IRS Penalties

Failure to File Penalty vs Failure to Pay: The 10× Difference (2026)

The short answer: in the failure to file penalty vs failure to pay comparison, filing late is 10 times more expensive. Failure to file costs 5% of your unpaid tax per month (capped at 25%); failure to pay costs 0.5% per month (same cap). Always file on time — even if you can't pay a dime.

Maybe you found this the way a lot of people do: pulling paperwork for a mortgage refinance and realizing there's a tax year you never filed, sitting on a balance you never paid. Two separate penalties are now running on the same debt — and they are wildly unequal. The good news: one of them can be stopped today, and both can often be removed entirely.

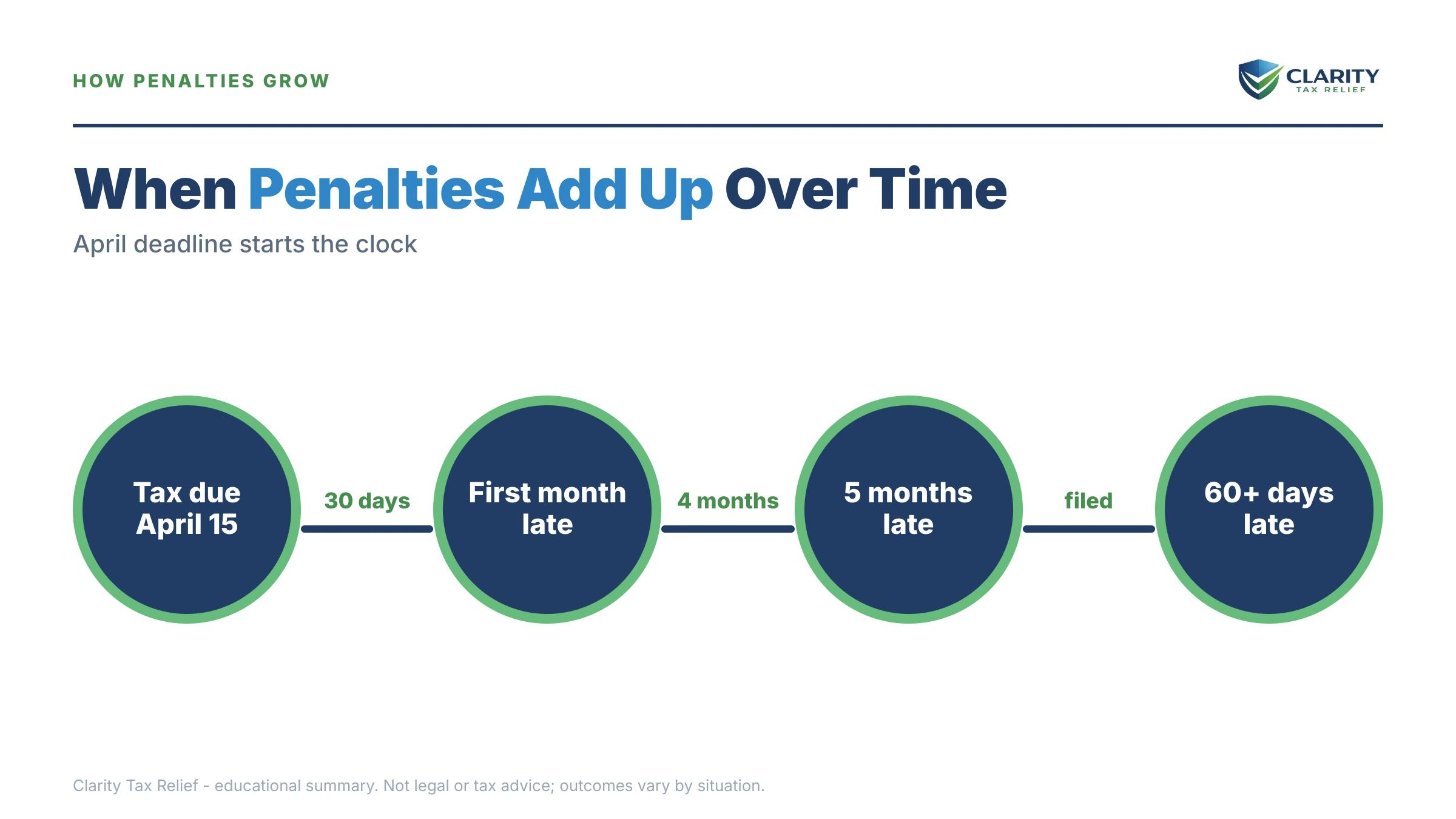

⏱ The real clock: the failure-to-file penalty reaches its full 25% cap in just 5 months — 5% of the unpaid tax for every month (or partial month) the return stays unfiled. The 0.5% failure-to-pay penalty and daily-compounding interest keep running long after that, until the balance is resolved.

Failure to File Penalty vs Failure to Pay: The Key Differences

The failure-to-file penalty runs at 5% of unpaid tax per month, exactly 10 times the 0.5% failure-to-pay rate. Both come from the same law — Internal Revenue Code §6651 — both are calculated on the unpaid tax (not your total tax), and both cap at 25%. The difference is speed: failure to file maxes out in 5 months, while failure to pay takes 50 months to hit the same ceiling.

The image below shows how the two penalties compare at a glance and where each one stops growing.

| Feature | Failure to file | Failure to pay |

|---|---|---|

| Monthly rate | 5% of unpaid tax (per month or partial month) | 0.5% of unpaid tax (per month or partial month) |

| Maximum | 25% — reached in 5 months | 25% — reached in 50 months |

| Trigger | Return not filed by the due date (including extensions) | Tax not paid by the original due date — extensions don't help |

| Rate can change? | No, but a flat minimum applies once you're 60+ days late | Yes: drops to 0.25%/month on a payment plan; rises to 1%/month after an ignored intent-to-levy notice |

| How to stop it | File the return — the clock stops that day | Pay the balance, or reduce the rate with an installment agreement |

