Business Tax Debt

C Corporation Tax Debt: How to Resolve an 1120 Balance Due (2025)

The short answer: C corporation tax debt is the balance your company owes after filing Form 1120 (the U.S. Corporation Income Tax Return) without paying in full. The corporation — not you personally — owes regular income tax, and the IRS offers business payment plans, hardship status, and settlement options. Acting before the IRS files a lien or levies the company's accounts gives you the most choices.

Holding an 1120 balance-due notice right now?

Send us a photo of it. An experienced tax professional will review where your corporation stands, what the IRS can and can't do next, and which resolution options you may qualify for — free, confidential, no pressure.

⏱ Your deadline: the "pay by" date on your IRS balance-due notice — usually 21 days from the notice date. A failure-to-pay penalty of 0.5% of the unpaid tax per month plus daily interest keeps building until the balance is paid or under an agreement. The longer you wait, the closer the IRS gets to filing a lien or issuing a levy against company assets.

Why your C corporation owes the IRS

If you're reading this with an 1120 balance-due notice in hand, your C corporation tax debt almost always traces back to one of a few things: the company reported a profit on Form 1120 but didn't send in the full tax, estimated tax payments during the year fell short of what was owed, or the IRS adjusted the return and added tax, penalties, and interest. Cash-flow crunches are the usual culprit — the tax was real, but the money wasn't there on the due date.

Form 1120 income tax is the corporation's own liability. That's different from payroll taxes, which sit in a separate and more dangerous bucket. The IRS explains the corporate return at its About Form 1120 page. Whatever the cause, the debt is manageable — but it does not go away on its own, and it gets more expensive every month.

What happens if you ignore an 1120 balance due

Business collection follows the same automated path as individual collection, and the IRS treats a company's bank accounts and receivables as fair game. Ignore the notices and the system escalates roughly every five weeks:

- First balance-due notice (CP161 or similar) — the IRS's opening bill for the corporation. No enforcement yet.

- Reminder notices — the balance keeps growing with the 0.5% monthly penalty and daily interest.

- CP504 — Notice of Intent to Levy. The IRS can seize state refunds and signals that a federal tax lien is coming.

- Final Notice of Intent to Levy (LT11 / Letter 1058) — after 30 days, the IRS can levy company bank accounts and accounts receivable. This is also when your formal appeal rights kick in.

- Revenue officer assignment — larger business balances are often handed to a field officer who may visit, demand records, and move quickly on enforcement.

A federal tax lien attaches to the corporation's property and can freeze your ability to get business financing. A levy on receivables tells your customers to pay the IRS instead of you — which is exactly the kind of disruption a struggling business can't absorb. Acting early is the whole game.

Are you personally on the hook?

This is the question that keeps business owners up at night, so let's be clear. For ordinary C corporation income tax on Form 1120, the corporation owes the debt — not you personally. That liability shield is a core reason the corporate structure exists.

