IRS Penalties

Trust Fund Recovery Penalty: Who Is Personally Liable and How to Fight It in 2026

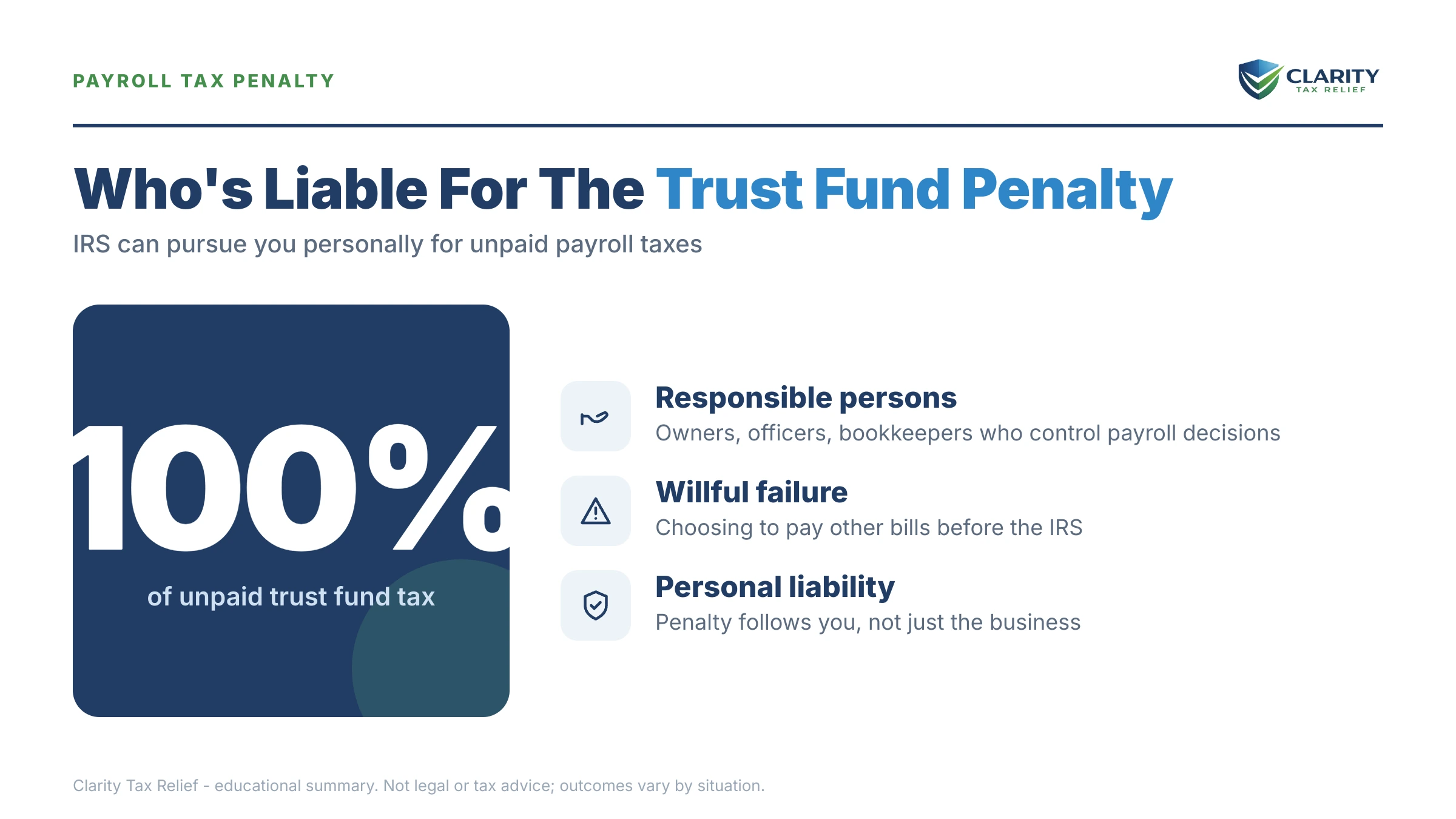

The short answer: the trust fund recovery penalty (TFRP) lets the IRS collect a business's unpaid trust fund taxes — the income tax withheld from paychecks plus the employees' share of Social Security and Medicare — from you personally, at 100 cents on the dollar. It targets any "responsible person" who willfully failed to pay, and it survives business closure and bankruptcy.

