Penalties & Interest

Can IRS Interest Be Waived? The Honest Answer for 2026

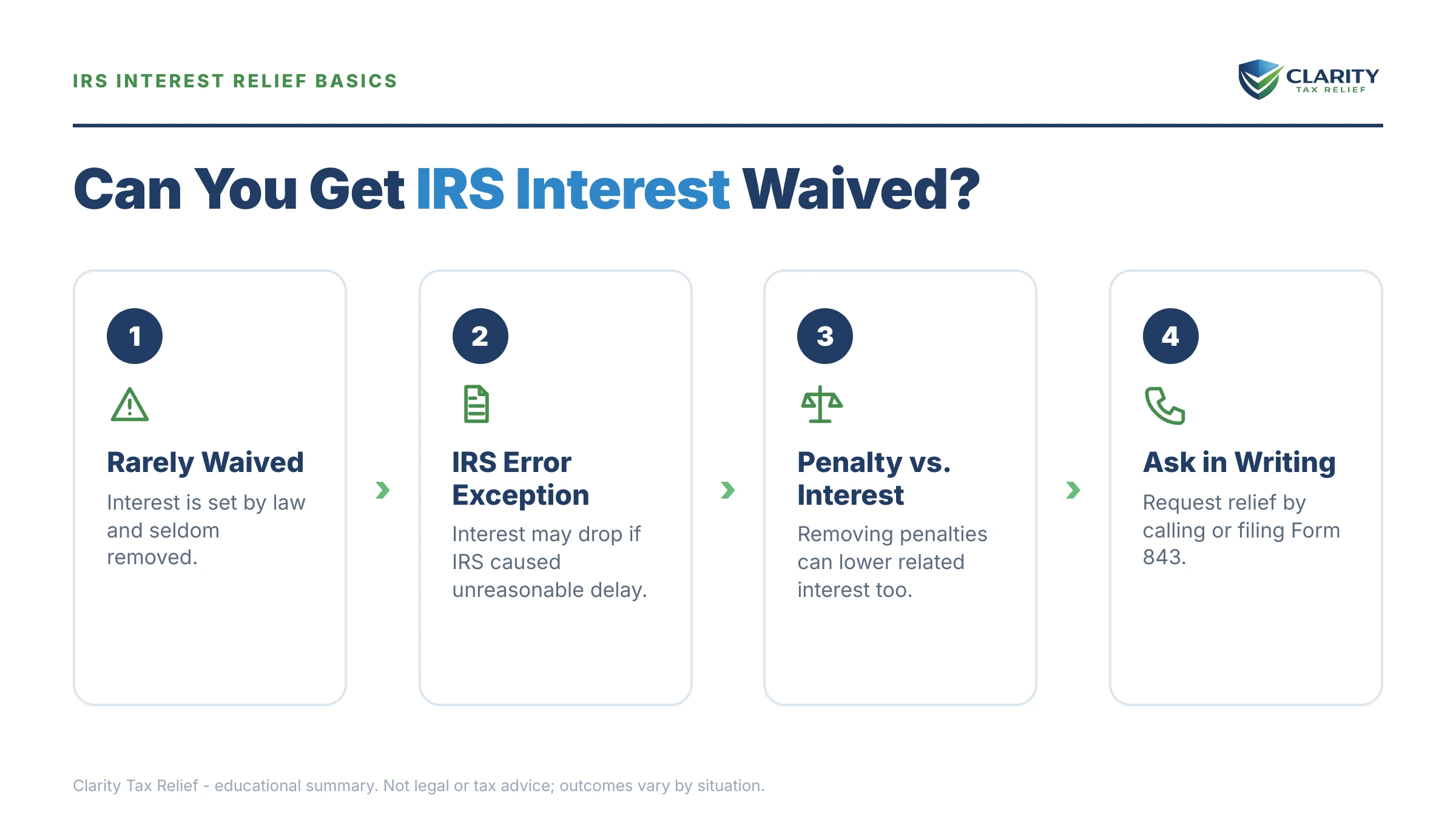

The short answer: can IRS interest be waived? Rarely — the law gives the IRS almost no discretion to forgive interest for a good excuse. It comes off in only three situations: IRS error or delay caused it (Section 6404 abatement), the penalty it rides on gets abated, or a statutory exception like disaster or combat-zone relief applies.

