IRS Collections

Can the IRS Take My 401(k)? What's Actually Protected in 2026

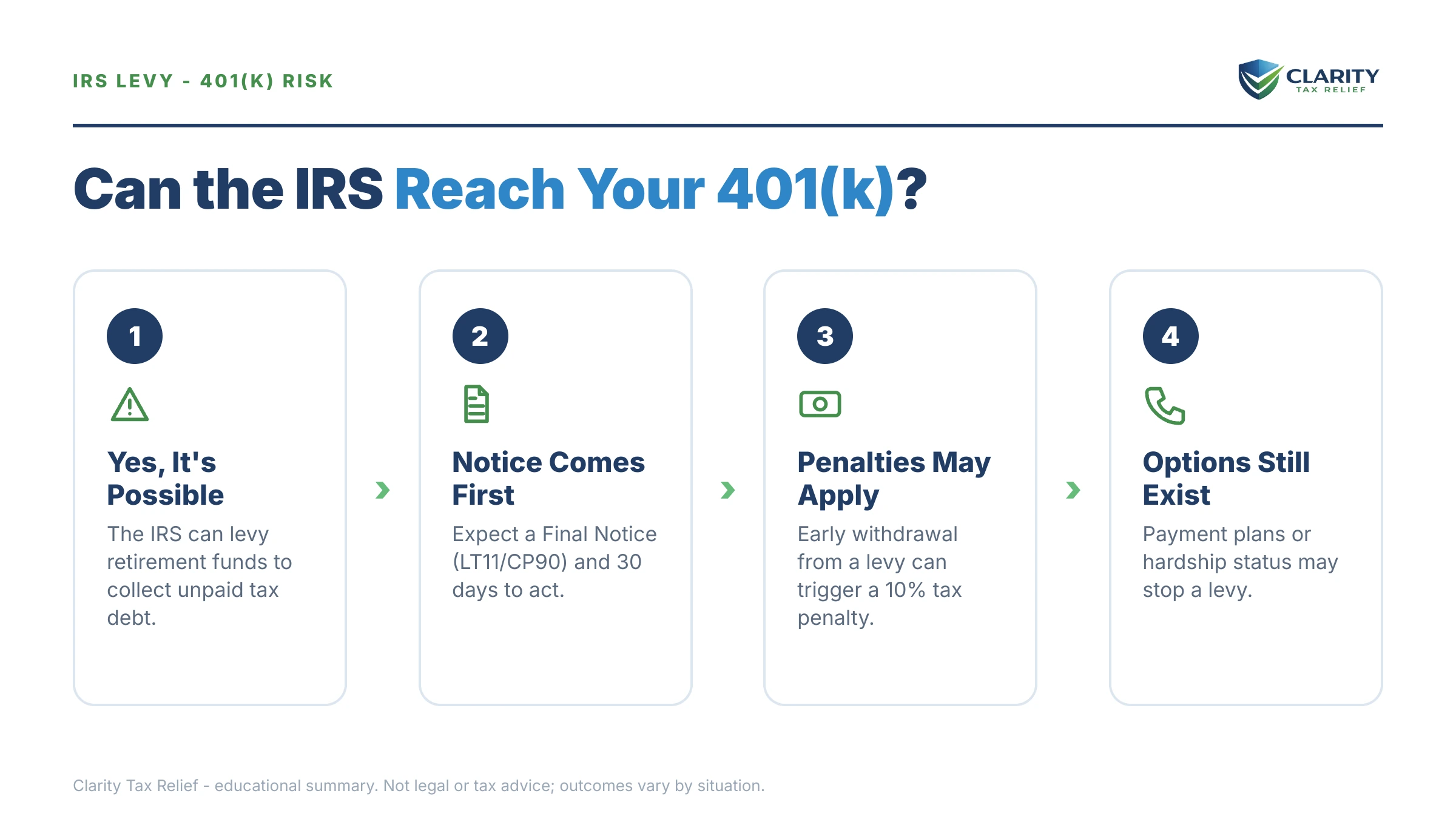

The short answer: Can the IRS take my 401k? Yes — it's one of the only creditors federal law lets past ERISA's shield, and unpaid federal taxes are the reason. In practice, retirement levies are rare: a revenue officer must document flagrant conduct, obtain extra written managerial approval, and can only reach money you could withdraw yourself.