You didn't own the company. You ran the office, you signed some checks, and now a revenue officer wants to interview you about payroll taxes the business never sent in — or a proposal is already on your table naming you for the debt. That fear of a business problem following you home is exactly what §6672 is built on. But the TFRP has a two-part legal test, a formal protest window, and more losing IRS positions than almost any other penalty — this page maps every stage and every exit.

The proposal arrives as Letter 1153 with Form 2751 stapled behind it, and the amount on that form is usually smaller than the business's full payroll debt for a specific reason. The image below shows you exactly what this paperwork looks like and where to find the figure and date that control everything that follows.

⏱ Your deadline: if you're holding Letter 1153, you have 60 days from the date printed on it to file a written protest. Miss that window and the IRS assesses the trust fund recovery penalty against you personally — after that, you're fighting collection instead of preventing assessment.

Why the IRS is coming after you for the business's payroll taxes

The trust fund recovery penalty under IRC §6672 makes an individual personally liable for 100% of a business's unpaid trust fund taxes. Here's the logic: every payday, the employer takes federal income tax and the employees' share of Social Security and Medicare out of workers' paychecks. That money never belonged to the business — the law says it was held "in trust" for the government on the employees' behalf.

When the business spends that money on rent, suppliers, or net payroll instead of sending it to the Treasury, the IRS doesn't treat it as a business falling behind. It treats it as trust money that was diverted — and it pierces straight through the LLC or corporation to the humans who let it happen. Whether the entity is open, sold, or dissolved changes nothing; payroll tax debt survives a closed business by design.

Two things must both be true before the IRS can assess you: you were a responsible person, and your failure to pay was willful. Each word has a specific legal meaning, and each is a separate place the IRS's case can fail. (For how ordinary late-filing and late-payment penalties compound — a different animal entirely — see how much IRS penalties on back taxes really grow.)

Who is a "responsible person" — and what "willful" really means

A responsible person is anyone with the status, duty, and authority to decide which creditors get paid — regardless of job title or ownership. The IRS builds its list from bank signature cards, Form 941 signatures, corporate minutes, and interviews. The usual suspects:

- Owners, officers, and partners — the default targets, even if they "left payroll to someone else."

- Controllers, CFOs, and office managers — non-owners with real control over the checkbook.

- Bookkeepers and check signers — exposed when they had genuine discretion, protected when they only executed orders. If this is you, read whether a bookkeeper can be personally liable to the IRS.

- Outside parties — lenders or family members who effectively controlled which bills got paid.

"Willful" is the word that surprises people most. It does not require fraud or bad intent. Willfulness means you knew the taxes were unpaid and paid anyone else instead — the landlord, a vendor, even the employees' net wages. "I was keeping the business alive" is, legally, an admission of willfulness, not a defense. What can defeat willfulness: you genuinely didn't know until after you left, you had no funds under your control once you learned, or a payroll company took the deposits and didn't pay the taxes without your knowledge.

One narrow statutory carve-out: unpaid, volunteer board members of tax-exempt organizations who serve honorarily and don't participate in day-to-day financial operations have limited protection under §6672(e). For the full liability map by role — owner, officer, spouse, check signer — see who is personally liable for payroll taxes.

How much of the payroll debt becomes a trust fund recovery penalty

The trust fund recovery penalty covers only the trust fund portion of the 941 debt — never the employer's own share, and never the business's penalties and interest. That distinction is why the number on your Form 2751 is smaller than the balance the business owes, and why checking the IRS's breakdown is always step one.

| Component of the 941 debt | Part of the TFRP? |

|---|---|

| Federal income tax withheld from employee paychecks | Yes — trust fund |

| Employees' share of Social Security and Medicare (FICA) | Yes — trust fund |

| Employer's matching share of Social Security and Medicare | No — stays with the business |

| Federal unemployment tax (Form 940 / FUTA) | No — stays with the business |

| Failure-to-deposit and late-filing penalties on the 941s | No — stays with the business |

| Interest accrued on the business account | No — stays with the business |

A worked example (hypothetical). Say you were the W-2 office manager of a small company that ran three quarters without making payroll deposits, and the total 941 balance is $34,600. The breakdown:

- Federal income tax withheld from paychecks: $14,800

- Employees' share of Social Security and Medicare: $9,000

- Trust fund portion — your maximum personal exposure: $14,800 + $9,000 = $23,800

- Employer matching FICA ($9,000) plus deposit penalties and interest ($1,800) = $10,800 that can only be collected from the business.