You run your own business, you finally logged into your IRS account to face the number, and it's bigger than the debt you remember — because interest has been quietly stacking on top of the tax and the penalties every single day. Here's the part most pages won't say plainly: the interest is the hardest piece to remove, but it is not untouchable. There are three legitimate paths, and one of them — attacking the penalties underneath the interest — works far more often than people think.

⏱ The clock that matters: there's no response deadline on interest — the deadline is every day. IRS interest compounds daily, which means today's interest gets charged interest tomorrow. Every month you wait to act, the amount that can't be waived gets bigger.

Why the IRS charges interest — and why it almost never gets waived

The IRS charges interest by statute at the federal short-term rate plus 3 percentage points for individuals, compounded daily — and unlike penalties, the law gives the IRS almost no discretion to forgive it. Congress treats interest as the cost of holding the government's money, not as a punishment. That's the entire reason "I had a good excuse" works for penalties and fails for interest.

Penalties exist to punish behavior, so the tax code builds in mercy: reasonable cause, first-time relief, and — starting in summer 2026 — automatic exemptions. Interest exists to make the Treasury whole, so the code builds in almost none. Reasonable cause cannot remove interest on tax — ever. Section 6404 of the tax code lists the only doors, and they're narrow.

Because the rate resets quarterly, the exact percentage changes; our guide to current quarterly IRS interest rates tracks each change. What doesn't change is the structure: interest runs on the unpaid tax and on unpaid penalties, from each amount's due date until the day it's paid. That second part — interest on penalties — is the crack in the wall this article will show you how to use.

What happens if you let the balance keep growing

Unpaid IRS interest compounds daily, so an ignored balance grows every single day — while the IRS's automated collection notices escalate on their own schedule. For a self-employed taxpayer with no employer withholding to hide behind, the sequence looks like this:

- Daily compounding. Interest accrues on the tax, on the penalties, and on yesterday's interest. Nothing pauses it — not a payment plan, not hardship status, not a pending abatement request.

- The bill cycle. A CP14 balance-due notice gives you roughly 21 days (10 business days when the balance is $100,000 or more) before the reminder notices (CP501, CP503) start arriving, each one showing a higher total than the last.

- Intent to levy. A CP504 lets the IRS take your state tax refund; the LT11 final notice starts a 30-day clock, after which the IRS can levy bank accounts and business receivables.

- Asset exposure widens. Once levies begin, retirement money and vehicles are on the table — see can the IRS take my 401(k) and can the IRS take my car for exactly where those lines sit.

- The passport threshold. Once your certified debt crosses $66,000 (the 2026 threshold), the IRS can certify it to the State Department, which can deny or revoke your passport — a real problem if your business travels. A $48,300 balance growing at several hundred dollars a month is on a path toward that line; see passport revoked for tax debt.

None of this requires a human at the IRS to look at your file. The 2025 workforce cuts made agents harder to reach, but the notice and levy systems are automated — they never stopped.

Watching interest stack on a balance you can't waive away?

Send us your notice or your account balance. An experienced tax professional will split it into tax, penalties, and interest — and tell you in one free call which charges can realistically come off. Interest compounds daily; the review takes minutes.

When can IRS interest be waived? The three real paths

IRS interest can be waived in exactly three situations: the IRS caused it, the penalty underneath it gets removed, or a statutory exception applies. Everything else you've read about getting IRS interest forgiveness for hardship or a good excuse is marketing, not law.

