Payroll Taxes & Personal Liability

Bookkeeper Personally Liable to the IRS? Non-Owner Responsible-Person Risk (2025)

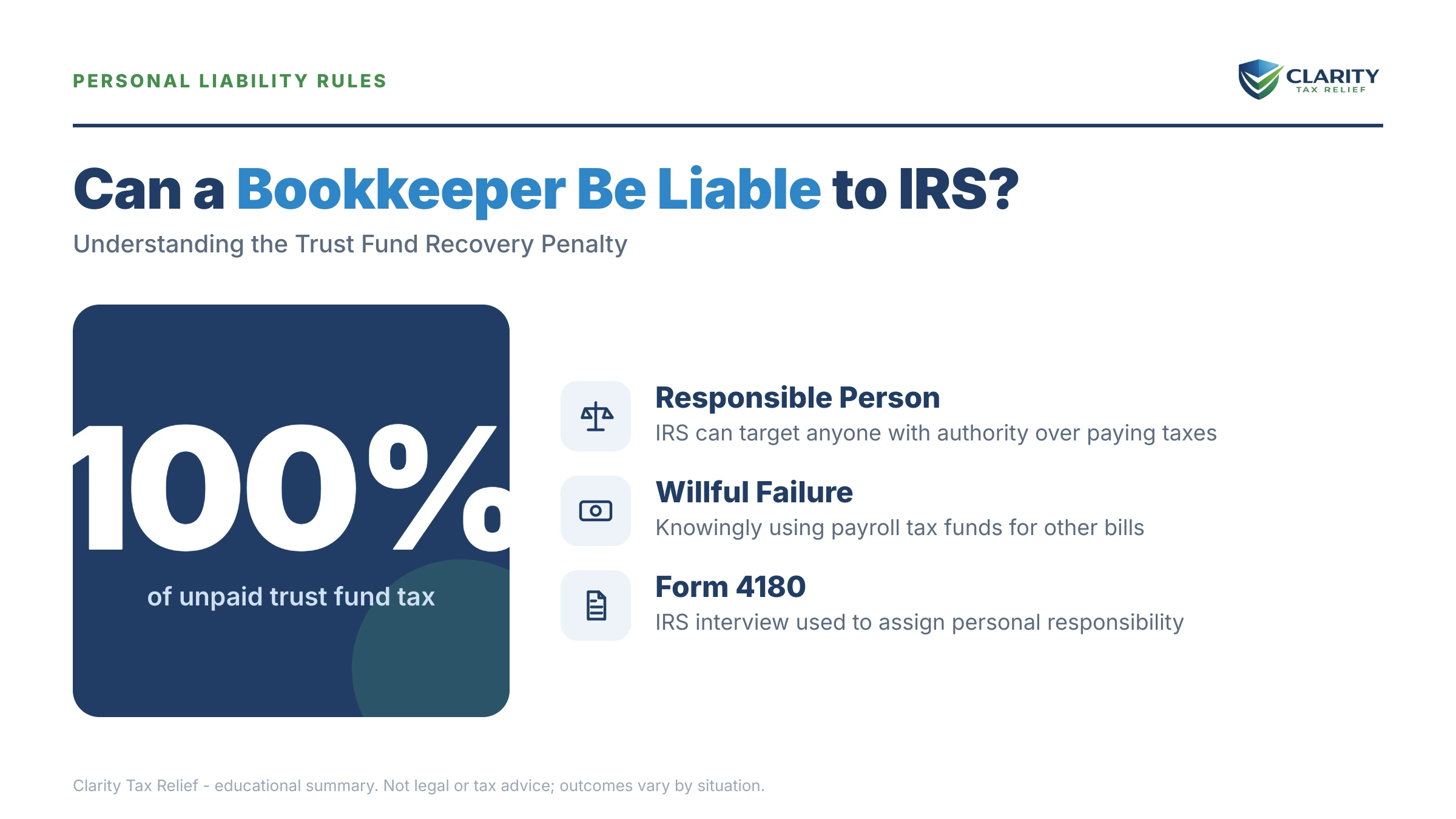

The short answer: a bookkeeper can be personally liable to the IRS even if they never owned the company. The Trust Fund Recovery Penalty (TFRP) targets anyone who was a "responsible person" — someone with authority over which bills got paid — who willfully let withheld payroll taxes go unpaid. Ownership is not required.

A revenue officer is asking about your role?

Before you sit for a Form 4180 interview or sign anything, talk to an experienced tax professional. We'll review where you actually stand on the responsible-person test — free, confidential, no pressure.

⏱ Your deadline: if you receive Letter 1153 proposing the penalty against you, you have 60 days from the date on the letter to file a written protest and request an Appeals hearing before the IRS formally assesses it. Miss that window and the penalty becomes your personal tax debt.

Why the IRS can come after a bookkeeper personally

If you're a bookkeeper and the IRS is asking whether you're personally liable, here's the hard truth up front: yes, a bookkeeper can be personally liable to the IRS for a company's unpaid payroll taxes — and your job title doesn't protect you. The rule that does this is the Trust Fund Recovery Penalty, sometimes called the TFRP or "100% penalty."

Here's the logic. When a company pays employees, it withholds income tax and the employee's share of Social Security and Medicare. That money never belonged to the business — it's held "in trust" for the government. When a company spends that withheld money on rent, vendors, or payroll instead of sending it to the IRS, the law lets the IRS reach past the business and collect the trust fund portion from the individuals who were responsible (the IRS explains this on its Trust Fund Recovery Penalty page).

