IRS Collections

IRS Lien vs Levy: What's the Difference and Which Is Worse? (2026)

IRS lien vs levy, in one line: a lien is the IRS's legal claim against everything you own — it takes nothing by itself. A levy is the actual seizure: your bank account, wages, or up to 15% of Social Security. Before most levies, the IRS must send a final notice and wait 30 days.

You've heard both words — maybe one was on a letter, maybe someone at the bank mentioned a "federal tax lien" during your refinance, maybe a notice warned of "intent to levy." They sound interchangeable. They are not, and the difference decides whether money leaves your account or a filing sits quietly against your house. One more thing most pages skip: if you owe unpaid tax, a lien already exists by law — even if the IRS never filed anything publicly.

Lien and levy paperwork looks confusingly similar at first glance — the image below shows exactly what these documents look like and where to find the notice number that tells you which one you're actually holding.

⏱ The clock that matters: you have 30 days from the date on an LT11 or Letter 1058 final notice before the IRS can begin seizing wages, bank accounts, or Social Security. A lien-filing notice (Letter 3172) also opens an appeal window — the exact deadline is printed on the letter itself.

IRS lien vs levy: the difference in one minute

A federal tax lien is the government's legal claim against everything you own; an IRS levy is the actual taking of money or property to pay the debt. The lien secures the debt. The levy collects it. A lien can sit for years without costing you a dollar directly — a levy empties an account or shrinks a check the month it lands.

| Question | Federal tax lien | IRS levy |

|---|---|---|

| What is it? | A legal claim securing the debt against all your property — home, vehicles, accounts, future assets | An actual seizure of specific property: bank funds, wages, federal payments |

| Does money leave your hands? | No — nothing is taken by the lien itself | Yes — funds are frozen or redirected to the IRS |

| Warning required? | Arises automatically by law after assessment and nonpayment; public filing announced by Letter 3172 | Final notice (LT11/Letter 1058) plus a 30-day wait, with narrow exceptions |

| Public record? | Yes, once a Notice of Federal Tax Lien is filed at the county | No public filing — but your bank or payer receives the order |

| How it ends | Release after full payment or CSED expiration; withdrawal, discharge, or subordination in specific cases | Release when you pay, get into a resolution, prove hardship, or win an appeal |

One more distinction trips people up: what most people call "garnishment" of a paycheck is legally an IRS wage levy — the mechanics of stopping one live in our guide to how to stop IRS wage garnishment.

Why you're facing a lien, a levy — or both

Every lien and every levy starts the same way: the IRS assessed a tax, sent you a bill, and the balance went unpaid. From there the two split.

The lien needs no action at all. Under federal law, once the IRS assesses the tax, demands payment, and you don't pay, a "silent" statutory lien attaches automatically to everything you own. Millions of people have one and don't know it. What changes things is the public step: the IRS files a Notice of Federal Tax Lien at your county recorder and mails you Letter 3172. In practice, the IRS reserves most public lien filings for larger balances — often $10,000 and up — though it has the authority to file at any amount.

The levy, by contrast, requires the IRS to work through a notice sequence and give you a final warning first. That sequence — and the rights each notice carries — is where most people either save themselves or lose their best options.

