IRS Levies & Collections

IRS Bank Levy & the 21-Day Rule: How to Get Your Money Back (2026)

The short answer: an IRS bank levy freezes the money in your account on the day it hits — but your bank must hold those funds for 21 days before sending them to the IRS. That 21-day window is your one chance to get the levy released and keep the money before it's gone for good.

You checked your balance and it was frozen, or a payment bounced you never expected to bounce. The panic is real — but with an IRS bank levy, the money hasn't actually left yet. Federal law forces your bank to sit on it for 21 days first, and almost everything that matters happens inside that window.

This is the single fact that separates people who recover their money from people who lose it: the levy is a one-time snapshot, not a permanent drain, and the clock is short. The image below shows what a levy notice looks like and where to find the date that starts your countdown.

Understand this and you can act instead of freeze. Miss it, and on day 22 your bank ships the money to the IRS, where getting it back becomes a slow, uphill fight.

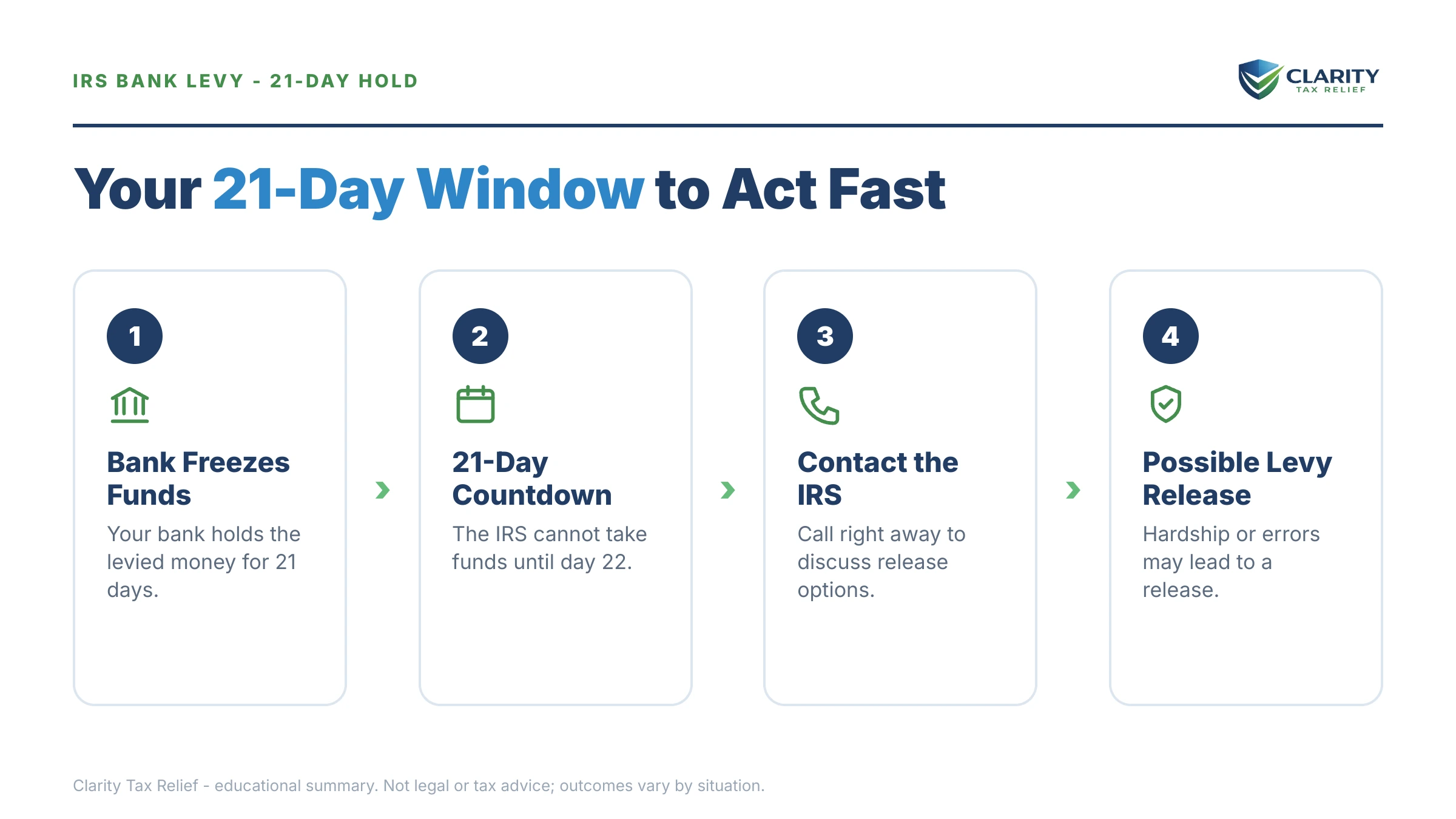

⏱ Your deadline: the bank holds the levied funds for exactly 21 calendar days from the day the levy attached. On day 22 the money is remitted to the IRS. To keep it, the IRS must send your bank a written release before day 21 ends — so treat this as a one-to-two-week window, not three.

