IRS Collections

The IRS Collection Process Step by Step: Every Notice, Deadline, and Off-Ramp (2026)

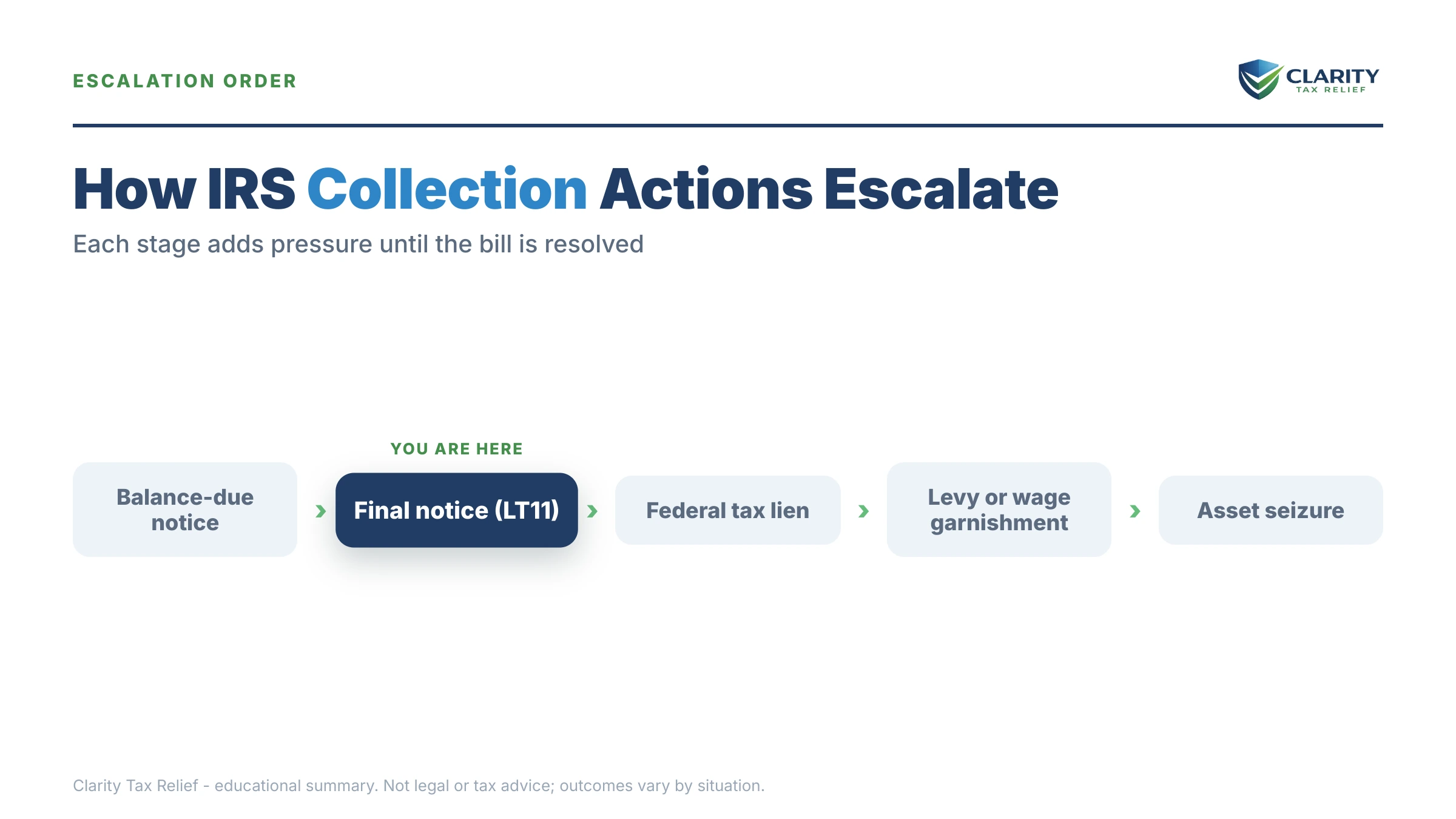

The IRS collection process, step by step: a first bill (CP14), one or two reminders (CP501/CP503), an intent-to-levy notice (CP504), then a final notice (LT11 or Letter 1058) that starts a 30-day clock before enforcement — liens, wage garnishment, bank levies. Every stage has an off-ramp: pay, arrange payments, or prove hardship.