Three details trip people up. First, when both penalties apply in the same month, they don't fully stack: the failure-to-file penalty is reduced by the failure-to-pay amount, so the combined charge is 5% per month (4.5% + 0.5%), and the failure-to-file portion tops out at 22.5% instead of 25%. The combined lifetime maximum is 47.5% of the unpaid tax — before interest.

Second, if your return is more than 60 days late with a balance due, a flat minimum failure-to-file penalty kicks in — an inflation-adjusted amount in the several-hundred-dollar range, or 100% of the unpaid tax if that's smaller. Even a tiny balance gets stung.

Third, the entire comparison collapses into one rule: file even if you can't pay. Filing on time with zero payment attached limits you to the small penalty. Not filing invites the big one on top of it. This is the most expensive misunderstanding in consumer tax debt, and it's the reason the IRS's own guidance repeats it. (For how these penalties fit into the wider penalty landscape, see how much are IRS penalties on back taxes.)

Why the IRS Charged You One — or Both — of These Penalties

Which penalty you're facing depends entirely on two dates: when you filed and when you paid. There are four common patterns:

- Filed on time, paid late or not at all: failure-to-pay only — 0.5% per month. The mildest version of this problem.

- Filed an extension, paid nothing in April: no failure-to-file penalty if you filed by October 15, but failure-to-pay ran from the original April deadline. A Form 4868 extension moves the filing deadline, never the payment deadline.

- Never filed, never paid: both penalties, combined at 5% per month for the first 5 months, then 0.5% ongoing.

- The IRS filed for you: if you ignored the non-filing long enough, the IRS may have prepared a substitute return with no deductions, then assessed tax plus both penalties on the inflated number. That's a separate fight — see the IRS filed a substitute return for me.

Two lookalikes to rule out. If you're self-employed and the penalty is for missing quarterly payments during the year, that's a different charge with different math — covered in didn't pay estimated taxes penalty. And if the IRS says you understated tax on a return you filed, that's the 20% accuracy-related penalty, not either of these.