Why the IRS bank levy 21-day rule exists

The 21-day hold is written into federal law specifically to give you time to fix a levy before the money is lost. When the IRS serves a levy on your bank, the bank immediately freezes your balance up to what you owe — but it cannot hand the money over right away. It must wait 21 calendar days.

That pause exists for two reasons: so you can prove the levy was wrong or duplicative, and so you can arrange a release if the levy shouldn't stand. It is the same protection that lets the IRS undo an over-collection or a mistaken freeze before real damage is done.

Two features of a bank levy make the 21-day rule so important. First, a bank levy is a one-time capture — it only reaches the balance sitting in the account on the day the levy hits, not future deposits. Second, unlike a wage levy, there is no automatically protected amount; the levy can take the entire balance up to your total debt. That's why understanding the difference between a one-time bank levy and a continuous wage levy changes your whole strategy — our guide on how to stop an IRS wage garnishment covers the continuous side in depth.

Why you got the levy in the first place

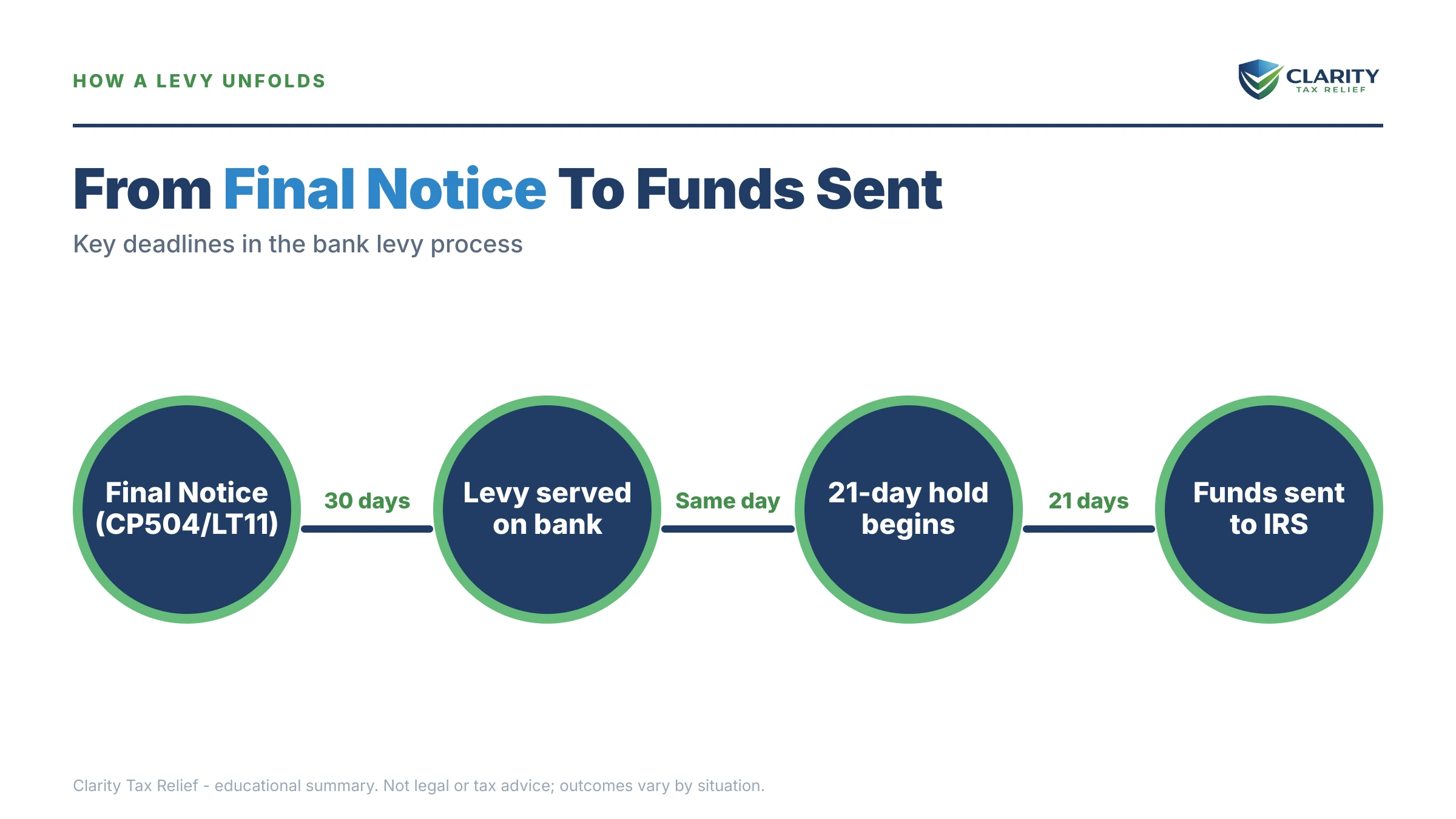

A bank levy almost never comes out of nowhere — it's the last step in a long collection sequence you were mailed warnings about. The IRS is required to send a series of notices before it can seize funds, and the levy only lands after those notices are ignored or missed.

The trigger is a Final Notice of Intent to Levy — an LT11 notice or Letter 1058 — mailed at least 30 days before any levy. That final notice also carries your Collection Due Process rights. Before it, you'd have received a CP504 notice (intent to levy your state refund) and earlier balance-due reminders.

Many people who feel "ambushed" simply never opened the final notice, or it went to an old address. If you genuinely never got one, that matters — it can be grounds to challenge the levy. The one true exception is a jeopardy levy, where the IRS believes collection is at risk and can skip the normal 30-day notice.

If you're asking whether the IRS can freeze an account with no warning at all, we break that down in can the IRS freeze my bank account without notice.

What happens if you do nothing during the 21 days

If you let the 21-day hold run out, the frozen money leaves your account and the IRS keeps escalating. The sequence after a bank levy is automated and unforgiving of delay:

- Day 1 — levy attaches. Your bank freezes the balance up to what you owe. You can still see the money, but you can't touch it.

- Days 2–20 — the hold. Nothing moves. This is your entire window to file returns, arrange a plan, or prove hardship and get a written release.

- Day 22 — funds remitted. If no release reached your bank, it sends the frozen money to the IRS and applies it to your debt.