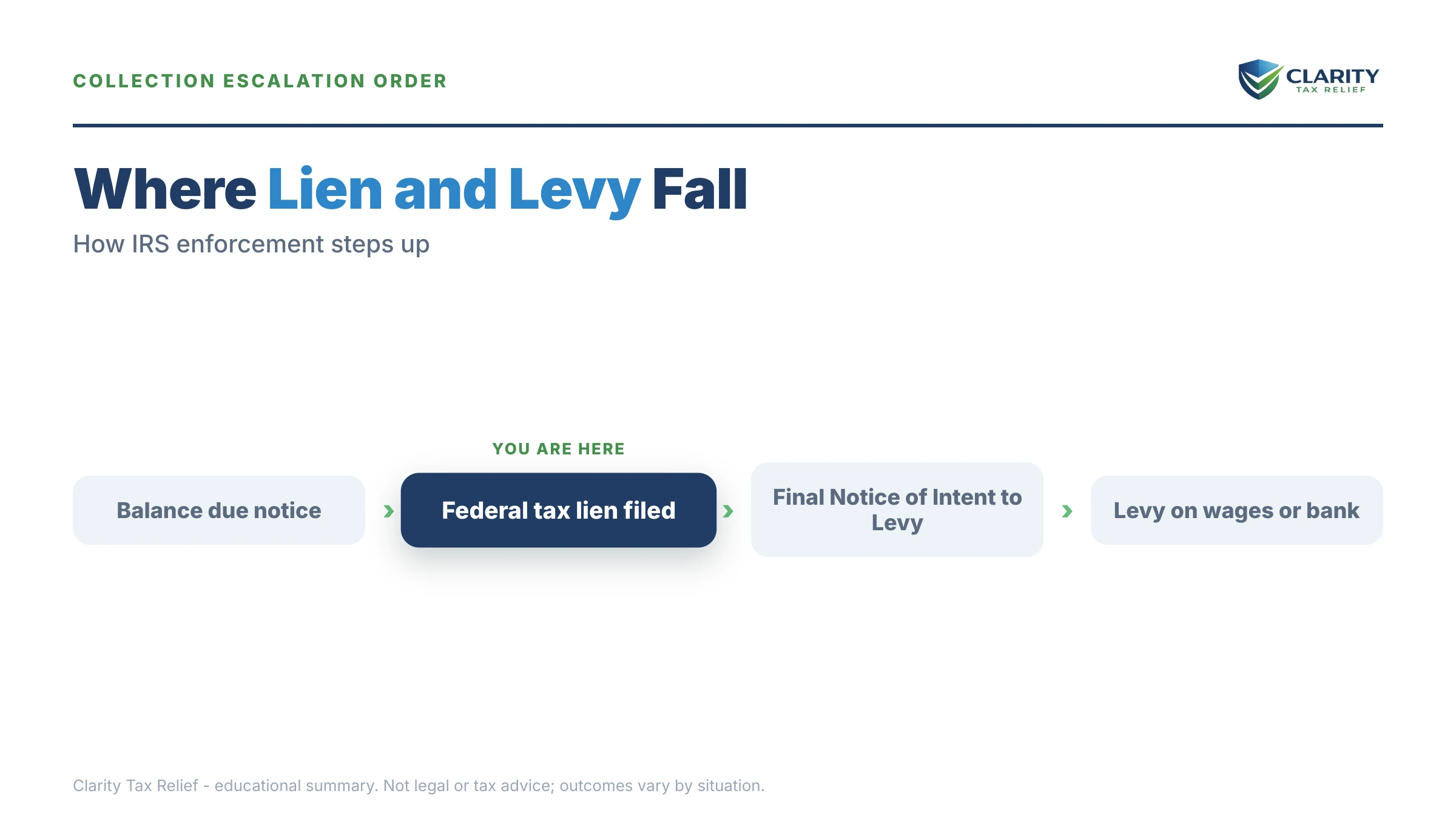

What happens if you ignore it: the road from lien to levy

The IRS collection machine moves from paper claim to actual seizure in a fixed, automated order. In 2026 that matters more than ever: the IRS workforce shrank roughly 27% in 2025, so reaching a human is harder — but the notices, lien filings, and levies are generated by systems that never got cut.

- First bill (CP14) — the balance is assessed and demanded, typically with about 21 days to pay. The moment it goes unpaid, the silent statutory lien attaches.

- Reminder notices (CP501/CP503) — still just bills, while interest and the 0.5%-per-month failure-to-pay penalty grow the balance.

- CP504 — Notice of Intent to Levy — the IRS can now seize your state tax refund. It cannot yet touch wages or bank accounts, but the public lien filing often happens around this stage.