You know a balance is out there — maybe one letter has arrived, maybe three — and what you really want to know is how far this goes and how fast. Here's the honest answer: the sequence is automated, it always moves in the same order, and it goes exactly as far as you let it. This page maps the whole road, with the exit at every stage.

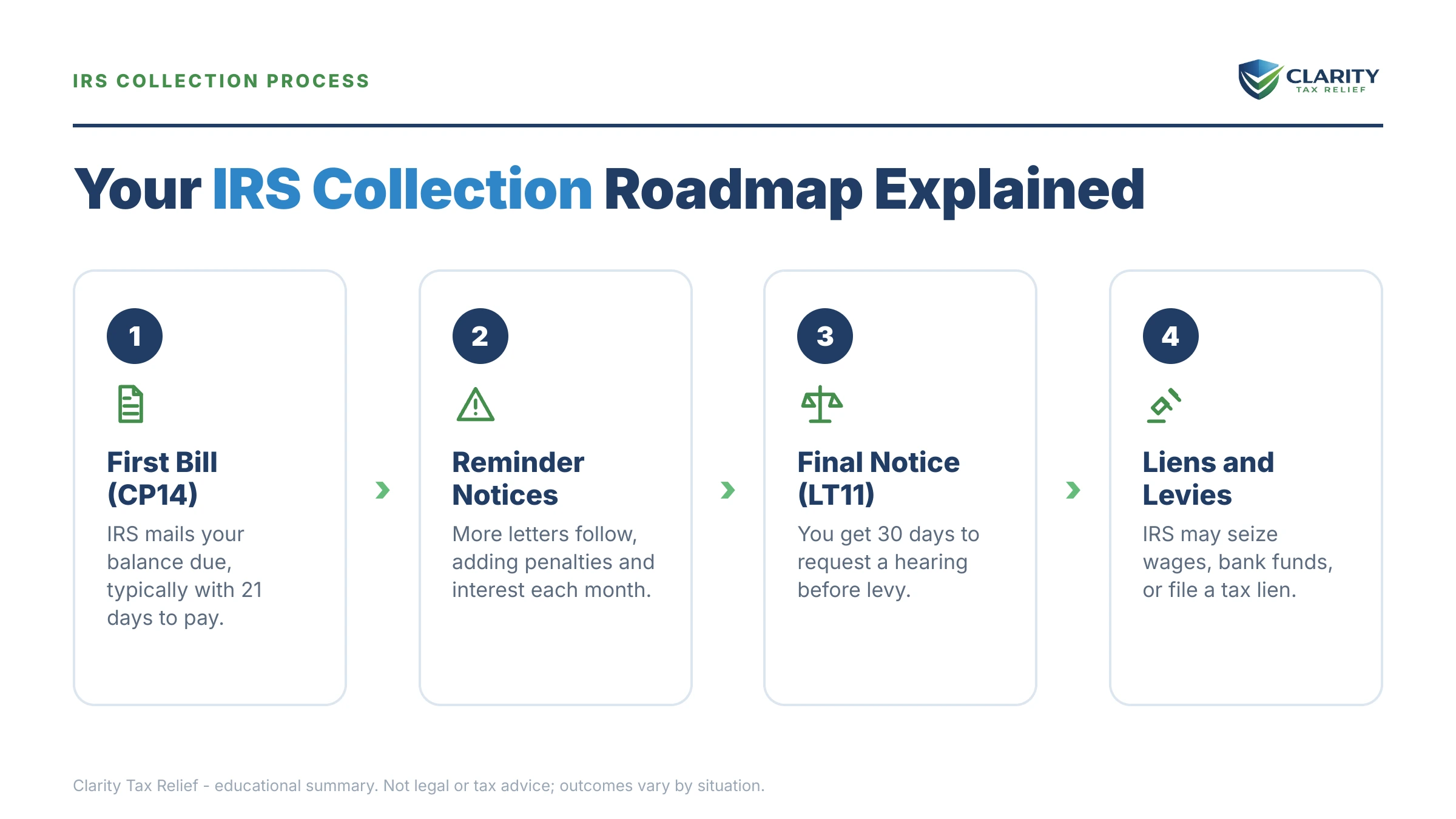

The image below lays out the full notice sequence at a glance, so you can match the letter on your kitchen table to its exact spot in the pipeline.

⏱ The clock that matters most: 30 days from the date on a final notice of intent to levy (LT11 or Letter 1058). Request a Collection Due Process hearing with Form 12153 inside that window and the IRS cannot levy while your case is heard. Every earlier notice sets its own pay-by date — always use the date printed on your letter.

