IRS Notices

IRS Letter 1058: Final Notice of Intent to Levy and Your 30-Day Clock (2026)

The short answer: IRS Letter 1058 is the Final Notice of Intent to Levy. It starts a 30-day clock: file Form 12153 within 30 days to request a Collection Due Process hearing and legally block the levy while your case is heard. A 1058 usually means a revenue officer — a human, not a computer — now controls your account.

You signed for a certified envelope between payroll runs, and now "IRS Letter 1058, Final Notice of Intent to Levy and Notice of Your Right to a Hearing" is sitting on the desk next to this week's timesheets. The dread is real — but so is the 30-day window it just opened, and everything in this guide is about using it. Unlike the earlier notices you may have set aside, this one carries legal force: it is the last thing the IRS must send before it can take money from your accounts, your receivables, or your paycheck.

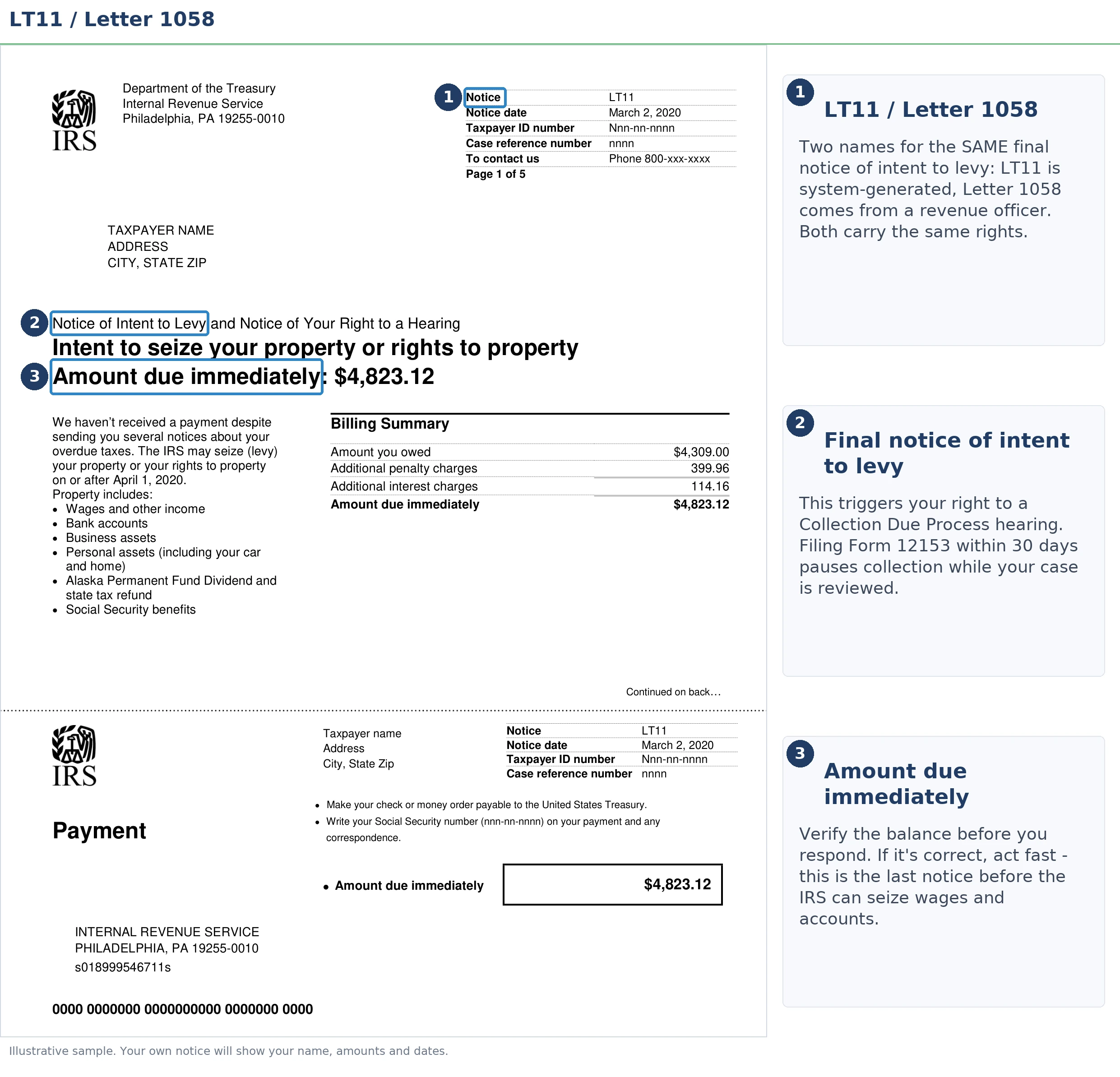

Two dates matter on this document — the letter date and the deadline it creates. The image below shows exactly what a Letter 1058 looks like and where to look for both.

