Penalty Relief

Reasonable Cause Penalty Abatement: What Qualifies and How to Request It in 2026

The short answer: reasonable cause penalty abatement removes IRS penalties — most often failure-to-file and failure-to-pay — when events beyond your control, like serious illness, disaster, or a death in the family, kept you from complying despite ordinary care. Request it in writing or on Form 843; interest charged on abated penalties comes off with them.

The penalties on your notice were added to a year you didn't choose — a hospital stay, a funeral, a flood, records you couldn't get. The IRS computer that assessed them never heard any of that, because you haven't told it yet. Reasonable cause abatement is the formal way to tell it, and it works when the story is documented, dated, and matched to the deadlines you missed.

Before you write anything, you need to know exactly which penalties you're fighting — the image below shows you what the penalty section of an IRS balance-due notice looks like and where to find each penalty by name, year, and amount.

⏱ The clock that matters: there's no deadline to request abatement of an unpaid penalty — but the failure-to-pay penalty adds another 0.5% of your unpaid tax every month and interest compounds daily until the balance is paid or abated. If you already paid the penalty, a Form 843 refund claim is generally limited to three years from filing or two years from payment, whichever is later.

What reasonable cause penalty abatement is — and which penalties it covers

Reasonable cause penalty abatement removes IRS penalties when circumstances beyond your control prevented you from filing or paying on time despite exercising ordinary business care and prudence. That phrase — "ordinary business care and prudence" — is the legal standard from the Internal Revenue Manual, and every request rises or falls on it. You're not asking for mercy; you're demonstrating that a reasonable person in your exact situation, acting carefully, would have missed the same deadline.

It applies to the penalties that hit most taxpayers hardest: the failure-to-file penalty (5% of unpaid tax per month, up to 25%), the failure-to-pay penalty (0.5% per month), and the failure-to-deposit penalty on business payroll taxes. How those penalties compound in the first place is covered in our guide to how much IRS penalties on back taxes really cost — this page is about getting them off your account.

Three important boundaries before you invest time in a request:

- Interest on the tax survives. Reasonable cause removes penalties and the interest charged on those penalties — but interest on the underlying tax is statutory. Separate, narrower rules cover IRS interest abatement when the IRS's own delays caused the interest.

- The estimated-tax penalty plays by different rules. The underpayment penalty for missed quarterlies generally can't be abated for reasonable cause; it has its own estimated tax penalty waiver exceptions on Form 2210 (casualty, disaster, retirement, disability).

- The accuracy-related penalty uses a cousin standard. The 20% accuracy related penalty requires showing "reasonable cause and good faith" for the position on the return — a different argument than explaining a missed deadline.

When the IRS evaluates your request, it asks five things: what happened and when, how those facts prevented compliance, how you handled the rest of your affairs during the same period, your compliance history, and how quickly you got compliant once the circumstances ended. A request that answers all five, with documents, is a different animal from a paragraph of apology.