You can confirm exactly what was charged without waiting for mail: your IRS account transcript shows a late-filing penalty line and code 276 for the failure-to-pay penalty, each with a dollar amount and date. The CP14 bill, when it arrives, breaks the balance into tax, penalties, and interest.

The Worked Math: What $19,700 Unpaid Actually Costs

On a $19,700 balance, filing on time instead of filing late saves $4,432.50 in penalties — every time, at every point on the timeline. Here's the arithmetic, clearly hypothetical:

Say you owe $19,700 and never filed. For the first 5 months, the combined penalty is 5% per month: 4.5% failure-to-file ($886.50) plus 0.5% failure-to-pay ($98.50) — $985 per month. By month 5, the failure-to-file portion maxes out at $4,432.50 and the failure-to-pay portion sits at $492.50: $4,925 in penalties in five months. After that, only the $98.50 monthly failure-to-pay charge keeps running.

Now say you'd filed on time and simply couldn't pay. Same $19,700, but only the 0.5% penalty applies: $98.50 per month, $1,182 after a full year. The person who filed is $4,432.50 ahead of the person who didn't — with the identical debt.

| Time late | Never filed, never paid | Filed on time, unpaid | Filing saves |

|---|---|---|---|

| 1 month | $985.00 | $98.50 | $886.50 |

| 3 months | $2,955.00 | $295.50 | $2,659.50 |

| 5 months | $4,925.00 | $492.50 | $4,432.50 |

| 12 months | $5,614.50 | $1,182.00 | $4,432.50 |

| 24 months | $6,796.50 | $2,364.00 | $4,432.50 |

| Penalty maximum | $9,357.50 (47.5%) | $4,925.00 (25%) | $4,432.50 |

Interest rides on top of everything in that table — charged on the tax and the penalties, compounding daily, at a rate the IRS resets each quarter (current figures in IRS interest rates 2026). You can estimate your own combined penalty-and-interest total with our Penalty & Interest Calculator.

If you're planning a refinance, there's a second cost hiding here. A growing, unresolved IRS balance can eventually lead to a federal tax lien — no longer on credit reports, but very much in the public records your lender's title search will pull. Resolving the balance (or at least getting it into an agreement) before underwriting is dramatically easier than dealing with a lien mid-application; see can I refinance with an IRS lien.

What Happens If You Ignore Both Penalties

Unpaid penalties don't sit still — they feed an automated collection sequence that escalates in a fixed order. Here's the progression:

- Months 1–5: the expensive window. Combined penalties accrue at 5% per month until the failure-to-file portion caps at 22.5%. Nothing you do later recovers this period — only filing stops it.

- Substitute for Return (non-filers). If you never file, the IRS eventually files for you — single or married-filing-separately status, no deductions, no credits — and assesses tax plus both penalties on that inflated figure.

- CP14: the first bill. Once a balance is assessed, the IRS mails a bill showing tax, penalties, and interest, with roughly three weeks to respond before the sequence continues.

- CP501 / CP503: reminders. Still just bills, but the 0.5% penalty and daily interest are compounding through every one of them.

- CP504: intent to levy. The IRS can seize your state tax refund, and — critically for these penalties — ignoring an intent-to-levy notice for more than 10 days pushes the failure-to-pay rate from 0.5% to 1% per month. The one penalty that was small stops being small.

- LT11 / Letter 1058: final notice. A 30-day clock starts, with Collection Due Process appeal rights. After it runs, the IRS can levy bank accounts and garnish wages, and a federal tax lien becomes likely — the public-record filing that complicates any refinance or sale.

One more thing 2026 adds: the IRS workforce shrank roughly 27% in 2025, so reaching a human is harder than ever — but every stage above is generated by automated systems that never stopped running. Silence from the IRS is not the same as the clock being paused.

Penalties stacking on a balance right now?

Whether you're staring at an unfiled year or a failure-to-pay penalty that keeps growing, an experienced tax professional can tell you — free — which penalties you can stop today and which ones can likely be removed. Filing stops the 5% monthly charge the day it happens.

