IRS Collections

Combat Zone IRS Collection Relief: How Deployment Pauses IRS Collections (2026)

The short answer: combat zone IRS collection relief under IRC §7508 pauses levies, seizures, filing and payment deadlines, and most penalty and interest accrual for your entire qualifying service plus at least 180 days after you leave the zone. It's powerful — but the IRS's automated collectors keep running until someone tells the IRS you deployed.

One of you is deployed. The other is at the kitchen table with a stack of IRS envelopes addressed to both of you, wondering how the government can bill a household whose service member is currently serving it overseas. Here's the part the letters don't say: the law already gives you combat zone IRS collection relief — you just have to switch it on.

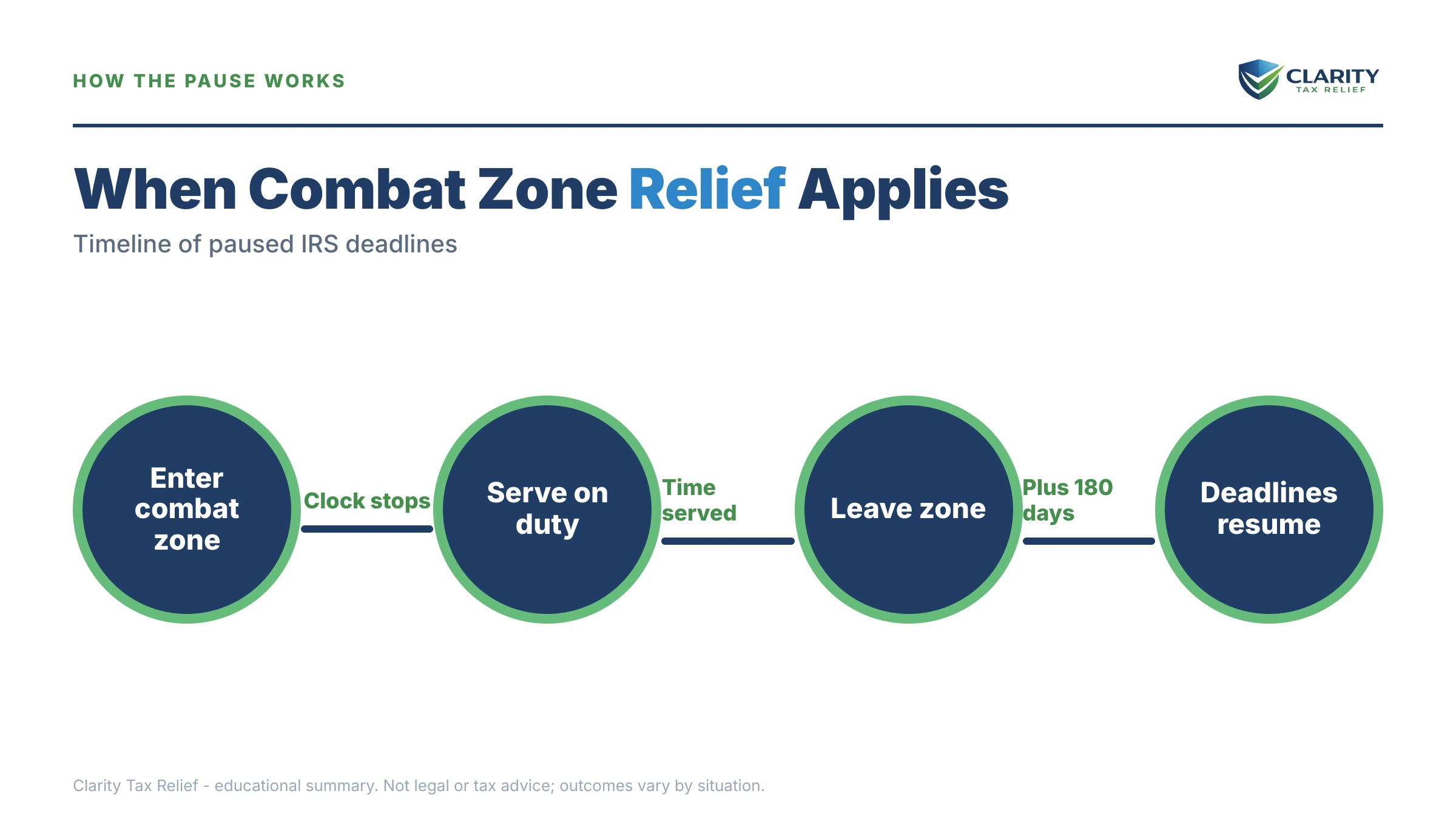

This guide covers who qualifies, exactly what pauses (and what doesn't), how to notify the IRS in one email, and how to use the quiet months so the debt is handled — not bigger — when the protection window closes. The image below maps the suspension window itself, from deployment date through the 180-day tail, so you can lay your own dates onto it.

⏱ Your real clock: the protection runs for your entire qualifying combat zone service plus at least 180 days after you leave the zone — plus any days that remained on the original deadline when you entered. Mark that end date now. When it passes, every paused deadline and the full collection machinery restart where they left off.

Why the IRS keeps sending collection letters during a deployment

The IRS's collection notices come from an automated system that has no idea you deployed until your account is coded with combat zone status. The Department of Defense reports deployments to the IRS, but that data feed misses people — especially reservists, Guard members in direct-support roles, and anyone whose orders changed mid-tour.

So the letters keep coming. A balance from before deployment — a filed-but-unpaid year, a self-employment year from a spouse's business, an adjustment the IRS made after you shipped out — rides the normal notice conveyor as if nothing changed.