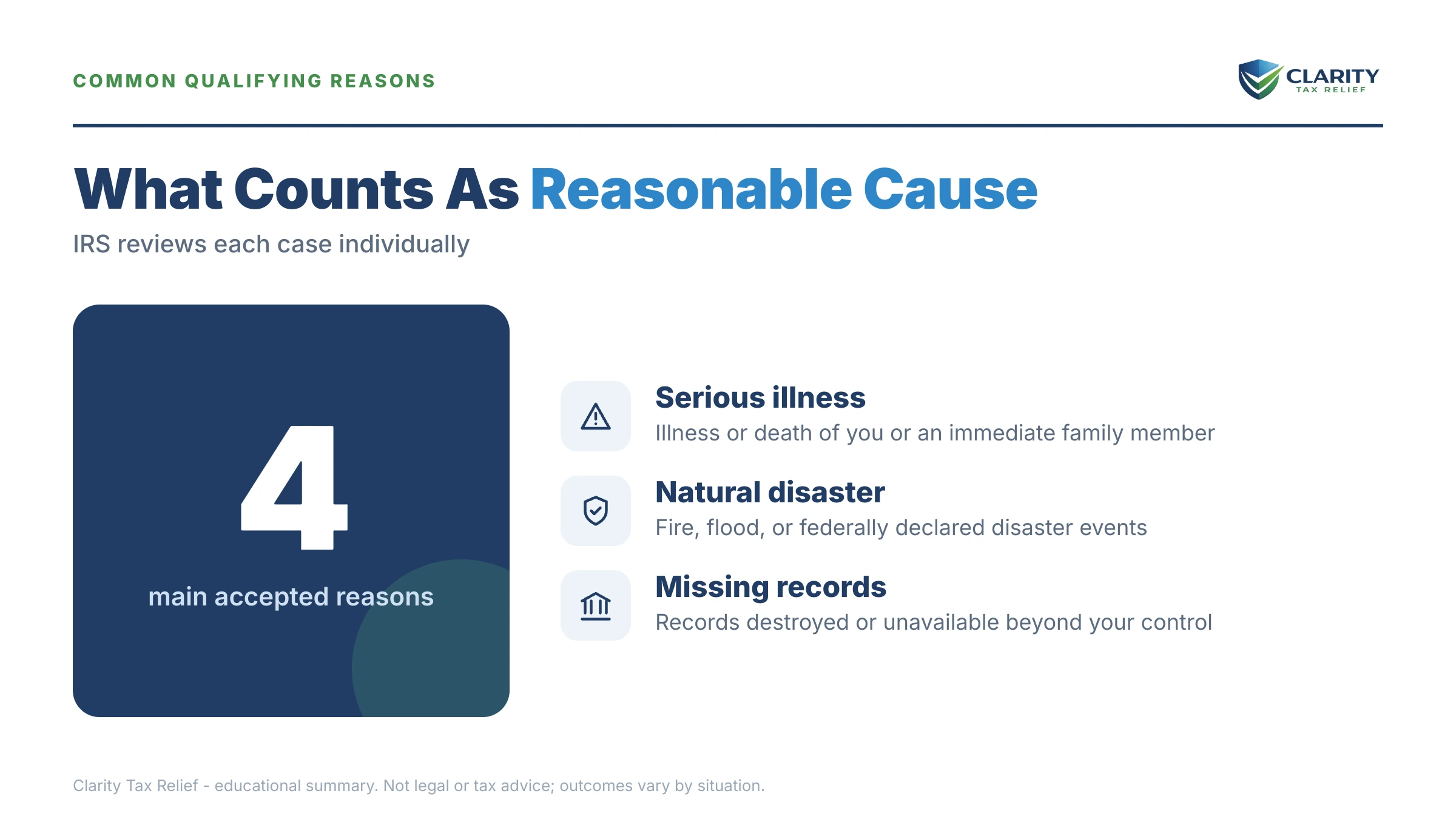

What counts as reasonable cause in 2026

The IRS accepts reasonable cause for death, serious illness, unavoidable absence, disaster, and inability to obtain records — and rejects it for forgetfulness, busyness, and misplaced reliance on a preparer to file. The table below maps the common fact patterns to the evidence the IRS expects for each; for deeper fact patterns and how officers actually weigh them, see our reasonable cause examples guide.

| Circumstance | Typically qualifies? | Evidence the IRS expects |

|---|---|---|

| Death of taxpayer or immediate family | Yes, for the surrounding period | Death certificate or obituary; dates showing proximity to the missed deadline |

| Serious illness or incapacitation | Yes — yours or a dependent's | Hospital/treatment records with admission and discharge dates; physician letters |

| Natural disaster, fire, casualty | Yes | Insurance or FEMA claims, photos, news of the declared disaster, repair records |

| Unable to obtain necessary records | Yes, if you tried promptly | Dated requests to the third party holding them, and their responses or silence |

| Wrong substantive advice from a tax professional | Sometimes | The written advice, proof you gave complete facts, the professional's credentials |

| Relied on preparer to file on time | No (the Boyle rule) | — |

| Lack of funds alone | No — but the cause of the shortfall can be | Bank records showing where the money went and why it was outside your control |

| Forgot, was busy, didn't know the rule | No | — |

Two of those rows sink more requests than everything else combined. First, the Boyle rule: the Supreme Court held that the duty to file on time is personal and non-delegable, so "my accountant was supposed to file it" fails almost every time — even when it's completely true. Second, money: "I couldn't afford to pay" is not reasonable cause by itself, but "a medical crisis consumed the tax money I had set aside, and here are the bank statements" can be, especially for the failure-to-pay penalty, where the IRS also weighs undue hardship.