⏱ Your deadline: You have 30 days from the date printed on Letter 1058 to file Form 12153 and preserve your Collection Due Process rights. After day 30, the IRS can levy without any further warning — and you lose the automatic right to have a court review the case before it does.

Why you got IRS Letter 1058 — and why a revenue officer sent it

Letter 1058 is the revenue-officer version of the IRS's final levy warning: it means your case left the computer system and landed on a specific person's desk. Its automated twin is the LT11 notice — legally identical, but issued by the Automated Collection System. When the same warning arrives as a 1058, the IRS assigned a field revenue officer to your account, which typically happens with larger balances, business and payroll debt, or unfiled returns stacked on top of a balance.

That distinction changes your playbook. An LT11 is a machine following a schedule; a 1058 is a person with direct authority to issue levies, file liens, and summon your financial records. Revenue officers work cases to conclusion — they don't cycle you back into the notice queue. If the officer has already visited or scheduled a visit, our guide to the Letter 725-B revenue officer visit covers what those contacts mean.

Why the letter exists at all: under IRC §6330, the IRS cannot levy most property until it has told you, in writing, that you have the right to a hearing. Letter 1058 is that telling. If you're not sure how your account got this far — or you've received other IRS mail you haven't decoded — start with why you got a letter from the IRS for the bigger map. This page stays on the 1058 itself, because nothing else in your mail pile carries this deadline.

| Notice | What it means | Enforcement power |

|---|---|---|

| CP14 / CP161 | First bill for the balance (CP161 for businesses) | None yet — roughly 21 days before the sequence advances |

| CP501 / CP503 / CP504 | Reminders, then intent to levy your state refund | CP504 lets the IRS take state tax refunds under §6331(d) |

| Letter 1058 / LT11 | Final Notice of Intent to Levy + right to a hearing | Starts the 30-day CDP clock; last required warning |

| Day 31 and beyond | No CDP request on file | Bank, wage, and receivables levies can issue at any time |

What happens after 30 days if you do nothing

Letter 1058 gives the IRS legal authority to levy your bank accounts, wages, and business receivables once 30 days pass from the date printed on it. There is no follow-up warning after day 30 — the next thing you hear about the levy is usually from your bank, your employer, or a customer who received one. Here's the sequence, in order:

- Day 1–30: The CDP window is open. Nothing can be levied yet (with narrow exceptions like state refunds and jeopardy situations). Every good option is still on the table.

- Day 31: Levy authority is live. A revenue officer can send levies the same week — there's no fixed grace period beyond the 30 days.

- Bank levy: Your bank freezes whatever is in the account that day and holds it 21 days before sending it to the IRS — a short window to prove hardship or reach a resolution. See the IRS bank levy 21-day rule.

- Wage levy: Unlike a bank levy, a wage levy is continuous — it attaches to every paycheck until the IRS releases it. You can estimate how much a wage levy could take with our IRS Wage Garnishment Calculator.

- Business levies: For a business, the officer can also levy the business bank account and send levies directly to your customers for accounts receivable — which cuts off cash flow at the source.

- Parallel actions: A Notice of Federal Tax Lien is often filed at this stage if it hasn't been already, and personal tax debt over $66,000 (the 2026 threshold) can be certified to the State Department, blocking passport issuance or renewal.

One 2026 reality worth naming: the IRS workforce shrank roughly 27% in 2025, but levy authority didn't. A revenue officer who is harder to reach by phone can still issue a levy on schedule — thinner staffing makes proactive contact more important, not less.

Holding a Letter 1058 right now?

The 30-day window on your letter is already running. Get it reviewed free before Form 12153 rights expire — an experienced tax professional will map your options against your exact deadline, no pressure, no obligation.