How to Reduce or Remove Failure-to-File and Failure-to-Pay Penalties

Both penalties are among the most commonly abated charges the IRS assesses — but relief is never automatic today, and each path has its own eligibility test:

| Option | Who may qualify | Cost & effect |

|---|---|---|

| First-time penalty abatement | No penalties in the prior 3 tax years; all required returns filed | Free; removes failure-to-file and failure-to-pay penalties for one year, by phone or letter |

| Automatic Exemption from Penalty (AEP) | Similar clean-history test — applied automatically starting summer 2026, no request needed | Free; the IRS's replacement for first-time abatement |

| Reasonable cause | Serious illness, death in the family, disaster, destroyed records, or similar events with documentation | Free; can remove penalties across multiple years where FTA can't |

| Installment agreement | Balances ≤ $50,000 can usually be set up online, up to 72 months | Setup fee varies (lower online/direct debit); cuts the failure-to-pay rate to 0.25%/month and halts escalation |

| Short-term plan / pay in full | Anyone who can clear the balance within 180 days | $0 setup; stops all penalty accrual when paid; interest runs until payoff |

| Form 843 refund claim | Already paid penalties that qualified for abatement | Free; requests the paid penalties back — relief isn't forfeited just because you paid first |

Strategy matters more here than on most tax problems, because abatement should usually come after the balance stops growing, not before. Penalties keep accruing until the underlying tax is paid or in an agreement — so if you win first-time abatement in month 3 and the balance keeps sitting, new failure-to-pay penalties simply re-accrue on top of the abated ones. File, get into a payment arrangement, then request relief. The full playbooks live in first-time penalty abatement, reasonable-cause penalty abatement, and — for the new automatic regime — automatic exemption from penalty (AEP) 2026.

Note what's not on the table: interest generally cannot be waived just because penalties were. When a penalty is abated, the interest charged on that penalty comes off with it — but interest on the tax itself stays until the tax is paid.