Timing is the silent third factor. Your circumstance has to overlap the deadline you missed, and the IRS expects you to have gotten compliant within a reasonable time after it ended. A hospitalization that ended in June doesn't explain a return still unfiled the following March — expect at most a partial abatement covering the months the cause actually existed.

What happens if you don't request penalty relief

IRS penalties don't pause while you decide whether to fight them — they compound, and the collection system escalates on its own schedule. Here's the sequence if you do nothing:

- The failure-to-file penalty maxes out at 25% of the unpaid tax. If your return went in very late, this one has likely already hit its ceiling — the damage is fixed, but it's still removable.

- The failure-to-pay penalty keeps climbing — 0.5% of the unpaid tax every month toward its own 25% cap — while interest compounds daily on the tax and the penalties stacked on top of it.

- Collection notices march forward: the first bill, then reminder notices, then a CP504 that lets the IRS take your state refund, then a final notice of intent to levy with a 30-day clock before wages and bank accounts are fair game. Penalties ride along at every stage, inflating the balance the IRS is collecting.

- Your evidence goes stale. Hospitals purge records, insurance files close, witnesses move. The reasonable cause case you could document today gets harder to prove every year.

- If you pay and wait, the refund window closes. Once the claim period on a paid penalty lapses, abatement of that money becomes legally impossible — no matter how strong your facts were.

One more 2026 reality: the IRS workforce shrank roughly 27% in 2025, but penalty assessments and collection notices are automated and never slowed down. The system that added your penalties doesn't need staff — the process that removes them needs you to start it.

Staring at a stack of penalties you didn't earn?

Get your penalty breakdown reviewed free before another month of failure-to-pay penalty and daily interest posts to your account. An experienced tax professional will tell you which penalties are removable and which relief path fits your facts — no pressure, no obligation.

Reasonable cause vs. your other penalty relief options

Reasonable cause is one of several penalty relief doors, and picking the right one first can save you the whole argument. If your prior three years are clean, first time penalty abatement removes qualifying penalties with no explanation required — and starting summer 2026, the IRS's new automatic exemption from penalty (AEP) begins applying that first-time relief automatically, with no request at all. Reasonable cause matters most when FTA can't reach your situation: multiple penalized years, a compliance history that disqualifies you, or penalty types FTA doesn't cover.

| Relief option | Who's eligible | What it covers |

|---|---|---|

| First-Time Abate (FTA) | Clean compliance in the prior 3 years; returns filed, payments arranged | Failure-to-file, failure-to-pay, failure-to-deposit — typically one tax period |

| Automatic Exemption from Penalty (AEP) | Same first-time profile — applied automatically starting summer 2026 | Qualifying first-time penalties, no request needed |

| Reasonable cause | Anyone who can document circumstances beyond their control | FTF, FTP, FTD — can span multiple years if the circumstances did |

| Statutory exception | You relied on written IRS advice, or a declared-disaster extension applied | The specific penalty the IRS's own error or the disaster rules cover |

| Form 2210 waiver | Casualty/disaster, or retired (62+) or disabled with reasonable cause | Estimated-tax underpayment penalty only |

| Interest abatement (§6404) | Interest caused by IRS error or unreasonable delay | Interest on the tax — the one thing reasonable cause can't touch |

These options stack. A 1099 contractor with penalties across 2022, 2023, and 2024 might take FTA on the first penalized year and argue reasonable cause on the rest — the sequencing rules are covered in first time abatement multiple years. Business owners fighting payroll deposit penalties should start with 941 penalty abatement, where the failure-to-deposit tiers change the math. And if California's Franchise Tax Board penalized the same year, FTB penalty abatement runs on the state's own rules — never assume an IRS approval transfers.

| Request path | Cost | Typical timeline |

|---|---|---|

| Phone call to the IRS (small penalties, FTA checks) | Free | Sometimes resolved on the call; hold times in 2026 are long |

| Written reasonable cause statement (unpaid penalty) | Free | Typically a few weeks to a few months for a written decision |

| Form 843 refund claim (penalty already paid) | Free | Often several months; subject to the refund-claim window |

| Appeal after a denial | Free | Typically several months or more, but strong reversal odds on RCA denials |

| Professional representation | Varies by case complexity | Same IRS timelines — the value is in the request done right the first time |

One path deserves its own note: if you already paid the penalties, you're not requesting abatement anymore — you're filing a refund claim, and the process and deadlines change. Our guide to penalty abatement after paying walks through that version.