- Weeks later — the next levy. Because a bank levy is one-time, the IRS can issue a fresh levy to grab new deposits. Repeat levies continue until you're paid up or in an approved arrangement.

- Beyond the bank — other assets. The same authority reaches wages (a continuous garnishment), accounts receivable, and, for a business, its operating cash.

In 2026, this matters more than ever. IRS staffing was cut roughly 27% during 2025, but levies are issued by automated systems that never got laid off. The machine keeps seizing whether or not a human ever reviews your file — which is exactly why deadlines, not phone calls, drive outcomes right now.

Your bank is holding your money — but not for long

Get your levy reviewed free before the 21-day hold runs out. An experienced tax professional can tell you today whether a release is realistic and what the IRS will need. Call or send us the notice — no pressure, just a straight answer.

The 21-day levy timeline, day by day

The whole game is racing the release to your bank before day 21 ends. Here is what the window actually looks like and what you lose at each stage.

| Stage | What's happening | What you can still do |

|---|---|---|

| Levy day (Day 1) | Bank freezes your balance up to the debt; funds untouchable | Confirm the exact date and amount frozen; start filing any missing returns |

| Days 2–14 | 21-day hold running; money still in your account | Best time to arrange a plan, prove hardship, or dispute — most releases happen here |

| Days 15–20 | Hold nearly over; release must reach the bank in time | Push for a same-day faxed release (Form 668-D); escalate to a manager or Taxpayer Advocate |

| Day 22 | Bank remits frozen funds to the IRS | Release window closed; recovery now needs a wrongful-levy claim or refund request |

| After remittance | IRS can issue a fresh levy on new deposits | Only a formal agreement or hardship status stops repeat levies |

How to get an IRS bank levy released before day 21

The IRS will release a bank levy when you remove the reason it was issued — and it can send the release to your bank the same day. There are four realistic paths, and the right one depends on your finances:

- Pay the balance — full payment triggers an immediate release. Rare when a levy already hit, but if the account holds more than the debt, paying frees the rest.

- Enter an installment agreement — agreeing to a monthly payment plan is the most common release path for people who can't pay in full but have steady income.

- Prove economic hardship — under IRC §6343, the IRS must release a levy that leaves you unable to pay basic living expenses. This is often the fastest route; see levy causing hardship and Currently Not Collectible status.

- Challenge a wrongful or premature levy — if you never got the final notice, the money isn't yours, or the debt is wrong, you can fight it. See wrongful levy and how to get an IRS levy released.

