IRS Letters

IRS Letter 1153: The Trust Fund Recovery Penalty Proposal and Your 60-Day Deadline (2026)

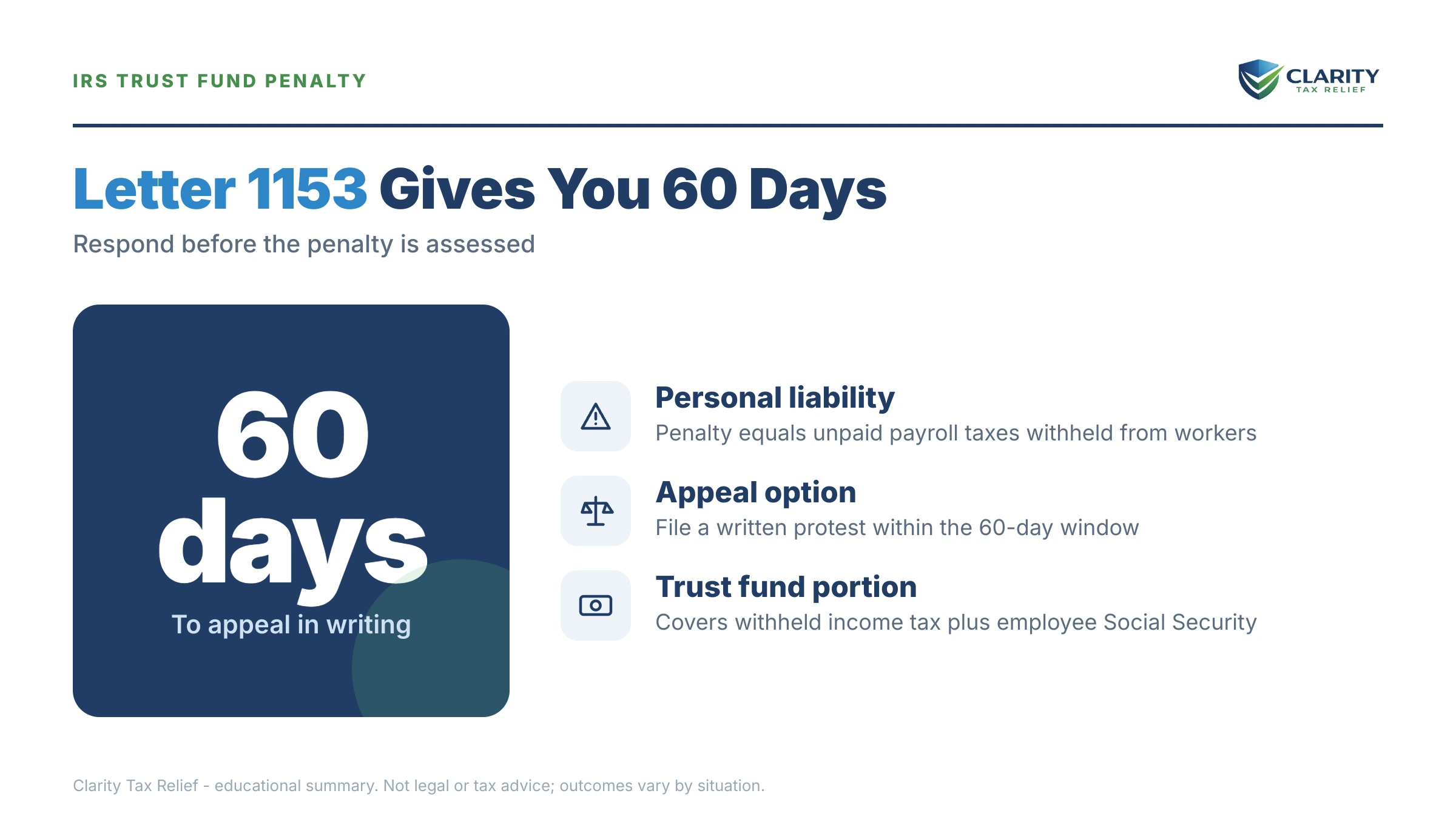

The short answer: Letter 1153 is the IRS's formal proposal to assess the Trust Fund Recovery Penalty against you personally for your business's unpaid payroll taxes. You have 60 days from the date on the letter to file a written appeal. Signing the enclosed Form 2751 means you agree the debt is yours.