- Letter 3172 — lien filed — the claim becomes public record, visible to title companies and lenders, and your window to appeal the filing opens.

- LT11 or Letter 1058 — Final Notice — the true tripwire. After 30 days, the IRS may levy — and you may request a Collection Due Process hearing before it can.

- Levy — a bank levy freezes funds with a 21-day hold before the money leaves; a wage levy is continuous until released; Social Security can lose up to 15% per check through the Federal Payment Levy Program.

Two exceptions skip the warning stages entirely: a jeopardy levy, used when the IRS believes collection is in immediate danger, and the automated seizure of your state refund after CP504.

| Notice | What it lets the IRS do | Your window and the right at stake |

|---|---|---|

| CP14 (first bill) | Nothing yet — but nonpayment triggers the silent lien | Typically about 21 days to pay or arrange a plan before escalation |

| CP504 | Seize your state tax refund | Pay or resolve by the printed date; a CAP appeal is available |

| Letter 3172 (lien filed) | The claim is now public record | Appeal window printed on the letter — request a hearing to contest the filing |

| LT11 / Letter 1058 | Levy wages, bank accounts, and most property after 30 days | 30 days to request a Collection Due Process hearing on Form 12153 — miss it and you lose the pre-levy hearing and Tax Court path |

| CP91 | Levy up to 15% of Social Security via FPLP | Respond by the date printed on the notice to stop the benefit levy before it starts |

Holding a lien filing or a levy warning right now?

If an LT11 or Letter 1058 arrived, the 30-day Collection Due Process window is the strongest legal right you'll get in this entire process. Have an experienced tax professional review your notice free — before that window closes.

Your options: stopping a levy and dealing with a lien

Any resolution that addresses the underlying balance stops the escalation for both — the difference is in the cleanup afterward. Getting into an approved arrangement generally prevents new levies and is the main path to releasing an active one; the lien has its own separate exit doors.

| Option | Who typically qualifies | Effect on the lien | Effect on the levy |

|---|---|---|---|

| Pay in full | Anyone able to pay (short-term plans give up to 180 days, $0 setup) | Release required within 30 days of payoff; withdrawal can be requested | Levy released; no new levies |

| Guaranteed installment agreement | Individuals only, owing $10,000 or less in income tax (excluding penalties and interest), all returns filed, on-time filing and payment for the past 5 years with no installment agreement in that period, full payment within 3 years | Public lien filing generally avoided at this balance level | Prevents levy; supports release of an active one |

| Streamlined installment agreement | Owe $25,000 or less — or up to $50,000 with direct debit — over up to 72 months | Withdrawal may be available at $25,000 or less on direct debit after consecutive payments | Prevents levy; supports release |

| Currently Not Collectible | Paying anything would prevent basic living expenses (financial disclosure required) | Lien usually remains — and may still be filed — while collection pauses | Levies stop while CNC lasts |

| Offer in Compromise | Assets plus future income genuinely can't cover the debt; roughly 1 in 5 offers were accepted in FY2024 | Lien released after the accepted offer is paid | Levies generally held while a processable offer is pending |

| CDP hearing (Form 12153) | Anyone within 30 days of a final levy notice, or within the window after a lien filing | Lets you contest the filing and propose alternatives | Levy action generally paused while a timely hearing is pending |

Lien-specific fixes. Beyond full release, three tools handle a lien that's blocking something specific: withdrawal (Form 12277) erases the public notice as if never filed; discharge (Form 14135) removes the lien from one property so a sale can close; subordination (Form 14134) moves the IRS behind a lender so a refinance can fund. None of these forgives the debt — they manage the claim while you resolve the balance.

Levy-specific fixes. An active levy can be released by full payment, an approved agreement, proof the levy creates economic hardship, or proof it was issued improperly. Timing differs by levy type: a bank levy comes with a built-in pause — see the IRS bank levy 21 days rule — while a wage or Social Security levy repeats every pay cycle until formally released. Bankruptcy's automatic stay also halts levy action while the case is open; whether that helps long-term depends on the debt, as our guide to does bankruptcy stop IRS levy explains.