So the IRS can propose $23,800 against you — not $34,600. If it's assessed and you don't dispute it, a $23,800 balance fits a streamlined installment agreement: spread over the maximum 72 months, that's roughly $23,800 ÷ 72 ≈ $331 per month before interest. No additional penalties stack on an assessed TFRP, but interest runs from the assessment date, so paying faster than the minimum always costs less — you can estimate the accrual with our Penalty & Interest Calculator.

One more wrinkle worth knowing: any payment applied to the trust fund portion — by the business, by you, or by any other responsible person — reduces the TFRP for everyone. A still-operating business can make voluntary payments designated in writing to the trust fund portion first, shrinking the owners' and managers' personal exposure with every dollar.

What happens if you ignore the TFRP investigation

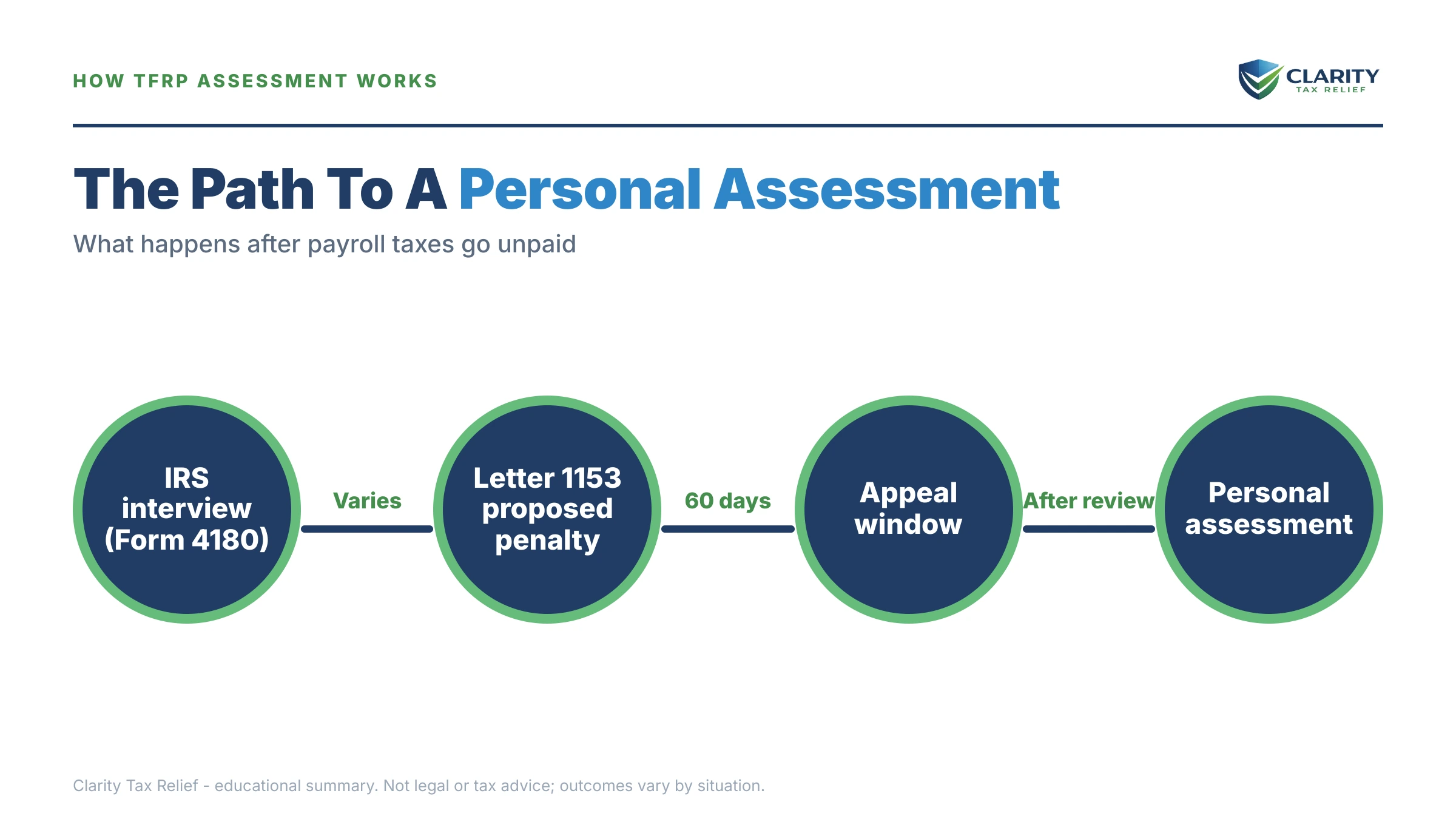

A TFRP case moves through a fixed sequence of documents, and each one closes a door the previous one left open. Silence never stalls it — the IRS simply assumes the worst version of the facts and assesses. The sequence:

- Letter 3164 or a revenue officer contact — the investigation opens. The RO pulls the business's 941s, bank signature cards, and canceled checks to build a list of candidates.

- The Form 4180 interview — a structured, recorded-in-writing interview about who had authority and who knew what, when. Your answers become the government's primary evidence. Skipping it doesn't help either — the IRS decides on the paper record alone.

- Letter 1153 with Form 2751 — the formal proposal of the penalty against you, with the trust fund amount per quarter. Your 60-day protest clock starts on the letter's date.

- Assessment — if you don't protest (or lose the appeal), the TFRP posts to your personal IRS account as a civil penalty, each unpaid quarter as its own assessment, and interest begins to run.

- Personal collection — the same machine that chases any individual debt: balance-due notices, then intent-to-levy notices, then an LT11 final notice giving you 30 days to request a Collection Due Process hearing on Form 12153 before wage garnishment, bank levies, and a federal tax lien against your home. If your combined seriously delinquent debt tops $66,000 (the 2026 threshold), passport certification can follow.

Timing matters more in 2026 than ever: IRS staffing fell roughly 27% in 2025, which makes humans harder to reach — but assessment and levy are automated, and the automation never stopped. The table below is the deadlines-and-rights map worth screenshotting.

| Document / stage | What it means | Your window — and what expires |

|---|---|---|

| Letter 3164 / revenue officer contact | TFRP investigation opened; evidence gathering begins | No fixed deadline — but everything you say and hand over now shapes the case. Prepare before engaging. |