What abatement is worth: a $23,800 example

A successful reasonable cause request routinely removes 20–25% of a late filer's total balance, because that's what the two big penalties add up to. Here's the math on a clearly hypothetical case.

Say you're a 1099 contractor who owed $17,500 in self-employment and income tax on your 2024 return. A car accident put you in and out of the hospital through filing season; the return went in 14 months late and the balance is still unpaid. Your notice now reads roughly $23,800:

- Failure-to-file penalty: ~$3,938. It ran at 4.5% per month (5% reduced by the concurrent failure-to-pay penalty) and capped after five months at 22.5% of $17,500.

- Failure-to-pay penalty: ~$1,225. 0.5% × 14 months = 7% of $17,500 — and still climbing every month.

- Interest: ~$1,140, compounding daily on the tax and both penalties.

If reasonable cause is granted for both penalties — hospitalization records covering the deadline, plus a prompt filing once you recovered — roughly $5,160 in penalties comes off, plus the interest that accrued on them, dropping the balance to about $18,400. That's a swing of roughly $5,400 on a single well-documented letter. The tax and the interest on the tax remain, and you'd still want a payment plan for the rest — but you'd be paying for what you actually owe, not for the accident.

Now the caveat that keeps this honest: if you recovered in month six and didn't file until month fourteen, expect the IRS to abate only the months your cause covered. Run your own penalty numbers with our Penalty & Interest Calculator to estimate what a full or partial abatement would be worth in your case.

How to request reasonable cause penalty abatement, step by step

- Identify every penalty on your account. Pull your notice and your IRS account transcript so you know each penalty's type, tax year, and dollar amount before you write a word.

- Rule first-time abatement in or out first. If your prior three years are penalty-free, take FTA for that year with a phone call and save your reasonable cause argument for the years it can't cover.

- Build a dated timeline. List what happened and when, and line each event up against the filing or payment deadline it caused you to miss.

- Gather proof for every event on the timeline. Hospital and treatment records, a death certificate, insurance or FEMA claims, court records — documents that date each event, not just your account of it.

- Submit the request in writing. Send a reasonable cause statement with your evidence to the address on your notice, or file Form 843 if you already paid the penalty.

- Calendar the follow-up and appeal a denial. If the IRS denies the request, the letter explains your appeal rights — many automated denials are reversed by the Independent Office of Appeals.

For the writing itself, structure beats eloquence: facts, dates, the compliance standard, the evidence list. Our IRS penalty abatement letter guide shows the format that gets read, and the Form 843 penalty abatement request walkthrough covers the paid-penalty route line by line. If the answer comes back as a denial, don't refile the same letter — the penalty abatement appeal process puts your file in front of a human with settlement authority, which is often where these cases are actually won.

Why do first requests get denied so often? Many are scored by the IRS's Reasonable Cause Assistant — software that pattern-matches your explanation against decision trees. A fact pattern that doesn't fit the tree gets a form-letter denial even when a person would approve it. Treat a first denial as a routing problem, not a verdict.

When you can handle this yourself — and when help changes the outcome

Plenty of reasonable cause requests are genuinely do-it-yourself. Handle it alone when: the penalty is a few hundred dollars on a single year; you qualify for first-time abatement (that's one phone call, no story needed); or your case is one clean event — a death certificate dated two weeks before the deadline speaks for itself.

Experienced help changes outcomes in the messier cases: penalties spanning multiple years or multiple types, where sequencing FTA against reasonable cause determines how much survives; business payroll penalties, where deposit-tier rules complicate the math; an accuracy-related penalty, which needs a legal argument about the return position rather than a life story; a denial you need to appeal; or a levy notice already running alongside the penalty fight — in which case the collection clock, not the abatement, is your first emergency. A professional's real value isn't the letterhead; it's knowing which facts the IRS's own manual treats as decisive and building the file around them.

If your situation looks like the worked example above — multiple penalties stacked on a year you couldn't control — have an experienced tax professional pressure-test your timeline and evidence for free before you send anything, so your one first impression counts.

Terms in your penalty notice, decoded

- Reasonable cause — the IRS's legal standard for excusing a penalty: events beyond your control prevented compliance despite genuine care.

- Ordinary business care and prudence — the yardstick the IRS measures you against: what a careful person in your exact circumstances would have done.