Say you owe $6,200 and live on Social Security: the math both ways

Here's a hypothetical to make it concrete. Say you're retired, you owe $6,200 from a year when a pension withdrawal outran your withholding, and your Social Security check is $1,900 a month.

If you do nothing: the notices run their course, and the Federal Payment Levy Program eventually takes 15% of each check — $1,900 × 0.15 = $285 per month, automatically, until the balance plus growing penalties and interest is gone. If the IRS also levies the bank account where that check lands, the frozen funds sit on a 21-day hold before leaving. Whether your specific benefits are even reachable is covered in can the IRS garnish Social Security, and you can estimate what a levy would leave you with using our IRS Wage Garnishment Calculator.

If you act first: because your $6,200 income-tax balance (excluding penalties and interest) is under $10,000, you may qualify for a guaranteed installment agreement — it's available only to individuals who have filed all required returns and filed and paid on time for the past five years with no installment agreement in that period, and who can pay in full within three years. Full payment within three years means roughly $6,200 ÷ 36 ≈ $172 a month, while interest and the 0.5%-per-month late-payment penalty continue on the shrinking balance. At this balance level a public lien filing is unlikely, and no levy ever issues.

Same debt, two futures: $285 a month taken from you, or about $172 a month on your terms — and if even $172 would crowd out food, housing, or medicine, Currently Not Collectible status exists precisely for that, pausing collection entirely while the hardship lasts.

How to respond to an IRS lien or levy, step by step

- Identify the document. Find the notice number in the top corner: Letter 3172 means a lien was filed; CP504, LT11, or Letter 1058 means a levy is coming. The number tells you which clock is running.

- Verify the balance. Log into your IRS online account and confirm the amount, the tax years, and whether any payments are missing before you respond.

- Protect your appeal rights. If your final notice of intent to levy is less than 30 days old, file Form 12153 to request a Collection Due Process hearing — the IRS generally cannot levy while a timely hearing is pending.

- Get into a resolution. Set up a payment plan, request Currently Not Collectible status, or start an Offer in Compromise; any of these, in place before the deadline, prevents or releases most levies.

- Clean up the lien. After the debt is resolved, confirm the release and consider requesting withdrawal on Form 12277 so the public filing disappears from record searches.

When you can handle this yourself — and when help changes the outcome

If you're at the lien-warning stage with a balance under $10,000 you agree with, you likely don't need to pay anyone. Set up a payment plan online at IRS.gov, and no levy will ever issue; at that balance a public lien filing is unlikely too. The same goes for a first bill you can pay within 180 days — the short-term plan costs nothing to set up.

Experienced help earns its cost in specific situations: a levy already pulling money (release arguments and hardship documentation are technical and time-sensitive), a filed lien blocking a home sale or refinance that's under contract, multiple unfiled years that must be cleaned up before the IRS will approve anything, a Collection Due Process hearing where the record you build controls what a settlement officer can offer, or a jeopardy levy that skipped the normal warnings. In those cases, the order and paperwork of the fix change what you end up paying — and what you keep.

Terms on your notice, decoded

- Statutory (silent) lien — the claim that attaches automatically to all your property once assessed tax goes unpaid, with no public filing.

- Notice of Federal Tax Lien (NFTL) — the public county filing that announces the lien to lenders, title companies, and anyone who searches.

- Levy — the legal seizure of property or money; a wage "garnishment" is a levy applied to your paycheck.

- CDP (Collection Due Process) — your right to an independent Appeals hearing before a levy proceeds, requested on Form 12153 within 30 days of the final notice.

- CSED — the Collection Statute Expiration Date: 10 years from assessment, after which the debt, the lien, and levy authority generally end (with pauses for appeals, offers, and bankruptcy).

