IRS Letters

Letter 725-B IRS Revenue Officer Visit: What It Means and How to Prepare (2026)

The short answer: a Letter 725-B IRS revenue officer visit letter means a human field collection officer — not a computer — has been assigned to your case and is scheduling an in-person or phone appointment. It replaced unannounced door knocks in July 2023. It is not an audit or a criminal case, but it is the most serious stage of civil collection short of seizure.

This letter is different from every IRS notice you've seen before: it has a real person's name on it, a direct phone line, and a specific appointment date and time. That's unnerving — and it's also your opening. A revenue officer is a person you can negotiate with, and how you handle the next two weeks largely decides whether this case ends in a payment plan or a levy.

Three details on the letter matter more than everything else on the page: the officer's name, the direct contact number, and the appointment date. The image below shows you exactly what a Letter 725-B looks like and where to find each one.

⏱ Your deadline: the appointment date and time printed on your Letter 725-B — or, if the letter asks you to call first, the contact-by date it states. There is no fixed statutory window here; the clock is the one the officer set. Miss it without calling and enforcement decisions — summons, levy, lien — move to a human being's desk with your silence as the last thing in the file.

What a Letter 725-B IRS revenue officer visit means

Letter 725-B means your case has left the IRS's automated collection system and been assigned to a revenue officer in field collection. Until now, everything you received — bills, reminders, intent-to-levy notices — was generated by computers. A revenue officer is a trained civil collection specialist whose entire job is resolving your case, one way or the other.

Since July 2023, the IRS has ended most unannounced revenue officer visits and replaced them with this scheduled-appointment letter. So the good news buried in the scary envelope: nobody should be knocking on your door without warning. The visit is on the calendar, which means you have time to prepare — and preparation is everything with an RO. (If someone did show up unannounced claiming to be IRS, read will the IRS come to my house before you open the door.)

Cases get routed to a revenue officer for a handful of reasons: a balance the automated system couldn't resolve after repeated notices, multiple years of unfiled returns, self-employment income with no withholding, or business and payroll tax debt. There's no published dollar cutoff — plenty of RO cases involve five-figure balances paired with unfiled years, which is exactly the profile of a gig worker who stopped filing when the bills got scary. If your case involves a business and 941s, the stakes and playbook are different — see revenue officer payroll taxes. And if you want the full picture of who ROs are and how they differ from auditors and scammers, start with what is an IRS revenue officer. For general background on how IRS letters work, our hub on why did I get a letter from the IRS covers the basics — this page stays focused on the 725-B itself.

One more thing worth saying plainly: in 2026, with the IRS workforce down roughly 27%, the fact that a scarce human officer was assigned to your file means the IRS considers your case worth working. That's not a reason to panic. It's a reason not to waste the scheduled appointment.

What happens if you ignore Letter 725-B

Ignoring a Letter 725-B puts enforcement decisions in the hands of the one IRS employee with direct authority to levy, summons, and file liens on your case. The sequence after a missed appointment typically runs in this order:

- Missed appointment, no call. The officer documents the non-response. From this point forward, you're an "uncooperative taxpayer" in the case history — the label that colors every later decision.

- Firm deadlines. The officer sets written deadlines for financial information and unfiled returns. These aren't suggestions; each one missed is another entry in the file.

- Summons. A summons legally compels you — or your bank, or the payment platforms that issue your 1099s — to produce records or testimony. Ignoring a summons can be enforced in federal court. This is also one of the limited situations where an unannounced visit can still happen.

- Final notice and levy. If an LT11 or Letter 1058 hasn't already been issued, the officer issues it; 30 days later, levies can follow — bank accounts, wages, and one-time levies on 1099 payments your platforms or clients owe you.

- Lien and substitute returns. The officer can file a Notice of Federal Tax Lien against everything you own, and for unfiled years, push through substitute-for-return assessments built from gross 1099 figures with zero business deductions.