Until now, the 941 balances were the company's problem. A revenue officer probably interviewed you weeks ago, and today Letter 1153 arrived with a Form 2751 stapled behind it — a document that, with one signature, moves the withheld payroll taxes from the business's books onto you as an individual. That shift is not automatic yet, and this letter is the single best moment to stop or shrink it.

Two documents came in this envelope, and they do different jobs: Letter 1153 explains your appeal rights, while Form 2751 states the exact dollar amount and quarters the IRS wants to pin on you. The image below shows exactly what this letter looks like and where to find the two things that control everything — the date that starts your 60 days and the proposed amount.

⏱ Your deadline: you have 60 days from the date printed on Letter 1153 to file a written appeal (75 days if the letter was addressed to you outside the United States). Miss it and the IRS assesses the penalty against you personally — and you lose the right to argue liability with the IRS Independent Office of Appeals.

Why you got Letter 1153

Letter 1153 means a revenue officer has completed a Trust Fund Recovery Penalty investigation and concluded you are personally liable for your business's withheld payroll taxes under Internal Revenue Code §6672. This is not a form letter from a computer — a human collector built a file on you, usually starting with a Letter 3164 investigation contact and a Form 4180 interview about who controlled the company's money.

The trigger is almost always unpaid Form 941 liabilities. When a business withholds income tax and FICA from paychecks but doesn't deposit it, the IRS treats that money as government funds the business held "in trust." When the business can't pay, §6672 lets the IRS pursue the people who decided where the money went instead. Our guide to the trust fund recovery penalty covers the statute in depth; this page is about the specific letter in your hand and the clock it starts.

One reassurance up front: Letter 1153 is a proposal, not an assessment. Nothing is on your personal account yet. No lien attaches to your house today, no levy can touch your personal bank account today, and no interest is accruing against you personally yet. All of that changes only if the 60 days pass without a fight — or you sign Form 2751.

If you're still not sure why the IRS contacts people the way it does, our overview of why you got a letter from the IRS maps the whole system. Letter 1153 sits near the serious end of it.

What Letter 1153 can make you owe — and what it can't

The Trust Fund Recovery Penalty equals 100% of the trust-fund portion of the payroll taxes — the money withheld from employees — and nothing more. It does not include the employer's matching FICA, the failure-to-deposit penalties, or the interest that piled up on the business account. Check Form 2751 against this table before you assume the number is right:

| Payroll tax item | Inside the TFRP? | Who can be made to pay |

|---|---|---|

| Federal income tax withheld from paychecks | Yes | You personally + the business |

| Employees' share of Social Security & Medicare | Yes | You personally + the business |

| Employer's matching share of FICA | No | Business only |

| Failure-to-deposit and late-filing penalties on the 941s | No | Business only |

| Interest accrued on the business account | No | Business only |

| FUTA unemployment tax (Form 940) | No | Business only |

A worked example (hypothetical). Say your company fell three quarters behind on 941 deposits. Each quarter, the payroll withheld $6,200 in federal income tax, $3,400 in employee Social Security, and $800 in employee Medicare — $10,400 of trust-fund money per quarter. Across three quarters, that's $31,200 of trust-fund taxes, and that's the figure Letter 1153 proposes against you personally.

Meanwhile the business's total 941 bill might be near $47,000 once you add the employer's $12,600 matching FICA and roughly $3,200 in deposit penalties and interest. That $15,800 gap stays with the company. If Form 2751 shows a number closer to $47,000 than $31,200, the revenue officer's math includes amounts the law doesn't allow — and that alone is grounds to appeal. The overall 941 mess is a separate fight; see 941 back taxes for the business-side playbook.

One more number that matters while the business still operates: voluntary payments can be designated. If the company sends the IRS $10,000 and designates it in writing to the trust-fund portion of the oldest quarter, your personal exposure in the example drops from $31,200 to $21,200. Levied or seized funds can't be designated — which is another reason to act while payments are still voluntary.

Do you have a defense? "Responsible" and "willful," decoded

The IRS must prove two things to make the penalty stick: you were a responsible person, and you acted willfully. Beat either element and the proposal fails as to you.