- FPLP — the Federal Payment Levy Program, the automated system that takes up to 15% of Social Security and other federal payments.

Lien vs levy questions, answered

Which is worse, an IRS lien or a levy?

A levy is worse in the short term because it takes money immediately — a lien takes nothing by itself. But a lien can quietly cost more over time: it attaches to your home and everything else you own, complicates selling or refinancing, and survives until the debt is resolved or the 10-year collection statute expires. The honest answer: a levy hurts today, a lien hurts every time you touch a major asset.

Can the IRS levy my bank account without warning?

Almost never. Before most levies, the IRS must send a final notice — LT11 or Letter 1058 — and wait 30 days so you can pay, arrange a plan, or request a Collection Due Process hearing. The narrow exceptions are jeopardy levies (when the IRS believes collection is at risk), levies on your state tax refund, and certain federal payment levies. If money left your account with no final notice on file, that itself may be grounds for a release.

Does an IRS tax lien show up on my credit report?

No — the three major consumer credit bureaus stopped reporting tax liens in 2018, so a Notice of Federal Tax Lien won't lower your credit score directly. It is still a public record, though: mortgage lenders, title companies, and some employers search public filings and will find it. That's why liens still derail home sales and refinances even without a credit-score hit.

Can the IRS levy Social Security benefits?

Yes. Through the Federal Payment Levy Program, the IRS can take up to 15% of each Social Security retirement or SSDI payment, and the levy continues automatically until the debt is resolved. You get warning first — typically a CP91 notice. SSI (Supplemental Security Income) is not subject to this levy. If losing 15% would leave you unable to cover basic living expenses, a hardship release or Currently Not Collectible status can stop it.

Can I have a lien and a levy at the same time?

Yes, and it's common in later-stage cases. The lien secures the IRS's claim against everything you own while a levy actively pulls money from a bank account, paycheck, or federal benefit. Resolving the account — through payment, a payment plan, hardship status, or an accepted offer — is what ends both; releasing a levy alone does not remove the lien.

How do I get an IRS lien removed after I pay?

The IRS must release a filed lien within 30 days of the debt being fully paid or becoming legally unenforceable — you'll receive a Certificate of Release. A release leaves the filing in the public record marked satisfied; a withdrawal, requested on Form 12277, removes the notice as if it were never filed. Withdrawal is worth requesting after full payment, and may be available earlier if you owe $25,000 or less on a direct-debit installment agreement.

Does a lien or levy expire after 10 years?

Generally, yes — the IRS has 10 years from assessment to collect (the CSED), and when that clock runs out the underlying lien self-releases and levy authority ends. But the clock pauses during bankruptcy, a pending Offer in Compromise, and Collection Due Process appeals, so many debts run longer than a calendar decade. Waiting out the statute while a levy is actively taking your money is rarely a workable plan.

Can the IRS take my house with a lien?

A lien attaches to your house but does not by itself force a sale. Actual seizure of a primary residence is a separate, rare process that requires court approval, and the IRS treats it as a last resort. The bigger practical problem is at closing: the lien must be paid, discharged, or subordinated before a sale or refinance can go through.

Your next 24 hours

- Find the notice number and the deadline. Top corner of the letter: 3172 means lien filed; CP504, LT11, or 1058 means levy ahead. Circle the response date printed on it — that date, not a guess, is your clock.

- Gather three things: the notice itself, your most recent tax return, and your income details (Social Security statement, pension, W-2s or 1099s). Every resolution starts with these.

- Get the notice reviewed free. If a final levy notice is running its 30-day window, don't let it close unanswered — call (888) 825-7779 or use the 2-minute form and an experienced tax professional will map your exact options. Even without a levy notice, interest and penalties are accruing monthly, so earlier is cheaper.

For the primary-source versions of everything above, see the IRS's own pages on understanding a federal tax lien and IRS payment options. If a levy is causing hardship and you can't get traction with the IRS, the independent Taxpayer Advocate Service can intervene.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.