Maybe the divorce settlement just split the retirement accounts and the ink is barely dry — and now an old IRS balance from a joint return has you staring at the 401(k) statement you fought to keep, wondering whether that money is next. Take a breath. The path that ends in any levy is slow, letter-by-letter, and interruptible — and retirement accounts sit at the very back of the line. Here's the full map, including what the IRS can legally reach, what it almost never touches, and how to end the threat for good.

⏱ The clock that matters: no levy of any asset — bank account, paycheck, or 401(k) — is legal until the IRS sends a final notice of intent to levy (LT11 or Letter 1058) and 30 days pass. If that letter is in your mailbox, the date printed on it is your real deadline; filing Form 12153 for a CDP hearing within the window pauses levy action while your case is heard.

Can the IRS take my 401k? The legal answer

The IRS can legally levy a 401(k) because a federal tax debt is the one creditor claim ERISA's anti-alienation rule does not stop. ERISA — the federal law governing workplace retirement plans — walls your 401(k) off from lawsuits, private debt collectors, and most bankruptcy claims. The tax code carves out an exception for federal tax collection: under IRC §6331, the IRS may levy "all property and rights to property," and courts have consistently held that includes employer retirement plans.

Two separate powers are in play, and they're easy to confuse. A federal tax lien attaches automatically to everything you own once a balance is assessed and unpaid — including your 401(k) — but a lien is a legal claim, not a seizure. A levy is the actual taking, and it operates under much stricter rules for retirement money than for a checking account.

There's also a hard structural limit: a levy only gives the IRS the rights you currently hold. If your plan won't let you withdraw today — because you're still employed and the plan bars in-service withdrawals — the IRS steps into your shoes and finds the same locked door you would. It can attach your future right and wait, but it cannot force the plan to pay out money you couldn't reach yourself.

When the IRS actually levies a retirement account — and why it's rare

In practice, the IRS levies a 401(k) only after a revenue officer documents flagrant conduct and obtains additional written managerial approval. The IRS's own internal manual treats retirement money differently from every other asset, requiring the officer to work through three questions before a retirement levy can go forward:

- Are there other ways to collect? Wages, bank accounts, refunds, and payment agreements all come first. Retirement money is a last resort, not a first move.

- Was your conduct flagrant? That means things like hiding assets, funneling money into the plan while ignoring the debt, piling up new unpaid balances year after year, or repeatedly making and breaking agreements. Simply owing money — even for several years — is not flagrant.

- Do you depend on the account for retirement? If taking the money would leave you without the means to cover necessary living expenses in retirement, the manual weighs against the levy.

Just as important: the IRS's automated collection machinery — the system that mails most notices and issues most bank and wage levies — never touches retirement accounts. A 401(k) levy requires a human revenue officer assigned to your case, which for individual debts generally means larger balances, unfiled years, or business/payroll issues. The deeper mechanics of retirement levies, including how the plan administrator responds, are covered in our guide to an IRS levy on a 401(k) or retirement account.

| Your 401(k) situation | Can the IRS levy it? | Why |

|---|---|---|

| Vested balance, you've left that employer (or can withdraw) | Yes | You have a present right to the money; a levy steps into your shoes |

| Still employed; plan bars in-service withdrawals | Not yet | The levy attaches your future right; funds become reachable when you can withdraw |

| Unvested employer match | No | Not your property until it vests |

| Roth 401(k) balance | Yes, same rules | Roth status changes the tax treatment, not the levy protection |

| 401(k) loan feature | Can't be forced | A levy reaches distributions, not loans — though the IRS may ask you to borrow during negotiations |

| Share transferred to your ex by QDRO | Follows the owner | Once transferred, it's your ex's property — your levy can't reach it, and theirs can't reach yours |

The same "yes legally, rarely in practice" framework applies to IRAs — with one meaningful difference: IRAs lack ERISA protection against private creditors, though the IRS analysis is similar. See can the IRS take my IRA for the account-specific rules.