| Form 4180 interview request | The responsibility-and-willfulness interview | Scheduled by the RO. You may have representation present; unprepared answers are the most common self-inflicted wound. |

| Letter 1153 + Form 2751 | Proposed TFRP assessment against you personally | 60 days from the letter date to file a written protest (75 if addressed outside the U.S.). Miss it and pre-assessment appeal rights are gone. |

| Assessment + notice and demand | The penalty is now your personal debt; interest runs | Pay or arrange payment promptly; the 10-year collection statute starts here. |

| LT11 / final notice of intent to levy | Levy on wages and bank accounts is authorized next | 30 days to request a CDP hearing via Form 12153. Miss it and you lose the right to Tax Court review of the collection action. |

Named in a TFRP investigation — or holding Letter 1153?

The 60-day protest clock started on the date printed at the top of your letter, and the Form 4180 interview is not a conversation to walk into cold. Get your TFRP paperwork reviewed free before the window closes — an experienced tax professional will tell you which stage you're in and whether the IRS's case against you actually holds.

Your options before and after assessment

Every TFRP has two distinct fights: whether you owe it at all (won before or shortly after assessment), and how to resolve it if you do (a personal collection matter like any other). Which tools are open depends entirely on which stage you're in:

| Option | Best fit | Upfront cost | Typical timeline |

|---|---|---|---|

| Written protest to Appeals (within 60 days of Letter 1153) | You dispute responsibility, willfulness, or the amounts | $0 (plus representation if you hire it) | Often several months in Appeals; assessment is on hold meanwhile |

| Pay in full | Small balance you agree with | The balance itself | Immediate — stops interest and all escalation |

| Installment agreement | Assessed balance you can pay monthly (up to $50,000 qualifies for up to 72 months online) | Setup fee varies by method; reduced or waived for low income | Can be set up in one online session; interest continues |

| Offer in compromise | Your own income and assets genuinely can't cover the debt | $205 fee + 20% down on lump-sum offers (both waived with low-income certification) | Many months; auto-accepted if the IRS doesn't decide within 2 years, with narrow exceptions — a returned or rejected offer stops the clock, and time during court disputes does not count |

| Currently Not Collectible | Paying anything would create genuine hardship | $0 (financial disclosure required) | Lasts until finances improve; interest accrues, CSED keeps running |

| Post-assessment refund claim (Form 843) + suit | You missed the protest window but have a strong liability defense | Payment of one quarter's tax for one employee, then the claim | The slowest path — months to years, potentially into federal court |

