IRS Collections

Can the IRS Take My Car? When the IRS Actually Seizes Vehicles (2026)

The short answer: yes — the IRS has legal power to seize and sell your car for back taxes, but it almost never does. A vehicle seizure requires a final notice (LT11 or Letter 1058), a 30-day waiting period, and enough equity to make an auction worthwhile — and bank and wage levies come first.

If you're typing "can the IRS take my car" into a search bar in 2026, something specific put the picture in your head — a notice with the word "levy" on it, a revenue officer's business card, or a payroll tax balance your business hasn't been able to catch up on. Take a breath: the tow truck is the rarest move in the IRS playbook, and every step that leads to it comes with a warning and a way out. This guide maps exactly when a vehicle seizure is legal, why it almost never happens, and what to do at whichever stage you're actually in.

⏱ The clock that matters: you have 30 days from the date on an LT11 or Letter 1058 — the final notice of intent to levy — to request a Collection Due Process hearing with Form 12153. That request generally pauses levy action, including any move against your car, while Appeals hears your case. If you haven't received a final notice yet, no seizure clock is running — but interest and the monthly late-payment penalty are.

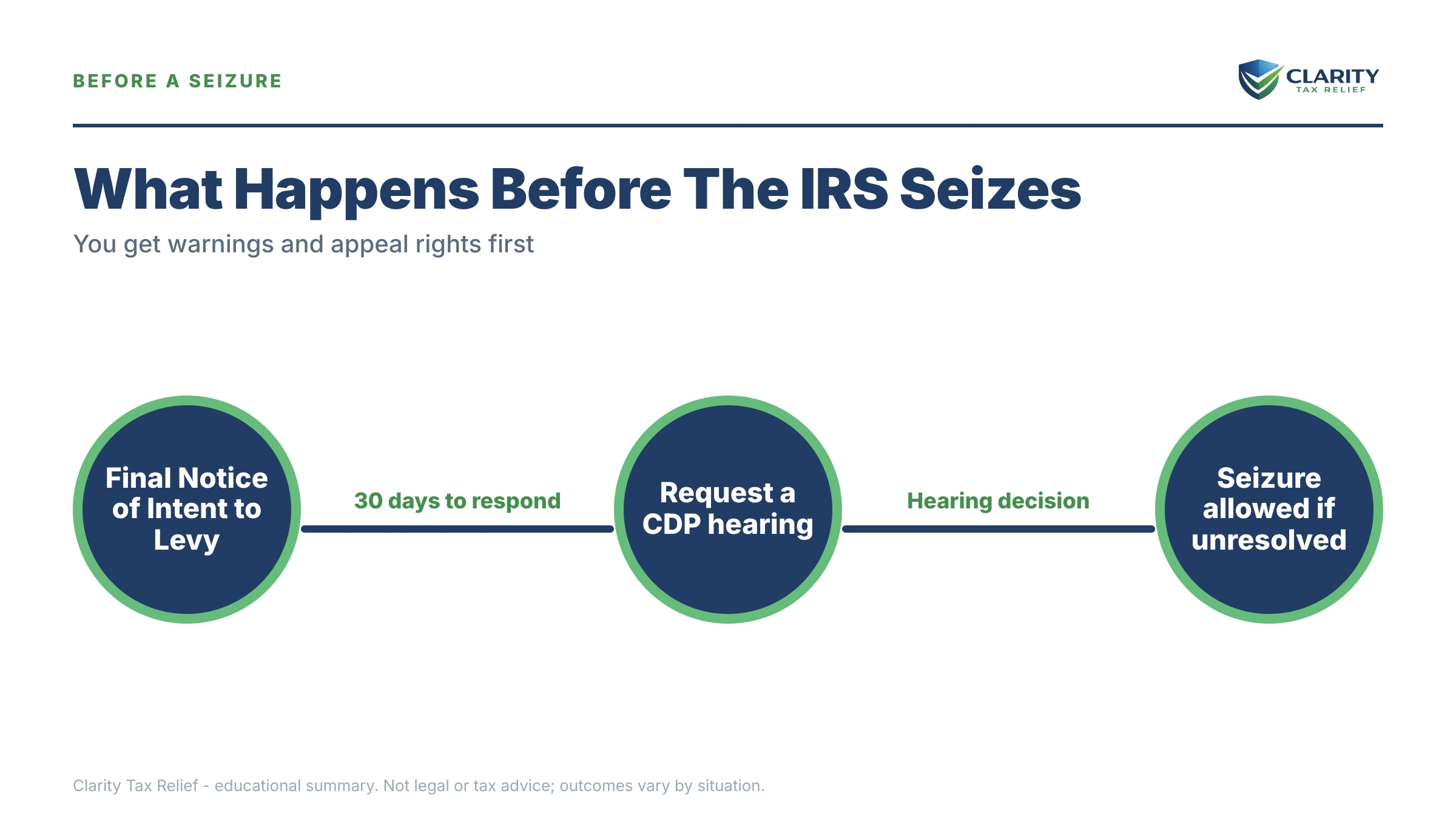

When the IRS can legally seize a vehicle

The IRS can seize a car only after it has assessed the debt, billed you, sent a final notice of intent to levy, and waited 30 days. That authority comes from IRC §6331, and the sequence is not optional: skip a required notice and the seizure is invalid. Before any tow truck is even a possibility, the IRS must have:

- An assessed balance and a bill — usually a CP14, followed by reminder notices.

- A final notice of intent to levy — the LT11 notice or Letter 1058, sent to your last known address, which starts the 30-day clock and grants your appeal rights.

- The 30 days to pass without payment, a resolution, or a timely hearing request.

Two more practical gates stand between the final notice and your driveway. First, vehicle seizures are not automated: the IRS's computer system issues bank and wage levies by mail, but physically taking property requires a human revenue officer and managerial sign-off. Second, the seizure has to make financial sense — which is where most cars fall out of reach, as the next section shows. One contrast worth knowing: a car needs no court order to seize, while a principal residence does. If real estate is your bigger worry, see can the IRS take my house.

