IRS Collections

Can the IRS Take My Spouse's Bank Account? (2026 Rules)

The short answer: Can the IRS take my spouse's bank account? Usually not — if the debt is yours alone, an account owned solely by your spouse is out of reach. But the IRS can levy joint accounts in full, reach community-property funds in nine states, and pursue money you moved to hide it.

The debt is yours — maybe several years of 1099 income with nothing withheld — but the account you're actually worried about isn't. Your spouse's paycheck lands there. The mortgage comes out of there. They never signed up for any of this. The good news: the law draws real lines around whose money the IRS can touch, and once you know where those lines sit, you can keep the safe accounts safe while you fix the debt itself.

Everything comes down to two questions: whose name is on the tax debt, and whose name is on the account. The exposure table below maps every combination — spouse-only accounts, joint accounts, community property, wages, and refunds — so you can see your family's actual risk at a glance. The image below shows how the pieces fit together visually.

⏱ The clocks that matter: if an LT11 or Letter 1058 has arrived, you have 30 days to request a Collection Due Process hearing before the IRS can levy. If a bank levy has already hit an account, the bank must hold the funds for 21 days before sending them to the IRS — that hold is your spouse's window to prove which money is theirs.

Whose debt is it? The question that decides everything

The IRS can only levy property that legally belongs to the person who owes the tax — and a joint tax return makes both spouses owe 100% of the balance. That rule is called joint and several liability, and it doesn't split the debt in half; each signer owes all of it, and the IRS collects from whichever spouse is easier to reach.

So check the notice or your account transcript first. If the balance comes from a jointly filed return, this article's question mostly answers itself: your spouse is a debtor too, and their accounts and wages are fair game everywhere.

If the debt is separate — self-employment tax from years you filed alone, a balance assessed before the marriage, or years you filed married-filing-separately — then your spouse is not liable, and the question becomes which accounts the IRS can characterize as yours. A spouse who signed a joint return but was deceived about the income may also have a path out of the liability itself through innocent spouse relief (Form 8857).

When can the IRS take my spouse's bank account? The three real risk zones

Three situations put your spouse's money within IRS reach even when the debt is only yours: a joint account, a community property state, or a transfer the IRS treats as a shield.

1. Joint accounts: the biggest surprise

If your name is on an account, the IRS can levy it — up to the entire balance on the day the levy lands — even if 95% of the deposits came from your spouse. Courts have long allowed the IRS to levy any account the taxpayer has the legal right to withdraw from. The non-liable spouse isn't helpless: during the 21-day hold they can document which deposits are theirs and ask for that share back, and after funds leave, a formal wrongful levy claim can recover money that never belonged to the taxpayer. But recovering money is far harder than never losing it. The same logic applies when your name sits on an aging parent's account — see joint bank accounts with family and IRS levies.

2. Community property states: nine exceptions to "their money is safe"

In Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin, most income earned by either spouse during the marriage is community property — owned by both of you. Because you own an interest in community funds, the IRS may reach them for your separate debt, including a portion of your spouse's wages and the account those wages sit in. State law carve-outs vary, and this is one of the few areas where the answer genuinely turns on which state you live in. If you're in a community property state, get specific advice before assuming any marital account is protected; community property tax relief under IRC §66 exists for spouses caught by these rules. You can estimate what a levy could reach from a paycheck with our IRS Wage Garnishment Calculator.

