IRS Collections

What Is an IRS Revenue Officer? How to Verify One — and Respond (2026)

What is an IRS revenue officer? A revenue officer is a civilian IRS field employee assigned to collect on the agency's most serious unpaid-tax and unfiled-return cases in person. Revenue officers can levy wages and bank accounts, file liens, and seize assets — but they cannot arrest you, and since 2023 they rarely show up unannounced.

Someone left a voicemail calling themselves "Officer," named a balance, and told you to call back today — and now you're trying to figure out whether the IRS really sends people after a debt like yours, or whether this is the scam everyone warns about. Both happen, and the difference is checkable in minutes. This guide shows you exactly who revenue officers are, who they aren't, and what to do in either case.

Real revenue officer contact follows a specific pattern in 2026 — a mailed appointment letter, two forms of federal ID, no demands for gift cards or wire transfers. The image below shows you exactly what legitimate revenue officer contact looks like and what to check before you say a word.

⏱ The real clock: a revenue officer's deadlines are set in writing — the appointment date on your Letter 725-B, or the response date in the officer's follow-up request, controls your case. Miss one and the usual next step is a summons or a levy, while penalties and interest keep accruing every month.

What is an IRS revenue officer — and what can one actually do?

An IRS revenue officer is a civilian field collection employee who works the agency's hardest unpaid-tax and unfiled-return cases one at a time, in person. Unlike the automated notice stream that handles most tax debt, a revenue officer is a human being with your file on their desk, a caseload measured in dozens rather than millions, and broad authority to close your case — cooperatively or not.

A revenue officer can:

- Interview you about your income, assets, and business, and require a full financial disclosure on Form 433-A.

- Set written deadlines for returns, documents, and payments — and enforce them.

- Issue a summons for your records, or your bank's and employer's, that is enforceable in federal court.

- Levy wages and bank accounts, file a Notice of Federal Tax Lien, and recommend seizure of property.

- Investigate who is personally responsible for a business's unpaid payroll taxes under the Trust Fund Recovery Penalty.

- Secure and process unfiled returns, or refer your account for a substitute return if you won't file.

What a revenue officer cannot do matters just as much: revenue officers are civil, not criminal — they carry no weapon, have no arrest power, and cannot threaten jail. They also cannot demand payment to anyone other than the United States Treasury, in any form other than normal IRS payment channels. Anyone who breaks either rule is not a revenue officer.