The equity test: why a loan or lease often protects your car

Federal law bars the IRS from a seizure that wouldn't raise money — under IRC §6331(f), if the costs of seizing and selling your car would exceed what the sale nets toward your debt, the levy is "uneconomical" and prohibited. That single rule protects more vehicles than any exemption, because the math runs against the IRS three ways:

- Forced sales are cheap sales. The IRS values seized property at a quick-sale figure, commonly around 80% of fair market value, because auctions don't fetch retail prices.

- Your lender usually gets paid first. A car loan recorded before the IRS files its tax lien generally has priority, so the IRS collects only from the equity left after the payoff.

- Seizure has overhead. Towing, storage, and auction costs come out before a dime touches your tax balance.

A leased car is off the table entirely — a levy reaches only property you own, and a leased vehicle is titled to the leasing company. There's also a statutory exemption for tools of your trade up to a modest inflation-adjusted amount, though it rarely shields a whole vehicle on its own.

A worked example: $13,600 owed, one financed work truck

Say you run a four-person landscaping company and owe $13,600 — $9,100 in unpaid Form 941 payroll taxes and $4,500 on your personal return. Your truck would sell for about $18,000, and you still owe $11,500 on it. Here's the seizure math from the IRS's side:

- Quick-sale value (roughly 80% of $18,000): $14,400

- Minus the lender's payoff: $14,400 − $11,500 = $2,900

- Minus towing, storage, and auction costs: perhaps $2,000 or less ever reaches the tax debt

Seizing the truck would strand your crew, cut off the income the IRS wants to collect from, and recover maybe 15 cents of every dollar owed. Compare the alternative: $13,600 fits well under the streamlined payment-plan threshold, and spread over 72 months that's roughly $189 a month before interest and the 0.5% monthly failure-to-pay penalty. A revenue officer would far rather have that agreement — or a levy on the business bank account — than your truck. One caution for this scenario: the trust-fund portion of payroll debt can be assessed against you personally, so the business balance follows you even if the company folds. Our guide to 941 back taxes covers that exposure in depth.