Responsible is about power, not titles. Did you sign checks, control the bank account, decide which creditors got paid, hire and fire, or sign the 941s? A silent investor with a fancy title may not be responsible; a bookkeeper who controlled disbursements may be. The Form 4180 answers you already gave are the government's main evidence here — your appeal is the chance to put them in context.

Willful doesn't mean malicious. It means you knew (or recklessly ignored) that the withheld taxes were unpaid and paid anyone else anyway — rent, suppliers, even net payroll. That's why "I was keeping the doors open" is not a defense; the IRS reads it as choosing other creditors over the Treasury.

Defenses that genuinely work in appeals:

- No real authority. You had a title or signature card but needed someone else's approval to move money — and can show it with emails, bylaws, or bank records.

- You learned late. Willfulness starts when you knew. If deposits were missed before you took over the books, quarters before your knowledge date may fall out of the penalty.

- Provider fraud. If a payroll company took your deposits and never paid the IRS, that fact pattern can defeat willfulness — if you acted once you discovered it.

- Lender control. A bank sweeping the account or dictating disbursements under a loan agreement can undercut both elements.

- The math is wrong. Wrong quarters, unposted payments, or non-trust-fund amounts folded into Form 2751.

- Time-barred quarters. The IRS generally must assess the TFRP within three years of the April 15 following the year the quarters fall in — but this three-year clock assumes the 941s were actually filed on time; a late-filed return starts the clock at the actual filing date, and if returns were never filed (or were fraudulent) there is no assessment deadline at all. Old quarters on Form 2751 deserve a statute check.

The broader question of who is personally liable for payroll taxes — officers, owners, check-signers, outside accountants — has its own guide. What matters here: the appeal you file in the next 60 days is where these defenses get decided.