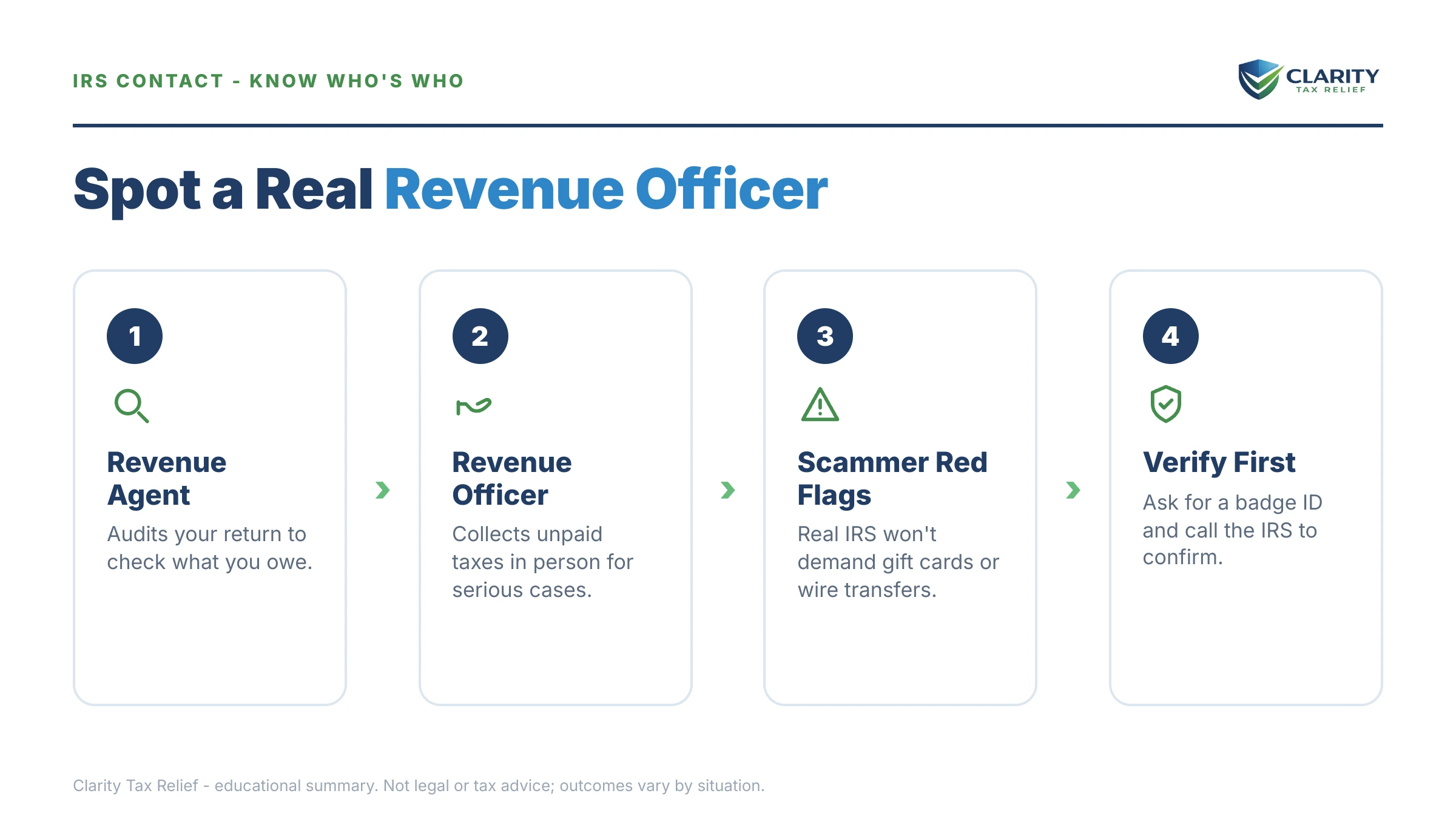

Revenue officer vs. revenue agent vs. special agent vs. scammer

A revenue officer collects tax that has already been assessed; a revenue agent audits returns to decide what you owe; a special agent investigates tax crimes. The title the person uses — and how they first reached you — tells you which situation you're in, and whether you're in one at all.

| Who contacted you | Their job | How genuine contact starts |

|---|---|---|

| Revenue officer (RO) | Collects assessed tax debt and unfiled returns in the field; can levy, lien, summons, and seize | Letter 725-B by mail scheduling an appointment; shows a pocket commission and HSPD-12 card in person |

| Revenue agent (RA) | Audits returns to determine the correct tax — the amount is still in dispute | An examination letter by mail opening an audit and scheduling it |

| Special agent (CI) | Investigates criminal tax matters; armed federal law enforcement | Two agents appear together, identify themselves as IRS Criminal Investigation, and advise you of your rights |

| Private collection agency | Handles certain older, inactive accounts by phone and mail only — cannot levy or lien | An IRS letter naming the specific agency arrives before the agency ever calls |

| Scammer | Impersonates all of the above; wants fast, untraceable payment | An unsolicited call, text, or email demanding gift cards, wire transfers, or payment apps, often with arrest threats |

Two of these deserve their own deep-dives: if the contact came from a debt collector rather than the IRS itself, read our guide to the IRS private collection agency program; if two agents showed up together and mentioned rights, that's an IRS criminal investigation — stop talking and get counsel before anything else.