What the IRS takes first — long before your car

Before any vehicle is seized, the IRS's automated system takes the money it can reach without a tow truck: bank accounts, paychecks, and tax refunds. If you're past the final-notice stage, expect these in roughly this order of likelihood:

- Bank levy. Your bank freezes the balance and holds it for 21 days before sending it to the IRS — a window you can use. See how the IRS bank levy 21-day rule works.

- Wage levy. Unlike a bank levy, a wage garnishment is continuous until released. You can estimate how much of a paycheck a levy could reach with our IRS wage garnishment calculator.

- Refund offsets. Federal refunds are applied to the debt automatically, and after a CP504 the IRS can seize your state refund.

- Business cash flow. For a business debtor, levies on merchant accounts, receivables, and payment platforms hit first — see whether the IRS can levy PayPal or Venmo business balances.

- Federal payments. Up to 15% of Social Security can be taken through the Federal Payment Levy Program, and retirement accounts are reachable too — here's when the IRS can take a 401(k).

Notice what all of those have in common: they're paperwork, not property. A car seizure requires a person, approvals, a locksmith or tow, storage, public sale notices, and an auction. In 2026 — with the IRS workforce down roughly 27% after the 2025 cuts — the agency has fewer humans than ever to run seizures, but the automated levies above never stopped. The realistic threat to most readers isn't the driveway; it's the bank account.

Can the IRS take my car if I ignore the notices?

Ignoring the notice sequence is the only way a vehicle seizure becomes realistic — every stage you let pass removes a protection you had the day before. The escalation runs in a fixed order:

- CP14 — the first bill. No enforcement power yet; just the balance, typically due about 21 days from the notice date. The cheapest moment to fix anything.

- CP501 / CP503 — reminders. Still bills, but the failure-to-pay penalty and interest compound monthly while they stack up.

- CP504 — intent to levy. The IRS can now seize your state tax refund under IRC §6331(d), and a federal tax lien — which attaches to your car's title along with everything else you own — becomes likely.

- LT11 / Letter 1058 — final notice. The 30-day clock starts. This is the last notice before the IRS can levy bank accounts, wages, and property — and the notice that grants your Form 12153 CDP hearing rights.

- After the 30 days. Bank and wage levies can issue at any time. If a revenue officer is assigned and finds real equity in a vehicle, seizure paperwork can begin — with you having already spent your strongest appeal.

| Notice | Your window | What passing it costs you |

|---|---|---|

| CP14 (first bill) | Typically 21 days from the notice date | The cheapest fix — penalties and interest start compounding |

| CP501 / CP503 (reminders) | Due date printed on each notice | A growing balance and a file moving toward enforcement |

| CP504 (intent to levy) | Due date printed on the notice | Your state tax refund; a federal tax lien becomes likely |

| LT11 / Letter 1058 (final notice) | 30 days from the notice date | Your Collection Due Process hearing — the strongest appeal you get |

| After the 30 days | None — levy authority is active | Bank and wage levies first; vehicle seizure possible where a revenue officer finds equity |

Worried a levy is coming for your car — or your business account?

If an LT11 or Letter 1058 is on your desk, the 30-day window to protect your appeal rights is already running. Send us the notice and an experienced tax professional will map exactly where you stand and which option fits — free, confidential, no pressure.