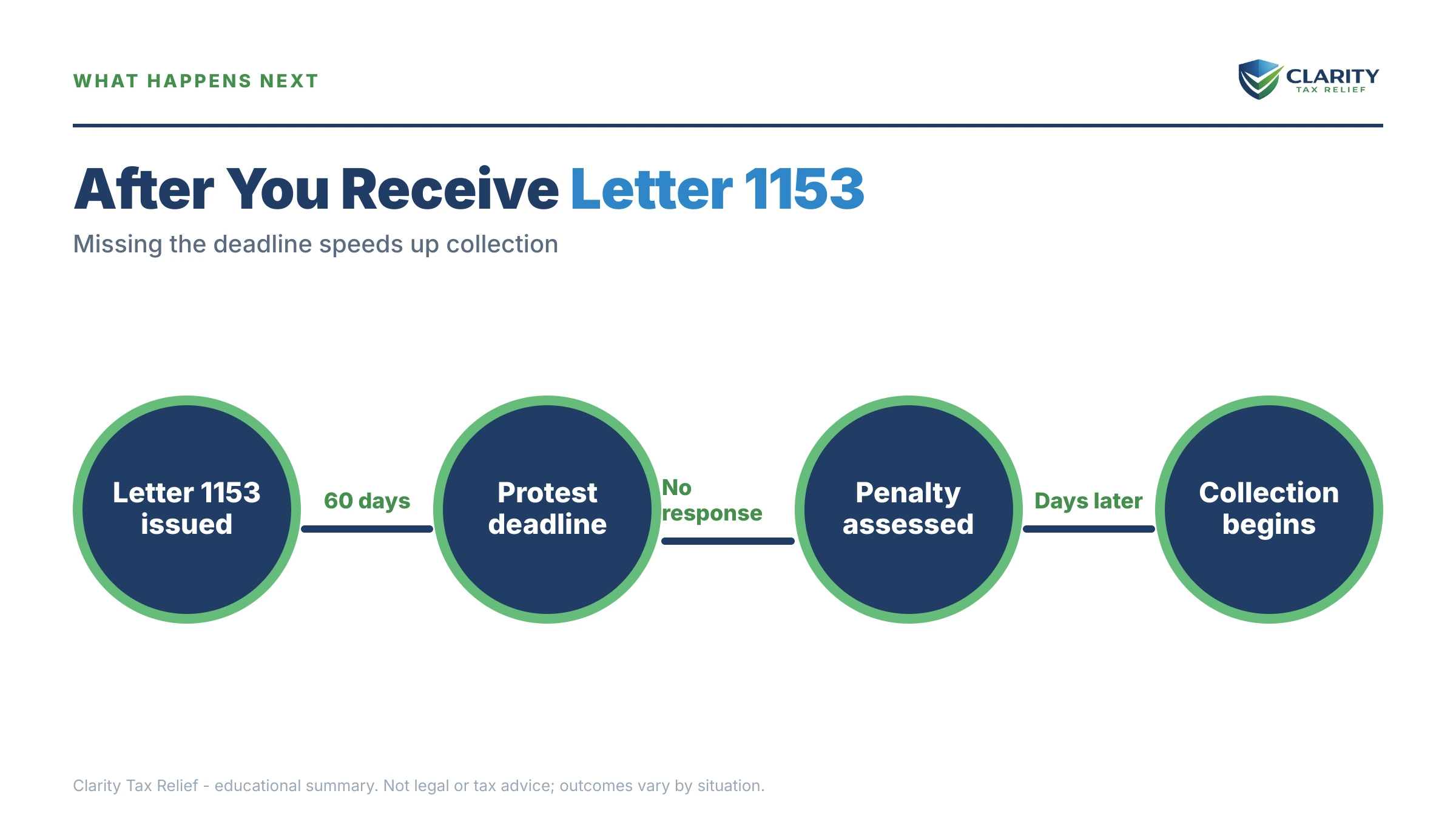

What happens if you ignore Letter 1153

If you do nothing for 60 days, the IRS assesses the Trust Fund Recovery Penalty against you as an individual — and from that moment the debt behaves like personal tax debt with a revenue officer already attached. The sequence runs:

- Day 60 passes. Your right to appeal the proposal lapses. The IRS assesses the full trust-fund amount on your personal account.

- Interest starts. The TFRP carries no interest before assessment — but from the assessment date, interest accrues on the full balance at the federal underpayment rate. You can estimate how fast interest compounds with our Penalty & Interest Calculator.

- You get billed, personally. Collection notices now come in your name, not the company's. A federal tax lien can be filed against everything you own — your home, your vehicles, your receivables if you're running a new business.

- Final notice of intent to levy. A Letter 1058 or LT11 starts a 30-day clock and your Collection Due Process rights (requested on Form 12153). Important: because Letter 1153 already gave you a chance to dispute liability, a CDP hearing at this stage generally can't re-argue whether you owe it — only how it gets collected.

- Levy. Personal bank accounts (with the 21-day hold), wages, and other income sources become fair game until the debt is resolved or the 10-year collection statute runs from assessment.

Two things make the TFRP uglier than ordinary tax debt. It survives bankruptcy — trust-fund taxes are priority, nondischargeable debts in both Chapter 7 and Chapter 13. And closing the company doesn't help; the assessment follows you, not the entity, as our guide to payroll tax debt after a business closes explains. In 2026, with IRS staffing down sharply, reaching a human is harder than ever — but assessment and levy run on systems that never stopped.

Holding a Letter 1153 and Form 2751 right now?

The 60-day window is the only stage where the trust fund penalty can be fought before it becomes your personal debt. Get your Letter 1153 reviewed free before the window closes — an experienced tax professional will check the responsibility case and the math, and map your strongest response.

Your options after Letter 1153, by situation and amount

Every path forward starts with one decision inside the 60 days: agree (sign Form 2751) or dispute (file a written appeal). Here is the full sequence you're inside, then the realistic options at each amount level:

| Stage | What arrives | Your window |

|---|---|---|

| Investigation opens | Letter 3164 / revenue officer contact | Cooperate carefully; facts gathered here become evidence |

| Interview | Form 4180 responsible-person interview | Scheduled by the revenue officer |

| Proposal — you are here | Letter 1153 + Form 2751 | 60 days to appeal (75 if abroad) |

| Assessment | Penalty billed on your personal account | Interest begins; lien filing becomes possible |

| Final notice | Letter 1058 / LT11 | 30 days to request a CDP hearing (Form 12153) |

| Enforcement | Lien, bank levy, wage levy | Runs until resolved or the 10-year statute expires |

If you dispute, the letter itself tells you the format: for amounts of $25,000 or less per period, a simple small case request; above that, a formal written protest stating the facts, the law, and a penalties-of-perjury declaration. Either way it goes to the address on the letter, and the case moves from the revenue officer to the IRS Independent Office of Appeals — a separate office whose job is to weigh hazards of litigation, not to collect. Our guide to trust fund recovery penalty defense walks through building the protest itself.