3. Transfers the IRS treats as hiding money

Depositing your contractor income into an account titled in your spouse's name doesn't protect it — it converts a safe account into a target. The IRS can pursue funds under nominee and transferee theories: if the money is yours in substance, the title on the account doesn't control. Worse, the transfer itself undermines every negotiation that follows. An Offer in Compromise examiner who finds income routed through a spouse's account will add it back to your ability to pay, and may treat it as a dissipated asset.

| Account or asset | Reachable for your separate debt? | What protects your spouse |

|---|---|---|

| Spouse's solely-owned account (separate-property state, their own income) | No — generally out of reach | Clean titling; never deposit your funds into it |

| Joint account (both names) | Yes — up to the full balance on levy day | 21-day hold + proof of whose deposits; wrongful levy claim after |

| Spouse's account in a community property state | Often yes — community funds are reachable | State-law exemptions vary; get state-specific advice |

| Spouse's wages | No in separate-property states; a community share may be reachable in the nine CP states | Separate liability + state property law |

| Joint tax refund | Yes — the IRS offsets the whole refund | Form 8379 Injured Spouse Allocation recovers their share |

| Money you moved into your spouse's name to shield it | Yes — nominee/transferee pursuit | Nothing; the transfer makes everything worse |

Two related protections deserve a sentence each. Filing married filing separately when your spouse owes the IRS keeps future liabilities from becoming joint — at the cost of some tax benefits. And when a joint refund is taken for one spouse's old debt, injured spouse Form 8379 gets the non-liable spouse's share back.