That's the entire problem this article solves. The relief is a legal right, not a favor — but in practice it protects you fully only once the IRS knows to apply it. Everything below is about closing that gap fast.

Who qualifies for combat zone IRS collection relief

You qualify if you serve in a designated combat zone, a qualified hazardous duty area, or in direct support of operations there while receiving hostile fire or imminent danger pay. Current designations include the Afghanistan area, the Kosovo area, and the Arabian Peninsula area — Iraq, Kuwait, Saudi Arabia, Bahrain, Qatar, the UAE, Oman, and surrounding waters and airspace — plus the Sinai Peninsula as a qualified hazardous duty area.

The relief follows the service, not the uniform or the component:

- Active duty, National Guard, and reservists serving in or in direct support of a designated zone all qualify.

- Civilians supporting the Armed Forces in a combat zone — DoD contractors, Red Cross workers, accredited correspondents — qualify for the deadline extensions too.

- Spouses generally receive the same filing and payment extensions on joint matters, with narrow exceptions.

- Hospitalization from combat zone injuries extends the protection through the hospitalization period (stateside hospitalization is capped by law), plus the 180-day tail.

A quick self-check: if your leave and earnings statement shows the combat zone tax exclusion — enlisted pay fully excluded from income, officer pay excluded up to the top enlisted rate plus hostile fire pay — you almost certainly qualify for the collection suspension as well.

Not in a combat zone but still on active duty? A separate protection under the Servicemembers Civil Relief Act lets you request deferral of income tax collection when military service materially affects your ability to pay. It requires a showing; combat zone relief does not. If neither applies, the general playbook in our how to settle tax debt yourself guide is your starting point.

