Penalties & Relief

Estimated Tax Penalty Waiver: Form 2210 Exceptions (2024)

The short answer: an estimated tax penalty waiver can erase the penalty the IRS charges for underpaying quarterly taxes. You may qualify if you retired after 62 or became disabled, if a disaster or unusual event got in the way, or if your income was uneven. You claim it on Form 2210, Part II.

Not sure which exception fits your year?

Send us your return and the penalty figure. An experienced tax professional will check whether a Form 2210 waiver or the annualized method could lower it — free, confidential, no pressure.

⏱ Timing that matters: the penalty is settled when you file your return — there's no separate appeal window. Claim the waiver with your return by attaching Form 2210. If you already filed and paid the penalty, you generally have 3 years from the filing date (or 2 years from payment) to claim a refund using Form 843.

Why you got an estimated tax penalty

The U.S. tax system is "pay as you go." If you don't have enough tax withheld from a paycheck, you're expected to send the IRS estimated payments four times a year. When those payments fall short, you owe an underpayment penalty under Internal Revenue Code section 6654 — separate from any failure-to-pay charge. It's really interest on the tax you should have paid sooner.

This hits self-employed people, gig workers, retirees with investment income, and anyone with a big one-time gain. The good news: a Form 2210 exception or waiver can knock the penalty down or remove it. If you want the full math behind the charge, see our guide to the estimated-tax underpayment penalty.

