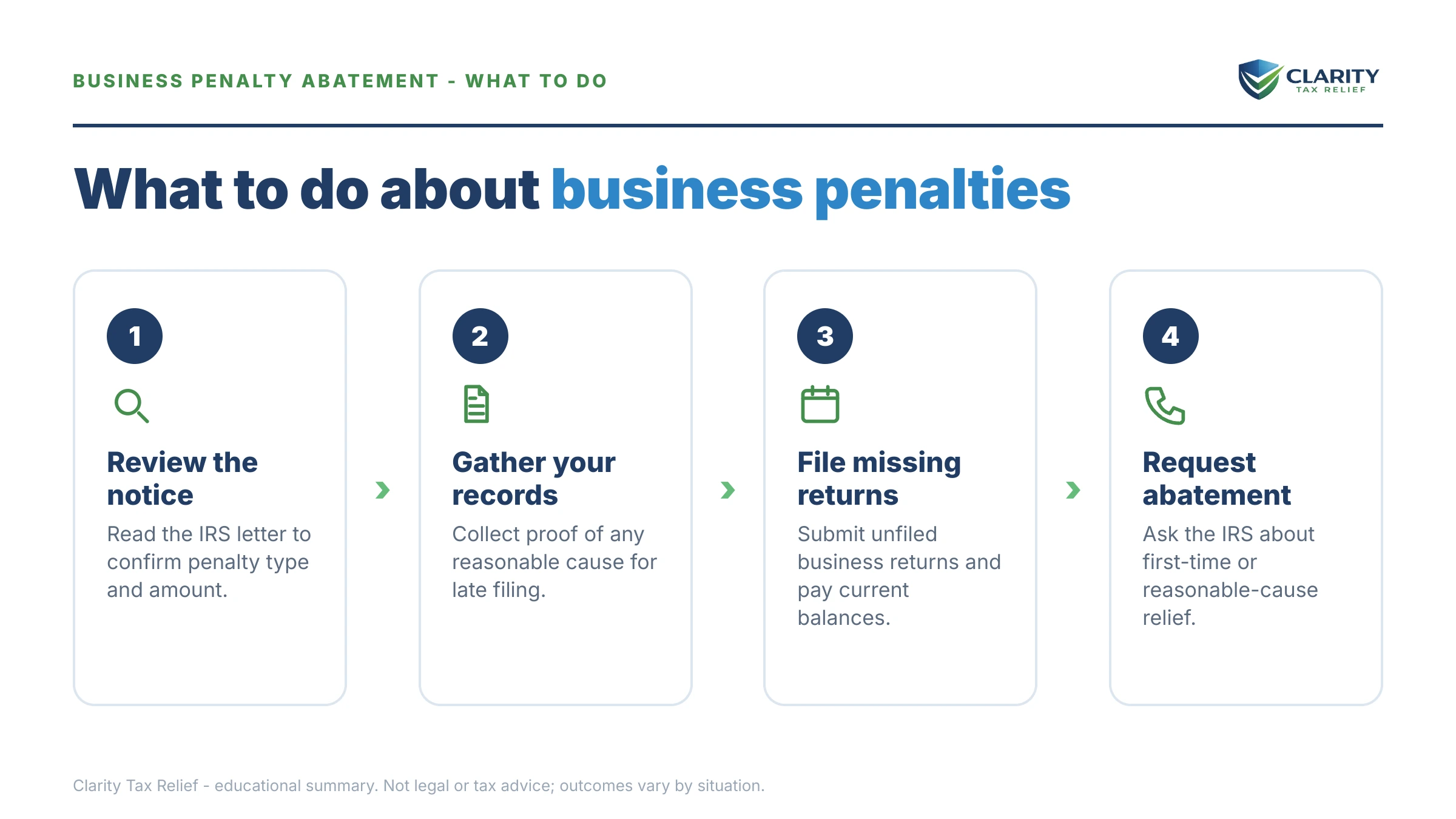

How to request business penalty abatement, step by step

- Pull the notice and your transcripts. Identify the exact penalty type, tax year, and amount. Confirm which return it ties to (941, 1120, 1065, or another).

- Check your three-year history. If the prior three years are clean, first-time abatement is usually the fastest route.

- Get current on filing and paying. File any missing returns and pay the tax, or set up an installment agreement. FTA generally requires this; with payroll debt, fixing the balance also limits personal exposure.

- Choose your path. FTA for a clean record; reasonable cause when events outside your control caused the delay. You can request reasonable cause as a backup if FTA is denied.

- Make the request. Call the number on the notice, write a letter explaining the facts with documentation, or file Form 843, Claim for Refund and Request for Abatement — especially if you already paid the penalty. Our Form 843 walkthrough shows exactly how to fill it out.

- Keep records of everything. Note the date, the agent's name and ID, and copies of all correspondence. If a request is denied, you have the right to appeal.

One caution about the marketing you'll see: anyone promising to wipe out your penalties or settle for "pennies on the dollar" before reviewing your business's compliance history is selling you something. Real relief depends on your facts.

Business penalty abatement, answered

Can a business get first-time penalty abatement?

Yes. First-time abatement applies to businesses too. Your company generally qualifies if it had no penalties in the prior three years, all required returns are filed (or on a valid extension), and any tax due is paid or on an arrangement. It covers failure-to-file and failure-to-pay penalties, including on Forms 941, 1120, and 1065.

Does penalty abatement remove the interest too?

Not directly. The IRS charges interest by law and will not waive it just because you had reasonable cause. But when a penalty is removed, the interest that was charged on that penalty is removed with it. Interest on the underlying tax stays unless the tax itself is reduced.

Can I abate the penalty on payroll taxes I haven't paid yet?

Reasonable-cause relief can apply even with a balance owed, but first-time abatement usually requires that the tax be paid or covered by an installment agreement. With 941 payroll debt, the bigger risk is the Trust Fund Recovery Penalty against owners and officers personally — so address the balance and the penalty together.

How do I request business penalty abatement?

You can call the number on your IRS notice to request first-time abatement, write a letter explaining reasonable cause with documentation, or file Form 843, Claim for Refund and Request for Abatement, especially if you already paid the penalty. Keep copies of everything and note the date and name of any agent you speak with.

What counts as reasonable cause for a business?

Reasonable cause means events outside your control kept you from filing or paying on time despite ordinary business care — serious illness or death of the person handling taxes, a natural disaster, fire or theft of records, or reliance on incorrect written advice. Simply not having the money, or not knowing the deadline, usually does not qualify.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.