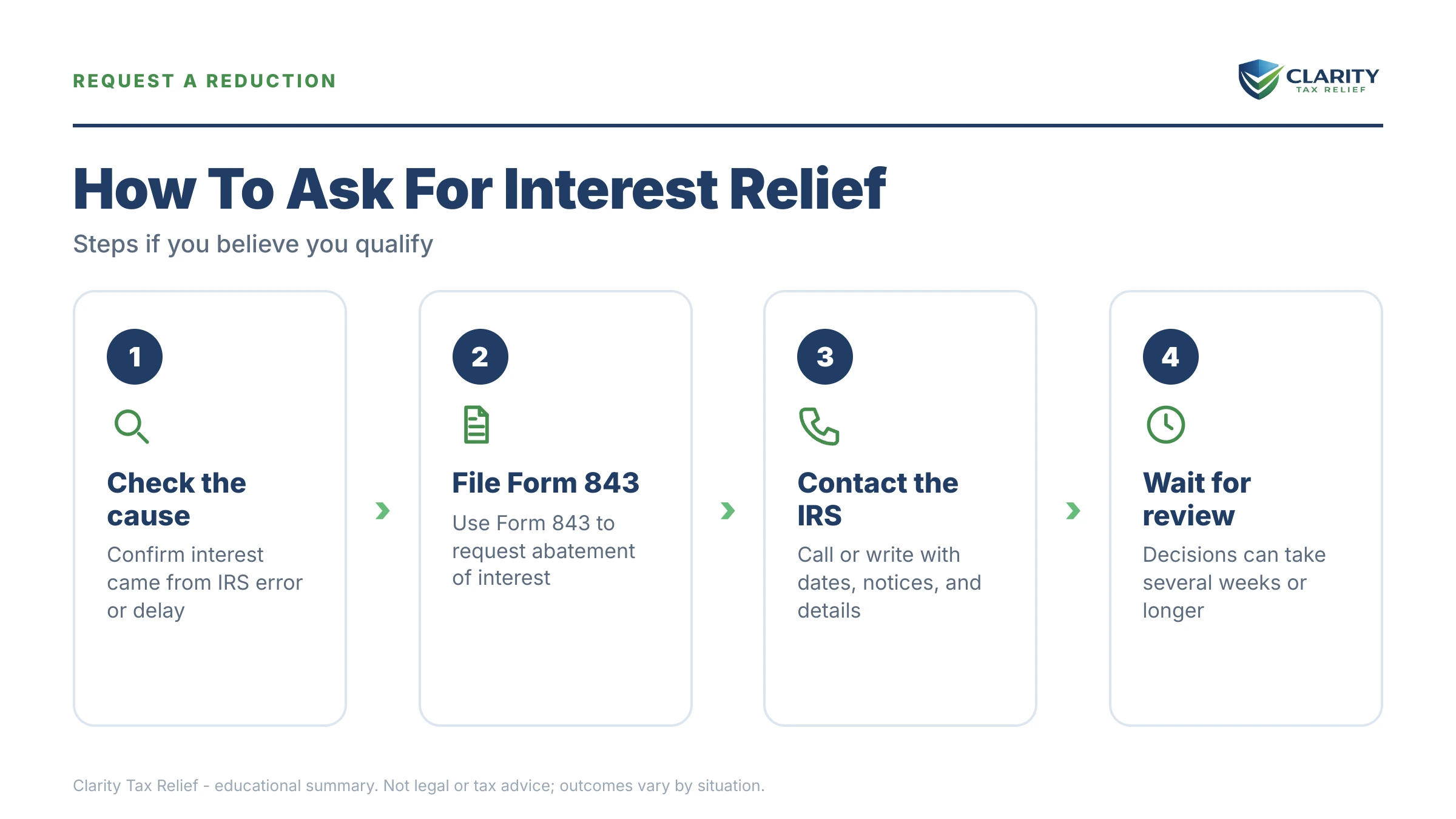

Path 1 — the IRS caused it (Section 6404(e) abatement). If interest piled up because of an unreasonable error or delay by an IRS employee performing a ministerial or managerial act — your audit sat untouched for months after an agent transferred, your response was lost and unworked, a processing mistake delayed resolution — that slice of interest can be abated. You must not have significantly contributed to the delay, and generally the delay has to occur after the IRS first contacted you in writing. The request goes on Form 843; our full guide to IRS interest abatement covers what counts as a qualifying delay.