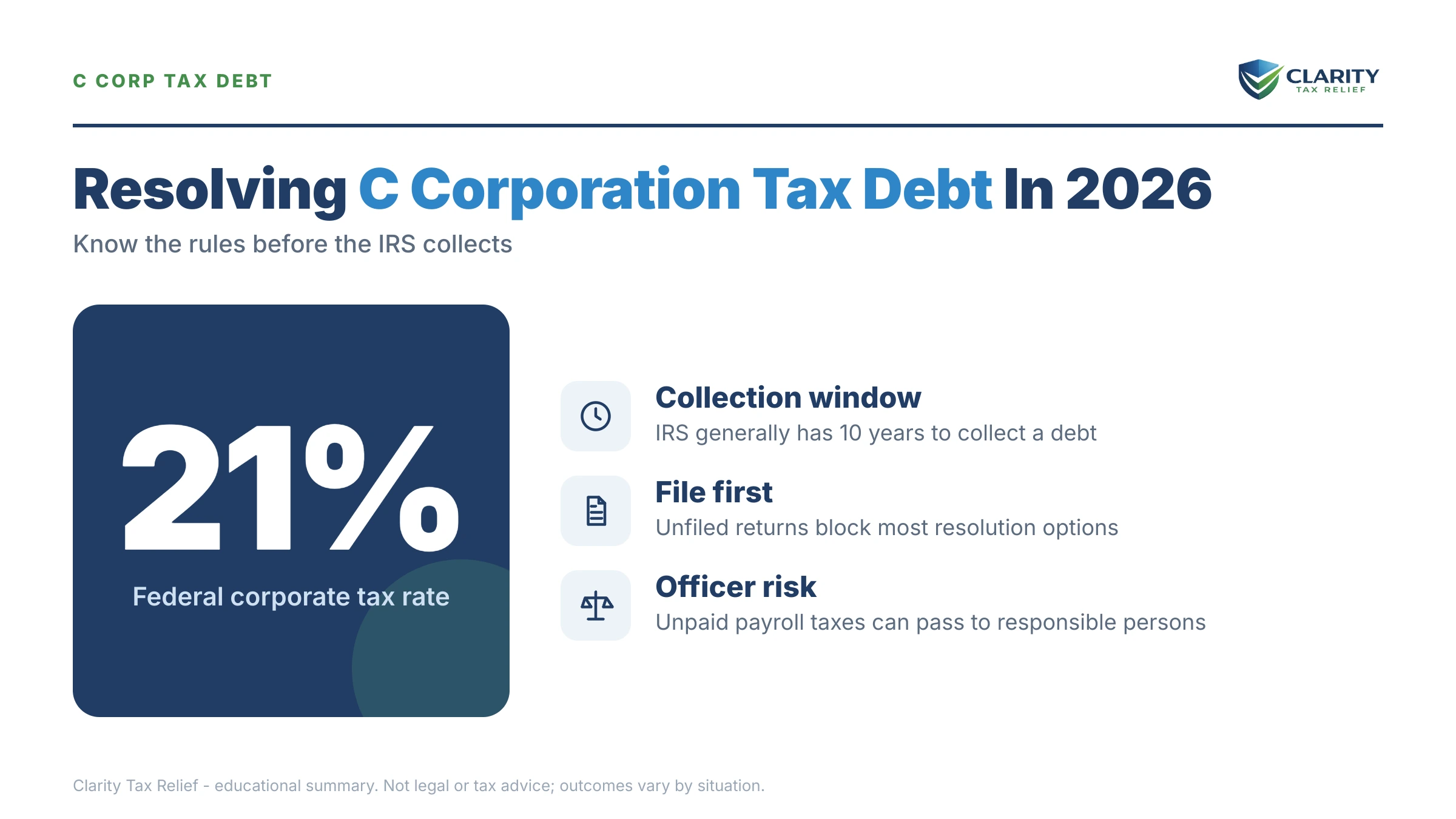

The big exception is payroll trust-fund taxes. If your company withheld income tax and the employee share of Social Security and Medicare from paychecks but didn't pay it over to the IRS, the agency can assess the Trust Fund Recovery Penalty against the owners, officers, or anyone "responsible" for the money. If your company is behind on 941 payroll taxes as well as 1120 income tax, sort out the payroll piece first — that's where personal exposure lives.

Your options to resolve C corporation tax debt

The notice makes it sound like you either pay in full or face enforcement. In reality the IRS has several business programs, and the right fit depends on the company's books:

- Pay in full or short-term plan — if the company can clear the balance now or within about 180 days, that stops the penalty clock and the notice sequence. Pay through IRS.gov/payments or the Electronic Federal Tax Payment System (EFTPS).

- In-business installment agreement — a monthly payment plan. Businesses that owe $25,000 or less in combined tax, penalties, and interest can often qualify for a streamlined agreement by direct debit over up to 24 months. The IRS outlines this on its payment plans page. A streamlined installment agreement avoids detailed financial disclosure; larger balances usually require Form 433-B.

- Currently Not Collectible-type status — if the corporation genuinely cannot pay anything without shutting down, collection can sometimes be paused while the business recovers. The debt remains and interest accrues, but levies stop.

- Offer in Compromise — settling for less than the full balance. A business can apply, but the IRS only accepts when the company's assets and projected income truly can't cover the debt within the collection period. Anyone promising to settle for pennies on the dollar before reviewing your finances is selling you something — see how an offer in compromise actually works.

- Penalty relief — if the company has a clean compliance history, first-time penalty abatement may remove the failure-to-pay penalty. Reasonable-cause relief can apply for circumstances beyond your control.

How to respond, step by step

- Verify the balance. Compare the notice against your filed Form 1120 and the corporation's IRS account. Confirm the tax year and how the balance splits between tax, penalties, and interest.

- Confirm all returns are filed. The IRS won't approve a payment plan or settlement while the corporation has unfiled returns. File any missing 1120s or payroll returns first.

- Separate payroll from income tax. If the company owes 941 payroll taxes too, address that first — that's where personal liability through the Trust Fund Recovery Penalty can arise.

- Pick the option that fits the cash flow. Pay in full if you can; otherwise request a short-term plan or an in-business installment agreement before the deadline. Starting any arrangement today blocks the levy sequence.

- Get a professional review for larger balances. If the company owes more than $25,000, has a revenue officer assigned, or has both income and payroll debt, the order you fix things in changes what you ultimately pay.

A worked example: how the penalty math adds up

Say a C corporation files its 1120 showing $40,000 of tax due but can't pay. The failure-to-pay penalty is 0.5% of the unpaid tax per month — that's $200 the first month, and it keeps compounding against the unpaid balance. On top of that, interest accrues daily on the tax and the penalties. Over a year, the penalty alone can climb into the thousands, and interest adds more. Set up an installment agreement and the failure-to-pay penalty rate is cut in half while the plan is active — one of many reasons acting early is cheaper than waiting.

C corporation tax debt questions, answered

Am I personally liable for my C corporation's tax debt?

For regular C corporation income tax reported on Form 1120, the corporation owes the debt, not you personally — that's the point of the corporate structure. The major exception is payroll trust-fund taxes: if your company withheld income and Social Security tax from employees and didn't pay it over, the IRS can assess the Trust Fund Recovery Penalty against you personally.

Can a C corporation get an IRS payment plan?

Yes. A C corporation can request an installment agreement for income tax it owes. Businesses that owe $25,000 or less in combined tax, penalties, and interest can often qualify for an in-business streamlined agreement paid over up to 24 months by direct debit. Larger balances usually require financial disclosure on Form 433-B.

Can a C corporation settle tax debt for less than it owes?

A business can apply for an Offer in Compromise, but the IRS only accepts it when the corporation's assets and projected income genuinely can't cover the debt within the collection window. Anyone promising to settle your corporate balance for pennies on the dollar before reviewing your books is selling you something, not telling you the truth.

What happens if my C corporation just stops paying the IRS?

The balance grows with penalties and interest, and the IRS collection system escalates automatically. It can file a federal tax lien against the business, levy company bank accounts and accounts receivable, and assign a revenue officer. Closing the corporation does not erase the debt and may shift attention to any unpaid payroll trust-fund taxes.

How long can the IRS collect a C corporation tax debt?

The IRS generally has 10 years from the date the tax is assessed to collect it — the Collection Statute Expiration Date, or CSED. Certain actions, like filing an Offer in Compromise or a bankruptcy, can pause and extend that clock. The 10-year rule applies to corporate income tax the same way it applies to individuals.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.