Divorced with a joint-return debt: whose 401(k) is exposed?

Both spouses are liable for 100% of a joint-return balance, and a divorce decree does not change what the IRS can collect from either of you. If your decree says your ex pays the tax debt and they don't, the IRS can still pursue you — and your assets — for the whole amount. That's a contract between the two of you, not a limit on the government; we break down why in why the IRS ignores your divorce decree.

The flip side protects you too. If the debt comes from your ex's separate return, their business, or their payroll taxes, your 401(k) is not reachable for it. And any share of a 401(k) transferred by QDRO belongs to whoever received it: the IRS collecting from your ex cannot reach the portion now titled to you.

If the joint-year debt traces to income your ex hid or misreported, innocent spouse relief can remove your liability entirely — which protects every asset you own, retirement included. Sorting out who realistically pays what after a split is its own analysis; start with divorce and IRS debt: who pays.

What happens if you ignore the debt: the sequence before any levy

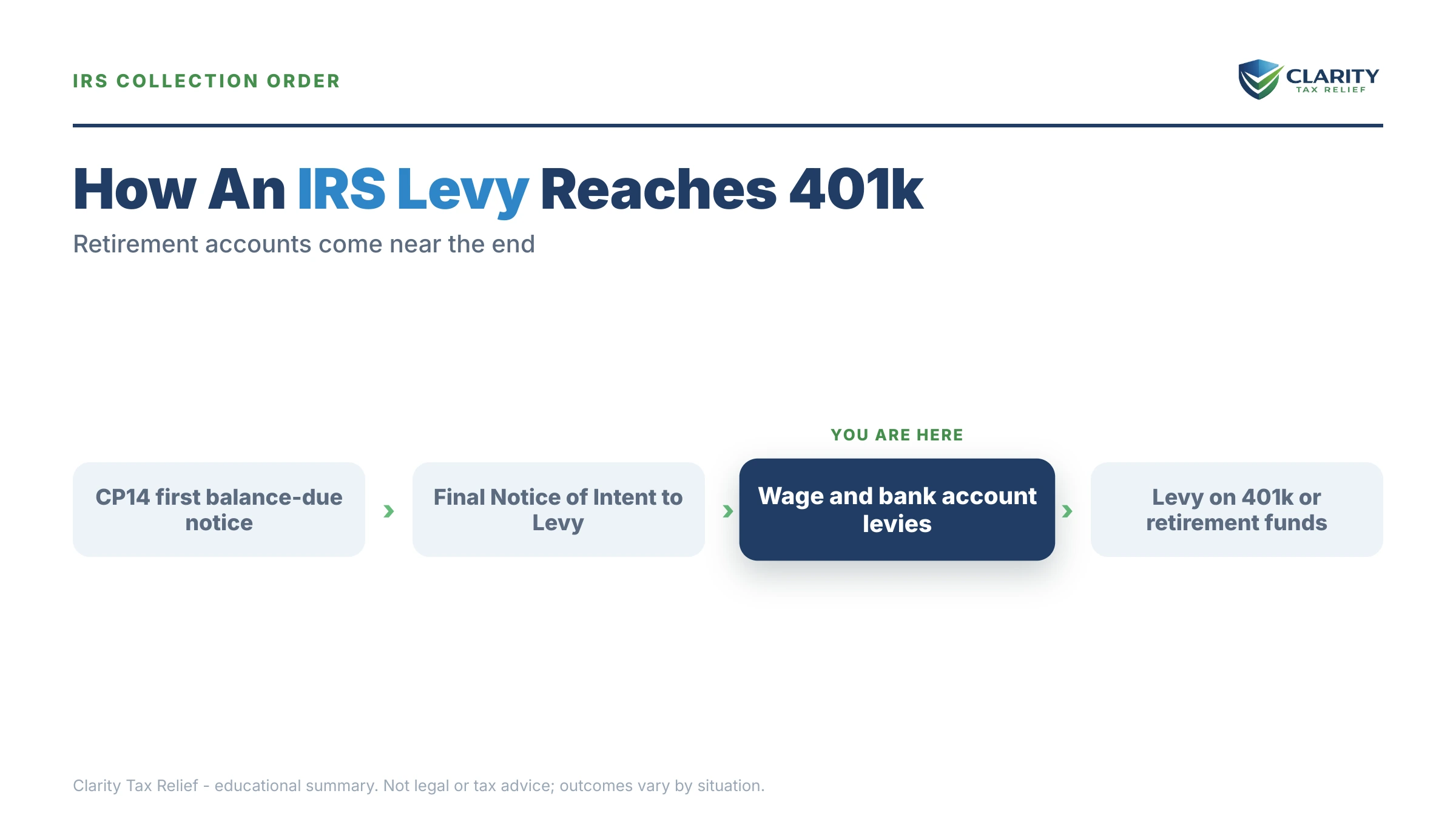

No IRS levy of any kind can happen until a final notice of intent to levy is issued and 30 days pass — and a 401(k) levy sits at the far end of an even longer road. The sequence runs in order, each stage carrying more enforcement power than the last:

- CP14 — the first bill. A statement of the balance. No enforcement power; typically about 21 days to respond before the next notice queues up (10 business days if the balance is $100,000 or more).

- CP501 / CP503 — reminders. Still just bills, but interest and the monthly failure-to-pay penalty are compounding the whole time.

- CP504 — intent to levy your state refund. The IRS can now take your state tax refund, and a federal tax lien filing becomes a live possibility. Not yet the final notice.

- LT11 / Letter 1058 — final notice. This starts the 30-day clock and your Collection Due Process rights. After 30 days, levies become legal.