What combat zone relief actually pauses — and what it doesn't

IRC §7508 suspends both IRS deadlines and IRS enforcement for the period of qualifying service plus at least 180 days. It is broader than any payment plan or hardship status, because penalties and interest attributable to the suspension period generally don't accrue — nearly every other IRS arrangement lets interest keep running.

| IRS action | During service + 180 days | After the window closes |

|---|---|---|

| Bank and wage levies | Suspended — none should issue | Can resume where the notice sequence left off |

| Filing and payment deadlines | Extended — 180 days plus days remaining at entry | The recalculated deadline controls |

| Penalties and interest | Generally don't accrue for the suspension period | Resume accruing on any unpaid balance |

| 10-year collection statute (CSED) | Paused — the clock stops | Restarts; expiration pushed out day for day |

| A federal tax lien already on record | Stays filed — it does not come off | Remains until the debt is resolved and released |

| Automated notices | May keep arriving until the IRS is notified | Sequence resumes from its last stage |

Two rows deserve a second look. First, the lien: if the IRS recorded a federal tax lien before deployment, the suspension stops new enforcement but doesn't erase the lien from public records. Second, the CSED: the same 10-year collection deadline that eventually kills IRS debt is paused during your service plus 180 days, exactly like the other events covered in what extends the IRS collection statute. Every month of protection is a month added to the IRS's collection window — you can estimate your own adjusted expiration date with our CSED Calculator.

This relief is also mechanically different from the IRS disaster relief deadline extension: disaster relief is applied automatically by ZIP code, while combat zone relief follows an individual person — which is precisely why notification matters so much more here.

What happens if the IRS never learns you deployed

An unflagged account rides the standard collection conveyor even while the taxpayer is legally protected from every stage of it. The sequence — covered stage by stage in the IRS collection process step by step — looks like this:

- Balance-due bill (CP14) — the first demand, typically with about 21 days to respond before the stream continues.

- Reminder notices (CP501, CP503) — the balance keeps growing on paper while nobody at home knows whether to pay it.

- CP504 — Notice of Intent to Levy — the IRS positions itself to seize the state tax refund and a federal tax lien becomes a live risk.

- LT11 / Letter 1058 — Final Notice — a 30-day clock toward wage and bank levies, plus Collection Due Process rights that expire if no one responds.

- Levy — a bank levy freezes funds for 21 days before the money leaves; a wage levy runs continuously until released.

Here's the crucial point: every one of those actions is suspendable — and reversible — under §7508. A levy issued during a protected period should be released once the IRS gets the deployment dates. But reversing a levy after the fact is slower and harder on a military family's cash flow than preventing it with one email today. And in 2026, with IRS staffing down roughly 27%, the humans who fix errors are scarce while the automated systems that make them never stopped.

Deployed — or holding a deployed spouse's IRS mail?

Send us the letters. An experienced tax professional will confirm the combat zone suspension is properly coded, stop the notice stream from escalating, and map out the resolution before the 180-day window closes — free and confidential.

Your options when the 180-day window closes

The suspension pauses the debt; it doesn't resolve it. The smartest use of a deployment's protected months is choosing the exit before the clock restarts. Which options are realistic depends mostly on the balance:

| Balance when the window closes | Realistic options | What it takes |

|---|---|---|

| Under $10,000 | Guaranteed installment agreement | Pay within 3 years; clean filing history — the IRS must accept |

| $10,000–$25,000 | Streamlined installment agreement (online) | Up to 72 months; no financial statement required |

| $25,000–$50,000 | Streamlined agreement with direct debit | Up to 72 months; direct debit required above $25,000 |

| $50,000–$100,000 | IRS payment plan over $50,000 — or pay down under $50k first | Form 433-F financial disclosure and negotiation |

| Hardship at any level | Currently Not Collectible or an Offer in Compromise | Financial proof that full payment isn't collectible |

Two military-specific notes on that table. Penalty relief stacks well here: reasonable cause built on deployment facts is strong, first-time penalty abatement may cover a year the suspension didn't reach, and starting summer 2026 the new Automatic Exemption from Penalty applies some relief with no request at all. And if part of your income is VA disability compensation, read can the IRS take VA disability before assuming everything is levyable — the answer changes the hardship math.

A worked example: deployed with an $83,100 balance

Say you and your spouse file jointly and owe $83,100 across two tax years from a business that struggled before your 10-month deployment. This is hypothetical — but the arithmetic is real.