Path 2 — remove the penalty, and its interest goes with it. Interest charged on a penalty is removed automatically when that penalty is abated. Since penalties are far easier to waive than interest, this is the highest-percentage play for most people — the next section walks through it.

Path 3 — statutory exceptions. A handful of situations suspend interest by law: federally declared disaster relief postpones deadlines without interest for covered taxpayers, combat-zone service suspends interest and penalties during service plus 180 days, and if you filed on time but the IRS waited more than 36 months to notify you of additional tax, interest for the period after that 36-month mark can be suspended until shortly after the notice arrives (exceptions apply, including fraud).

| Relief path | What it removes | Who qualifies | How to request |

|---|---|---|---|

| Section 6404(e) abatement | Interest caused by IRS error or delay | IRS ministerial/managerial delay you didn't contribute to | Form 843 with a dated timeline |

| Interest on abated penalties | All interest charged on the removed penalty | Anyone whose penalty is abated (FTA, AEP, reasonable cause) | Automatic once the penalty comes off |

| 36-month notice suspension | Interest accruing after the 36-month mark | Individuals who filed on time; IRS notified late | Automatic by law — verify on your transcript |

| Disaster relief | Interest during the postponement period | Taxpayers in a federally declared disaster area | Automatic by address |

| Combat-zone relief | Interest during service + 180 days | Qualifying military service | Automatic; notify the IRS if misapplied |

| Dispute the underlying tax | Interest on tax you never owed | Anyone whose assessment is reduced (amendment, reconsideration) | Recalculated automatically when tax drops |

The bigger win: remove the penalties, and their interest goes too

When the IRS abates a penalty, the interest charged on that penalty is removed automatically — no separate request, no Form 843. For most taxpayers asking whether IRS interest can be forgiven, this is the answer that actually moves the number, because penalties are where the tax code's mercy lives.

Three penalty-relief doors, in the order to try them:

- First-time penalty abatement — if your compliance was clean for the prior three years, the failure-to-file and failure-to-pay penalties can come off on request, often in a single phone call.

- Automatic Exemption from Penalty (AEP) — starting in summer 2026, the IRS is replacing first-time abatement with an automatic version: qualifying penalties come off with no request needed. If you're reading this mid-2026, check whether your year is covered before writing a letter you may not need.

- Reasonable cause penalty abatement — serious illness, disaster, records destroyed, reliance on bad professional advice. This works on penalties that first-time relief doesn't reach, including the 20% accuracy-related penalty.

Here's why this matters for the interest question. On a multi-year self-employment balance, penalties routinely make up 15–25% of the total, and interest has been compounding on those penalties the whole time. Abate the penalties and you remove two layers at once: the penalty itself and every dollar of interest it generated. On your transcript, a manual removal posts as code 780-style abatement entries alongside adjusted interest lines.

| Charge on your account | How it accrues | Can it be waived? | Main relief path |

|---|---|---|---|

| Failure-to-file penalty | 5% per month, capped at 25% | Yes — most waivable charge | First-time abatement / AEP, reasonable cause |

| Failure-to-pay penalty | 0.5% per month (0.25% on an approved plan), capped at 25% | Yes | First-time abatement / AEP, reasonable cause |

| Accuracy-related penalty | Flat 20% of the understatement | Yes, but harder | Reasonable cause (first-time relief doesn't apply) |

| Interest on the tax | Short-term rate + 3%, compounded daily | Rarely | Section 6404 abatement, statutory exceptions |

| Interest on penalties | Same rate, compounded daily | Yes — indirectly | Falls off automatically when the penalty is abated |

What a $48,300 balance actually costs — and what relief changes

Say you're a sole proprietor who owes $48,300 for tax year 2024, broken down as $36,000 in tax, $9,600 in combined late-filing and late-payment penalties, and $2,700 in interest. (This is a hypothetical illustration — your rate and mix will differ; you can run your own numbers with our IRS penalty and interest calculator, which estimates, not guarantees, your figures.)