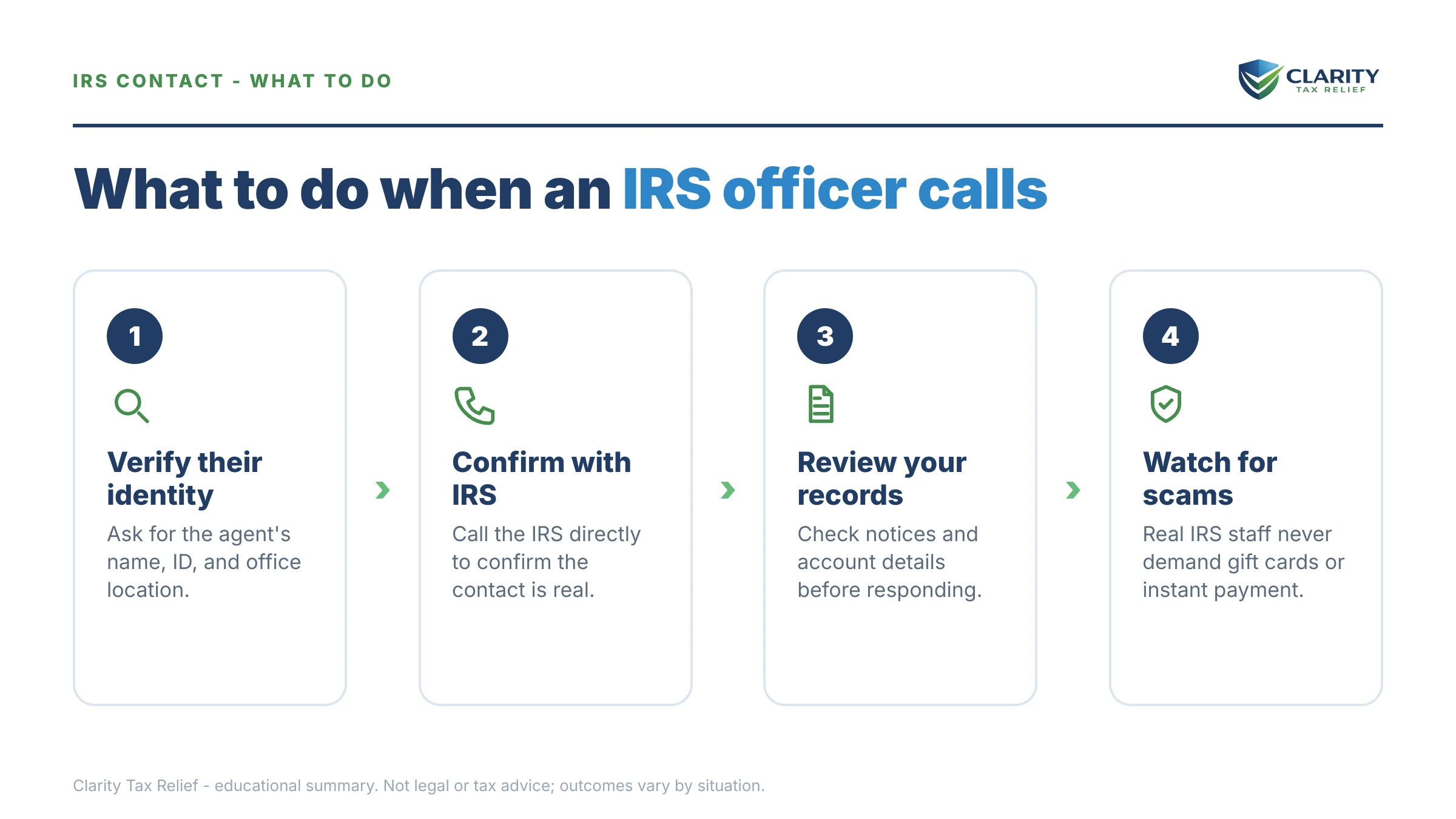

How to verify a real IRS revenue officer in 2026

Since July 2023, the IRS has ended most unannounced revenue officer visits — first contact now almost always arrives by mail as Letter 725-B, an appointment letter naming your officer and setting a meeting date. Our full guide to Letter 725-B walks through that letter line by line.