- The pause: 10 months in the zone plus the 180-day tail is roughly 16 months of suspension. The failure-to-pay penalty alone would otherwise run 0.5% per month — about $415 per month on $83,100, or roughly $6,650 in penalties attributable to that window that generally never accrue, before counting interest.

- The statute trade: those same 16 months are added to the IRS's 10-year collection clock on the back end.

- The exit decision: $83,100 is above the $50,000 online-plan ceiling. Option A: pay the balance down by $33,100 (savings, combat pay that was accumulating tax-free, a bonus) to reach $50,000 — then a streamlined direct-debit plan runs about $695/month over 72 months before interest. Option B: keep the full $83,100 and negotiate a non-streamlined agreement with Form 433-F — roughly $1,154/month on a 72-month pace. Option C: if separation from service cut your income sharply, run the Currently Not Collectible or Offer in Compromise math on your actual numbers instead.

The couple that decides this in month 6 of the deployment sets it up calmly. The couple that waits until day 181 decides it while the notice stream — see the order of IRS collection letters — restarts around them.

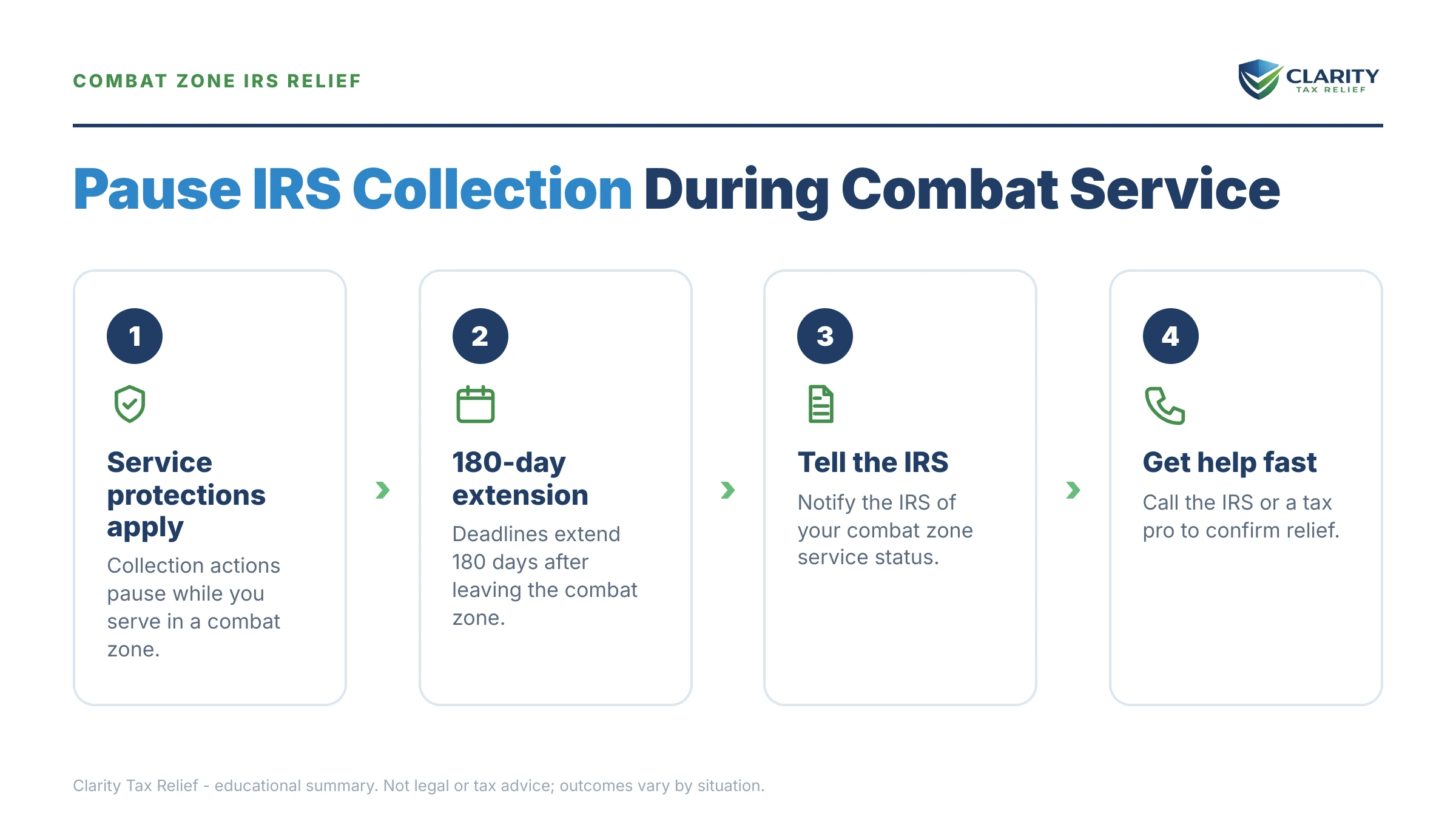

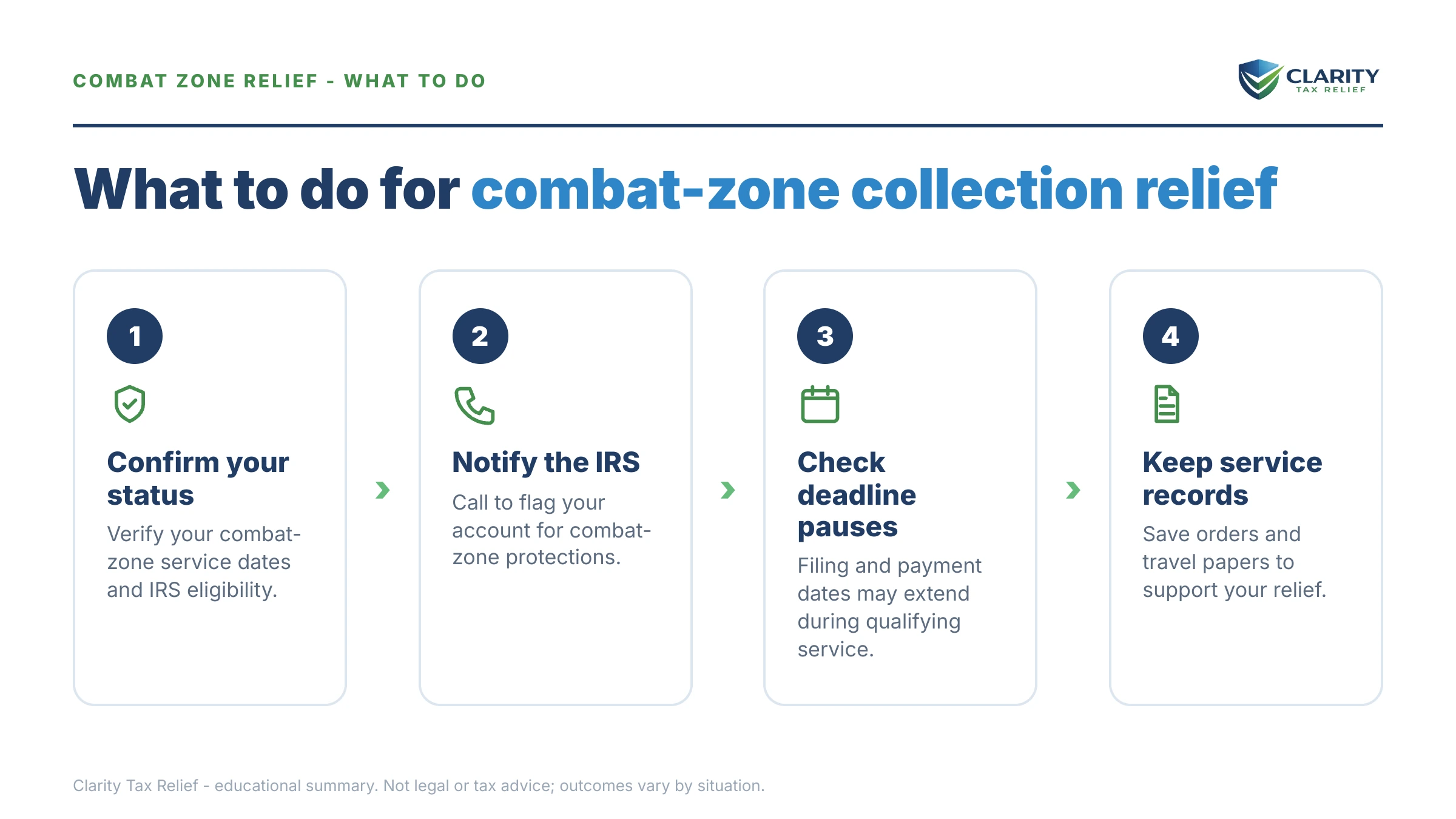

How to respond, step by step

- Notify the IRS of the combat zone service — email combatzone@irs.gov with the service member's name, stateside address, date of birth, and deployment date (never include a Social Security number in the email) — or write "COMBAT ZONE" across the top of any notice you received and mail it back to the address printed on it.