Why the IRS collection process starts

Every IRS collection case begins with an assessment — the moment the IRS formally records a tax debt on its books. That happens when you file a return with a balance you didn't pay, when the IRS adjusts your return, when an audit or underreporter case closes with tax due, or when the IRS files a substitute return for a year you never filed.

The assessment date matters for two reasons. First, it triggers the notice sequence below. Second, it starts the IRS's 10-year collection statute — the deadline after which the debt generally becomes uncollectible (more on that clock further down).

From the day of assessment, interest compounds daily and the failure-to-pay penalty adds 0.5% of the unpaid tax each month. Nothing about the process requires a human at the IRS to decide anything — the notices are generated by computer, on schedule.

The IRS collection process step by step: from first bill to levy

The IRS collection process runs through five stages — first bill, reminders, intent to levy, final notice, then enforcement — and each stage adds power the previous one didn't have. For a letter-by-letter breakdown of every notice in this chain, see the order of IRS collection letters.

- Stage 1 — CP14, the first bill. The IRS states the balance, broken into tax, penalties, and interest, and gives you typically 21 days to pay (10 business days if you owe $100,000 or more). No enforcement exists yet — this is the cheapest moment in the entire process to resolve the debt. Full details in our CP14 notice guide.

- Stage 2 — CP501 and CP503, the reminders. Same balance, restated with fresh interest, typically arriving about five weeks apart. These letters carry no new powers, which lulls people into thinking the process stalled. It didn't — the computer is simply working through its queue.

- Stage 3 — CP504, notice of intent to levy. Sent by certified mail, this notice authorizes the IRS to seize your state tax refund under IRC §6331(d), and a federal tax lien filing becomes a realistic next move. Despite the alarming language, a CP504 is not the final notice — it cannot yet reach your wages or bank account. See the CP504 guide.

- Stage 4 — LT11 or Letter 1058, the final notice. This is the legal gateway to full enforcement. It starts a 30-day clock and attaches your Collection Due Process rights: file Form 12153 within those 30 days and levies stay on hold while an independent appeals officer reviews your case. Miss the window and the IRS may levy wages, bank accounts, and more. Our LT11 guide covers this notice in depth.

- Stage 5 — Enforcement. A bank levy freezes the funds with a 21-day hold before the bank sends them to the IRS. A wage levy is continuous — it takes a slice of every paycheck until released. The Federal Payment Levy Program can take up to 15% of Social Security benefits. A filed lien (announced by Letter 3172) attaches to everything you own, including your home.

You keep appeal rights even between notices: a CAP appeal can challenge a specific action — a lien filing, a levy, a rejected or terminated payment plan — often faster than a CDP hearing, though without the right to go to Tax Court afterward.

One 2026 reality worth naming: the IRS workforce shrank roughly 27% in 2025, so reaching a human is harder than ever — but the notice stream, lien filings, and levies are automated and never stopped. A thinner IRS does not mean a slower collection machine; it means fewer people to call when the machine reaches your paycheck.

| Stage & notice | What it means | Your response window |

|---|---|---|

| CP14 — first bill | Balance assessed; billing begins. No enforcement yet. | Typically 21 days (10 business days if $100,000+) |

| CP501 / CP503 — reminders | Same balance, growing monthly. No new powers. | Pay-by date printed on each notice |

| CP504 — intent to levy | State tax refund can be seized; lien filing likely soon. | Date printed on the notice |

| LT11 / Letter 1058 — final notice | Full levy power unlocks after 30 days; CDP rights attach. | 30 days to file Form 12153 |

| Enforcement — lien, levy, garnishment | Bank levy (21-day hold), continuous wage levy, 15% Social Security levy. | Immediate — negotiate a release |

Somewhere in this sequence right now?

Whether you're holding a first CP14 or a final LT11, an experienced tax professional will pinpoint your exact stage, your real deadline, and your best exit — free and confidential. Interest and the monthly late-payment penalty accrue while you wait.

Your off-ramp at every stage: resolution options compared

Every stage of the IRS collection process can be exited through one of five paths: full payment, a payment plan, hardship status, an Offer in Compromise, or penalty relief. Which one fits depends on your balance and your budget — and any of them, once approved, stops the escalation.

