Payroll & Trust Fund Taxes

Form 4180 Interview: The "Responsible Person" Interview — How to Prepare (2025)

The short answer: the Form 4180 interview is how the IRS decides whether to hold you personally liable for a business's unpaid payroll taxes. A revenue officer asks who controlled the money and who knew taxes weren't being paid. Your answers shape whether the Trust Fund Recovery Penalty lands on you — so prepare carefully and consider representation.

Got a Form 4180 appointment letter?

Don't walk into that interview alone. An experienced tax professional can review the facts, sit in under power of attorney, and help you avoid answers that hand the IRS a personal liability — free, confidential, no pressure.

⏱ Your deadline: there's no fixed clock on the interview itself, but the revenue officer is working a case and will set an appointment date. Once they propose the penalty, you'll get Letter 1153 with Form 2751 — and from that date you have just 60 days to file a written appeal before the penalty becomes a personal debt.

Why the IRS wants a Form 4180 interview

When a business withholds income tax and Social Security and Medicare from employee paychecks, that money isn't the company's — it's held "in trust" for the government. If the business files its Form 941 payroll returns but doesn't send in those withheld dollars, the IRS can come after the people behind the business personally. That's the Trust Fund Recovery Penalty (TFRP), and the Form 4180 interview is the fact-finding step the IRS uses to decide who pays it.

Form 4180 is officially titled the "Report of Interview with Individual Relative to Trust Fund Recovery Penalty or Personal Liability for Excise Taxes." A revenue officer fills it out by asking you a fixed set of questions. You can read the IRS's overview of the process on the Trust Fund Recovery Penalty page.