Whichever path you choose, the release must physically reach your bank as a written Form 668-D before the hold ends — a verbal "we'll release it" does not free your money. And be aware: releasing this levy does not stop the next one. Without a resolution, the IRS can and does re-levy, as we cover in IRS levied me again.

I owe the IRS this much — what are my realistic options?

The best resolution to stop levies depends heavily on how much you owe. Here's how the options break down by balance — the same options that get a current levy released and prevent the next one.

| Amount owed | Most likely path | What it takes |

|---|---|---|

| Under $10,000 | Guaranteed or streamlined installment agreement | Usually approved with little financial disclosure; releases the levy quickly |

| $10,000–$25,000 | Streamlined installment agreement (up to 72 months) | Direct-debit setup often required; no full financial statement |

| $25,000–$50,000 | Streamlined plan with direct debit, or CNC / OIC if finances qualify | Direct debit mandatory; financials may be requested |

| Over $50,000 | Full financial review: IA, Currently Not Collectible, or Offer in Compromise | Form 433-A/F required; often needs professional help to release the levy fast |

| Any amount, genuine hardship | Economic-hardship levy release (§6343) + CNC status | Document that the levy prevents basic living expenses |

For the general mechanics of setting these up, our hub on how to stop an IRS wage garnishment walks through installment agreements, CNC, and hardship in detail — the same tools apply to a bank levy.

A worked example: $7,400 owed, three unfiled years

Say you drive for a couple of gig apps and haven't filed in three years. The IRS filed substitute returns for you, assessed roughly $7,400 in tax, penalties, and interest, and mailed a final notice to an old address. One Tuesday your checking account — holding $2,300 — is frozen by a bank levy.

Here's the math and the moves. The levy grabs the full $2,300 (there's no protected floor on a bank levy), and your bank starts the 21-day hold. You have about two weeks of usable time.

- Step one — file the three returns. Because your actual deductions (mileage, phone, fees) were never counted, your real liability may be well under $7,400. The IRS won't release a levy or approve a plan while returns are missing, so this comes first. See didn't track miles if your records are thin.

- Step two — argue hardship. If that $2,300 was your rent money, you request an economic-hardship release under §6343. If granted, the bank returns the frozen funds.

- Step three — set up a resolution. Once returns are filed and your true balance is known — say it drops to $4,100 — a streamlined installment agreement at roughly $60–$120 a month, or Currently Not Collectible status if your income is low, stops the next levy.

Note that penalties and interest keep accruing until the balance is cleared or you're in an accepted arrangement — the failure-to-file penalty alone runs 5% per month, ten times the failure-to-pay penalty, though in any month both penalties apply the failure-to-file portion is reduced to 4.5% so the combined charge stays at 5% per month — which is exactly why filing those returns is the highest-value move in the first 48 hours.

How to respond, step by step

- Confirm the levy and pin down day 21. Call your bank to confirm the date the levy attached and the amount frozen; count 21 days forward — that's the day the money leaves.

- File any unfiled returns immediately. The IRS won't release a levy or approve a resolution with missing returns; this is usually the biggest bottleneck.

- Call the number on your levy notice. Ask what the IRS needs to release the levy and what resolution it will accept. Have a professional make the call if you have multiple years or hardship.

- Propose a resolution the IRS accepts. Offer an installment agreement, CNC status, or an economic-hardship release under §6343.

- Get the release in writing before day 21. Ask the IRS to fax Form 668-D (release of levy) to your bank before the hold ends — a verbal agreement won't return your money.

When you can handle this yourself — and when help changes the outcome

You can often handle a bank levy alone if the facts are simple. If you owe under $25,000, all your returns are filed, and you have steady income, you can usually call the IRS, agree to a streamlined installment agreement, and get the levy released in a few days without paying anyone. Setting up a plan is genuinely straightforward at that level.

Experienced help changes the outcome when the clock is short and the facts are messy: you have unfiled returns (the number-one release bottleneck), multiple years, a business or payroll debt, a joint account where part of the money isn't yours, or a hardship you need documented fast. In those cases the difference between reaching the right IRS unit on day 5 versus day 18 is the difference between keeping your money and losing it. It's also the moment to be honest about scams — no legitimate firm promises to "settle for pennies on the dollar" or "wipe out" a levy; a real professional tells you what's actually achievable given your numbers.

If your levy hit a business bank account, involves accounts receivable, or reaches commission income, the stakes and rules shift — and professional timing matters even more. Get a free levy review while the 21-day hold is still running.

Terms on your levy, decoded

- Levy vs. lien: a levy actually takes your money or property; a lien is only a legal claim against it. The difference between an IRS lien and levy matters for what's at risk right now.