If you agree — or if the appeal only partially succeeds — the resolution options depend mostly on the dollar amount:

| Proposed amount | Appeal format | Realistic paths if assessed |

|---|---|---|

| $25,000 or less per period | Small case request | Full pay; streamlined personal payment plan; designated business payments to shrink it first |

| $25,001–$50,000 | Formal written protest | Personal installment agreement up to 72 months; hardship (CNC) if income can't support payments |

| $50,001–$100,000 | Formal written protest | Plan with financial disclosure (Form 433 series); CNC; Offer in Compromise only with genuine inability to pay |

| Over $100,000 | Formal written protest | Revenue-officer-managed resolution with full asset review; experienced representation strongly advised |

Back to the $31,200 example: assessed personally and paid over a 72-month agreement, that's roughly $433 a month ($31,200 ÷ 72) before interest — realistically closer to $475–$500 once accruing interest is folded in. If the business is still operating and can commit $1,500 a month in designated trust-fund payments, your personal balance shrinks before you ever set up a plan. If the business is gone and your household budget genuinely can't cover payments, Currently Not Collectible status or — rarely — a business offer in compromise on payroll debt enters the picture. For an operating company, the in-business trust fund rules in our business payroll tax payment plan guide usually matter more than anything on your personal side.

Two options that do not work here, despite what you may read elsewhere: first-time penalty abatement doesn't reach the TFRP, because this isn't a late-filing or late-payment penalty — it's the withheld tax itself, restated as a penalty against you. Relief from the TFRP comes from winning on responsibility, willfulness, or the math, as covered in trust fund penalty abatement. And Tax Court is off the table: no 90-day letter exists for the TFRP. After assessment, the only litigation route is the divisible-tax path — pay the trust-fund tax for one employee for one quarter, file Form 843 as a refund claim, and sue in federal district court if it's denied.