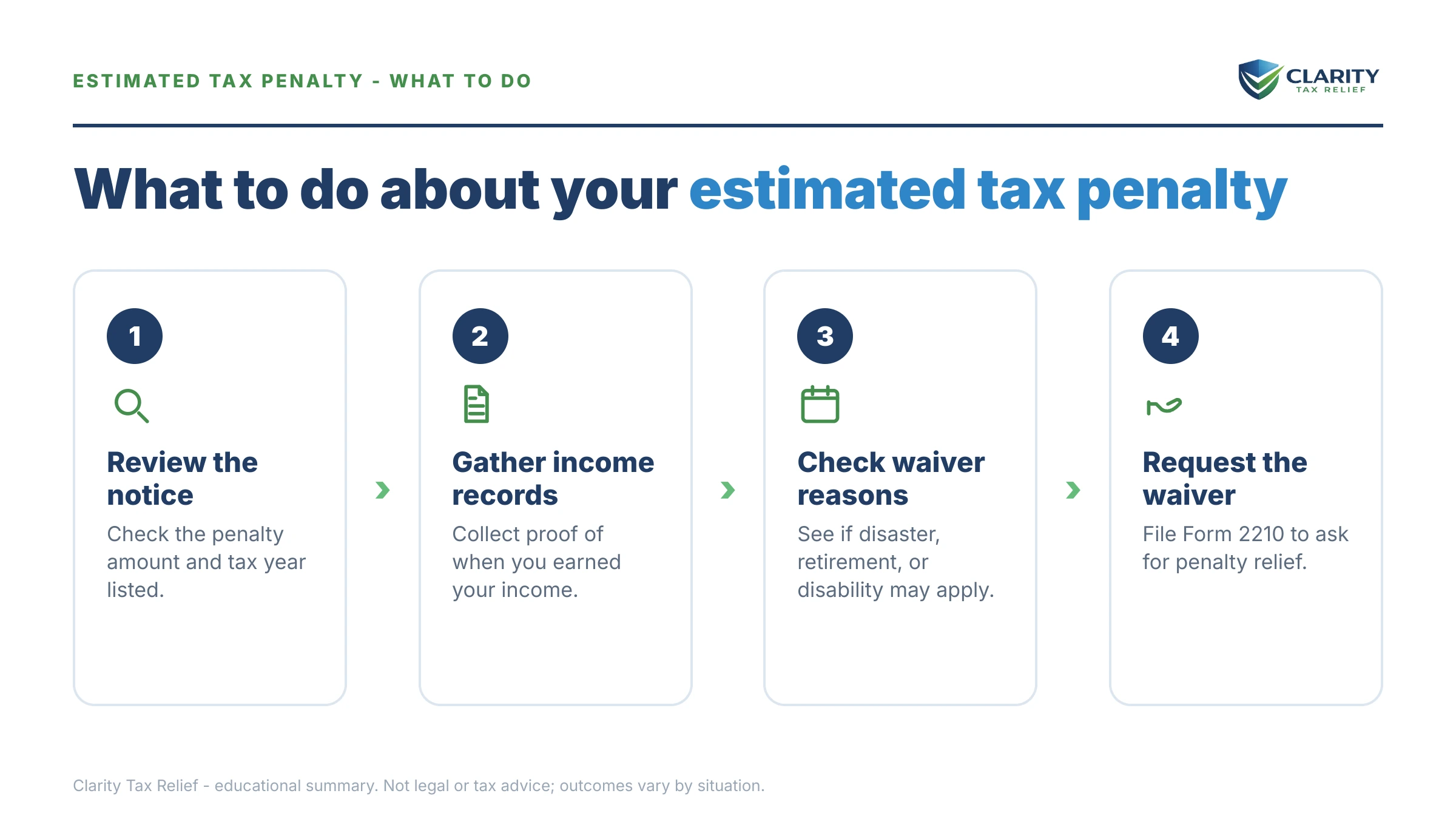

First, check whether you even owe the penalty

Before requesting any waiver, confirm a penalty applies at all. You owe nothing if you meet one of the "safe harbors." You're in the clear if your withholding plus estimated payments covered at least 90% of this year's tax, or 100% of last year's tax (110% if your prior-year adjusted gross income topped $150,000). There's also a small-balance rule: if you owe less than $1,000 after withholding, there's no penalty.

The IRS will often calculate the penalty for you, so many filers don't need Form 2210 at all. The flowchart in the official Form 2210 instructions tells you whether filing is even required.

The Form 2210 exceptions and waivers — who qualifies

Form 2210 builds in several ways to reduce or remove the penalty. These are the ones most people qualify for:

- Retirement or disability waiver. If you retired after reaching age 62, or became disabled, during the tax year (or the year before) — and the underpayment was due to reasonable cause, not willful neglect — the IRS can waive the penalty entirely.

- Casualty, disaster, or unusual circumstance. If a fire, flood, federally declared disaster, or other event beyond your control made it unfair to charge the penalty, you can request a waiver. The IRS already grants automatic relief in many declared disaster areas.

- Annualized income installment method. Not technically a "waiver," but the most powerful tool. If your income arrived unevenly — a year-end bonus, a fall property sale, a busy holiday season — Schedule AI of Form 2210 matches the penalty to when you actually earned the money. It frequently shrinks the charge.

- Federal disaster relief. When the IRS postpones deadlines for a disaster, payments made by the new date count as on time. That can wipe out a penalty that looks owed on paper.

One thing the estimated tax penalty does not qualify for: first-time penalty abatement. That program covers the failure-to-file and failure-to-pay penalties only. For the estimated tax penalty, the Form 2210 routes above are your path.

A worked example

Say a self-employed designer expected to owe $12,000 in tax. She made no estimated payments because most of her income — a $40,000 project — landed in November. On a straight calculation, Form 2210 might show a penalty of around $400, because the IRS assumes income came in evenly across four quarters.

Using the annualized income method on Schedule AI, she shows that almost nothing was earned in the first three quarters. The penalty is calculated only on the period when the money actually arrived — and her penalty drops to a fraction of the original figure. Same income, same tax, far smaller penalty, just by reporting when she earned it.

What happens if you ignore it

The estimated tax penalty doesn't snowball the way unpaid back taxes do, but ignoring it still costs you:

- You skip Form 2210. The IRS figures the penalty itself — on the least favorable, even-quarters assumption — and adds it to your bill.

- The penalty becomes part of your balance due. If you don't pay, it now also accrues interest and a separate failure-to-pay penalty.

- It joins the collection sequence. An unpaid balance leads to a CP14 notice and the standard collection notices that follow if left unaddressed.

- You may overpay. Most people who never claim a waiver simply pay a penalty they could have legally reduced or removed.