Your options to take a vehicle seizure off the table

Any resolution the IRS accepts — a payment plan, hardship status, or an offer under review — generally suspends levy action, including vehicle seizure, while it's in place. Interest and penalties keep accruing under most of them, but the enforcement machine stops moving. The full do-it-yourself playbook for each program lives in our guide to how to settle tax debt yourself; here's how each maps to seizure risk:

| Option | Who typically qualifies | Effect on seizure risk |

|---|---|---|

| Short-term payment plan | Can pay in full within 180 days; $0 setup fee | Ends the escalation while you pay it off |

| Streamlined installment agreement | Individuals owing $50,000 or less; up to 72 months, set up online | Seizure off the table while payments stay current |

| In-business payroll plan (IBTF-Express) | Operating businesses owing generally $25,000 or less in payroll tax, paid within 24 months by direct debit | Keeps a revenue officer from moving on business assets |

| Currently Not Collectible | Paying anything would leave you unable to cover basic living expenses; financial disclosure required | Levy action pauses; the debt and interest remain |

| Offer in Compromise | Assets plus future income genuinely can't cover the debt; $205 fee and 20% down on lump-sum offers (both waived with low-income certification) | Levy action generally suspended during review — but only about 1 in 5 offers were accepted in FY2024 |

| CDP hearing (Form 12153) | Anyone within 30 days of an LT11 / Letter 1058 | Pauses levy action while Appeals considers alternatives |

Two notes for the small-business reader. If payroll tax is part of your balance, the business-specific rules in our business payroll tax payment plan guide matter more than anything above — trust-fund debt is handled differently and moves faster. And if penalties are inflating the balance, ask about relief: first-time abatement applies with a clean prior three years, and starting in summer 2026 the IRS's new Automatic Exemption from Penalty (AEP) grants the same relief automatically, with no request needed.

Business vehicles and payroll tax debt: the higher-risk case

A truck titled to a business with unpaid 941s faces meaningfully more seizure risk than a family sedan, because payroll cases are the ones the IRS still assigns to human revenue officers. An officer working a trust-fund case can inventory business assets, and equipment — vehicles included — is a natural pressure point when a business keeps operating without a resolution. The equity test still applies, and shutting down your ability to earn still cuts against seizure, but the discretion sits with a person standing in your parking lot rather than a computer in Ogden.

The single best predictor of a business asset seizure is a missed revenue officer deadline. If an officer has given you a date to produce financials or returns, treat it as hard. What seizure of an operating company actually looks like — and every alternative that prevents it — is covered in our guide to IRS seized business assets.

How to respond when the IRS threatens your car, step by step

- Identify the notice. Check the code in the top corner of your latest letter — a CP504 means the state-refund stage; an LT11 or Letter 1058 means the 30-day levy clock is running.

- Protect your appeal rights. If you're holding a final notice, file Form 12153 within 30 days of its date to request a Collection Due Process hearing — levy action generally pauses while it's heard.

- Run your equity numbers. Look up the car's market value, get your loan payoff, and subtract — low or negative equity is a fact worth stating to the IRS.

- Set up a resolution. Choose the option from the table above that fits your balance and cash flow, and put it in place before the notice deadline at IRS.gov/payments.

- Escalate to a professional when it's complicated. Payroll tax, an assigned revenue officer, or multiple unfiled years change the strategy — get experienced eyes on it before you respond.

Most payment plans can be set up in one sitting through the IRS payment plans page. If a levy is already causing genuine hardship — you can't buy groceries or get to work — the Taxpayer Advocate Service exists for exactly that emergency.

When you can handle this yourself

You probably don't need professional help if you're still in the billing stage, you agree with the balance, and you can either pay within 180 days or fit a streamlined plan into your budget — the IRS's online tools handle that in under an hour, and the seizure question answers itself once an agreement is in place. The same goes if your only "asset" question is a financed car with no equity: the math already protects you.

Experienced help changes outcomes in a narrower set of situations: a final notice already issued with the 30-day window running, a revenue officer assigned to a payroll or business case, multiple unfiled years that must be filed before any agreement is possible, or an Offer in Compromise where the asset-and-income math decides everything. In those cases, the order you fix things in — returns first, then penalties, then the balance — often matters more than any single form, and a misstep can spend appeal rights you don't get back.

Terms on your notices, decoded

- Levy — the actual taking of property or money to pay a tax debt; the word on your notice that carries real force.