What happens if you ignore the debt

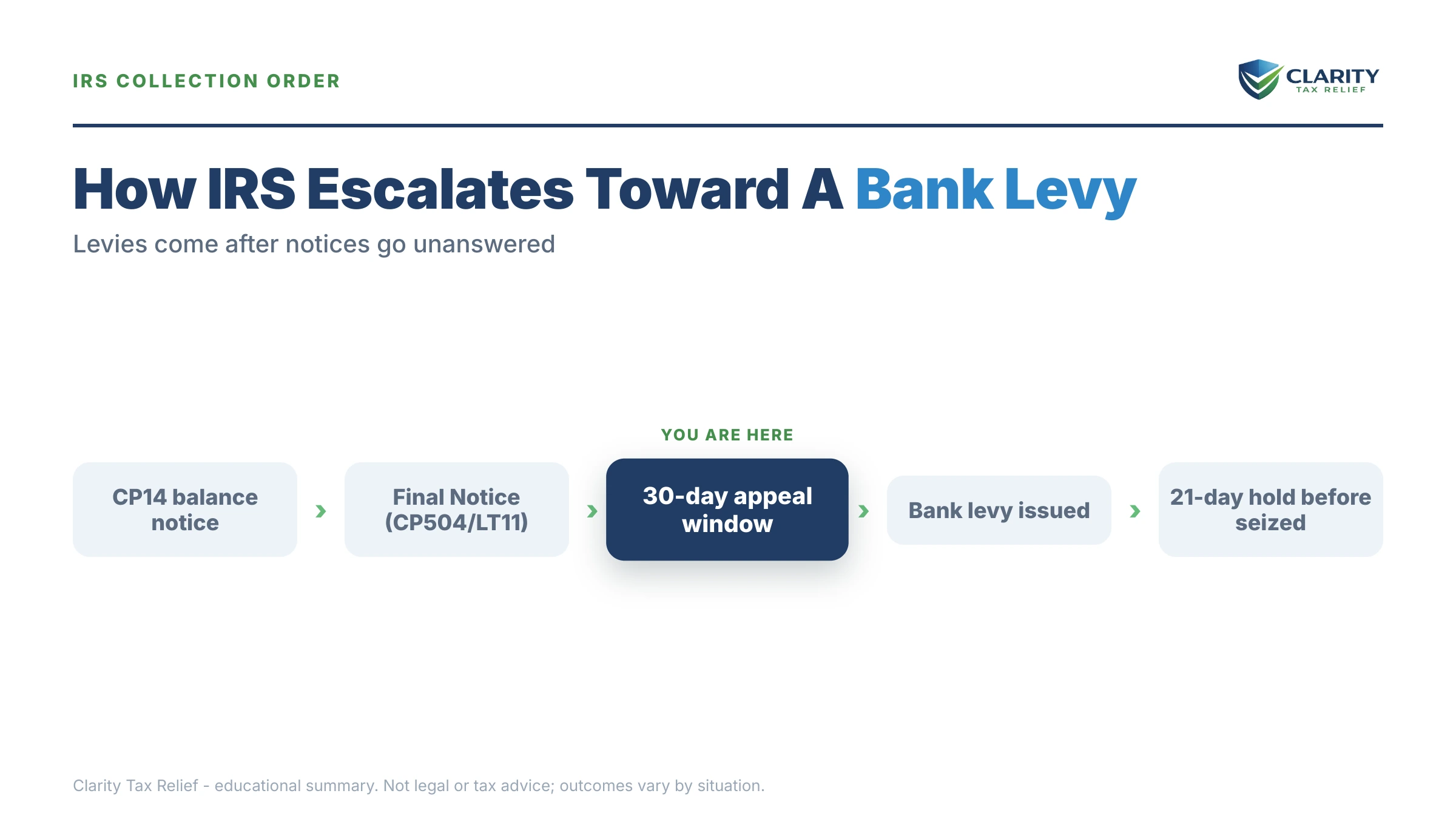

A bank levy is the last step in an automated notice sequence, and the final notice in that sequence starts a fixed 30-day clock. Nothing about being married slows the machine down — but each stage tells you how much room you have left:

- CP14, then CP501/CP503 — bills and reminders. No enforcement yet; penalties and interest compound monthly while they arrive.

- CP504 — Notice of Intent to Levy under IRC §6331(d). The IRS can now seize your state tax refund. It is not yet authorized to levy bank accounts or wages.

- LT11 or Letter 1058 — Final Notice of Intent to Levy. This starts your 30-day window to request a Collection Due Process hearing on Form 12153. Miss it, and levies become legal.

- Bank levy — the IRS sends a levy to banks where your SSN appears: joint accounts included. The bank freezes the balance and holds it 21 days before remitting (the full mechanics are in our guide to the IRS bank levy and the 21-day rule).

- Continuing enforcement — a bank levy is one-time, so the IRS repeats it, adds wage or 1099 levies, and may file a federal tax lien that attaches to jointly owned property.

How does the IRS find accounts in the first place? Through your own paper trail: 1099-INT forms banks file under your SSN, the account your refunds were deposited to, and checks you've written to the Treasury. That's the practical reason spouse-only accounts rarely get levied for separate debt — they report under a different SSN — and the practical reason joint accounts always show up.

In 2026 there's a twist worth knowing: the IRS workforce shrank roughly 27% in 2025, so reaching a human to fix an erroneous levy is harder than it has ever been. The levies themselves are issued by automated systems that never stopped. Prevention is now dramatically cheaper than cure.

Worried a levy will hit the account your family lives out of?

If an LT11 or Letter 1058 is on your table, the 30-day Collection Due Process window is the clock that matters. Get your notices and account structure reviewed free — an experienced tax professional will map exactly which accounts are exposed and how to protect the rest before a levy is authorized.

Your options: resolve the debt and the levy risk disappears

Every resolution that puts your account in good standing also takes your spouse's money out of the crossfire — the IRS doesn't levy taxpayers who are in an active agreement. The full DIY playbook lives in our guide to how to settle tax debt yourself; here's how each option lines up against a debt in the $76,400 range:

| Option | Who qualifies | Setup cost | Timeline & notes |

|---|---|---|---|

| Short-term payment plan | Can full-pay within 180 days | $0 | Immediate; interest and penalties still accrue |

| Streamlined installment agreement | Balance ≤ $50,000 | Online setup fee (reduced with direct debit) | Up to 72 months, set up online, no financial disclosure |

| Non-streamlined installment agreement | Balance over $50,000 | Setup fee + Form 433-F financials | Weeks to negotiate; payment based on ability to pay |

| Currently Not Collectible | Paying anything would create genuine hardship | $0 (financial disclosure required) | Pauses levies; debt remains and interest accrues |

| Offer in Compromise | Assets + future income genuinely can't cover the debt | $205 fee + 20% down on lump-sum offers (waived with low-income certification) | Months to years; roughly 1 in 5 offers accepted in FY2024 |

| Penalty relief (FTA / AEP) | Clean compliance the prior 3 years; AEP becomes automatic starting summer 2026 | $0 | Reduces the balance itself, not just the payment |