When you do meet an officer, verification is your right, not an insult. Every genuine revenue officer carries two forms of federal ID — a pocket commission and an HSPD-12 card — and will show both on request. You can also hang up on any caller and dial the IRS through the number on official correspondence or IRS.gov to confirm an officer is assigned to you.

Unannounced visits still happen in narrow situations — serving a summons, or an asset seizure already in motion — and officers still visit business locations, especially over unpaid 941s. If that's your situation, our guide to revenue officer payroll taxes covers the first 24 hours after an officer appears at your business.

The red flags never change: demands for gift cards, wire transfers, or payment-app transfers; threats of immediate arrest or deportation; pressure to pay before you can verify anything. The IRS does none of these, ever.

Why a revenue officer would be assigned to your case

Revenue officer assignment is reserved for cases the automated system couldn't resolve — there is no published dollar threshold, but the profile is consistent. Cases that land on an officer's desk typically involve:

- Large balances — often $100,000 or more, where the IRS wants a human reviewing assets and income directly.

- Unpaid payroll taxes — employment tax debt gets field attention faster than any other kind, because withheld taxes are treated as the government's money.

- Repeated non-filing — multiple missing years, especially with visible income.

- Broken agreements and dodged notices — defaulted payment plans, returned mail, exhausted collection attempts.

Here's the flip side that matters for most readers: smaller individual balances almost never get a revenue officer. The Automated Collection System works most balances — often well into six figures — by mail and phone, no field visits, so a $6,200 balance from a messy divorce year stays in that automated stream. So if someone claiming to be a "revenue officer" is pressing you over a balance that size, treat verification as step one, not a formality. And if the balance came from a joint return, know that your divorce decree doesn't bind the IRS — our guide to who pays IRS debt after divorce explains what actually protects you.

In 2026, with the IRS workforce down roughly 27% from 2025 cuts, per TIGTA reports, fewer officers are in the field — but the cases that do get assigned get concentrated, personal attention. An assigned officer is not a sign the system forgot you; it's the opposite.

What happens if you ignore an IRS revenue officer

Ignoring a revenue officer removes your input from the case — the officer then resolves it using the tools that don't require your cooperation. The sequence hardens in stages:

- The missed deadline gets documented. A skipped 725-B appointment or ignored document request goes in the case file as noncooperation, which shapes every later decision.

- The officer builds your financial picture without you. Banks, employers, payers, and property records get pulled directly — you lose the chance to explain context.

- A summons issues. Unlike a letter, a summons is legally enforceable; ignoring it can put you in front of a federal judge.

- Levy and lien follow. If a final notice of intent to levy is already on file — and in RO cases it usually is — the officer can levy quickly. A bank levy freezes funds for 21 days before they're sent to the IRS; a wage levy is continuous until released. You can estimate how much of a paycheck a wage levy could reach with our IRS Wage Garnishment Calculator.

- Seizure and personal assessments come last. For stubborn cases, officers can recommend seizing property; for business payroll debt, they run the interviews that pin the Trust Fund Recovery Penalty on owners, officers, and check-signers personally.

Every stage of that sequence is easier to prevent than to unwind — which is why the response steps below all start before the officer's first deadline, not after.

A revenue officer has your case — or someone claims to?

Send us the letter or the caller's details before your officer's appointment date passes. An experienced tax professional will verify the contact, decode where your case actually stands, and map your options — free and confidential.