Here's how the 725-B fits into the collection sequence you've probably been receiving pieces of for months:

| Stage | Who's handling it | What it means |

|---|---|---|

| CP14, CP501, CP503 | Automated system | Bills and reminders — no enforcement yet, balance growing monthly |

| CP504 | Automated system | Intent to levy your state tax refund; lien becomes realistic |

| LT11 / Letter 1058 | Automated system or RO | Final notice — 30 days until levy authority; CDP appeal rights attach |

| ACS phone collection | Call-center collectors | No single person owns your case; resolutions are formulaic |

| Letter 725-B | Assigned revenue officer | You are here — a named human schedules a meeting and owns your file |

| RO deadlines & summons | Revenue officer | Compelled records and returns if you don't cooperate voluntarily |

| Levy, lien, seizure | Revenue officer | Bank, wage, and 1099 levies; lien filing; asset seizure in extreme cases |

Holding a Letter 725-B with an appointment date on it?

Don't walk into a revenue officer meeting unprepared — and don't skip it. Send us a photo of your letter and an experienced tax professional will map out exactly what the officer will ask for and what to propose, free, before your scheduled appointment.

Your options when the revenue officer asks how you'll pay

Revenue officers can approve every major IRS resolution — but only after you're in "filing compliance," meaning all required returns (generally the last six years) are in. That's the RO's non-negotiable first ask. Once you're compliant, these are the realistic paths:

| Option | What it costs | What the officer requires | Typical timeline |

|---|---|---|---|

| Pay in full (up to 180 days) | $0 setup; interest and penalties until paid | All returns filed; ability to pay shown | Enforcement stops once arranged |

| Installment agreement | Setup fee (reduced with direct debit); interest continues | All returns filed; balances ≤ $50,000 can qualify for streamlined terms up to 72 months | Often approved within weeks of compliance |

| Partial-pay installment agreement | Setup fee; monthly amount based on documented ability | Full Form 433-A financial disclosure with proof | Longer review; periodic re-evaluation |

| Currently Not Collectible | $0; balance still accrues interest | Form 433-A proving paying anything creates hardship | Collection pauses while hardship lasts |

| Offer in Compromise | $205 fee + 20% down on lump-sum offers (both waived with low-income certification) | All returns filed; full financials; assets and income genuinely can't cover the debt | Months to over a year; roughly 1 in 5 offers accepted in FY2024 |

Two RO-specific realities the table can't capture. First, the officer will run your numbers through a Form 433-A financial statement using IRS allowable-expense standards — not your actual budget — so the monthly payment they calculate may be higher than what feels affordable. Documentation is your only counterweight. Second, an officer who sees good-faith movement (returns coming in, a plan proposed, current-year estimated taxes started) almost always holds enforcement while you work the plan. Cooperation buys time; silence spends it.

If the levy stage has already arrived — or the officer issues the final notice while you're negotiating — you have the right to request a Collection Due Process hearing within 30 days using Form 12153, which pauses levy action on those periods while Appeals reviews your case.

A worked example: $11,300 owed, three years unfiled

Say you're a gig worker who owes $11,300 on the one year you filed, and you haven't filed the three years since. That combination — a known balance plus unfiled years with 1099s on file — is a classic 725-B profile. Here's the math the revenue officer is looking at, and the math you should bring instead. (All figures are rough and hypothetical.)

If the IRS files for you: your platforms reported, say, $38,000 in gross 1099 income each unfiled year. A substitute for return taxes that gross figure with no mileage, no phone, no supplies — roughly $7,600 per year in tax before penalties. Three years of that is about $22,800 added to your $11,300, before the failure-to-file penalty (5% per month, capped at 25%) piles on top.