A worked example: $76,400 in 1099 debt, one non-liable spouse

Say you're a 1099 contractor who owes $76,400 across three self-employed years you filed alone, and your spouse has a W-2 job with their paycheck going to an account in their name only. This is hypothetical, but the math is real:

- Your spouse's account: in a separate-property state, it's generally out of reach — as long as you never route your contractor deposits through it. In a community property state, their earnings during the marriage may be reachable; get state-specific advice before relying on the account.

- Your joint household account: fully levyable. If a levy hits while $9,000 sits there for the mortgage, the whole $9,000 freezes for 21 days.

- The plan math: $76,400 is above the $50,000 streamlined line, so an online 72-month agreement isn't available as-is. Pay it down by $26,401 to $49,999 and you can set up a streamlined plan at roughly $49,999 ÷ 72 ≈ $695/month before accruing interest and the 0.5%/month failure-to-pay penalty. Can't pay it down? A non-streamlined agreement on the full $76,400 requires Form 433-F financials, with the payment set by your actual ability to pay.

- The passport problem: $76,400 sits above the 2026 seriously-delinquent threshold of $66,000, so certification and a CP508C notice are on the table — a real issue if your contracting work involves travel. See passport revoked for tax debt.

- The OIC question: if your income is irregular and your assets are thin, an Offer in Compromise may be worth pricing out — the IRS looks only at what it could realistically collect, never at what you "deserve" to pay. Acceptance is means-tested and far from automatic.

How to respond, step by step

- Confirm whose debt it is — pull your IRS notice or account transcript and check whether the balance comes from a joint return (both spouses owe all of it) or your separate filing (only you owe it).

- Map every account by title — list your accounts, your spouse's solely-owned accounts, and every joint account — and note whether you live in one of the nine community property states.

- Answer the live notice on time — if you are holding an LT11 or Letter 1058, file Form 12153 within 30 days to request a Collection Due Process hearing and pause the levy.

- Stop commingling funds — route your spouse's income into an account titled in their name only, and do not deposit your money into it — clean titling is what keeps their funds out of reach.

- Set up a resolution before the IRS levies — choose a payment plan, Currently Not Collectible status, or an Offer in Compromise — any active resolution takes joint accounts out of the crossfire.

- If a levy already hit, use the 21-day hold — contact the IRS before the bank releases the funds, with proof of your spouse's ownership of the deposits or documentation of economic hardship.

When you can handle this yourself

Plenty of these situations don't need professional help. If your debt is under $50,000, your spouse's money is in a clearly separate account in a separate-property state, and no final notice has arrived, you can set up a streamlined installment agreement online in an afternoon and the levy risk evaporates. Same if you can full-pay within 180 days — the short-term plan is free to set up.

Experienced help changes outcomes in four situations: a levy has already frozen a joint account and the 21-day hold is running; you live in a community property state and the "whose money is it" question has no obvious answer; the debt exceeds $50,000 (financial disclosure, passport exposure, and negotiation leverage all come into play); or your spouse may qualify to escape a joint liability entirely through innocent spouse relief. In those cases, the order and framing of what you submit genuinely changes what your family keeps.

Terms on this page, decoded

- Levy vs. lien: a levy takes property (money from an account); a lien is a legal claim recorded against property you own, including jointly owned property.

- Joint and several liability: when spouses file jointly, each one owes the entire balance — not half.

- Community property: in nine states, most income earned by either spouse during the marriage belongs to both — which is what lets the IRS reach a non-liable spouse's earnings there.

- Nominee levy: an IRS action against property titled in someone else's name (like a spouse) when the money is really the taxpayer's.