Fighting liability. The written protest within 60 days of Letter 1153 is the highest-value move in the entire process — it puts your case in front of the IRS Independent Office of Appeals before the debt ever touches your account. The winning arguments and how to frame them are covered in our guide to trust fund recovery penalty defense; if the penalty is already assessed, the reduction paths are in trust fund penalty abatement. Because the TFRP is a "divisible" tax, there's also a back door after assessment: pay the tax attributable to one employee for one quarter, file Form 843 as a refund claim, and if it's denied, sue for the refund in federal court — a real option for strong cases that missed the protest window, but the slowest and most expensive route on the board.

Resolving the balance. Once assessed, the TFRP behaves like any personal tax debt for payment purposes: installment agreements, hardship status, and — when the math supports it — an offer in compromise, explained in how an offer in compromise actually works. Two hard truths, though. It is never dischargeable in bankruptcy. And routine penalty relief doesn't touch it: first-time abatement and the new Automatic Exemption from Penalty (AEP) rolling out in summer 2026 apply to ordinary filing and payment penalties — including the business's own 941 penalties, where 941 penalty abatement may cut the entity's bill — but not to the §6672 penalty itself.

The clock. Collection of an assessed TFRP is limited to 10 years from the assessment date — a separate clock from the business's, pausable by an offer, appeal, or bankruptcy.

