IRS Collections

Order of IRS Collection Letters: The Full 2026 Sequence, Explained

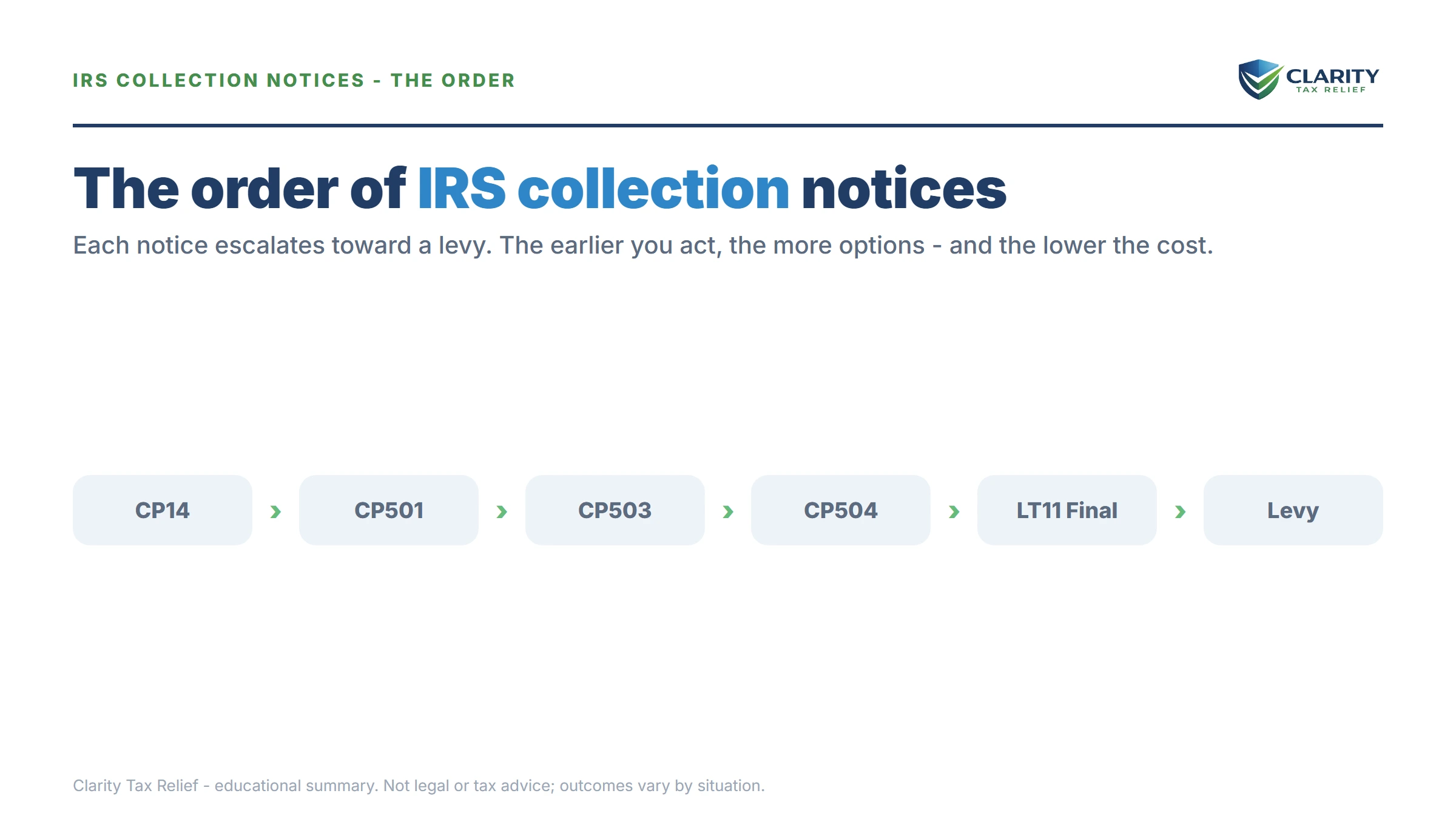

The short answer: the order of IRS collection letters is fixed — CP14 (the first bill), then CP501 and CP503 (reminders), then CP504 (intent to levy your state refund), then LT11 or Letter 1058 — the final notice that starts a 30-day clock before the IRS can levy wages, bank accounts, or up to 15% of Social Security.

You've almost stopped opening them. The first IRS envelope was a bill, the next one sounded firmer, and the one that arrived this week says "intent to levy" — words that land hard when your income is a monthly Social Security deposit that has to stretch. Here's what those envelopes don't tell you: they follow a strict, predictable order, each one tells you exactly how much time is left, and at every single stage there is still a move that stops the sequence cold.