Your options when a revenue officer has your case

Revenue officers close cases through the same IRS programs available to everyone — the difference is that the officer, not a computer, decides which one your finances support. Bringing a specific, realistic proposal to the first meeting is the single biggest thing you control. (For the shared background on each program, see our pillar on how to settle tax debt yourself; the official terms live on the IRS payment plans page.)

| Option | Who's eligible | Cost / key catch |

|---|---|---|

| Pay in full | Anyone | Stops penalties immediately; interest runs through the payoff date |

| Short-term plan (up to 180 days) | Balance you can clear within 180 days | $0 setup; penalties and interest keep accruing until paid |

| Guaranteed installment agreement | Owe $10,000 or less in tax, compliant filing history, can pay within 36 months | The IRS must accept it; a setup fee applies |

| Streamlined installment agreement | Balance of $50,000 or less, up to 72 months | Usually no full financial disclosure; set up online |

| RO-negotiated installment agreement | Larger balances and assigned cases | Requires Form 433-A financials; the officer sets the terms |

| Currently Not Collectible | Allowable living expenses meet or exceed your income | Collection pauses; the debt and interest remain, and a lien may still be filed |

| Offer in Compromise | Assets plus future income genuinely can't cover the debt | $205 fee and 20% down on lump-sum offers (both waived for low-income filers); per IRS data, the IRS accepted roughly 1 in 5 offers in FY2024 |

| Penalty relief | Clean compliance in the prior 3 years (first-time abatement, becoming automatic under AEP starting summer 2026) | Removes penalties, not interest |

A worked example: the $6,200 divorce-year balance

Say you owe $6,200 from the tax year your divorce was finalized — withholding set for married filing jointly, a return filed single, and a balance you never expected. This is a hypothetical, but the math is real. At $6,200 you're under the $10,000 line for a guaranteed installment agreement: $6,200 ÷ 36 months ≈ $173 a month in principal, plus the 0.5%-per-month failure-to-pay penalty (about $31 in month one, shrinking as the balance falls) and daily-compounding interest. Pay it in 180 days instead and setup costs nothing at all — our comparison of the best way to pay the IRS shows which channel is cheapest.

Two takeaways from this example. First, a balance this size will not get you a revenue officer — so a caller using that title over $6,200 has failed the plausibility test before you've checked a single credential. Second, penalties on a first slip are often removable, though interest almost never is; see can IRS interest be waived for the honest breakdown.