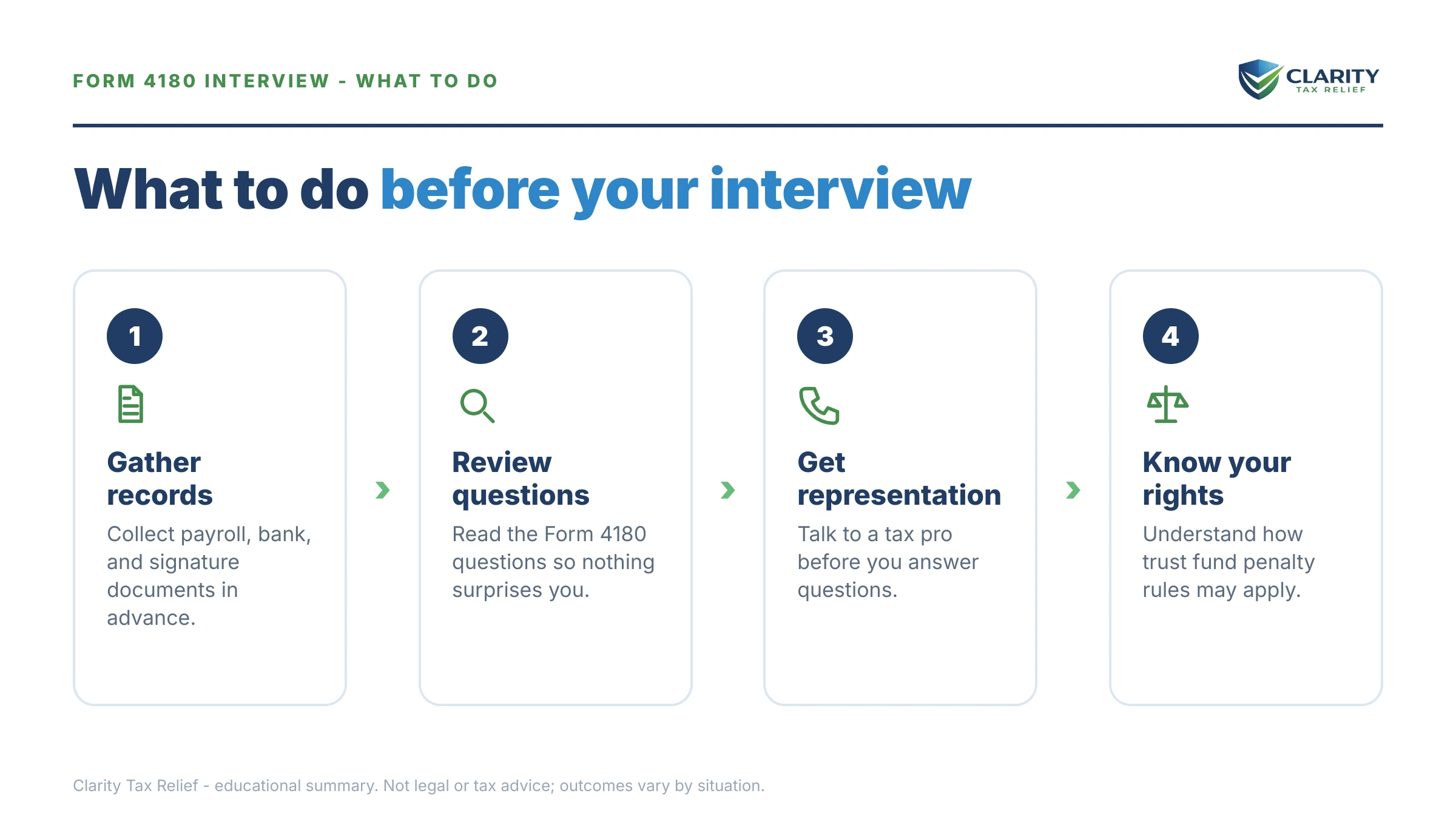

The interview exists because the law sets two tests. To be hit with the penalty, you must be both a responsible person (someone with control over the company's finances) and have acted willfully (you knew the taxes were due and chose to pay other bills instead). Every question on Form 4180 is built to prove or disprove one of those two things.

What happens if you ignore the request

This is a personal-liability investigation, and skipping it doesn't make it go away. Here's how the case typically moves:

- Form 4180 interview — the revenue officer gathers facts. You are here. Nothing is assessed yet.

- Determination — using your answers plus bank signature cards, canceled checks, and corporate records, the officer decides who was responsible and willful.

- Letter 1153 & Form 2751 — the IRS proposes the penalty against you by name. You get 60 days to appeal in writing.

- Assessment — if you don't appeal or pay, the trust fund amount is assessed as your personal tax debt, separate from the company.

- Personal collection — from there the IRS can file a federal tax lien, levy your bank account, and garnish your wages personally — even if the business is closed or bankrupt.

If you don't participate, the revenue officer simply builds the case from everyone else's answers and the paper trail. Refusing to engage often makes you look like the obvious target.

What questions are on Form 4180

The form runs through your role at the company. Expect questions like these, grouped by what the IRS is really testing:

- Authority (responsibility): Could you sign checks? Could you authorize payments? Could you hire and fire employees? Did you have a financial stake in the business?

- Day-to-day control: Who decided which creditors got paid when money was tight? Who prepared payroll? Who made the federal tax deposits? Who signed the Form 941 returns?

- Knowledge (willfulness): When did you first learn the taxes weren't paid? Once you knew, did the company keep paying other bills — rent, vendors, your own salary — instead of the IRS?