This guide walks the whole ladder — what each letter is, what it legally allows the IRS to do, which rights attach to which notice, and where your best exits are. The image below lays the full sequence out at a glance, so you can place the letter in your hand on the map.

⏱ The one clock you can't get back: you have 30 days from the date on an LT11 or Letter 1058 — the final notice — to request a Collection Due Process hearing with Form 12153. Every earlier letter has its own pay-by date printed on it, but the 30-day final-notice window is the only deadline in the sequence that permanently costs you a right when it closes.

Why the IRS sends collection letters in a fixed order

Federal law forces the IRS to mail specific notices, in a specific order, before it can legally seize your wages or bank account. The CP504 exists because IRC §6331(d) requires a notice of intent to levy; the LT11 exists because §6330 requires a final notice with appeal rights. Each letter isn't just a warning — it's the IRS checking a legal box that moves it one step closer to enforcement.

Nobody at the IRS is sitting with your file deciding when to write next. The sequence is run by computers — campus systems generate the "CP" notices, and the Automated Collection System (ACS) generates the "LT" letters. The letters are produced on a schedule by machine, whether or not a human ever reviews your account. That matters in 2026: the IRS workforce shrank roughly 27% in 2025, so reaching a person is harder than ever — but the automated notice stream, and the automated levies behind it, never stopped. This article covers the letters themselves; for the full picture of what happens around them — liens, revenue officers, levies — see the complete IRS collection process step by step.

The order of IRS collection letters, first to last

Five letters make up the core individual collection sequence: CP14, CP501, CP503, CP504, and LT11 (or its twin, Letter 1058). Each has one job, and each raises the stakes over the last. The image below shows exactly where each letter sits in the sequence and which one actually opens the door to a levy.

| Letter (in order) | What it is | What the IRS can do at this stage |

|---|---|---|

| CP14 | The first bill — the IRS says you owe, with a pay-by date typically about 21 days out | Nothing enforced yet; penalties and interest accrue |

| CP501 | First reminder — "you have a balance due" | Still just a bill; balance keeps growing monthly |

| CP503 | Second reminder — "we haven't heard from you" | Still no enforcement; your cheapest window is closing |

| CP504 | Notice of Intent to Levy under IRC §6331(d) — usually certified mail | Can seize your state tax refund; a federal tax lien becomes a real possibility |

| LT11 / Letter 1058 | Final Notice of Intent to Levy and Notice of Your Right to a Hearing — certified mail | After 30 days: bank levies, wage levies, Social Security levies. You may request a CDP hearing within the window |

| CP90 | Final-notice variant aimed at federal payments, including Social Security | Same 30-day clock and hearing rights as the LT11 |

The order is fixed, but the run isn't identical for everyone. Some accounts skip the CP501 or CP503 entirely and jump from bill to CP504. Businesses see parallel versions (CP504B instead of CP504). And if your account sat dormant during the IRS's pandemic-era notice pause, you may have re-entered the sequence through an LT38 notice — a "collection is resuming" letter that restarts the ladder wherever you left off.

One letter confuses more readers than any other: the CP504's bold "Notice of Intent to Levy" heading makes it look like the end of the line. It isn't. A CP504 only authorizes the IRS to take your state tax refund — the LT11 or Letter 1058 is the notice that unlocks everything else. Reading the notice number, not the headline, is how you know your true position.

What happens if you ignore each collection letter

Only one letter in the sequence — the LT11 or Letter 1058 — gives the IRS legal authority to take your wages, bank account, or Social Security; everything before it is the countdown. Here is what ignoring each stage actually costs:

- Ignore the CP14 — nothing is seized, but the failure-to-pay penalty (0.5% per month) and daily-compounding interest start stacking, and the reminder notices queue automatically.

- Ignore the CP501 and CP503 — still no enforcement, but you're burning the stage where every resolution option is cheapest and no rights have been spent.

- Ignore the CP504 — the IRS can intercept your state tax refund, and a Notice of Federal Tax Lien — a public claim against everything you own — moves from possibility to likelihood. If your total debt reaches $66,000 (the 2026 threshold), passport certification also enters the picture.

- Ignore the LT11 / Letter 1058 for 30 days — the levy door opens. A bank levy freezes your account with a 21-day hold before the money leaves; a wage levy runs continuously until released; and Social Security can be cut by up to 15% through the Federal Payment Levy Program.