If you file accurate returns first: with mileage and expenses documented, net profit might be around $21,000 per year — roughly $3,500 in tax. Add the maxed 25% failure-to-file penalty (~$875) and accrued failure-to-pay penalty and interest (call it ~$700 per year), and each year lands near $5,100. Three years ≈ $15,300, for a total balance around $26,600 including the original $11,300. You can estimate your own penalty and interest buildup with our IRS Penalty & Interest Calculator.

At roughly $26,600, you're under the $50,000 streamlined threshold: about $26,600 ÷ 72 months ≈ $370/month, with interest continuing until paid — and the officer will also expect you to start quarterly estimated payments so the hole stops deepening. Filing accurately versus letting the SFRs stand is the difference between a manageable monthly plan and a balance nearly $20,000 higher. That's why the returns come first: start with your IRS wage and income transcript for each year, and if your records are a shoebox of nothing, filing back taxes with no records is more doable than you think. Our guide to haven't filed taxes in 3 years walks the catch-up sequence in detail, and the 6-year lookback rule explains why the officer will rarely ask for more than six years of returns.

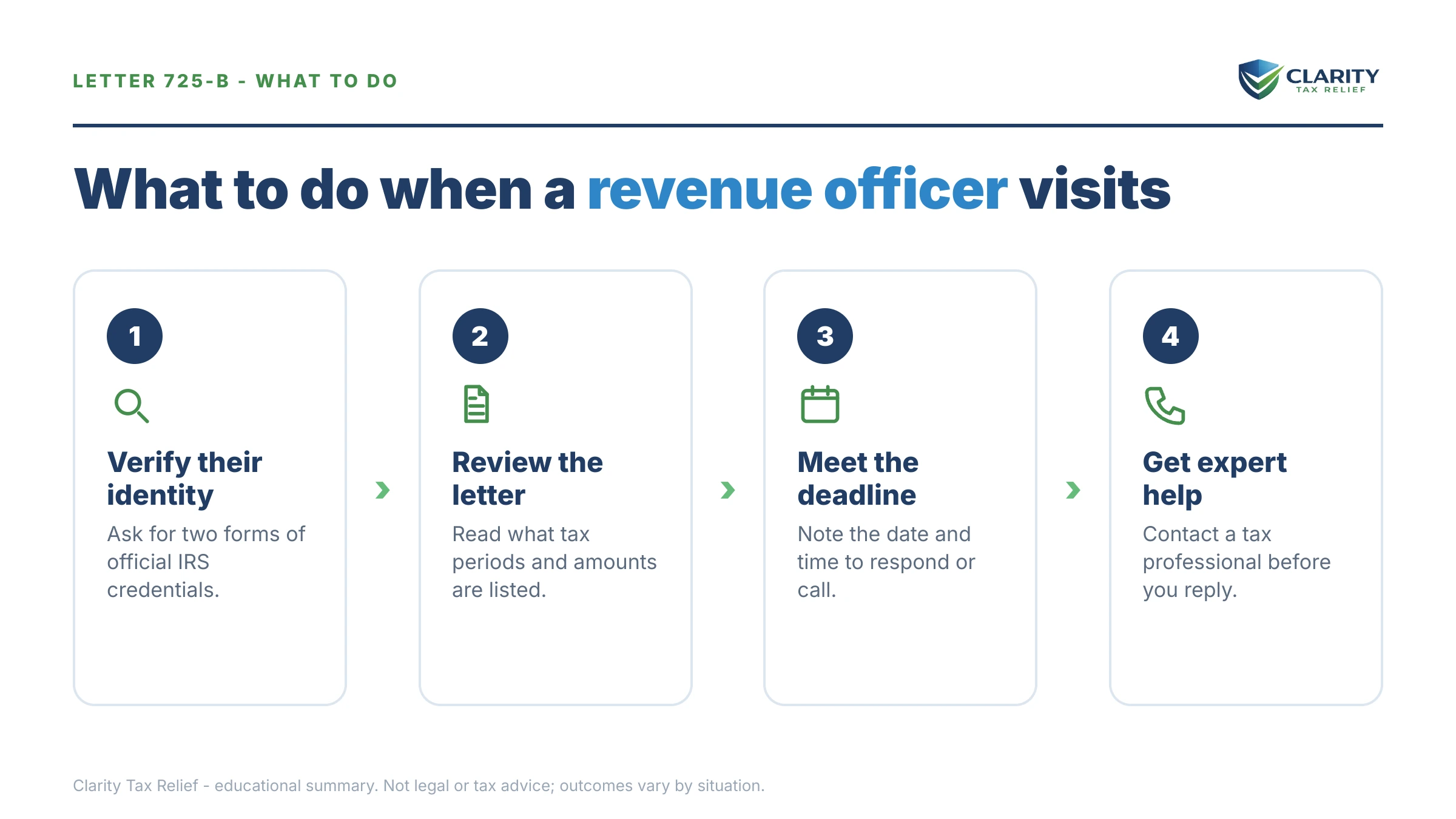

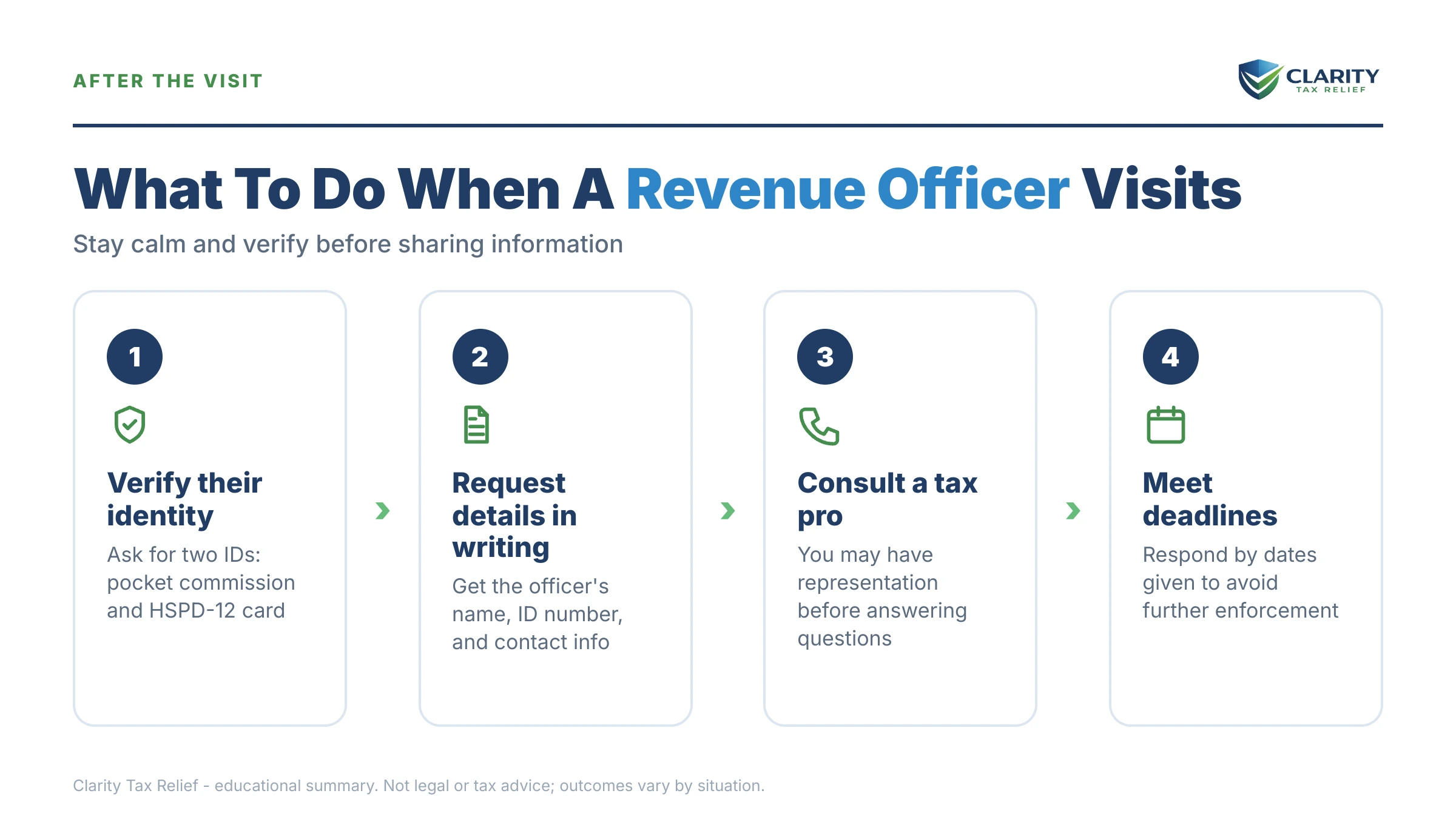

How to respond to Letter 725-B, step by step

- Verify the letter is real. Call the officer's number on the letter or log into your IRS online account to confirm a balance and an assigned case. Real officers carry two forms of official IRS identification and never demand gift cards or wire payments.