- Put someone stateside on the account with Form 2848 — file Form 2848 naming a spouse or an experienced tax professional as power of attorney so someone can talk to the IRS, receive notices, and act while the service member is unreachable.

- Confirm the suspension actually posted — a few weeks after notifying the IRS, check the account transcript or have your representative call to verify the account is coded with combat zone status and collection holds are in place.

- Calendar the end of the protection window — mark the date the service member leaves the combat zone, then count at least 180 days forward — plus any days that remained on the original deadline at entry — and treat that date as the real deadline.

- Choose the resolution before the window closes — use the quiet months to pick the payment plan, hardship status, penalty relief, or settlement path that fits the balance, so it's set up the day the suspension ends instead of racing the restarted notice stream.

When you can handle this yourself

Claiming the relief itself is genuinely do-it-yourself — one email or one notation on a returned notice, no forms and no fees. If the balance is modest and undisputed, you can also set up the post-deployment payment plan online in under an hour once you're home; balances under $50,000 don't require financial disclosure.

Experienced help changes outcomes in specific situations: a levy or lien already executed during a protected period that needs to be unwound; multiple unfiled years stacked across back-to-back deployments; a balance over $50,000 where Form 433-F numbers get negotiated rather than accepted; or a post-service income drop that puts Currently Not Collectible or an Offer in Compromise genuinely on the table. In those cases the order of operations — notification, returns, penalties, then the balance — often matters more than any single form.

Terms on your notices, decoded

- IRC §7508 — the statute that disregards your combat zone service period (plus 180 days) for IRS deadlines, enforcement, penalties, and interest.

- Combat zone — an area designated by Executive Order where the Armed Forces are engaged in combat, triggering both the pay exclusion and collection relief.

- Qualified hazardous duty area — an area Congress treats like a combat zone (currently including the Sinai Peninsula) for members receiving hostile fire or imminent danger pay.

- Direct support — service outside the zone that qualifies for the same relief because it supports zone operations and earns hostile fire or imminent danger pay.

- CSED — the Collection Statute Expiration Date, the 10-year deadline on IRS collection, which pauses during your protected period.

- SCRA — the Servicemembers Civil Relief Act, a separate law letting any active-duty member request tax collection deferral when service materially affects ability to pay.

For the full picture of military tax provisions — pay exclusions, extensions, and state notes — see the IRS's tax information for members of the military and Publication 3, Armed Forces' Tax Guide. If a protected account was levied and normal channels stall, the Taxpayer Advocate Service exists for exactly that.