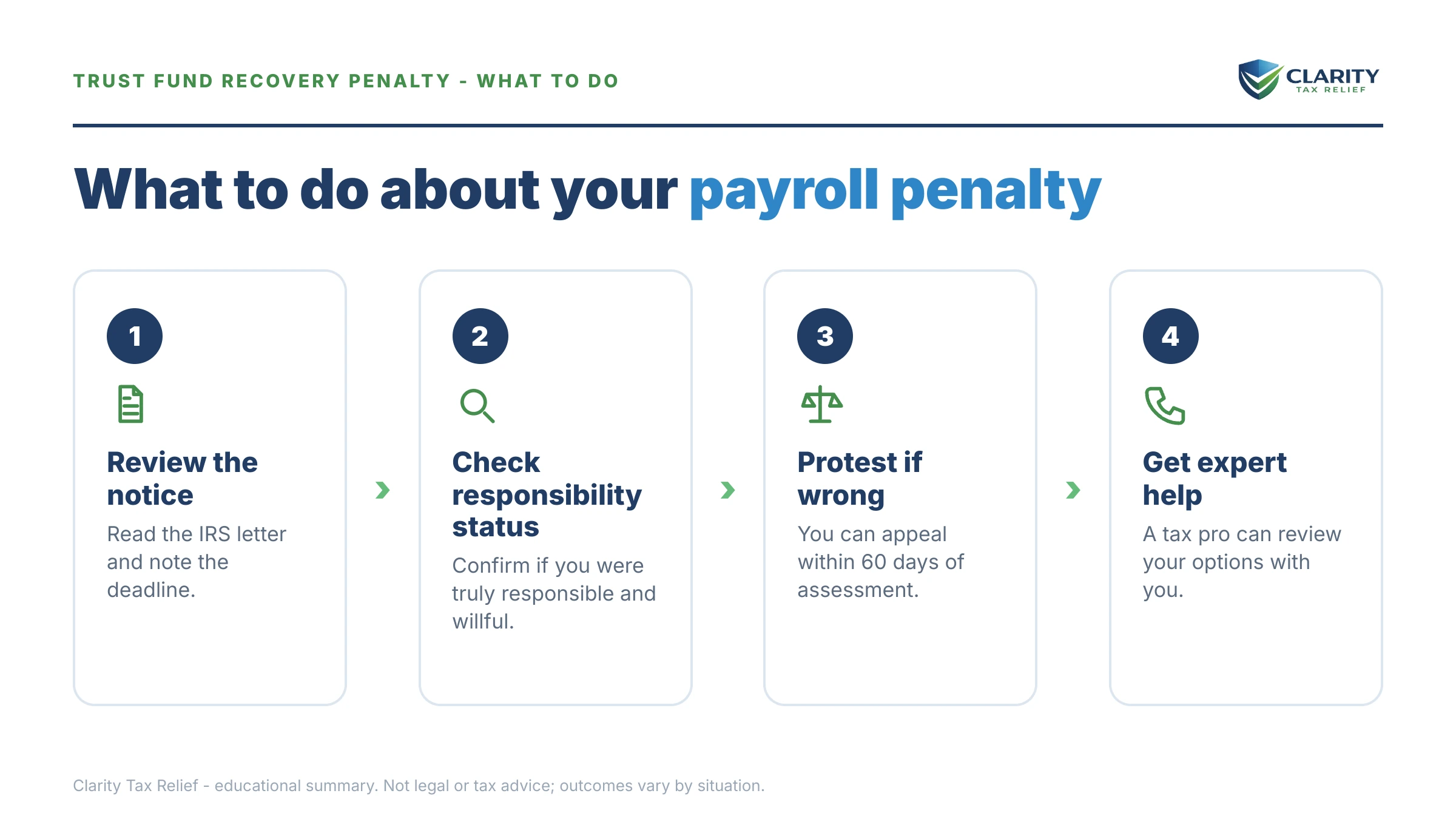

How to respond to a trust fund recovery penalty, step by step

- Identify your stage. Match the document in your hand — Letter 3164, a Form 4180 interview request, Letter 1153, or a personal balance-due notice — to the timeline above; each one changes your best move.

- Calendar the deadline. Write down the date printed on your letter and count forward — 60 days from Letter 1153 to file a protest, 30 days from an LT11 to request a CDP hearing.

- Gather your evidence. Pull bank signature cards, check registers, payroll records, corporate minutes, and emails showing who actually decided which bills got paid.

- Hold off on Form 2751. Don't sign the consent to assessment until someone who knows your facts has reviewed whether responsibility, willfulness, and the dollar figures are actually right.

- File your protest or pick a payment path. Before assessment, send a written protest to the address on Letter 1153; after assessment, set up an installment agreement, offer, or hardship status before enforcement starts.

- Get experienced representation if you're disputing it. TFRP cases are won on evidence and procedure — an experienced tax professional can handle the interview and protest so your own words don't become the IRS's case.

When you can handle this yourself — and when help changes the outcome

You can reasonably handle a TFRP alone when all three of these are true: you agree you were the person who controlled the money, the trust-fund math on Form 2751 matches the payroll records, and the balance is one you can pay in full or through a simple online installment agreement. In that case, verifying the breakdown and setting up payment at IRS.gov/payments may be all you need — no firm required.

Experienced help genuinely changes outcomes in the disputed and high-stakes versions: a Form 4180 interview is scheduled and your answers will be the IRS's evidence; you were a non-owner who signed checks at someone else's direction; several people are pointing fingers at each other and the RO is proposing against everyone; the proposed quarters may be outside the assessment statute; the business is still operating and at risk of pyramiding new quarters on top of old ones; or you're weighing an offer in compromise where the Reasonable Collection Potential math decides everything. These are evidence-and-procedure fights, and the record you build in the first weeks is usually the record you're stuck with. The IRS's own overview of the penalty is at its trust fund recovery penalty page, and if the process itself breaks down — deadlines ignored, hardship unaddressed — the Taxpayer Advocate Service exists precisely for that.

Terms on your TFRP paperwork, decoded

- Trust fund taxes — the money withheld from employee paychecks (income tax plus their share of FICA) that the business held "in trust" for the government.

- Responsible person — anyone with the status, duty, and authority to decide which creditors got paid; title and ownership are not required.

- Willfulness — knowing the taxes were unpaid and paying any other creditor instead; no bad intent or fraud is needed.

- Letter 1153 — the formal proposal of the TFRP against you, which starts your 60-day protest window.

- Form 2751 — the consent form attached to Letter 1153; signing it agrees to immediate assessment and waives your pre-assessment appeal.

- Civ Pen — how an assessed TFRP is labeled on your personal IRS notices and transcript; it means the §6672 penalty, not a new or different debt.

- CSED — the Collection Statute Expiration Date: 10 years from the date the TFRP was assessed against you, pausable by appeals, offers, and bankruptcy.

If any of these terms describes paperwork already sitting in your mailbox, a free TFRP case review — or a call to (888) 825-7779 — can tell you in minutes which stage you're in and which window is still open.