If you can pay in full, the cleanest routes are compared in our guide to the best way to pay the IRS. If you can't, the table below shows the thresholds that decide what you can set up — and our how to settle tax debt yourself pillar walks through each program in DIY detail.

| Option | Who typically qualifies | Cost & key terms |

|---|---|---|

| Short-term payment plan | Can pay in full within 180 days | $0 setup fee; interest and penalties keep accruing |

| Guaranteed installment agreement | Owe $10,000 or less with a compliant filing history | IRS must approve when the conditions are met |

| Streamlined installment agreement | Owe $25,000 or less — or up to $50,000 with direct debit | Up to 72 months; no financial statement required |

| Non-streamlined agreement | Owe more than $50,000 | Form 433-F financials; payment set by your budget |

| Currently Not Collectible | Paying anything would leave basic living costs uncovered | Collection paused; debt, interest, and refund offsets remain |

| Offer in Compromise | Assets plus future income genuinely can't cover the debt | $205 fee + 20% down on lump-sum offers (both waived if AGI ≤ 250% of the poverty level); roughly 1 in 5 offers accepted in FY2024 |

| Penalty abatement (FTA / AEP) | Clean compliance for the prior 3 years; AEP becomes automatic starting summer 2026 | Removes penalties, not the tax or interest |

Two notes on that table. An Offer in Compromise is real but means-tested — the IRS runs the math on your equity and future income, and most applicants don't qualify, which is why anyone promising a settlement before seeing your financials is selling, not advising. And penalty relief is changing: First-Time Abate currently requires a request, but the new Automatic Exemption from Penalty (AEP) begins applying qualifying relief automatically starting summer 2026, so don't pay someone just to ask for something the IRS may soon grant on its own.

What $68,500 in the collection pipeline actually looks like

Say you and your spouse filed jointly and owe $68,500 — a big filing-season surprise you couldn't pay. Because the return was joint, the liability is joint and several: the IRS can collect the entire amount from either of you, and enforcement can reach either spouse's wages plus any joint accounts.

Because the balance is over $50,000, the streamlined online payment plan is off the table. That leaves two realistic paths:

- Pay it under the threshold. If you can put $18,501 toward the balance — savings, a family loan, a home-equity draw — the remaining $49,999 fits a streamlined agreement with direct debit: roughly $694 a month over 72 months ($49,999 ÷ 72), with no financial disclosure required, while interest and the 0.5% monthly penalty continue on the shrinking balance.

- Disclose and negotiate. Keep the full $68,500 and submit Form 433-F financials for a non-streamlined agreement — see our guide to an IRS payment plan over $50,000. Spread over 72 months that's about $952 a month, but the actual payment is set by what your budget shows, which cuts both ways: it can come in lower, or the IRS can demand more if the numbers support it.

One more number matters at this balance: $68,500 sits above the $66,000 passport-certification threshold for 2026. If the debt becomes "seriously delinquent" — generally after enforcement milestones like a levy or a lien with lapsed appeal rights — the IRS can certify it to the State Department, which can deny a passport renewal. Getting a payment plan in place before that happens avoids the problem entirely; our passport revocation for tax debt guide covers the fix if it already has. An Offer in Compromise is unlikely here unless the couple's home equity and two incomes genuinely can't cover $68,500 within the collection window — for most two-income households at this balance, a payment plan is the honest answer.