Do nothing, and here's the monthly bleed at an illustrative 7% annual interest rate:

- Interest: $48,300 × 7% ÷ 12 ≈ $282 per month, compounding daily.

- Failure-to-pay penalty: 0.5% × $36,000 unpaid tax = $180 per month (until it hits its 25% cap).

- Total drift: roughly $462 a month — about $5,500 a year — added to a balance that started at $48,300.

Now run the relief playbook. If a clean three-year history (or the new AEP rules) removes the $9,600 in penalties, the interest that accrued on those penalties — call it a few hundred dollars here — comes off automatically with them. Your balance drops to roughly $38,400. Set up a direct-debit installment agreement and the failure-to-pay penalty falls to 0.25% per month (about $90 instead of $180). The monthly accrual drops from ~$462 to roughly $315 — and it shrinks further with every payment, because interest is charged on what remains, not on what you started with.

What relief didn't do: touch the interest on the $36,000 of tax. Unless the IRS caused a documented delay, that interest gets paid or settled — it doesn't get waived. That's the honest shape of every interest case.

How to request IRS interest relief, step by step

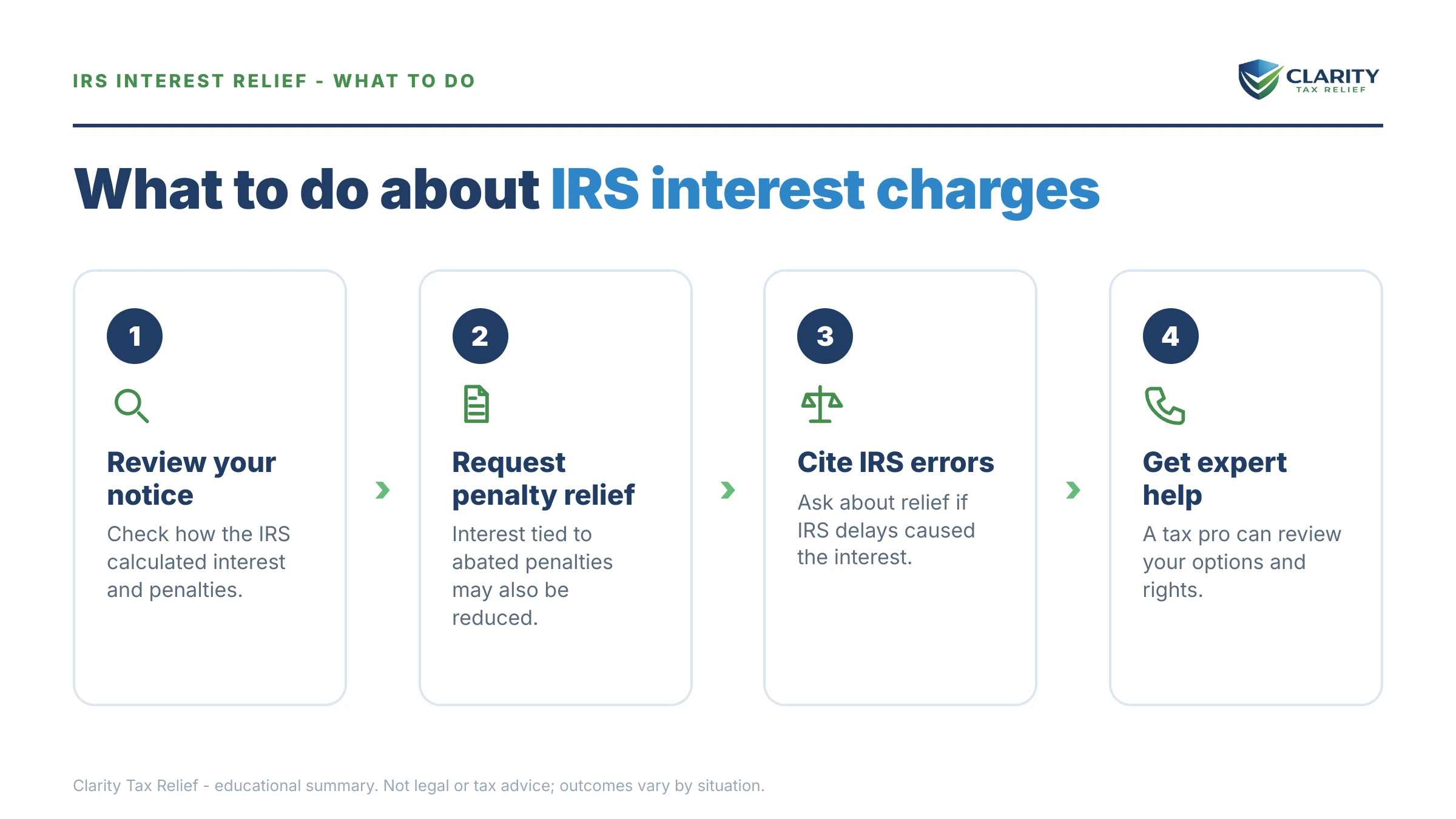

Interest relief starts with knowing exactly what you're being charged — then attacking each piece with the tool built for it.

- Split your balance. Pull your IRS account transcript and separate tax, penalties, and interest — interest posts as code 196, so you can see exactly what each relief path could remove.

- Request penalty abatement first. Ask for first-time abatement or reasonable-cause relief on the penalties — when a penalty comes off, the interest charged on it comes off automatically.

- File Form 843 if the IRS caused a delay. Request interest abatement under Section 6404 with a dated timeline showing the specific IRS error or delay — one form per tax year.

- Slow the accrual. Pay whatever you can now and set up a payment plan — interest is charged on the remaining balance, and the failure-to-pay penalty typically drops to 0.25% per month on an approved agreement.