Combat zone tax relief questions, answered

Does the IRS stop collection during a combat zone deployment?

Yes. Under IRC §7508, the IRS must suspend levies, seizures, and other enforced collection for your entire period of qualifying service plus at least 180 days after you leave the combat zone. The protection also covers filing and payment deadlines. The practical catch is notification: the IRS's automated collection stream keeps running until your account is coded with combat zone status, so tell the IRS as soon as deployment orders arrive.

How do I tell the IRS I'm serving in a combat zone?

You, your spouse, or an authorized representative can email combatzone@irs.gov with the service member's name, stateside address, date of birth, and deployment date — never include a Social Security number in the email. If you're responding to a specific notice, you can also write "COMBAT ZONE" across the top and mail it back to the address printed on the notice. The Department of Defense also reports deployments to the IRS, but don't rely on that alone.

Do IRS penalties and interest stop while I'm in a combat zone?

Generally, yes — the suspension period is disregarded when the IRS computes interest, penalties, and additions to tax, so amounts attributable to your qualifying service plus the 180-day tail generally don't accrue. This is different from almost every other IRS program: payment plans and hardship status pause enforcement but let interest run. If your balance was assessed before you entered service, ask about a Servicemembers Civil Relief Act deferral as well.

Does combat zone service extend the IRS 10-year collection statute?

Yes. The 10-year collection statute (CSED) is paused during your qualifying combat zone service plus 180 days, which pushes the expiration date out by the same number of days. That's the trade built into the relief: you get protection now, and the IRS gets the same amount of time added on the back end. Every month of suspension is a month added to the collection deadline.

Does my spouse get the same IRS deadline relief?

Generally yes for joint filings — the spouse of a combat zone participant is typically entitled to the same filing and payment deadline extensions, with limited exceptions (for example, the extension doesn't apply to a spouse for tax years beginning more than two years after the zone's combat activities end). For a joint balance, the suspension protects the joint account. A Form 2848 power of attorney lets your spouse or a tax professional handle IRS matters while you're deployed.

What if the IRS levied my bank account or wages during my deployment?

Contact the IRS (or have your representative do it) and provide your deployment dates — a levy issued during a period protected by IRC §7508 should be released, and enforcement taken while your account should have been suspended can be reversed. Move quickly on a bank levy: the bank holds funds 21 days before sending them to the IRS, and money is easier to keep than to claw back. The Taxpayer Advocate Service can help if normal channels stall.

Do National Guard and reservists qualify for combat zone tax relief?

Yes, if they serve in a designated combat zone or qualified hazardous duty area, or serve in direct support of operations there while receiving hostile fire or imminent danger pay. The relief follows the service, not the component. Civilians serving in a combat zone in support of the Armed Forces — Red Cross workers, accredited correspondents, DoD contractors — can also qualify for the deadline extensions.

What counts as a combat zone for IRS purposes?

Combat zones are designated by Executive Order and currently include the Afghanistan area, the Kosovo area, and the Arabian Peninsula area (including Iraq, Kuwait, Saudi Arabia, Bahrain, Qatar, the UAE, Oman, and surrounding waters and airspace). The Sinai Peninsula is treated as a qualified hazardous duty area for service members receiving hostile fire or imminent danger pay. Check IRS Publication 3 or your leave and earnings statement — the combat zone tax exclusion code is a strong indicator you qualify.

Your next 24 hours

- Find your dates. Pull the deployment orders for the date the service member entered the zone — and, if the tour is over, the date they left, because the 180-day tail counts from that day. If you're holding IRS letters, note the notice date and tax year on each.

- Gather three things: every IRS notice received, a copy of the orders or a leave and earnings statement showing combat zone pay, and the last tax return you filed.

- Get the free case review. Call (888) 825-7779 or use the 2-minute form — an experienced tax professional will confirm the suspension is coded on your account, stop the notice stream from escalating further, and have your resolution ready before the protection window closes.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.