Trust fund recovery penalty questions, answered

Can the IRS really collect a business's payroll taxes from me personally?

Yes. Under IRC §6672, the IRS can assess the trust fund portion of a business's unpaid payroll taxes against any responsible person who willfully failed to pay it — even if the business is an LLC or corporation. The entity's liability shield does not apply, because the law treats withheld wages as employee money the business held in trust, not as ordinary business debt.

How much is the trust fund recovery penalty?

It equals 100% of the trust fund portion of the unpaid payroll taxes — the federal income tax withheld from paychecks plus the employees' share of Social Security and Medicare. It does not include the employer's matching FICA, FUTA, or the penalties and interest on the business account, so your personal exposure is always less than the business's full 941 balance — in the worked example above, $23,800 of a $34,600 debt.

Who counts as a responsible person for the TFRP?

Anyone with the status, duty, and authority to decide which bills get paid: owners, officers, and partners, but also non-owners like controllers, office managers, and bookkeepers with real control over the finances. The IRS looks at check-signing authority, who hired and fired, who dealt with the bank, and who prioritized creditors. Title matters far less than actual control — and more than one person can qualify at the same time.

Can a bookkeeper or regular W-2 employee be personally liable?

Yes, but only if they had genuine authority over which creditors got paid — not just mechanical check-signing at the owner's direction. Courts regularly distinguish employees who followed orders from people who made the decisions. If you only cut the checks the owner told you to cut, that is a real defense to raise in the Form 4180 interview and in a written protest, backed by emails and bank records showing who actually controlled the money.

Can the IRS assess the TFRP against more than one person at the same time?

Yes — the IRS routinely assesses 100% of the trust fund amount against every responsible person, then collects from whoever it can reach first. It only keeps the money once: payments by the business or by any other responsible person reduce the balance for everyone. IRC §6672(d) also gives you a right of contribution to recover from co-responsible persons who paid less than their share.

Is the trust fund recovery penalty dischargeable in bankruptcy?

No. Trust fund taxes are priority debts that survive both Chapter 7 and Chapter 13, no matter how old they are. Bankruptcy can pause collection while the case is open, but the TFRP comes out the other side intact — and the bankruptcy pauses the 10-year collection clock, so filing can actually extend how long the IRS has to pursue you.

How long does the IRS have to assess and collect the TFRP?

Quarterly Forms 941 are treated as filed on April 15 of the following calendar year, and the IRS generally has 3 years from that date to assess the TFRP for those quarters. Once assessed, a separate 10-year collection statute starts running on your personal account. If a proposed assessment reaches quarters more than three years past that April 15 mark, the statute of limitations itself may be a defense worth raising.

Should I sign Form 2751?

Not before you understand what it does. Form 2751 is a consent that agrees to immediate assessment of the trust fund recovery penalty and gives up your right to a pre-assessment appeal. Sign it only if you agree you were responsible and willful and the numbers are correct. If any one of those three points is in doubt, use the 60-day window to file a written protest instead.

Can I settle a trust fund recovery penalty with an offer in compromise?

Sometimes. Once the TFRP is assessed against you, it is a personal liability, and you can submit an offer in compromise based on your own income and assets — not the business's. Eligibility is strictly means-tested, and the IRS accepted roughly 1 in 5 offers in FY2024, so treat it as a math problem, not a discount program. An offer also pauses the 10-year collection clock while it is under review.

Does first-time abatement or the new AEP apply to the TFRP?

No. First-time abatement — and the Automatic Exemption from Penalty (AEP) that begins replacing it in summer 2026 — covers routine filing and payment penalties, not the §6672 trust fund recovery penalty. Relief from a TFRP runs through different doors: proving you were not responsible or not willful, correcting the numbers, appealing before assessment, or resolving the assessed balance through payment options.

Your next 24 hours

- Find the controlling date and amount. On Letter 1153, both are printed near the top, with the per-quarter trust fund figures on the attached Form 2751 — write the date down and count 60 days forward.

- Gather your paper trail. The business's 941s for the quarters listed, the bank signature card, check registers or online-banking access logs, and any emails showing who directed payments — plus your own most recent tax return.

- Get the free case review. Call (888) 825-7779 or use the 2-minute form before the protest window on your letter closes — the stage you're in decides which defenses are still on the table, and that clock is already running.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.