- Wrongful levy claim: the formal process a non-liable person uses to recover their own money taken by a levy aimed at someone else.

- Collection Due Process (CDP): the appeal right that comes with a final levy notice — requested on Form 12153 within 30 days, it pauses levies while your case is heard.

Spouse and IRS levy questions, answered

Can the IRS levy a joint bank account for only one spouse's debt?

Yes. If your name is on the account, the IRS can levy it — up to the entire balance on the day the levy hits, even if most of the money came from your spouse. The bank must hold the funds for 21 days before sending them, and during that window your spouse can present proof (deposit records, pay stubs) that specific funds are theirs and ask that their share be released.

Can the IRS take my spouse's bank account if we file separately?

Filing separately keeps your spouse off the liability for your return, so an account in their name only is generally out of the IRS's reach. Two exceptions remain: any joint account still carries your name and can be levied, and in the nine community property states the IRS may reach community funds — including a portion of your spouse's earnings — even for your separate debt.

Can the IRS take my spouse's wages for my tax debt?

Not in the 41 separate-property states, if the debt is yours alone — a wage levy attaches to the taxpayer named on the assessment, and your spouse is not that person. In community property states (Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, Wisconsin), earnings during the marriage are generally community property, so the IRS may be able to reach a share of your spouse's paycheck. If the debt comes from a joint return, both spouses owe it and both incomes are exposed everywhere.

Is my spouse responsible for tax debt I had before we married?

No. A tax debt assessed before your marriage belongs to you alone, and marrying does not transfer it. Their separate income and separate accounts stay out of reach in separate-property states. The two practical exposures are a joint refund — the IRS will offset all of it unless your spouse files Form 8379 — and community property rules in the nine states that have them.

Can I protect money by moving it into my spouse's account?

No — and it usually backfires. If you deposit your income into an account titled in your spouse's name to keep it from the IRS, the agency can pursue those funds under nominee and transferee theories, treating the account as yours in substance. It also damages your credibility in any payment plan, hardship, or Offer in Compromise negotiation. Keep your money in your name and resolve the debt instead.

How does the IRS know which bank accounts to levy?

Mostly through your own paper trail: 1099-INT and 1099-DIV forms banks file under your Social Security number, the account you used for refunds or past payments, and checks you have written to the IRS. A joint account shows up because your SSN is attached to it. An account solely in your spouse's name reports under their SSN, which is the practical reason the IRS does not typically levy it for your separate debt.

What is the 21-day rule when the IRS levies a bank account?

When a levy hits, the bank freezes the funds but must hold them for 21 days before sending them to the IRS. That window exists so ownership disputes and hardship claims can be raised — it is when a non-liable spouse proves which deposits are theirs. A bank levy is also one-time: it captures only what was in the account on levy day, not future deposits.

Will the IRS take our joint tax refund for my separate debt?

Yes — the IRS will apply the entire joint refund to your balance unless your spouse claims their share. They do that with Form 8379, Injured Spouse Allocation, which allocates the refund between you based on each spouse's income, withholding, and payments. It can be filed with the return or on its own after the offset, and community property rules change how the split is calculated in those nine states.

Your next 24 hours

- Find the liability line on your notice. Check whose name(s) and SSN appear and which tax years are listed — that one glance tells you whether the debt is joint or yours alone, which decides everything above.

- Gather three things: your most recent IRS notices, your last filed return for each year with a balance, and bank statements showing whose deposits fund each account — especially any joint account.

- Get a free case review. Call (888) 825-7779 or use the 2-minute form. If a final notice has arrived, the 30-day CDP window is running; even if it hasn't, interest and the 0.5%/month late-payment penalty are compounding while the account structure stays exposed.

The IRS's own references are worth bookmarking: the IRS payment plans and installment agreements page for setting up an agreement, IRS.gov/payments for every way to pay, and the Taxpayer Advocate Service if a levy is causing hardship and you can't get a human on the line.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.