- Enforcement — the easy assets first. Bank accounts (funds held 21 days before they're sent), a continuous wage levy that runs until released, and up to 15% of Social Security. The IRS is far more likely to garnish your paycheck than crack your 401(k) — you can estimate what a wage levy would take with our IRS Wage Garnishment Calculator.

- Retirement accounts — last, and human-approved only. Only a revenue officer, only after the flagrant-conduct analysis, only with written managerial sign-off.

One 2026 reality worth naming: per TIGTA reports, IRS staffing fell roughly 27% in 2025, so reaching a human is harder than ever — but the notice-and-levy machinery is automated and never stopped. Silence doesn't slow the sequence; it just removes your input from it. The same logic applies to your other property, on different timelines — see can the IRS take my house for how real-estate seizure compares.

Worried your retirement savings are exposed?

Send us your most recent IRS letter. An experienced tax professional will tell you exactly where you sit in the collection sequence, which assets are genuinely at risk, and the fastest way to shut it down — free and confidential. If an LT11 is already in hand, the 30-day window on it is real, so don't sit on it.

Your options: how to resolve the debt before a levy is ever on the table

A tax debt under $10,000 qualifies for a guaranteed installment agreement — a plan the IRS must accept if you've filed all returns, haven't had an installment agreement in the past five years, and agree to pay the balance within three years. Any agreement in good standing takes levies off the table entirely, which means the whole 401(k) question becomes moot. For the full do-it-yourself playbook on each program, see our pillar guide to how to settle tax debt yourself; here's how the options stack up for a balance like $8,900:

| Option | Who qualifies | Cost & timeline |

|---|---|---|

| Short-term payment plan | Anyone who can pay in full within 180 days | $0 setup; interest and the 0.5%/month late-pay penalty continue until paid |