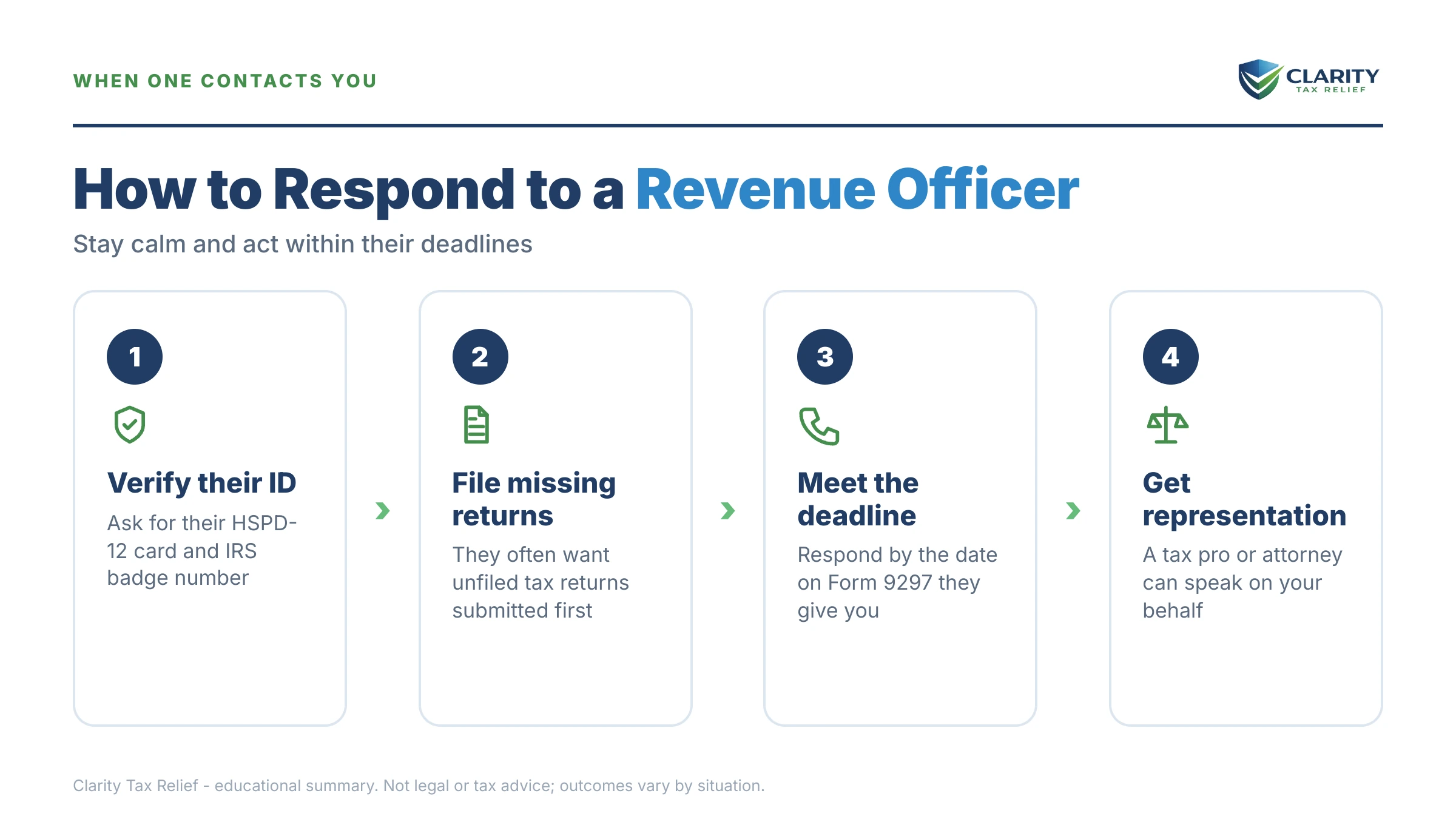

How to respond to an IRS revenue officer, step by step

- Verify the contact. Check for Letter 725-B in your mail and ask to see both credentials — the pocket commission and the HSPD-12 card — before discussing anything.

- Confirm what the IRS says you owe. Log into your IRS online account and match the balance and tax years against what the officer describes; never rely on a phone caller's numbers.

- Calendar every deadline the officer sets. The appointment date and every document-request date are hard deadlines; if you need more time, ask in writing before the date, never after.

- Gather your financial picture. Pull your last filed return, pay stubs, bank statements, and monthly expenses — the raw material for Form 433-A if the officer requires financials.

- Decide who speaks for you. File Form 2848 power of attorney if you want an experienced tax professional to attend meetings and field questions in your place — the officer must then work through your representative.

- Propose a resolution before the officer picks one. Come to the meeting with a specific plan — full pay, an installment agreement, hardship status, or an offer — because officers close cases faster and gentler when you bring the solution. Any payment you make goes only through IRS.gov/payments or to the United States Treasury.

When you can handle this yourself

If no officer is actually assigned — a small balance, notices by mail, a caller who failed verification — you don't need professional help to fix it. A balance under $10,000 that you agree with can be put on a payment plan online in an afternoon, and a scam call needs nothing more than a hang-up and a report. If collection action is causing genuine hardship the IRS won't acknowledge, the Taxpayer Advocate Service is a free, independent option.

Experienced help changes outcomes in a different set of situations: a revenue officer is actually assigned to you, a summons has issued, a levy is in motion, multiple years are unfiled, the debt involves business payroll taxes and a Form 4180 interview is coming, or the balance is large enough that the officer's read of your Form 433-A determines what you pay for years. In those cases, what you say — and what you concede in the first meeting — is hard to take back, and representation exists precisely so you don't have to navigate it alone.

Terms in a revenue officer case, decoded

- Pocket commission — the credential wallet identifying an IRS employee and their authority; one of the two IDs every real officer carries.