- First-Time Abate (FTA) — administrative penalty relief for taxpayers with a clean prior three years; no explanation or evidence required.

- Automatic Exemption from Penalty (AEP) — the successor to FTA rolling out in summer 2026, applied automatically with no request.

- Form 843 — the "Claim for Refund and Request for Abatement," used mainly when you've already paid the penalty you're disputing.

- Reasonable Cause Assistant (RCA) — the IRS software that scores many first-round requests; its mechanical denials are frequently reversed on appeal.

Primary sources worth reading before you write: the IRS's own penalty relief overview, the official Form 843 page, and the Taxpayer Advocate Service if your request stalls inside the IRS with no response.

Reasonable cause penalty abatement FAQs

What qualifies as reasonable cause for IRS penalty abatement?

Circumstances beyond your control that prevented compliance despite ordinary business care: death or serious illness in your immediate family, natural disaster, fire, inability to obtain necessary records, or your own incapacitation. The IRS weighs timing — the event has to line up with the deadline you missed — plus your compliance history and how quickly you fixed things once you could. Being busy, forgetting, or not knowing the rules never qualifies.

Does not having the money count as reasonable cause?

Lack of funds by itself is not reasonable cause, but the reason you lacked funds can be. For the failure-to-pay penalty, the IRS considers whether you exercised ordinary care and still could not pay without undue hardship — say, a medical crisis drained the account you had set aside for taxes. Document where the money went and why the shortfall was outside your control.

Is relying on my accountant reasonable cause?

Only for substantive advice, not for filing on time. Under the Supreme Court's Boyle decision, the duty to file by the deadline is yours and cannot be delegated — "my CPA never filed it" almost always fails. But if a tax professional gave you wrong advice on a technical question, like whether income was taxable or which form applied, reliance on that advice can support abatement if you gave them complete, accurate information.

How long does a reasonable cause request take?

Phone requests for small penalties can be resolved on the call; written reasonable cause requests typically take a few weeks to a few months, and Form 843 refund claims often take several months. IRS staffing cuts in 2025 slowed written correspondence further, so send complete evidence the first time — an incomplete request that bounces back for more documentation can double the wait.

Does reasonable cause abatement remove interest too?

Only the interest that was charged on the abated penalties — that comes off automatically when the penalty does. Interest on the underlying tax is set by statute and survives a reasonable cause request. The IRS can abate interest on the tax itself only in narrow situations, mainly when its own errors or unreasonable delays caused the interest to accrue.

Can I get a penalty refunded after I already paid it?

Yes — file Form 843 with your reasonable cause statement and evidence attached. Refund claims are generally limited to three years from when the return was filed or two years from when you paid the penalty, whichever is later, so older paid penalties can expire out of reach. If your window is close to closing, file the claim now and supplement the evidence afterward.

Should I use first-time abatement or reasonable cause?

Check first-time abatement first: if your prior three years are penalty-free, it is near-automatic and requires no story or evidence. Save reasonable cause for the years FTA cannot reach — it is not limited to a single year and can cover multiple periods if your circumstances span them. Starting summer 2026, the IRS's Automatic Exemption from Penalty applies qualifying first-time relief without any request at all.

What happens if my reasonable cause request is denied?

You can appeal. Many first-round denials come from the IRS's automated Reasonable Cause Assistant software, which mechanically scores requests and rejects fact patterns a human officer would accept. The denial letter explains your appeal rights; a written protest to the IRS Independent Office of Appeals, with a tightened timeline and stronger evidence, frequently succeeds where the first request failed.

Does reasonable cause work for the estimated tax penalty?

Generally no. The underpayment penalty for missed quarterly estimates has its own narrow waiver rules on Form 2210 — a casualty or disaster, or retirement or disability with reasonable cause for the underpayment. If your notice shows an estimated-tax penalty alongside failure-to-file or failure-to-pay penalties, you may need two different relief requests for the same year.

Your next 24 hours

- Find the penalty breakdown on your notice — the section listing each penalty by name, tax year, and amount — and note the notice date. That list is your target.

- Gather three things: the notice, the tax return for that year (or proof you've now filed it), and the documents that date your hardship — hospital records, a death certificate, an insurance or FEMA claim.

- Get a free case review. Fill out the 2-minute form or call (888) 825-7779 and an experienced tax professional will map which penalties are removable — before another month of failure-to-pay penalty and daily interest posts to your balance.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.