- Lien — the IRS's legal claim against everything you own, including your car's title; a claim, not a taking.

- Seizure — a levy on physical property (a vehicle, equipment, real estate) rather than money; requires a revenue officer.

- Quick-sale value — the discounted figure (commonly around 80% of market value) the IRS uses to estimate what seized property would fetch at auction.

- CDP (Collection Due Process) — your right, after a final notice, to a hearing before Appeals that pauses levy action; requested on Form 12153 within 30 days.

- CSED — the collection statute expiration date; the IRS generally has 10 years from assessment to collect, though appeals, offers, and bankruptcy pause the clock.

Can the IRS take your car? Your questions, answered

Can the IRS take your only car?

There is no blanket exemption for your only car, but seizing it is close to a last resort. The IRS must consider whether a seizure creates economic hardship, and a levy can be released under IRC §6343 if it prevents you from meeting basic living expenses — including getting to work. If losing the car would end your income, say so on the record: hardship is grounds for release, not just sympathy.

How much do you have to owe before the IRS seizes a car?

There is no statutory dollar threshold that triggers a vehicle seizure. In practice, seizures happen in larger cases assigned to a revenue officer — often business, payroll, or six-figure debts — where the vehicle has real equity. Smaller balances are collected through bank levies, wage levies, and refund offsets long before anyone considers towing a car.

Can the IRS take a car that's financed?

Usually not, because your lender gets paid first. A car loan recorded before the IRS files its lien generally has priority, so the IRS only collects from the equity left after the payoff. If your payoff is close to or above the car's quick-sale value, federal law treats the levy as uneconomical and prohibits it. Check your payoff before you panic — negative equity is real protection here.

Can the IRS take a leased car?

No — a levy only reaches property you own, and a leased vehicle belongs to the leasing company. The IRS cannot seize an asset titled to someone else to pay your debt. What it can still levy is the bank account you make lease payments from, so a lease protects the car itself but not the money around it.

Will the IRS warn me before taking my car?

Yes. Outside of rare jeopardy situations, the IRS must send a final notice of intent to levy — an LT11 or Letter 1058 — and then wait at least 30 days before seizing property. That notice also grants Collection Due Process rights: file Form 12153 within the 30 days and levy action generally pauses while Appeals hears your case. A seizure with no warning almost always means notices went to an old address.

Does a federal tax lien mean the IRS is taking my car?

No. A lien is a legal claim that attaches to everything you own, including your vehicle; a levy is the actual taking. A recorded lien means you can't sell or refinance the car with clean title until the debt is addressed, but nobody is coming for the keys because of a lien alone. The lien is the warning that levies can follow if the balance sits unresolved.

Can the IRS take my business truck for unpaid payroll taxes?

Business assets face more seizure risk than personal ones, because unpaid 941 payroll taxes usually put a revenue officer on the case, and equipment titled to the business is a natural target. The equity test still applies — a financed truck with little equity isn't worth seizing — and an in-business installment agreement typically takes seizure off the table. Move before the officer's deadline, not after.

Can the IRS take my car without a court order?

Yes. An IRS levy is an administrative action — no judge signs off before the IRS seizes a vehicle, bank account, or paycheck. The major exception is a principal residence, which does require court approval. The 30-day final notice and your Collection Due Process hearing rights are the safeguards Congress built in instead of a courtroom.

Your next 24 hours

- Find your latest notice and read the code in the top corner. CP14 through CP503 means you're in the billing stage; CP504 means your state refund is exposed; LT11 or Letter 1058 means the 30-day levy window is open — note the notice date.

- Gather three things: the notice itself, your car's loan payoff or lease agreement, and your last filed return (plus, for a business, your most recent 941 filings). These answer the equity question and the eligibility question in one sitting.

- Get a free case review. If a final notice is running its 30 days, don't spend them guessing — call (888) 825-7779 or use the 2-minute form and an experienced tax professional will walk your exact notice, balance, and options before the window closes.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.