- Confirm or reschedule the appointment. Call before the printed date. Officers routinely grant a short delay to gather records or bring in representation — silence is the only response that hurts you.

- Pull your income records. Request wage and income transcripts for every unfiled year so your returns match what the IRS already has on file.

- Prepare the missing returns and Form 433-A. The officer will require unfiled returns (generally the last six years) and a documented financial statement before approving any resolution.

- Choose your proposal before the meeting. Decide whether you're offering full payment, a monthly installment agreement, hardship status, or an Offer in Compromise — and bring the numbers that support it.

- Consider representation. Filing Form 2848 lets an experienced tax professional deal with the officer for you, including attending the appointment in your place.

That last step deserves a sentence more: once Form 2848 is on file, the officer generally must work through your representative. For many people, never sitting across the table from the RO — while still fully cooperating — is the single biggest stress reducer in the whole process.

When you can handle this yourself — and when help changes the outcome

You can reasonably handle a Letter 725-B alone if all your returns are filed, you agree with the balance, and you can either pay in full within 180 days or afford the streamlined monthly payment. In that case, your job is simple: show up (or call) on time, be straight with the officer, and set up the agreement. Revenue officers close cooperative, compliant cases quickly — they have no interest in dragging out a case you're actively fixing.

Experienced help tends to change outcomes in four situations. Multiple unfiled years — because how those returns are prepared (deductions reconstructed, income matched to transcripts) sets the size of the debt you'll be negotiating for the next decade. Disputed balances — an RO collects what's assessed; challenging the assessment is a separate track with its own deadlines. Hardship and partial-pay cases — the Form 433-A allowable-expense math is where self-represented taxpayers most often agree to payments they can't sustain. And any case where a final levy notice has already been issued or a levy is in motion — because the appeal windows are short and unforgiving.

Terms on your Letter 725-B, decoded

- Revenue officer (RO): a civilian IRS field collection employee — not an auditor, not law enforcement — with authority to arrange resolutions and to levy, summons, and file liens.

- Field collection: the IRS division that works cases in person rather than through the automated notice-and-call-center system.

- Form 433-A: the Collection Information Statement — the detailed financial disclosure the officer uses to calculate what you can pay.

- Summons: a legal demand for records or testimony, enforceable in federal court, that the officer can issue to you or third parties like your bank.

- Notice of Federal Tax Lien: a public filing that attaches the government's claim to everything you own; the officer decides whether and when to file it.

- Substitute for return (SFR): a return the IRS prepares for an unfiled year using gross reported income and no business deductions — almost always worse than filing yourself.