- Appeal a denial in writing. If the IRS denies your Form 843 request, you can appeal — keep every submission and response dated and documented.

Our Form 843 walkthrough covers the boxes, attachments, and mailing addresses line by line. For the wider strategy — which order to fix returns, penalties, and the balance itself — start with our guide on how to settle tax debt yourself.

When you can handle this yourself — and when help changes the outcome

Plenty of interest problems don't need a professional. If your balance is one year, your prior compliance is clean, and you can pay within 180 days, you can call the IRS, request first-time penalty abatement, and set up a short-term plan yourself — total cost: your time on hold. The same goes for a straightforward streamlined installment agreement set up online for a balance under $50,000.

Experienced help earns its fee in the harder patterns: a Section 6404 claim, where winning depends on reconstructing a dated timeline of IRS inaction from transcripts and correspondence; multiple unfiled or amended years, where the order of fixes changes the penalty math; self-employment balances large enough that an Offer in Compromise or hardship status is on the table; or any case where a levy is already in motion. A $48,300 balance sits squarely in "get the free review first" territory — not because you can't do it alone, but because a missed penalty-abatement angle or a botched 843 timeline costs real money that never comes back.

Terms on your account, decoded

- Abatement — the formal removal of a charge (penalty or interest) the IRS already put on your account.

- Section 6404 — the tax-code section that lists the only situations where the IRS may remove interest.

- Ministerial act — a routine, procedural IRS task (like transferring a file); delays here can qualify interest for abatement.

- Managerial act — an IRS management decision, like losing your case in a personnel shuffle; also a qualifying delay.