Your options after Letter 1058

Every IRS resolution program is still available at the Letter 1058 stage — the letter changes the deadline, not the menu. What changes with the balance is how much paperwork the IRS demands and who decides:

| What you owe | Realistic options | What the IRS will require |

|---|---|---|

| Under $10,000 (personal) | Guaranteed installment agreement; pay in full within 180 days | Filed returns; ability to pay within 3 years for the guaranteed IA |

| $10,000–$50,000 (personal) | Streamlined installment agreement up to 72 months; CNC if hardship | Usually no full financial statement if set up before default |

| Over $50,000 (personal) | Non-streamlined IA, partial-pay IA, Offer in Compromise, CNC | Full financials — Form 433-F or 433-A, reviewed by the revenue officer |

| Business payroll (941) debt — any amount | Business payroll tax payment plan; IBTF-Express if $25,000 or less | Form 433-B above the express threshold, current-quarter deposits on time, and a Trust Fund Recovery Penalty review |

A few notes the table can't hold. An installment agreement proposal that's pending generally stops levy action while the IRS considers it — proposing a plan before day 30 is itself protective. Currently Not Collectible status pauses collection entirely if paying would leave you unable to cover necessary living or operating expenses; the debt remains and interest accrues, but levies stop. An Offer in Compromise is real but means-tested: a $205 application fee, 20% down on lump-sum offers (both waived with low-income certification), and the IRS accepted roughly 1 in 5 offers in FY2024 — a candidacy question, never a given.

If the debt is payroll tax, one more track runs alongside all of this: the revenue officer will evaluate the Trust Fund Recovery Penalty, which can make owners, officers, and anyone who signed checks personally liable for the withheld portion — even if the business folds. Resolving the business balance and defending the personal exposure are two different fights, and the second one has its own deadlines.

Your CDP rights: what Form 12153 actually does

Filing Form 12153 within 30 days of Letter 1058 legally bars the IRS from levying the listed tax periods while your Collection Due Process case is pending. Your case goes to the IRS Independent Office of Appeals — a different office from the revenue officer — where you can propose an installment agreement, an offer, hardship status, or challenge the levy as premature. If Appeals rules against you, a timely CDP request preserves the right to take the decision to Tax Court. Our full Form 12153 CDP hearing guide walks through the form line by line.

Two trade-offs to know before you file. First, a CDP request pauses the 10-year collection statute while the hearing is pending — you gain levy protection but stop the expiration clock. Second, if you miss the 30 days, you can still file within one year for an "equivalent hearing": same Appeals conference, same alternatives, but no levy bar and no Tax Court review. Whether to file a CDP request at all is a judgment call — if you can reach a straightforward payment plan with the officer this week, a hearing may add months without adding value. If the balance is disputed, the levy would cause hardship, or the officer won't consider alternatives, the hearing is your leverage.

A worked example: $83,100 in payroll tax debt

Say your business owes $83,100 across four unpaid quarters of Form 941, and the revenue officer just issued Letter 1058 to the business. Here's how the math and the strategy actually play out — this is a hypothetical, not a client case:

- The IA math: $83,100 spread over 72 months is roughly $1,154 per month ($83,100 ÷ 72 ≈ $1,154) — before continued interest and the 0.5%-per-month failure-to-pay penalty, so the real payment needed to retire the debt runs higher. Because the balance exceeds the $25,000 IBTF-Express ceiling, the officer will require Form 433-B and proof that current-quarter deposits are being made on time.

- The trust-fund split: Roughly the withheld income tax plus the employees' share of FICA — often on the order of 55–65% of a 941 balance, so perhaps $45,000–$55,000 here — is "trust fund" money the officer can assess against responsible individuals personally.

- The passport angle: The business balance itself doesn't touch anyone's passport. But if the officer assesses the trust-fund portion against you personally, that personal assessment alone could clear the $66,000 certification threshold for 2026.

- The protective move: Filing Form 12153 on, say, day 20 blocks receivables and bank levies while Appeals hears the case — buying the weeks needed to get deposits current and financials assembled, at the cost of tolling the collection statute.

The order of operations matters more than any single number: deposits current first, then the payment structure, then the trust-fund defense. Reversing that order is how owners end up with a levy on the operating account mid-negotiation. Background on the whole payroll cascade is in our guide to 941 back taxes.