Two things must be true for the IRS to assess you:

- You were a responsible person — you had the duty and authority to collect, account for, or pay over the withheld taxes. Check-signing authority, deciding which bills get paid, and handling payroll all point here.

- You acted willfully — you knew the taxes were unpaid (or recklessly disregarded that fact) and paid other creditors instead. "Willful" here doesn't mean evil intent. It means you had the choice and made it.

Notice what's missing from that test: ownership, a fancy title, and signing the company's tax returns. A non-owner bookkeeper who signs checks and chooses which vendors get paid each week can fit the definition. That's the trap.

What you can — and can't — be held liable for

The good news inside the bad news: you are not on the hook for the entire company tax bill. The TFRP only covers the trust fund portion — the income tax and the employee's half of Social Security and Medicare. The employer's matching share, plus the federal penalties and interest piled onto the company's account, stay with the business.

Here's a concrete example. Say a company falls behind on $100,000 of total Form 941 payroll tax debt. Roughly $60,000 to $70,000 of that is typically trust fund money. That trust fund slice is the maximum that can be assessed against responsible individuals personally. So if the IRS names you, the penalty is built on that smaller number — not the full $100,000, and not the company's separate penalties and interest.

One more important point: if three people are named as responsible, the IRS can assess the full trust fund amount against each of them. It only collects the money once, but everyone named is individually on the hook until it's paid.

What happens if you ignore the IRS on this

The trust fund process moves through predictable stages. Each one narrows your options:

- Revenue officer investigation — a real IRS employee is assigned. They gather bank signature cards, canceled checks, and payroll records to find responsible people.

- Form 4180 interview — the IRS interviews you about your duties, your authority, and who decided which bills to pay. Your answers become the case for or against you.

- Letter 1153 — the IRS proposes the penalty against you and gives you 60 days to protest.

- Assessment — if you don't respond, the penalty becomes your personal balance. From here it behaves like any individual tax debt.

- Collection — the IRS can file a federal tax lien against you, garnish your wages, and levy your personal bank accounts.

Once the penalty is assessed against you personally, it doesn't disappear when the company closes or files bankruptcy. Trust fund liability generally survives both. That's why the 60-day window after Letter 1153 is the moment that matters most.

How to fight being named a responsible person

Being a bookkeeper is not automatic liability. The IRS has to prove both responsibility and willfulness, and many bookkeepers have real defenses:

- You followed orders, you didn't give them. If you only processed payroll on the owner's instructions and could not decide which creditors got paid first, you may not be a responsible person at all.

- No real authority over funds. Limited or no check-signing authority, no ability to open or close accounts, and no say over priorities all cut against responsibility.

- You didn't act willfully. If you didn't know the taxes weren't being paid — or you flagged the shortfall to the owner and were overruled — that weakens the willfulness element.

- The numbers are wrong. The IRS sometimes overstates the trust fund portion or names the wrong period. The math and the records can be challenged.

The Trust Fund Recovery Penalty is one of the most fact-driven areas in tax. Two bookkeepers at the same company can get completely different outcomes based on who held the checkbook and who knew what. That's why how you answer the Form 4180 interview is so important — and why you're allowed to be represented for it.

How to respond, step by step

- Don't talk before you're ready. If a revenue officer contacts you, you can politely decline an on-the-spot interview and arrange representation first. You have that right.

- Gather your records. Find your job description, emails showing you raised the unpaid-tax issue, bank signature cards, and anything showing who controlled payment decisions.

- Read Form 4180 before the interview. It's the IRS's own questionnaire (see About Form 4180 on IRS.gov). Know which questions decide responsibility.

- If you get Letter 1153, calendar the 60 days immediately. File a written protest and request an Appeals hearing within that window to keep the penalty from being assessed.

- If the penalty is already assessed, you still have options — payment plans, hardship status, and refund-claim challenges. The Taxpayer Advocate Service can also help if collection is causing real hardship.

- Get a professional review. The defense you raise and the order you raise it in change the outcome. This is not a do-it-yourself area when your personal assets are at stake.

Bookkeeper liability questions, answered

Can a bookkeeper be personally liable to the IRS if they don't own the company?

Yes. Ownership has nothing to do with it. The Trust Fund Recovery Penalty applies to any person who was responsible for paying over withheld payroll taxes and willfully failed to do so. A non-owner bookkeeper with check-signing authority and knowledge of unpaid taxes can be assessed personally.

What part of the payroll tax debt can a bookkeeper be held liable for?

Only the trust fund portion — the income tax and the employee's share of Social Security and Medicare withheld from paychecks. The employer's matching share, plus penalties and interest on the company account, are not part of the personal penalty. On most payrolls the trust fund piece is roughly 60 to 70 percent of the total payroll tax liability.

What is the Form 4180 interview and should I just answer it?

Form 4180 is the IRS interview the revenue officer uses to decide who is a responsible person. Your answers about check-signing, payroll duties, and who decided which bills to pay become the evidence for or against you. You are not required to do it without representation, and many bookkeepers should talk to an experienced tax professional before answering.

How do I fight a Trust Fund Recovery Penalty against me as a bookkeeper?

You can show you were not responsible — you only processed payroll on instruction and could not decide which creditors got paid — or that you did not act willfully. If you get Letter 1153, you have 60 days to file a written protest and request an Appeals hearing before the penalty is assessed.

Can the IRS take my house or wages for a company's payroll taxes?

If the Trust Fund Recovery Penalty is assessed against you personally, it becomes your own tax debt. The IRS can then file a federal tax lien, garnish your wages, and levy your bank accounts the same way it would for any individual balance. That is why responding before assessment matters so much.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.