- Underpayment rate — the quarterly interest rate on unpaid tax: the federal short-term rate plus 3 percentage points for individuals.

- Code 196 — the transcript line showing interest assessed on your account, so you can measure exactly what you're fighting.

The IRS's own explanation of how interest is charged and the narrow removal rules is at IRS.gov — interest on underpayments, and the abatement request form lives at About Form 843. If the IRS's own delay is the problem and normal channels stall, the Taxpayer Advocate Service exists for exactly that.

IRS interest waiver questions, answered

Can the IRS waive interest for reasonable cause?

No — reasonable cause can remove penalties, but the law does not allow the IRS to waive interest on tax just because your reason for paying late was good. Interest abatement under Section 6404 applies only when IRS error or delay caused the interest, or when a statutory exception like disaster relief applies. The practical workaround is to abate the penalties, because the interest charged on an abated penalty comes off with it.

Does first-time penalty abatement remove interest?

Not on the underlying tax. First-time abatement removes qualifying penalties if you have a clean compliance history for the prior three years, and the interest that accrued on those penalties is removed automatically with them. Interest on the tax itself keeps running until the tax is paid. Starting in summer 2026, the new Automatic Exemption from Penalty (AEP) applies this kind of relief automatically, with no request needed.

What form do I use to request IRS interest abatement?

Form 843, Claim for Refund and Request for Abatement. Check the box for interest under Section 6404 and attach a dated timeline showing the IRS error or delay that caused the interest — for example, months your response sat unworked. File a separate Form 843 for each tax year, and expect the IRS to reduce only the interest tied to its own delay, not the whole interest balance.

Does an IRS payment plan stop interest from accruing?

No — interest compounds daily until the balance reaches zero, even on an approved installment agreement. A plan does help: while it's in effect, the failure-to-pay penalty typically drops from 0.5% to 0.25% per month if you filed your return on time, and enforced collection stops. Paying the plan off early cuts total interest, since interest is charged on the remaining balance, not the original one.

What is the IRS interest rate on unpaid taxes right now?

For individuals, the rate is set each quarter at the federal short-term rate plus 3 percentage points, and it compounds daily. Because it resets quarterly, check the current figure on IRS.gov before running your own math. The same rate applies to interest charged on penalties, which is why removing a penalty also shrinks the interest side of your balance.

How do I find out how much of my balance is interest?

Pull your IRS account transcript or log into your IRS online account. On the transcript, interest posts as code 196, and penalties post under their own codes, so you can split the balance into tax, penalties, and interest in a few minutes. That split matters because each piece has a different relief path — penalties are the most waivable, interest the least.

Does IRS interest ever expire or go away on its own?

Yes — interest dies with the debt. The IRS generally has 10 years from assessment to collect (the CSED), and when that clock runs out, the tax, penalties, and interest all become uncollectible together. But the clock pauses for things like offers in compromise, bankruptcy, and appeals, so most balances don't simply age out on schedule.

Can an Offer in Compromise settle the interest too?

If accepted, yes — an Offer in Compromise resolves the entire balance, including penalties and interest, for the offer amount. Acceptance is means-tested, not automatic: the IRS accepted roughly 1 in 5 offers in FY2024, and approval depends on whether your offer matches what the IRS calculates it could ever collect from you. Interest stops being an issue only after the offer is paid and its terms are met.

Your next 24 hours

- Split the number. Log into your IRS online account or pull your account transcript, and write down three figures: tax, penalties (their own codes), and interest (code 196). You can't fight a total — you can fight the pieces.

- Gather the paper. The return for each year involved, every IRS notice with its date, and any correspondence showing the IRS sat on something — that timeline is the raw material of a Section 6404 claim.

- Get the free review. Use the 2-minute form or call (888) 825-7779. An experienced tax professional will tell you which penalties are realistically abatable, whether an interest claim exists in your file, and what the balance costs you each month you wait — because the interest, unlike the penalties, compounds every day you don't act.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.