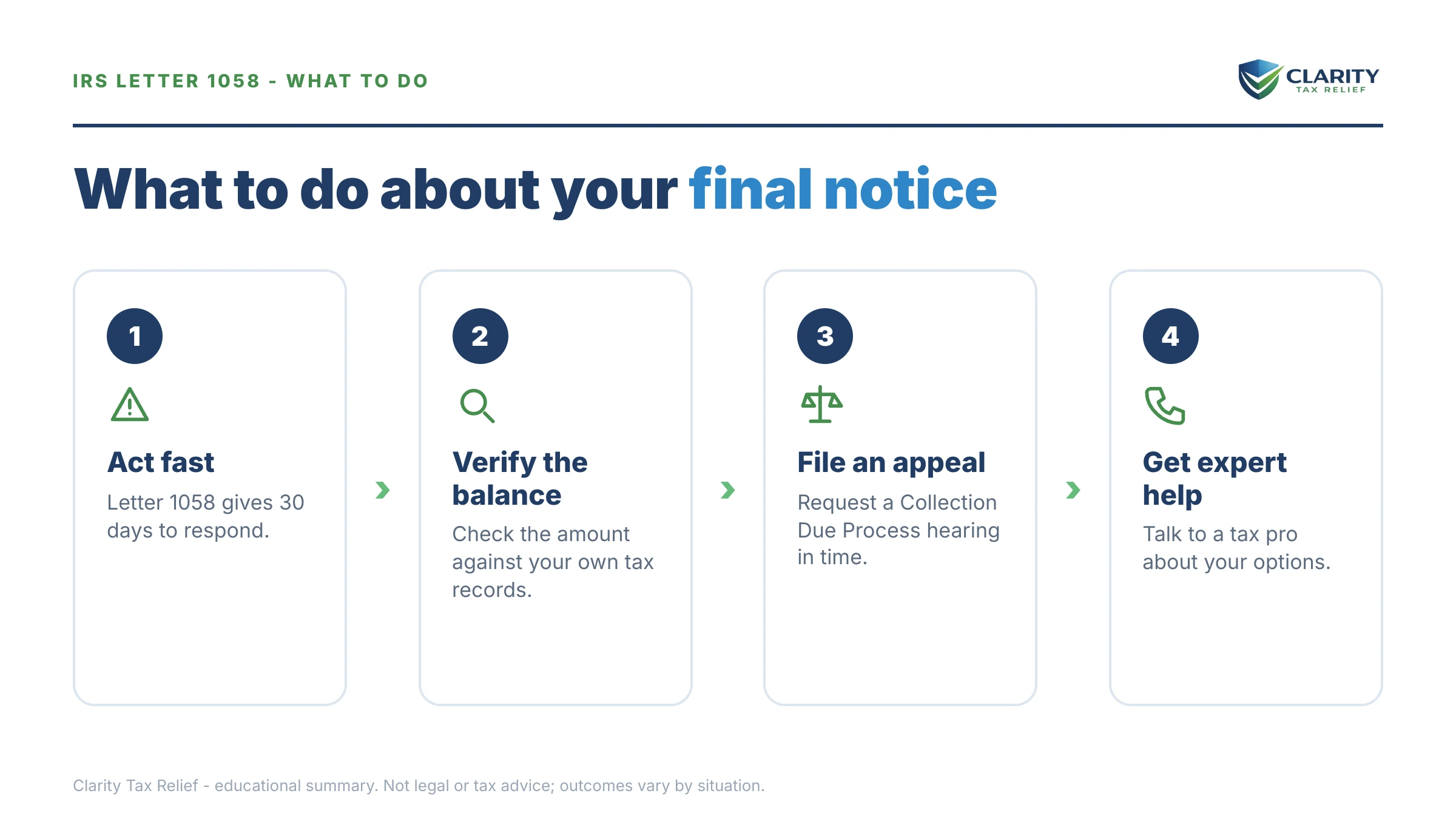

How to respond to Letter 1058, step by step

- Find the date on the letter and calculate day 30 — write that date down; it is the deadline that controls everything else.

- Verify the balance against your IRS online account or account transcripts before you agree to anything.

- File Form 12153 before day 30 to preserve your Collection Due Process hearing and block levy action while it's pending — send it to the address on the letter and keep proof of mailing.

- Choose the resolution you'll propose — installment agreement, hardship status, or an offer — and gather the financial documents (Form 433-B or 433-F) that support it.

- Contact the revenue officer named on the letter — or have a representative do it under Form 2848 — so the person with levy authority knows a resolution is in motion.

When you can handle Letter 1058 yourself

Not every 1058 needs professional help. You can reasonably handle this alone if the balance is accurate, it's personal income tax under about $50,000, all your returns are filed, and you simply need a payment plan — call the officer, propose the streamlined agreement, get it in writing before day 30. The same goes if you can pay in full within 180 days: say so, get the deadline noted, and pay.

Experienced help changes outcomes in four situations. First, payroll or business debt — because the Trust Fund Recovery Penalty investigation runs in parallel, and what you say to the officer about who controlled the money becomes evidence in the personal-liability case. Second, a levy already in motion or imminent, where release timing is everything. Third, multiple unfiled years, where filing order and substitute-return corrections change the balance itself. Fourth, offer math — Reasonable Collection Potential calculations that decide whether an OIC is viable before you spend a year pursuing one. In those cases, representation under Form 2848 also means the officer's calls and deadlines route through someone who handles them daily.