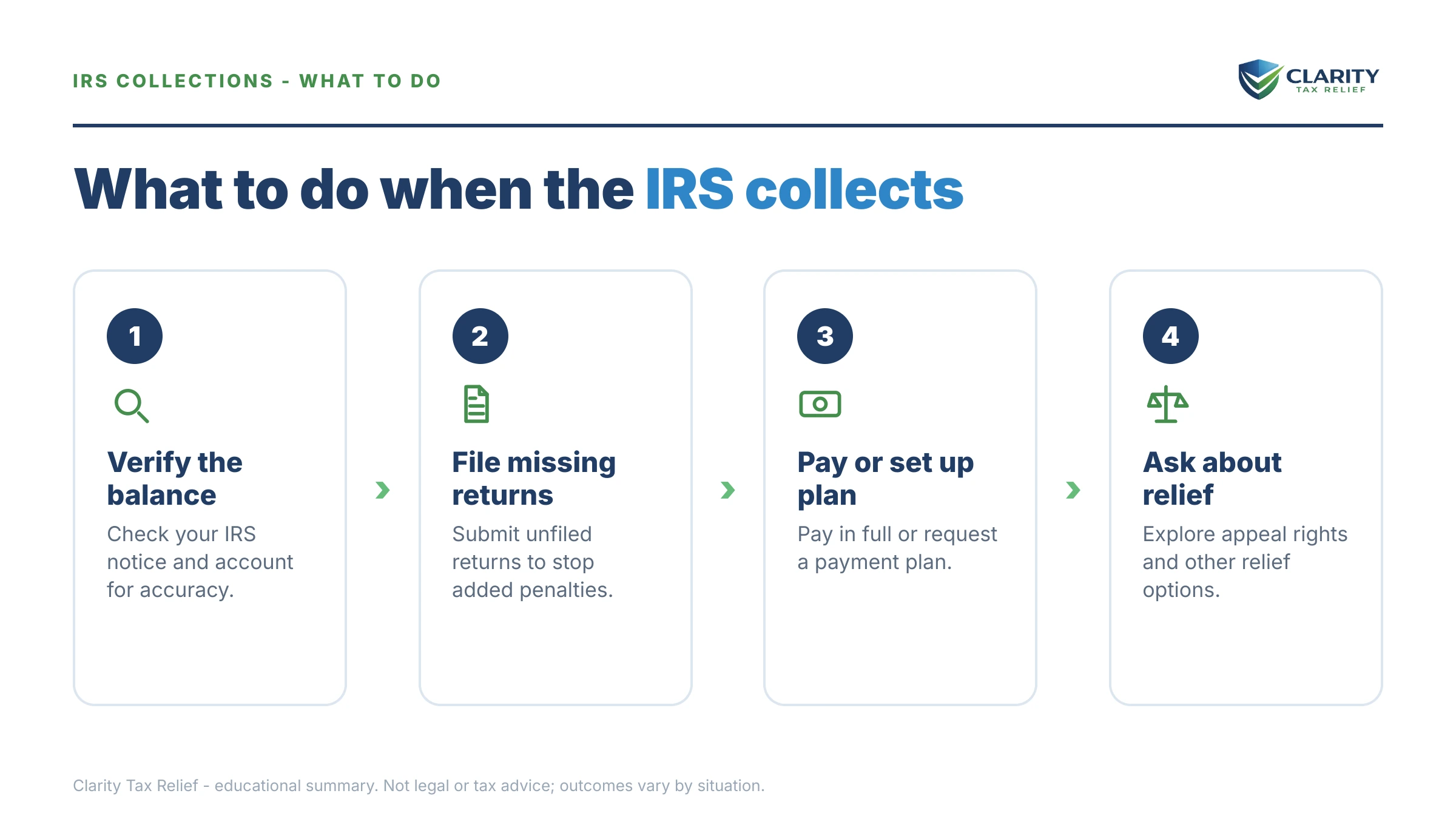

How to respond, step by step

- Identify your stage. Find the notice number in the top corner of your most recent IRS letter and the date it was issued — together they tell you exactly where you are in the sequence and how much time you have.

- Verify what you owe. Log into your IRS online account and compare the balance, tax years, and payments on record against your letter before you pay or negotiate anything.

- File any unfiled returns. The IRS will not approve a payment plan, hardship status, or an Offer in Compromise while required returns are missing — filing is the gate to every resolution.

- Choose your off-ramp before the next notice. Pick the option that fits your budget — a payment plan, Currently Not Collectible status, or an Offer in Compromise — and set it up now; every stage you wait removes choices and adds interest.

- Protect your appeal rights. If you are holding an LT11 or Letter 1058, request a Collection Due Process hearing with Form 12153 within 30 days — a timely request stops levies while your case is heard.

Most plans can be set up directly at the IRS's payment plans and installment agreements page, and payments of any kind go through IRS.gov/payments — never to a caller, a gift card, or a payment app.

The 10-year clock running underneath the whole process

Every assessed tax debt carries a Collection Statute Expiration Date (CSED) — generally 10 years from assessment — after which the IRS's legal right to collect ends. The collection machine is racing that clock, which is one reason enforcement intensifies rather than fades on older debts.

The clock pauses, though. Bankruptcy, a pending Offer in Compromise, and certain appeals all stop it from running, and each pause pushes the expiration date further out — the full list is in what extends the IRS collection statute. You can estimate your own expiration date with our CSED Calculator.

Older, lower-priority accounts sometimes take a detour: the IRS assigns them to a contracted private collection agency. Those contractors can call and write but cannot levy or file liens — and the IRS mails you a letter naming the agency before any call, which is how you separate a real contractor from a scammer.

When you can handle this yourself — and when help changes the outcome

You can usually resolve this on your own if you agree with the balance, owe $50,000 or less, and just need a plan: the streamlined agreement is a self-serve online setup, and a short-term plan costs nothing to establish. A single tax year with no notice past a CP503 is a DIY situation for most people.