| Guaranteed installment agreement | Individuals owing $10,000 or less in tax, all returns filed, full pay within 3 years | Setup fee varies (lowest with direct debit); set up online in one sitting |

| Streamlined installment agreement | Balances up to $50,000; up to 72 months | Online setup, no detailed financial disclosure required |

| Currently Not Collectible | Income doesn't cover IRS allowable living expenses (Form 433-F financial review) | $0; collection pauses, but interest accrues and the account is periodically re-reviewed |

| Offer in Compromise | Assets plus future income genuinely can't cover the debt; means-tested — per IRS data, the IRS accepted roughly 1 in 5 offers in FY2024 | $205 fee plus 20% down for lump-sum offers (both waived with low-income certification); months to a decision |

| Penalty relief (First-Time Abate / AEP) | Clean compliance for the prior 3 years; starting summer 2026, Automatic Exemption from Penalty applies without a request | Free; reduces the balance rather than restructuring it |

The math: raiding your 401(k) vs. a payment plan (hypothetical)

Say you owe $8,900 from a joint return, you're 41, recently divorced, and in the 22% bracket. Pulling the money out of your 401(k) voluntarily costs 22% income tax plus the 10% early-withdrawal penalty — you keep only 68 cents of every dollar. To net $8,900, you'd have to withdraw about $13,088 ($13,088 × 0.68 ≈ $8,900), surrendering roughly $4,188 to tax and penalty, plus decades of compound growth on the whole amount. Many people who do this discover the withdrawal itself creates next spring's balance due — the classic early-401(k)-withdrawal tax bill trap.

Compare a guaranteed installment agreement: $8,900 ÷ 36 months is about $247 a month before interest and the 0.5% monthly late-pay penalty, which continue to accrue on the shrinking balance. Even with that accrual, the total extra cost of paying over time is a fraction of the $4,188 the withdrawal burns on day one — and your retirement money keeps growing untouched.

And if the IRS ever did levy the account (again: rare, human-approved, last resort), the $8,900 taken would still be taxable income to you — about $1,958 at 22% — but the 10% penalty would not apply, because levy distributions are exempt from it. That exemption is the one silver lining of a levy, and it never applies to a withdrawal you make yourself.

How to respond, step by step

- Locate your latest IRS notice. The letter code (CP14, CP504, LT11) tells you exactly how close enforcement is — and whether any levy is even legally possible yet.

- Check the 30-day window. If you received an LT11 or Letter 1058 within the last 30 days, file Form 12153 to request a Collection Due Process hearing; levy action pauses while your case is heard.

- Verify the balance and whose it is. Log in to your IRS online account, confirm the tax year, and note whether the debt came from a joint return — that changes which relief options apply to you.

- Set up a resolution before a revenue officer gets the file. Under $10,000, a guaranteed installment agreement can usually be arranged online in one sitting, which takes every levy off the table while you pay.

- Run the math before touching retirement money. Compare the true after-tax cost of a withdrawal against a monthly plan — for most balances, the plan wins by thousands of dollars.

When you can handle this yourself — and when help changes the outcome

If you agree with the balance, owe under $10,000, and can manage roughly $250 a month, you don't need to hire anyone. Set the plan up directly on the IRS payment plans page, keep every payment current, and the 401(k) question disappears — no levy of any asset happens while an agreement is in good standing.

Experienced help earns its cost in a handful of specific situations: an LT11 has arrived and the 30-day CDP window is running; a revenue officer has been assigned to your case; you have multiple unfiled years alongside the balance; the joint-return debt really belongs to your ex and you need an innocent spouse case built on evidence; or you're weighing an Offer in Compromise, where the financial math determines everything. If a levy is already causing genuine hardship and you can't get traction with the IRS, the Taxpayer Advocate Service is a free, independent avenue as well.

Terms in this fight, decoded

- Levy — the actual seizure of money or property to pay a tax debt; the taking itself, not the threat.