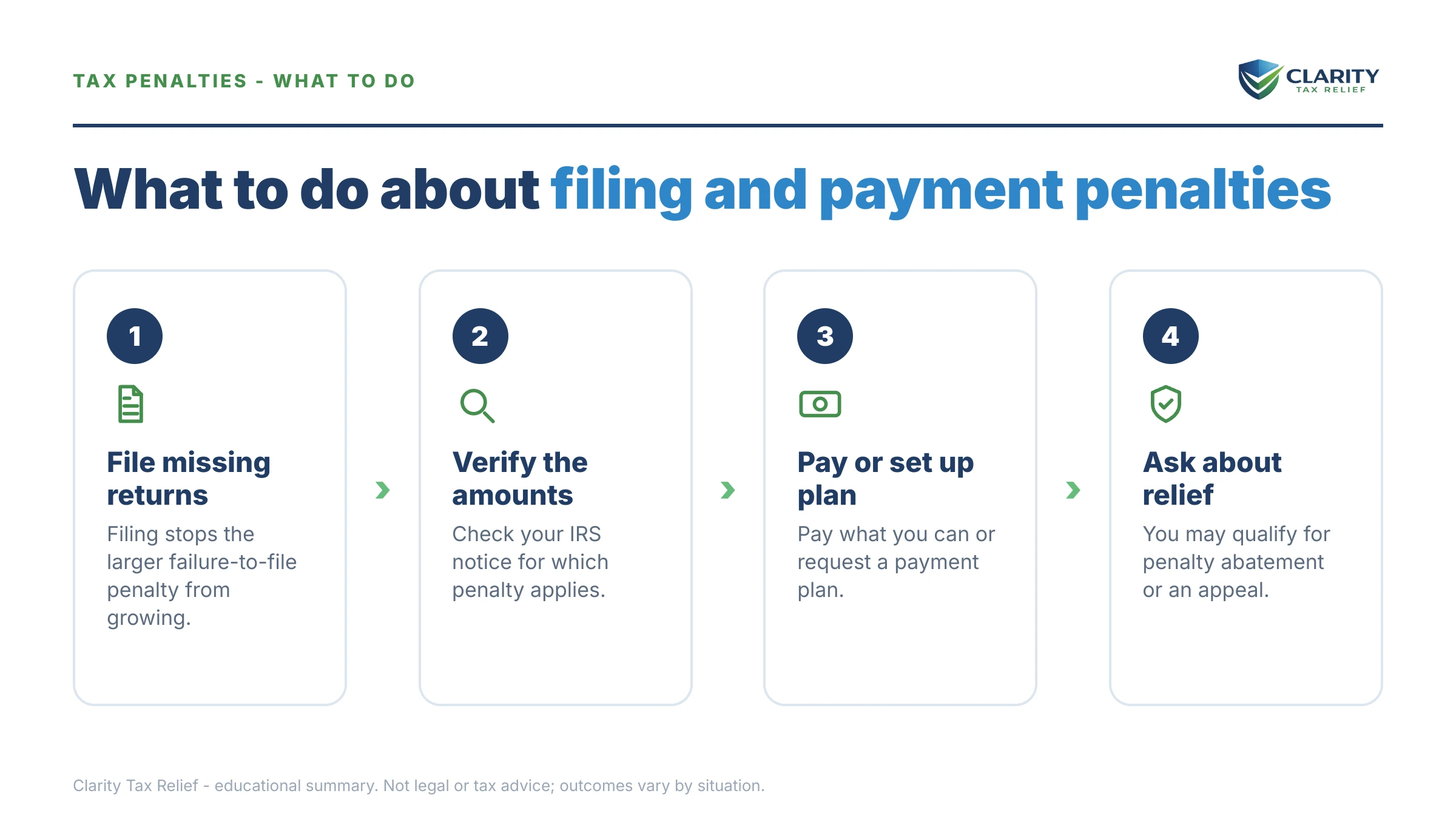

How to Respond, Step by Step

- Confirm which penalties posted. Log in to your IRS online account or pull your account transcript and look for the late-filing penalty line and transcript code 276, the failure-to-pay penalty, so you know exactly what was charged.

- File every unfiled return now. Filing — even with no payment attached — stops the 5% monthly failure-to-file penalty immediately; it is the single highest-value move on this list.

- Pay what you can and set up a plan for the rest. Any payment shrinks the base both penalties are calculated on, and an approved installment agreement cuts the failure-to-pay rate in half, to 0.25% per month.

- Request penalty relief. Ask for first-time abatement by phone or letter if your prior three years are clean, or submit Form 843 with documentation if you have reasonable cause like illness or disaster.

- Verify the abatement posted. Check your transcript a few weeks later for the penalty-removal entry, and appeal in writing if the IRS denies relief you qualify for.

For step 3, the walkthrough in how to set up an IRS payment plan online covers the whole process, including which plan tier fits which balance.

When You Can Handle This Yourself

Most single-year penalty problems don't need professional help. You can handle this on your own if: you filed on time and just owe the 0.5% penalty on a balance you can clear within 180 days; you have one late year with a clean three-year history behind it (first-time abatement is genuinely a phone call); or your balance is small enough that an online payment plan takes ten minutes to set up.

Experienced help changes the outcome in a narrower set of situations: multiple unfiled years (the order you file them in affects both the penalty total and refund recovery), a substitute return already assessed on inflated numbers, a reasonable-cause case that needs to be documented and argued rather than just claimed, a denied abatement worth appealing, or a lien threat landing in the middle of a refinance or home sale where timing is everything. In those cases, the fee usually costs less than the penalties left on the table.

Terms on Your Notice, Decoded

- Failure-to-file penalty — the 5%-per-month charge under IRC §6651(a)(1) for not filing a required return by its deadline.

- Failure-to-pay penalty — the 0.5%-per-month charge under IRC §6651(a)(2) for not paying assessed tax by the original due date.

- Combined-penalty offset — the rule that reduces the failure-to-file penalty by the failure-to-pay amount in overlapping months, capping the combined monthly charge at 5%.