Experienced help earns its cost when the stakes and the math get heavier: a final notice or levy already in motion, where the 30-day window and release negotiations are unforgiving; a balance over $50,000, where every number on Form 433-F shapes your monthly payment for years; multiple unfiled years that must be reconstructed before anything can be negotiated; business or payroll tax debt, which carries personal-liability risk; or an Offer in Compromise, where the calculation — not hope — decides acceptance. In those cases, the review is about protecting rights and money you can't get back later.

Terms in the collection process, decoded

- Assessment — the official recording of your tax debt on the IRS's books; it starts both the notice sequence and the 10-year collection clock.

- Lien — a legal claim against your property securing the debt; it doesn't take anything, but it attaches to what you own.

- Levy — the actual seizure of money or property: bank funds, wages, certain federal payments.

- CSED — Collection Statute Expiration Date, the day the IRS's 10-year right to collect ends (subject to pauses).

- CDP — Collection Due Process, your right to an independent appeals hearing before a levy, triggered by the final notice and requested on Form 12153.

- ACS — the Automated Collection System, the computer-and-call-center operation that runs most collection cases; only larger or complex cases get a human revenue officer.

If your account stalls in the system — a levy causing hardship the IRS won't release, or a resolution stuck in processing — the independent Taxpayer Advocate Service exists precisely to break those logjams.

IRS collection process questions, answered

How long does the IRS collection process take from first notice to levy?

For most taxpayers, the sequence from a CP14 to a levy-eligible final notice takes several months, because the automated notices arrive in order, typically about five weeks apart. But the pace varies — accounts can skip reminder notices, and an older debt can jump straight to a final notice. The only reliable timeline is the letter in your hand: each notice states its own deadline.

Can the IRS take money from my bank account without warning?

No — before levying a bank account or paycheck, the IRS must send a final notice of intent to levy (LT11 or Letter 1058) and give you 30 days to respond. What feels like 'no warning' is usually a string of notices mailed to an old address. Two exceptions: your state tax refund can be taken after a CP504, and rare jeopardy levies skip the notice when the IRS believes collection is at immediate risk.

Does the IRS collection process ever stop on its own?

Yes — the IRS generally has 10 years from the date of assessment to collect, a deadline called the CSED. When it expires, the remaining balance is written off. But the clock pauses for bankruptcy, a pending Offer in Compromise, and certain appeals, so the real expiration date is often later than year ten. Waiting it out also means living under liens and potential levies for a decade.

What is the difference between a tax lien and a levy?

A lien is a legal claim against your property that protects the government's interest — it doesn't take anything, but it attaches to your home and other assets and complicates selling or refinancing. A levy is the actual seizure: money out of your bank account, wages out of your paycheck. Liens can be filed relatively early in the process; a levy requires a final notice and a 30-day window first.

Can I stop IRS collections after a levy has already started?

Often, yes. A bank levy comes with a 21-day hold before the bank sends your money to the IRS, which is enough time to negotiate a release in many cases. A wage levy is continuous but ends the day the IRS approves an installment agreement, hardship status, or another resolution. The later you act, the fewer options remain — but a levy in motion is not the end of the road.

Are both spouses responsible for a joint tax debt?

Yes — a balance from a jointly filed return carries joint and several liability, meaning the IRS can collect the full amount from either spouse, in any mix. Levies can reach either spouse's wages and any joint accounts. Innocent spouse relief can shift liability in limited situations, such as one spouse hiding income from the other, but it must be requested and proven — it isn't automatic.

What does it mean if a private collection agency contacts me about IRS debt?

The IRS assigns certain older, inactive accounts to contracted private collection agencies, which can call and send letters but cannot levy, file liens, or threaten arrest. The IRS mails you a letter first naming the agency and giving you an authentication number the caller must match. Any payment still goes only to the U.S. Treasury — a caller asking for gift cards or wire transfers is a scammer, not a contractor.

Your next 24 hours

- Find the notice number and date on your most recent IRS letter — the number is in the top corner, and together with the date it pins your exact stage and your real deadline.

- Gather three things: your last filed return, every IRS letter you've received, and a rough picture of your monthly income and expenses — that's everything a resolution decision needs.

- Get a free case review — the 2-minute form at the top of this page or (888) 825-7779. Wherever you sit in the sequence, the next notice is already queued, and interest plus the monthly late-payment penalty accrue until a resolution is in place.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.