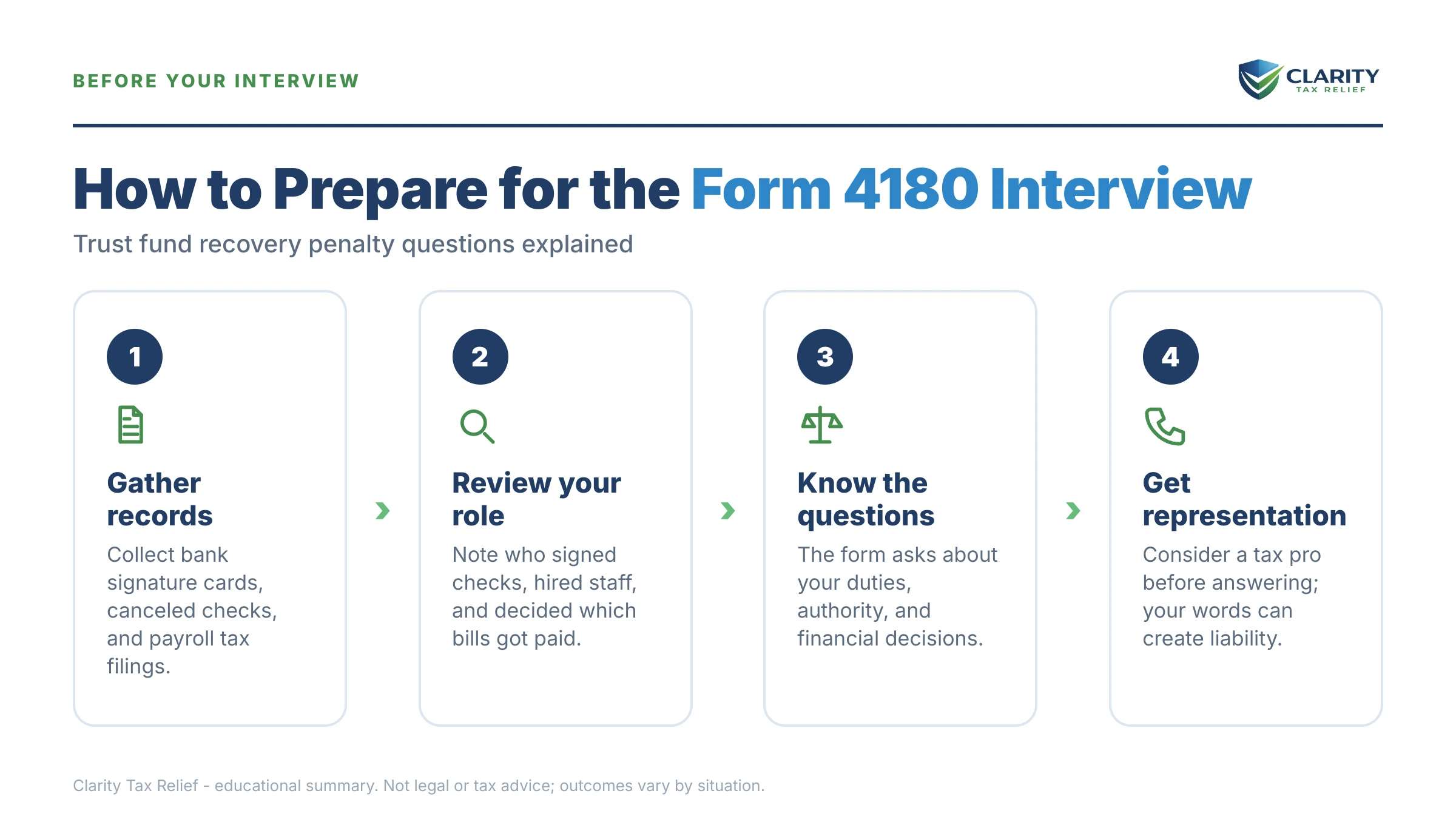

The willfulness questions are the most dangerous. "Willful" doesn't mean evil intent — it just means you knew, or should have known, and let other payments go first. A casual answer like "I figured we'd catch up once cash flow improved" can be read as an admission. You can review the actual questions on the IRS Form 4180 page before any interview.

Your options for handling the interview

You have more control over this than the appointment letter suggests:

- Bring a representative. An enrolled agent, CPA, or attorney can attend with you under Form 2848, Power of Attorney. With authorization on file, your representative can speak for you and, in many cases, respond to the form so you don't sit across from the revenue officer alone.

- Answer in writing. The Form 4180 doesn't have to be done as a live interview. Many cases are handled by completing the form on paper, which gives you time to think and check records before committing to an answer.

- Document your limits. If you truly lacked check-signing authority or were shut out of financial decisions, gather the proof — board minutes, signature cards, emails — that shows it. Facts win these cases, not arguments.

- Don't volunteer extra. Answer each question honestly and completely, then stop. Long explanations often hand the IRS the willfulness it's looking for.

One honest caution: never lie or hide records. The penalty is a civil matter, but knowingly false statements can turn a bad situation into a far worse one. The goal is accurate, careful, well-prepared answers — not deception.

How to prepare for the Form 4180 interview, step by step

- Pull the records first. Get bank signature cards, canceled checks, the corporate org chart, board minutes, and copies of the unpaid Form 941 payroll returns. Know what the IRS already has before you answer.

- Map your actual role. Write down exactly what you could and couldn't do — and when. Roles change over time, and the penalty only applies to the quarters where you were responsible and willful.

- Identify who else was involved. The penalty can be shared among several people. Knowing who controlled the checkbook matters for your defense.

- Decide on representation early. Talk to an experienced tax professional before the appointment, not after. The interview answers are hard to walk back.

- Practice the hard questions. Especially the willfulness ones — when you knew, and what got paid after. Calm, accurate, short answers protect you.

- Keep copies of everything you provide and a record of what was asked.

Form 4180 interview questions, answered

Do I have to do the Form 4180 interview?

You are not legally required to sit for the Form 4180 interview yourself. You can have an authorized representative answer in your place, or the form can be completed in writing. Declining to be interviewed in person is not an admission of guilt — but ignoring the request entirely lets the IRS build its case using everyone else's answers.

What questions are on Form 4180?

Form 4180 asks who could sign checks, who decided which bills got paid, who handled payroll and federal tax deposits, who could hire and fire, and whether you knew the trust fund taxes weren't being paid. Every question is aimed at the two legal tests for the Trust Fund Recovery Penalty: responsibility and willfulness.

Can I bring a representative to the Form 4180 interview?

Yes. You can have an enrolled agent, CPA, or attorney represent you using Form 2848, Power of Attorney. With a valid authorization on file, your representative can attend the interview, answer procedural questions, and in many cases respond to the Form 4180 on your behalf so you don't face the revenue officer alone.

What happens after the Form 4180 interview?

The revenue officer uses your answers, bank signature cards, and corporate records to decide whether to propose the Trust Fund Recovery Penalty against you. If they do, you'll receive Letter 1153 with Form 2751, giving you 60 days to appeal before the penalty is assessed as a personal debt.

How much is the Trust Fund Recovery Penalty?

The penalty equals 100% of the trust fund portion of the unpaid payroll taxes — the income tax and the employee's share of Social Security and Medicare that was withheld from paychecks but never sent to the IRS. It does not include the employer's share or late-payment penalties on the business account.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.