- First-Time Abate (FTA) — administrative removal of these penalties for one year when your prior three years were penalty-free.

- Substitute for Return (SFR) — a return the IRS prepares for a non-filer using only reported income, with no deductions or credits.

- Statutory interest — daily-compounding interest charged on the tax and the penalties, at a rate reset quarterly; separate from both penalties and rarely waivable.

The IRS's own pages on the failure-to-file penalty and the failure-to-pay penalty publish the official rates, and IRS payment plans covers the arrangements that cut the paying penalty in half. For scale, the IRS assesses this penalty tens of millions of times a year — the data lives in our IRS failure-to-pay penalty statistics report.

Failure to File vs Failure to Pay: Your Questions, Answered

Which is worse, the failure to file penalty or the failure to pay penalty?

The failure-to-file penalty is far worse — 5% of your unpaid tax per month versus 0.5% for failure to pay, a 10-times difference. Both cap at 25% of the balance, but failure to file hits that cap in just 5 months while failure to pay takes 50 months. That's why filing on time matters even when you can't send a payment.

Can the IRS charge failure to file and failure to pay penalties at the same time?

Yes, and for most late filers with a balance due it charges both. In any month where the two overlap, the failure-to-file penalty is reduced by the failure-to-pay amount, so the combined charge is 5% per month — 4.5% for filing late plus 0.5% for paying late. Once the failure-to-file portion maxes out, the 0.5% failure-to-pay penalty keeps running on its own.

What is the maximum combined penalty for not filing and not paying?

The combined ceiling is 47.5% of the unpaid tax — 22.5% for failure to file plus 25% for failure to pay — and that's before interest. Interest compounds daily on both the tax and the penalties at a rate the IRS resets quarterly, so a balance left alone for years can grow well past 60% of the original tax.

Does filing a tax extension stop the failure to file penalty?

Yes — an extension moves your filing deadline to October 15, so no failure-to-file penalty applies if you file by then. It does not extend your time to pay: the 0.5% monthly failure-to-pay penalty and daily interest still run from the original April deadline on any unpaid balance. An extension is protection against the big penalty, not the small one.

Can the failure to file penalty be removed?

Often, yes. If your prior three years were penalty-free, first-time penalty abatement can wipe the failure-to-file and failure-to-pay penalties for one year with a phone call or letter. Starting in summer 2026, the IRS's Automatic Exemption from Penalty (AEP) applies similar relief automatically. Reasonable cause — serious illness, disaster, records destroyed — is a separate path when FTA doesn't fit.

Is there a failure to file penalty if the IRS owes me a refund?

No. Both penalties are calculated as a percentage of unpaid tax, so if your withholding covered your bill, the penalty math comes out to zero. The real risk for refund-year non-filers is the 3-year refund deadline: wait more than three years past the original due date and the refund is forfeited permanently.

What is the minimum penalty for filing more than 60 days late?

If your return is more than 60 days late and you owe tax, the IRS charges a flat minimum failure-to-file penalty — an inflation-adjusted amount in the several-hundred-dollar range — or 100% of the unpaid tax, whichever is smaller. This floor exists so small balances still sting; it's another reason to file the moment you realize you're late.

Does the failure to pay penalty rate ever change?

Yes, in both directions. It drops to 0.25% per month while an approved installment agreement is in effect and you filed on time. It jumps to 1% per month if you ignore the IRS's intent-to-levy notice for more than 10 days. Setting up a payment plan literally cuts the monthly penalty in half.

Your Next 24 Hours

- Pull your account transcript or IRS online account and write down two numbers: the late-filing penalty amount and the code 276 failure-to-pay amount for each year involved.

- Gather what a filing or relief request needs: the unfiled year's income documents (W-2s, 1099s), your last filed return, and any records of the event — illness, disaster, family crisis — that caused the lapse.

- Get a free case review at the 2-minute form or (888) 825-7779. Every month an unfiled return sits adds another 5% of the balance, and every month unpaid adds penalty and daily interest — the sooner the clock stops, the less there is to abate.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.