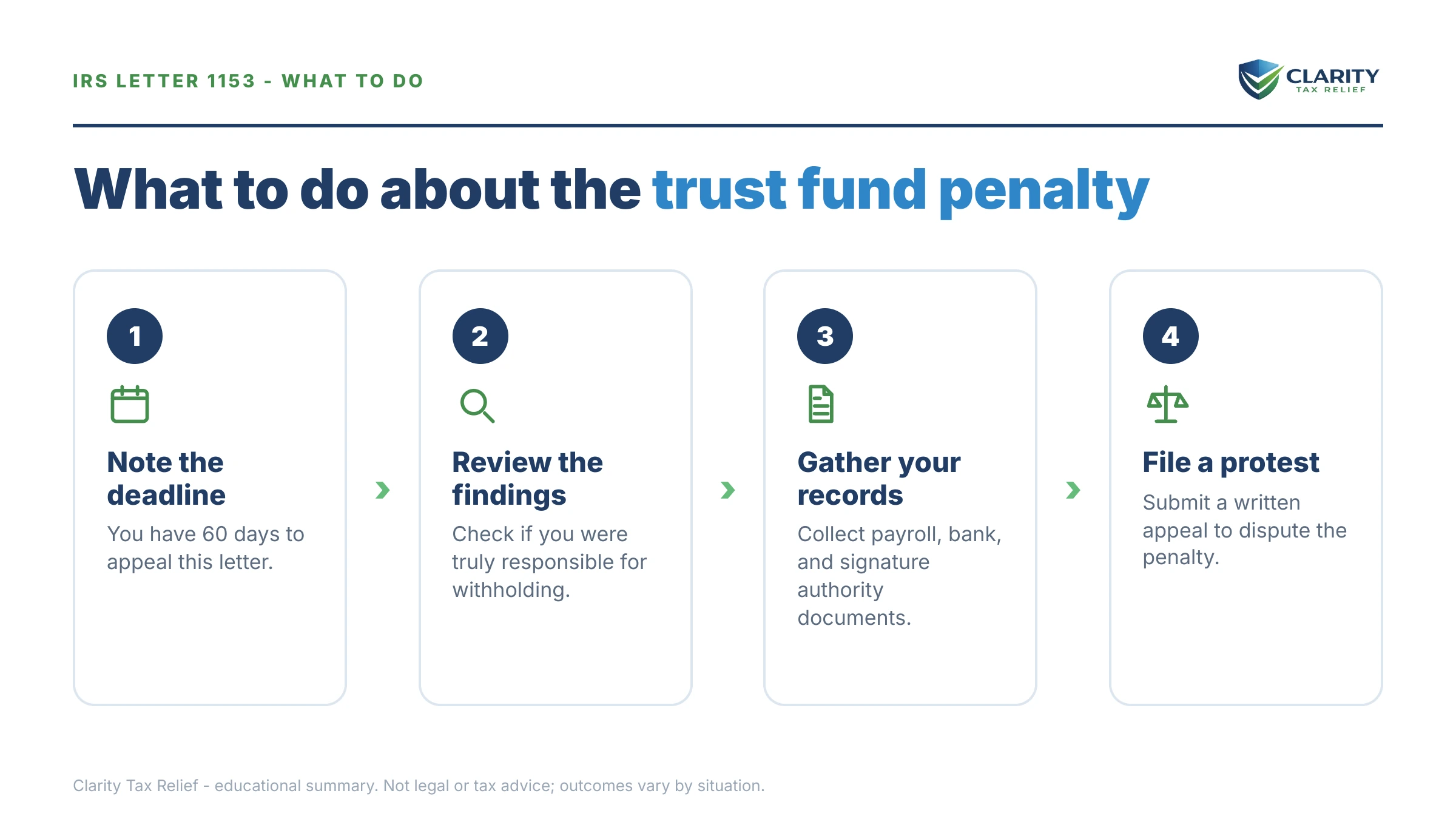

How to respond, step by step

- Calendar your deadline. Count 60 days from the date printed on Letter 1153 — not the day it arrived — and work backward from a week before it.

- Verify the numbers. Pull the 941s and payroll records for each quarter listed on Form 2751 and confirm the trust-fund math is right.

- Decide agree or dispute. Sign Form 2751 only if responsibility, willfulness, and the dollar amounts are all correct; otherwise prepare an appeal.

- File your written appeal before day 60. Use a small case request or formal protest per the letter's instructions, and mail it to the address on the letter with proof of delivery.

- Keep current payroll taxes perfect. Deposit every new payroll tax on time — fresh trust-fund debt undercuts any appeal or resolution.

- Get experienced help lined up. An experienced tax professional can shape the responsibility and willfulness record now, while it can still change the outcome.

When you can handle Letter 1153 yourself — and when you shouldn't

You can reasonably handle this alone if three things are all true: you were unmistakably the person who controlled the money, the Form 2751 figures match your own payroll records, and you can full-pay or comfortably afford a payment plan on the amount. In that case, signing Form 2751 and arranging payment directly through IRS.gov/payments is a legitimate, cheap resolution — no firm required.

Experienced help changes outcomes in the situations Appeals actually argues about: you dispute being responsible or willful; several people at the company are pointing at each other (whoever builds the better record usually shifts the burden); the Form 4180 interview already went badly; the business is still operating and needs payroll protected while the personal case runs; or the proposed amount is large enough that a lien would wreck financing you depend on. TFRP cases are won on documents — bank signature authority, board minutes, emails about who decided which bills got paid — assembled before Appeals ever sees the file. If a revenue officer is actively working your case, our guide to a revenue officer visit over payroll taxes covers that dynamic too.

Terms on your Letter 1153, decoded

- Trust fund taxes: the money withheld from employee paychecks — income tax plus the employees' FICA share — that the business held "in trust" for the government.

- Responsible person: anyone with the status, duty, and authority to decide which creditors got paid, regardless of job title.

- Willfulness: knowing the withheld taxes were unpaid and paying anyone else anyway; no bad intent required.

- Form 2751: the consent form enclosed with Letter 1153 — signing it agrees to the assessment and waives your appeal.

- Divisible tax: the rule that lets you litigate the TFRP by paying just one employee's tax for one quarter, then suing for a refund.

- CSED: the collection statute expiration date — the IRS has 10 years from assessment to collect, though appeals, offers, and bankruptcy pause the clock.

If you're inside your 60 days and unsure whether your facts support a protest, a free case review before you sign or file anything costs nothing and can't hurt your appeal.

Letter 1153 questions, answered

What is IRS Letter 1153?