- 21-day hold: the mandatory waiting period a bank must observe before sending levied funds to the IRS — your entire window to act.

- Form 668-A vs. 668-W: 668-A is the one-time bank levy; 668-W is the continuous wage levy. A bank levy is a snapshot; a wage levy repeats every payday.

- Form 668-D: the release of levy — the document the IRS sends your bank to unfreeze the money.

- CDP rights: Collection Due Process — your right to appeal a levy, requested with Form 12153 after a final notice.

- Economic hardship release: the §6343 requirement that the IRS release a levy leaving you unable to pay basic living costs.

If the frozen money was actually shared with a spouse, parent, or partner, read joint account with parent IRS levy before day 21 — the recovery process is different, and faster if raised early. You can also estimate what the IRS could reach from your income with our wage garnishment calculator if a continuous levy is your bigger worry.

Bank levy questions, answered

How long does an IRS bank levy last?

A bank levy is a one-time snapshot, not a continuous grab — it only captures the money in your account on the day it hits. Your bank then freezes that money and holds it for 21 days before sending it to the IRS. New deposits after the levy date are not affected, but the IRS can issue a fresh levy at any time to catch them.

How many days does the bank hold funds after an IRS levy?

Your bank must hold the frozen funds for exactly 21 calendar days before releasing them to the IRS. That waiting period exists so you have time to resolve a dispute or arrange a release. On day 22, if nothing has changed, the bank sends the money — so the 21-day window is the whole ballgame.

Can I get my money back after an IRS bank levy?

Yes, if you act inside the 21-day hold — the IRS can send your bank a release (Form 668-D) and the frozen money stays in your account. You get a release by entering a payment plan, proving hardship, or showing the levy was wrongful. Once the 21 days pass and the funds transfer, recovering them is far harder and usually requires a wrongful-levy claim or a refund request.

Can the IRS levy my bank account without warning?

Usually no — the IRS must first send a Final Notice of Intent to Levy (LT11 or Letter 1058) and give you 30 days to request a Collection Due Process hearing. The exception is a jeopardy levy, used when the IRS believes collection is at risk, which can skip the 30-day notice. Many people are "surprised" only because they missed or ignored the final notice mailed weeks earlier.

Does the IRS take everything in my bank account?

A bank levy captures the balance in the account up to the amount you owe, including penalties and interest — there is no automatic protected amount like there is with a wage levy. If you owe $7,400 and have $2,300 in the account, the levy grabs the $2,300. If you have $15,000 in the account, it grabs $7,400 plus additions and leaves the rest.

Can the IRS levy my bank account twice?

Yes. A bank levy is a one-time event, so the IRS often issues repeated levies to catch new deposits until the debt is paid or you are in an approved arrangement. Even after a levy is released, the IRS can levy the same account again if your resolution defaults or you never set one up. The only reliable way to stop repeat levies is a formal agreement or hardship status.

Will the IRS levy a joint bank account?

Yes — the IRS can levy a joint account even if only one owner owes the tax, because either owner generally has full access to the funds. The non-liable co-owner can file a claim to recover their share, but they must prove the money was theirs. This catches spouses, adult children on a parent's account, and business partners off guard.

What if the IRS bank levy causes financial hardship?

If the levy takes money you need for rent, utilities, food, or medicine, the IRS must release it under IRC Section 6343 once you show the hardship. Call the number on your levy notice, explain the specific bills you cannot pay, and be ready to document them. Economic-hardship releases are one of the fastest ways to free frozen funds inside the 21-day window.

Can the IRS take money that isn't mine from my account?

If the frozen funds belong to someone else — a client's deposit, a tax refund not yet yours, or a co-owner's money — you can file a wrongful-levy claim to get them back. Certain federal benefits like some Social Security and VA payments also carry protections. Raise it fast: proving the money was not yours is far easier before the 21-day hold ends and the funds leave.

How fast can I get an IRS bank levy released?

A release can happen the same day if you reach the right IRS unit and either pay, agree to a plan, or prove hardship — the IRS then faxes a release directly to your bank. In practice it takes a few days, which is why you cannot wait until day 20. Unfiled returns are the most common delay, so file them first.

Your next 24 hours

- Find the levy date. Call your bank or check your alerts for the exact day the funds were frozen, then count 21 days forward. That single date drives everything.

- Gather your paperwork. Pull the levy notice, your most recent return, a list of any unfiled years, and proof of the bills the frozen money was meant to cover.

- Get a free case review. Call (888) 825-7779 or use the 2-minute form today — the 21-day hold does not pause while you decide, and a release has to reach your bank before it ends.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.