Terms on your Letter 1058, decoded

- Levy vs. lien: a levy takes your property (money in an account, part of a paycheck); a lien is a legal claim against your property that secures the debt. The 1058 threatens the first; the second may already exist.

- CDP (Collection Due Process): your statutory right to an independent Appeals hearing before the levy — the right this letter exists to announce, and the one that expires at day 30.

- Form 12153: the one-page form that invokes your CDP rights. Mail or fax it to the address on the letter, not a generic IRS address.

- Equivalent hearing: the fallback if you file Form 12153 late (within one year) — same conference, but no levy bar and no Tax Court review.

- CSED (Collection Statute Expiration Date): the date, 10 years after assessment, when the IRS's right to collect expires — paused while a CDP hearing, offer, or bankruptcy is pending.

- Trust Fund Recovery Penalty: the mechanism that turns a business's withheld payroll taxes into a personal debt for the people responsible for paying them over.

Letter 1058 questions, answered

Is Letter 1058 the same as LT11?

Legally, yes — both are the final notice of intent to levy under IRC §6330, and both start the same 30-day Collection Due Process clock. The difference is who sent it: LT11 comes from the IRS's automated collection system, while Letter 1058 comes from a revenue officer personally assigned to your account. A 1058 means a human is now working your case, which usually signals a larger balance, business or payroll debt, or unfiled returns.

How long after Letter 1058 will the IRS levy?

The IRS must wait 30 days from the date on the letter before levying. After day 30, a levy can come at any time — there is no second warning. If it hits a bank account, the bank holds the funds for 21 days before sending them to the IRS; a wage levy, once issued, is continuous until released. Filing Form 12153 within the 30 days generally blocks levy action while your hearing is pending.

What if I missed the 30-day deadline on Letter 1058?

You can still request an equivalent hearing by filing Form 12153 within one year of the letter's date. You get a hearing with Appeals and can propose the same alternatives, but the levy is no longer legally barred while you wait, and you lose the right to Tax Court review. Missing the 30 days is a setback, not the end — payment plans, hardship status, and offers all remain available.

Does filing Form 12153 stop a levy?

A timely Form 12153 generally prohibits the IRS from levying the tax periods listed while your Collection Due Process case is pending. It also pauses (tolls) the 10-year collection statute during the hearing, so the clock stops running in your favor while you wait. It does not erase the debt or stop the meter — penalties and interest keep accruing the whole time.

Why did my business get a Letter 1058 for payroll taxes?

Payroll (941) debt goes to a revenue officer faster than almost any other tax debt, because withheld payroll taxes are treated as trust funds the business held for the government. Alongside the levy threat, the RO can pursue the Trust Fund Recovery Penalty — assessing the trust-fund portion against owners, officers, and check-signers personally. If you receive a Form 4180 interview request or Letter 1153, the personal-liability track is already moving.

Does Letter 1058 mean a tax lien has been filed?

Not automatically — a levy takes property, a lien is a claim against it, and they are separate actions. But by the time a revenue officer issues a 1058, a Notice of Federal Tax Lien is often already filed or about to be, especially on balances over $10,000. If a lien is filed, you will receive Letter 3172, which carries its own separate 30-day appeal right.

Can I still get a payment plan after Letter 1058?

Yes — an installment agreement is the most common resolution at this stage, and a pending plan proposal generally stops levy action while the IRS considers it. Above $50,000, expect to provide a full financial statement: Form 433-B for a business, Form 433-F or 433-A for individuals. A payroll balance adds one more condition: your current-quarter deposits must be on time before the IRS will formalize any plan.

Your next 24 hours

- Find the date at the top of your Letter 1058 and count forward 30 days. Write that date where you'll see it daily — it's the deadline every option depends on.

- Gather three things: the letter itself, your most recent filed return (and a list of any unfiled years or quarters), and a snapshot of income and bank balances — the raw material for Form 12153 and any plan proposal.

- Get the letter reviewed free before the 30-day window closes — call (888) 825-7779 or use the 2-minute form. An experienced tax professional will tell you whether to file the CDP request, propose a plan, or both.

For primary sources, see the IRS's own page on understanding your LT11 notice or Letter 1058, the official Form 12153 page, payment options at IRS.gov/payments, and the Taxpayer Advocate Service if IRS action is causing immediate hardship.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.