Letter 1153 is the IRS's formal proposal to assess the Trust Fund Recovery Penalty against you personally for payroll taxes your business withheld from employees but never paid over. It arrives with Form 2751, which shows the proposed amount, and it starts a 60-day window to appeal. It is the last step before the debt legally becomes yours as an individual.

How long do I have to respond to Letter 1153?

You have 60 days from the date printed on the letter to file a written appeal — 75 days if the letter was addressed to you outside the United States. The clock runs from the letter's date, not the day you opened it. If you miss the window, the IRS assesses the penalty and your only remaining dispute route is paying a portion and suing for a refund.

Should I sign Form 2751?

Sign Form 2751 only if you agree you are a responsible person, you acted willfully, and the dollar figures are correct — signing consents to the assessment and gives up your appeal. Many people sign under pressure without checking whether the trust-fund math is even right. If any of the three elements is in doubt, appeal within the 60 days instead.

What happens if I ignore Letter 1153?

The IRS assesses the Trust Fund Recovery Penalty against you personally after the 60-day window closes. Interest then starts accruing, a federal tax lien can attach to your home and personal assets, and collection escalates to a final notice of intent to levy and then bank and wage levies. You also lose the ability to argue liability with the IRS Independent Office of Appeals.

Can I take Letter 1153 to Tax Court?

No — the Trust Fund Recovery Penalty is an assessable penalty, so there is no 90-day Tax Court ticket like an audit deficiency gets. Your dispute routes are the 60-day appeal to the IRS Independent Office of Appeals, or, after assessment, paying the trust-fund tax for one employee for one quarter, filing Form 843 for a refund, and suing in federal court if it's denied.

How much of my business's payroll tax debt can the IRS collect from me personally?

Only the trust-fund portion: the federal income tax withheld from employee paychecks plus the employees' share of Social Security and Medicare. The employer's matching FICA, the failure-to-deposit penalties, and the interest on the business account stay with the business. On a typical 941 balance, the trust-fund portion often runs roughly 60 to 70 percent of the total.

Can the IRS assess the Trust Fund Recovery Penalty against more than one person?

Yes. Every person who was responsible and willful can be assessed 100 percent of the same trust-fund amount — owners, officers, bookkeepers, even outside check-signers. The IRS collects the money only once in total, but it pursues everyone simultaneously and lets payments from any of them reduce the shared balance. Who ultimately pays often turns on who fights the proposal within the 60 days.

Does bankruptcy wipe out the Trust Fund Recovery Penalty?

No. Trust-fund taxes are priority debts that survive both Chapter 7 and Chapter 13 discharge, no matter how old they are. Bankruptcy can pause collection while the case is open, and a Chapter 13 plan can force a payment structure, but the penalty itself does not go away. That permanence is why fighting the proposal at the Letter 1153 stage matters so much.

Can I settle a Trust Fund Recovery Penalty with an Offer in Compromise?

Sometimes, but the IRS scrutinizes trust-fund offers hard because the money was employees' withholding. You must show that the amount offered is the most the IRS could ever collect from your income and assets; per IRS data, the IRS accepted roughly 1 in 5 offers overall in FY2024, and payroll-based offers face extra review. A payment plan or hardship status is the more common outcome.

My payroll company or bookkeeper caused this — am I still on the hook?

Possibly. Liability turns on whether you were responsible and willful, not on who made the bookkeeping error. If a payroll provider took your deposits and never sent them to the IRS, that fraud is a genuine defense worth raising in your appeal. But if you learned deposits were missed and kept paying other bills first, the IRS treats that as willfulness even though someone else caused the original miss.

Your next 24 hours

- Find the date on Letter 1153 — top right of the first page — and count 60 days forward. Write that date somewhere you can't miss it; every option in this article lives inside it.

- Gather your evidence: Form 2751, the 941s for the quarters listed, bank signature cards, and anything showing who actually decided which bills got paid.

- Get a free case review before the 60-day window closes — send us a photo of the letter through the 2-minute form or call (888) 825-7779. An experienced tax professional will tell you whether you have a responsibility or willfulness defense, and what the realistic path looks like if you don't.

Primary sources: the IRS's own explanation of employment taxes and the Trust Fund Recovery Penalty, payment options at IRS.gov/payments, and independent help through the Taxpayer Advocate Service if IRS process itself is causing you harm.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.