- HSPD-12 card — the standardized federal-employee smart ID card; the second required credential.

- Summons — a legal demand for testimony or records, enforceable in federal court, unlike an ordinary IRS letter.

- Form 433-A — the Collection Information Statement that discloses your income, assets, and expenses; it drives what resolution the officer will accept.

- Levy vs. lien — a levy takes property (wages, bank funds); a lien is a legal claim against property that secures the debt without taking anything yet.

- Trust Fund Recovery Penalty (TFRP) — the personal assessment of a business's unpaid withheld payroll taxes against the individuals responsible for paying them.

IRS revenue officer questions, answered

How do I know if an IRS revenue officer is real?

A real revenue officer carries two forms of official identification — a pocket commission and an HSPD-12 government ID card — and will show both on request. In 2026, first contact almost always arrives by mail, usually Letter 725-B scheduling an appointment. Anyone who demands immediate payment by gift card, wire transfer, or payment app, or threatens arrest, is a scammer, not the IRS.

Can an IRS revenue officer arrest me?

No. Revenue officers are civil employees with no arrest powers and they don't carry firearms. Criminal tax matters are handled by special agents from IRS Criminal Investigation, who work in pairs and identify themselves as such. If someone claiming to be from the IRS threatens jail over an unpaid balance, that threat itself is the strongest sign you're dealing with a scam.

How much do you have to owe before the IRS assigns a revenue officer?

There is no published cutoff — the Automated Collection System handles most balances, often well into six figures, while revenue officers are typically assigned to larger (often $100,000+), business/payroll, or repeat-noncompliance cases. If someone claims to be a revenue officer over a small balance, verify before you engage.

Do IRS revenue officers still make unannounced home visits?

Rarely. In July 2023 the IRS ended most unannounced revenue officer visits and replaced them with Letter 725-B, which schedules an appointment in advance. Unannounced visits still happen in limited situations, such as serving a summons or conducting an asset seizure. An unexpected knock with a demand for immediate payment should be treated as a red flag, not a routine IRS practice.

What is the difference between a revenue officer and a revenue agent?

A revenue officer collects tax that has already been assessed; a revenue agent audits returns to determine how much tax is owed in the first place. If an agent is involved, the amount is still in dispute and you have exam appeal rights. If an officer is involved, the IRS considers the debt settled law — the conversation is about how it gets paid, not whether you owe it.

Can a revenue officer levy my bank account or wages?

Yes — once the IRS has issued a final notice of intent to levy and the 30-day window has passed, a revenue officer can levy bank accounts and wages. A bank levy freezes funds for 21 days before they're sent to the IRS; a wage levy is continuous until released. Officers generally levy after missed deadlines, so meeting every date they set is your best protection.

Should I talk to a revenue officer without a representative?

For a simple case where you agree with the balance and can propose a realistic payment plan, you can handle the first meeting yourself. Once payroll taxes, a Form 4180 interview, a summons, or a six-figure balance is involved, filing Form 2848 lets an experienced tax professional attend in your place — and everything you say to an officer goes in the case file, so unprepared answers can narrow your options.

What is IRS Letter 725-B?

Letter 725-B is the appointment letter a revenue officer now sends to schedule an initial in-person or phone meeting, replacing most unannounced visits since July 2023. It names your officer, gives contact information, and sets a meeting date. Treat that date as a hard deadline: showing up prepared — or having a representative respond — sets the tone for the entire case.

Your next 24 hours

- Find the letter and the date. Locate the Letter 725-B (or any officer correspondence), note the officer's name and contact information, and circle the appointment or response date — that date now runs your calendar.

- Gather your file. Pull your last filed return, the letter itself, and a rough picture of your monthly income and expenses — everything a first conversation with the officer (or a professional) needs.

- Get the contact reviewed free. Whether you're facing a real revenue officer or a caller you can't verify, send it to us through the 2-minute form or call (888) 825-7779 — penalties and interest accrue every month you wait, and the first meeting is where your options are widest.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.