- Lien — the government's automatic legal claim against everything you own once tax is assessed and unpaid; silent until enforced.

- ERISA anti-alienation — the federal rule that shields workplace retirement plans from creditors; federal tax collection is the major exception.

- Flagrant conduct — the internal IRS standard (hiding assets, pyramiding new debt, repeated broken agreements) a revenue officer must document before levying retirement money.

- Vested balance — the portion of your 401(k) that legally belongs to you; unvested employer contributions are outside the IRS's reach.

- Collection Due Process (CDP) — your right, after a final levy notice, to a hearing (requested on Form 12153) that pauses levy action while alternatives are considered.

Can the IRS take my 401k? Your questions, answered

Does the IRS actually take 401(k)s very often?

No — retirement account levies are among the rarest IRS collection actions. The automated collection system never issues them; only a revenue officer can, and only after documenting that your conduct was flagrant and getting additional written managerial approval. The taxpayers who see them typically hid assets, pyramided new debt, or broke repeated agreements — not people who simply couldn't pay one year's bill.

Can the IRS take my 401(k) while I'm still employed there?

Only to the extent you could take the money yourself. A levy gives the IRS your rights — nothing more — so if your plan bars in-service withdrawals, the IRS attaches your future right and waits. Once you separate from the employer, retire, or become eligible to withdraw, the funds become reachable. Plans that allow hardship or in-service withdrawals give the IRS the same door you have.

Do I pay the 10% early-withdrawal penalty if the IRS levies my 401(k)?

No. Money paid out of a retirement plan because of an IRS levy is exempt from the 10% additional tax, even if you're under 59½. You still owe ordinary income tax on the distribution, which can create a new balance for next year. Be careful: the exemption applies only to an actual levy — if you voluntarily withdraw money to pay the IRS, the 10% penalty applies normally.

Can the IRS force me to withdraw from my 401(k) to pay my debt?

The IRS cannot order you to take a voluntary withdrawal. What it can do is count accessible retirement money as an asset when it evaluates a payment plan, hardship claim, or Offer in Compromise — so a large reachable balance can get a settlement or hardship request rejected. Money you cannot legally touch yet, such as an unvested employer match, is not counted.

Can the IRS take my 401(k) for my ex-spouse's tax debt?

It depends on where the debt came from. If it arose from a joint return you both signed, you are each liable for 100% of it, and your 401(k) is exposed no matter what the divorce decree says. If the debt is from your ex's separate return or their business, your account is not reachable for it. Innocent spouse relief can remove your liability for a joint-year debt your ex created.

Does a federal tax lien attach to my 401(k)?

Yes. A federal tax lien attaches to everything you own, including retirement accounts — ERISA does not block a federal tax lien or levy. A lien is a silent legal claim, not a seizure; your plan keeps operating normally. It matters most if you later take distributions or the case escalates to enforcement, and it is released once the debt is resolved.

How much of my 401(k) can the IRS take?

Up to your entire vested, accessible balance — but no more than the debt plus penalties and interest. The IRS serves a levy notice on the plan administrator, who pays over the amount you currently have a right to receive. Unvested employer contributions can't be taken because they aren't yet your property. For a smaller balance like $8,900, an actual retirement levy is extremely unlikely.

Your next 24 hours

- Find your most recent IRS letter and note the code and date in the top corner. Anything before LT11 or Letter 1058 means no levy is legally possible yet; an LT11 means the 30-day CDP clock is running from the date printed on it.

- Gather three things: your last filed return, your divorce decree (if the debt is from a joint year), and your most recent 401(k) statement showing the vested balance. Those three documents answer 90% of what any professional — or the IRS — will ask.

- Get a free case review. Interest and the monthly late-pay penalty are accruing on the balance every day it sits, whether or not any levy is near. Call (888) 825-7779 or use the 2-minute form, and an experienced tax professional will map your exact exposure and the cheapest way out — or, if you'd rather pay directly, start at IRS.gov/payments today.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.