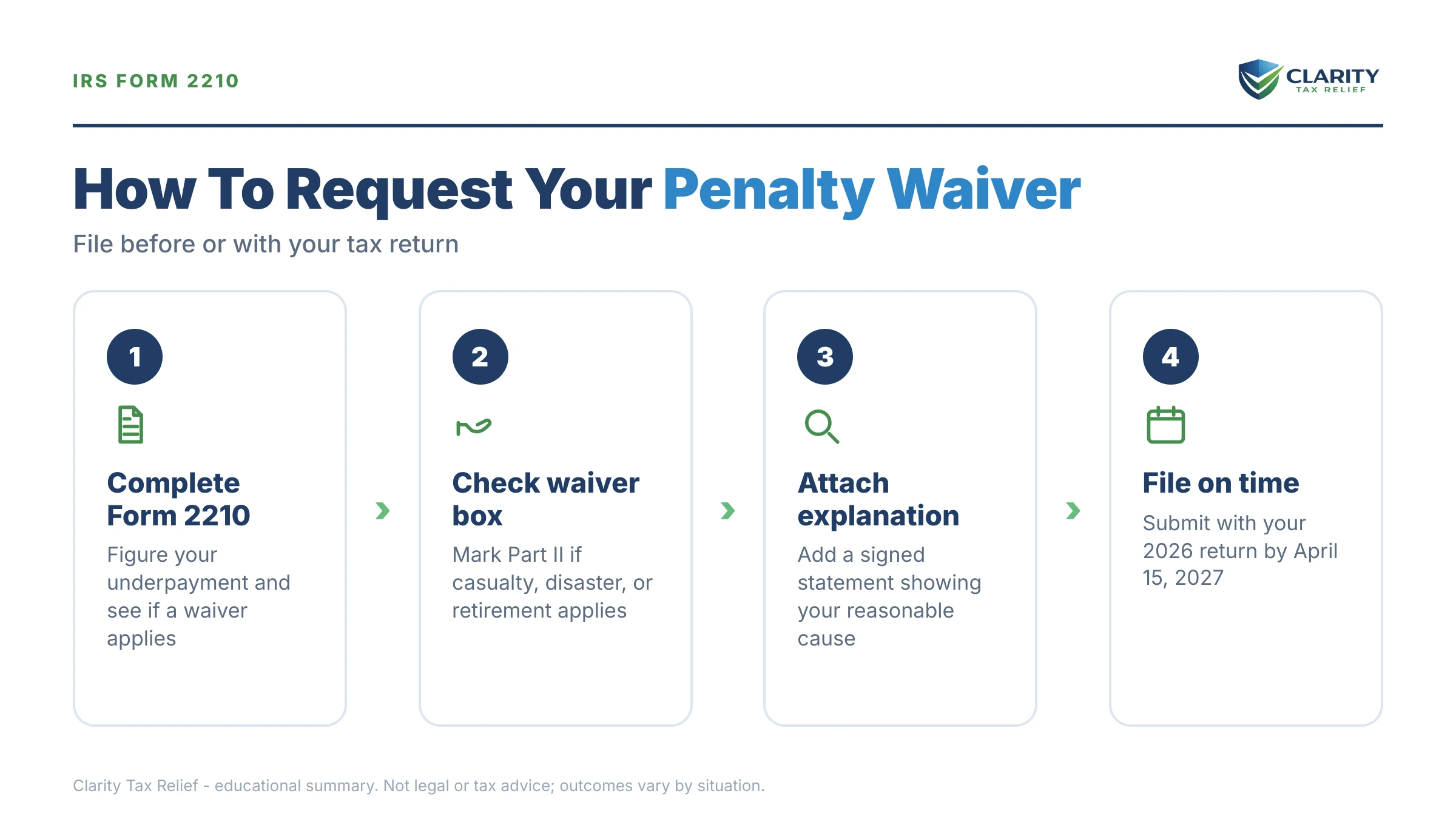

How to claim an estimated tax penalty waiver, step by step

- Confirm a penalty actually applies. Run the safe-harbor checks above (90% / 100% / 110%, or under $1,000 owed). If you're covered, you owe nothing.

- Get Form 2210. Download the current form and instructions from IRS.gov. Most tax software includes it.

- Pick your basis. Retirement/disability or disaster waiver? Complete Part II and check the waiver box. Uneven income? Complete Schedule AI for the annualized method.

- Write a short statement. For a waiver, attach a brief explanation — your retirement date, the disaster, or the circumstance — plus any supporting documents.

- File it with your return. Attach Form 2210 so the IRS adjusts the penalty before billing you.

- Already paid the penalty? Use Form 843 to request a refund — generally within 3 years of filing or 2 years of payment.

Estimated tax penalty waiver questions, answered

Can the estimated tax penalty be waived?

Yes, in specific situations. The IRS can waive the estimated tax penalty if you retired after age 62 or became disabled during the tax year, if a casualty, disaster, or other unusual circumstance made paying unfair, or if you fit an automatic exception built into Form 2210. You request the waiver on Form 2210 with a short statement explaining why.

Do I even have to file Form 2210?

Often you don't. If you don't owe the penalty, or the IRS will figure it for you, you can usually skip Form 2210 entirely. You only need to file it to claim a waiver, use the annualized income method, or because a box on the form's flowchart tells you to. The form's instructions walk you through whether filing is required.

What is the 90 percent and 100 percent safe harbor?

You avoid the penalty if your withholding and estimated payments cover at least 90 percent of this year's tax, or 100 percent of last year's tax (110 percent if your prior-year adjusted gross income was over $150,000). Meeting either safe harbor means no penalty, even if you still owe a balance at filing time.

Does the estimated tax penalty qualify for first-time penalty abatement?

No. First-time penalty abatement covers the failure-to-file and failure-to-pay penalties, not the estimated tax penalty under Internal Revenue Code section 6654. To reduce or remove the estimated tax penalty you use the Form 2210 exceptions and waivers, or the annualized income method if your income was uneven during the year.

I had uneven income during the year. Can that lower the penalty?

Yes. If most of your income arrived late in the year — a year-end bonus, a fall home sale, or a busy gig-work season — the annualized income installment method on Schedule AI of Form 2210 can match the penalty to when you actually earned the money. It often shrinks or eliminates the penalty, but it takes more paperwork.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.