- Collection Due Process (CDP): your right to an independent Appeals hearing, requested on Form 12153 within 30 days of a final levy notice, which pauses levy action while it's pending.

Letter 725-B questions, answered

Is IRS Letter 725-B serious?

Yes — it's one of the most serious collection letters the IRS sends, because it means a human revenue officer now controls your case instead of a computer. Revenue officers are typically assigned to balances the automated system couldn't resolve, unfiled returns, or business debts. It is still fixable: officers can approve payment plans, hardship status, and settlements — but only if you engage before their deadlines pass.

Will the revenue officer show up at my house unannounced?

Usually not anymore. In July 2023 the IRS ended most unannounced revenue officer visits and replaced them with the Letter 725-B scheduled appointment. Unannounced contact is now generally reserved for limited situations such as serving a summons or carrying out an asset seizure. If someone appears at your door claiming to be from the IRS with no letter on file, verify their credentials — real officers carry two forms of official identification.

Can I reschedule a Letter 725-B appointment?

Yes. Call the revenue officer at the number printed on the letter and ask for a new date — officers routinely reschedule when you ask before the appointment, and a short delay to gather records or hire representation is reasonable. What you cannot safely do is skip the meeting without calling. A missed appointment with no contact is what pushes officers toward summonses, levies, and lien filings.

Do I have to meet the revenue officer myself, or can a representative go instead?

Once you file Form 2848, a power of attorney, an experienced tax professional can speak with — and in most cases meet — the revenue officer on your behalf, and the officer must generally direct contact through your representative. Many taxpayers never sit in the meeting at all. You may still need to sign returns and financial forms, and the officer can require your participation in limited circumstances.

What will the revenue officer ask for at the meeting?

Expect three things: any unfiled tax returns, a completed financial statement (Form 433-A for individuals, Form 433-B for businesses) with proof — bank statements, pay records, bills — and a plan for paying the balance. The officer will also check that you're staying current on this year's taxes, such as quarterly estimated payments if you're self-employed. Going in with those items prepared is what separates a cooperative case from an enforcement case.

Can a revenue officer levy my bank account or garnish my wages?

Yes — revenue officers have direct authority to levy bank accounts, wages, and even 1099 payments owed to you, once the IRS has issued a final notice of intent to levy (LT11 or Letter 1058) and 30 days have passed. If you never received that final notice, the officer must issue it before levying, which gives you the right to request a Collection Due Process hearing on Form 12153.

Is Letter 725-B a criminal investigation?

No. Letter 725-B comes from a revenue officer in the civil collection division — their job is collecting tax, not prosecuting. Criminal cases are handled by IRS Criminal Investigation special agents, who don't send appointment letters or negotiate payment plans. That said, if you have years of unfiled returns or unreported cash income, resolve it through the civil process promptly — voluntary compliance is the strongest protection against a case ever turning criminal.

What if I haven't filed the returns the revenue officer wants?

Tell the officer your plan to file them and ask for a realistic deadline — then hit it. Officers generally require the last six years of returns before they'll consider any resolution. If you don't file, the IRS can prepare a substitute for return using gross 1099 and W-2 figures with no business deductions, which almost always assesses far more tax than an accurate self-filed return would.

Your next 24 hours

- Find three things on your letter: the revenue officer's name, the direct phone number, and the appointment (or contact-by) date. Write the date somewhere you can't ignore it.

- Gather your paper trail: the Letter 725-B itself, your last filed return, every 1099 and income record you have for the unfiled years, and a rough list of monthly income and bills.

- Get the letter reviewed free — before the appointment date. Call (888) 825-7779 or use the 2-minute form, and an experienced tax professional will tell you exactly what the officer will ask for and what to propose.

For the IRS's own resources: payment options live at IRS.gov/payments, plan details at the IRS payment plans page, and if the process itself breaks down — deadlines you can't meet through no fault of your own, hardship the officer won't recognize — the independent Taxpayer Advocate Service can intervene.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.