- Ignore everything after that — levies repeat, and older inactive accounts can be handed to a contracted IRS private collection agency. The debt doesn't quietly fade in the meantime: the 10-year collection statute keeps running, but several common events pause it — here's what extends the IRS collection statute.

A stack of IRS letters on the kitchen table?

The notice number on the newest one decides your deadline — and if it's an LT11 or Letter 1058, the 30-day window is already running. Send us a photo of the top letter and an experienced tax professional will tell you exactly where you are in the sequence and what your options are. Free and confidential.

Your options at each stage of the letter sequence

Every resolution option works better — and costs less — the earlier in the letter sequence you use it. The full playbook for each program lives in our guide to how to settle tax debt yourself; here's the map of what fits whom, and what each does to the letters:

| Option | Who typically qualifies | Cost to start | Effect on the sequence |

|---|---|---|---|

| Pay in full | Anyone able to pay | $0 | Ends the sequence immediately |

| Short-term plan (up to 180 days) | Balances you can clear within six months | $0 setup | Letters and enforcement stop; interest continues |

| Streamlined installment agreement | Balances up to $50,000; up to 72 months, set up online | Setup fee (reduced with direct debit; low-income waivers) | Letters stop while payments stay current |

| Guaranteed installment agreement | Balances of $10,000 or less with all returns filed | Setup fee (same tiers) | The IRS must accept it when the criteria are met |

| Currently Not Collectible | Income fully consumed by allowable living expenses | $0 (financial disclosure required) | Collection pauses; annual CP71 reminders continue; balance still accrues |

| Offer in Compromise | You can show the IRS could never collect the full amount | $205 fee (waived with low-income certification) | Collection generally held during review; roughly 1 in 5 offers accepted in FY2024 |

| Penalty abatement (FTA / AEP) | Clean compliance history for the prior 3 years | $0 | Shrinks the balance; pair it with a plan to stop the letters |

Two options exist only at specific rungs of the ladder. When the LT11 or Letter 1058 arrives, filing Form 12153 for a CDP hearing within 30 days generally pauses levy action and puts an appeals officer — a human — between you and the machine. And at any point where the IRS proposes or takes a specific collection action, a faster CAP appeal can challenge that action, though without the Tax Court rights a CDP hearing preserves.

Note on penalties: through mid-2026, First-Time Abate is the request-based path — but it's being replaced by the Automatic Exemption from Penalty (AEP) starting summer 2026, which applies without you asking. If your only penalty issue is a first slip after years of clean filing, relief may arrive on its own; the letters, however, won't stop until the underlying balance is addressed.

What waiting costs: a $13,600 example

Say you owe $13,600 from a retirement-account withdrawal two years ago, and your steady income is a $1,900 monthly Social Security check. This is hypothetical — but the arithmetic is real.

Act at the CP14 or reminder stage: $13,600 is under the $25,000 streamlined band, so you can set up a plan online with no financial disclosure. Stretched over the maximum 72 months, that's about $189/month ($13,600 ÷ 72 ≈ $188.90), and the failure-to-pay penalty rate is cut in half while the agreement is active. Interest still accrues, so paying faster saves real money — but the amount is yours to choose around your budget.

Ride it out to the levy stage instead: once the LT11's 30 days pass, the Federal Payment Levy Program can take 15% of your Social Security automatically — $285 every month (15% × $1,900) — chosen by a computer with zero regard for your rent, utilities, or prescriptions. Meanwhile the unabated 0.5% monthly penalty (about $68/month at the start) plus interest keeps inflating the balance the levy is chasing. Same debt; the imposed payment is nearly $100/month more than the negotiated one, and your savings account is exposed to a bank levy on top of it.

And here's the part the letters never mention: if that $1,900 genuinely covers only your basic living expenses, you may qualify for Currently Not Collectible status and pay nothing while it lasts — a far better outcome than a levy taking $285 you can't spare. Our guide for readers who are retired and owe back taxes walks that path in detail, and you can estimate how fast your own balance is growing with our IRS Penalty & Interest Calculator.

How to respond, step by step

- Find the notice number on your newest letter. Look at the top corner — CP14, CP503, CP504, LT11 — because that code, not the letter's tone, tells you which stage you're in and what the IRS can legally do next.

- Verify the balance in your IRS online account. Confirm the amount, check that recent payments posted, and note every year with a balance — a single letter may only show one year of several.

- Calendar the deadline printed on the letter. Every notice has a pay-by or respond-by date; if the letter is an LT11 or Letter 1058, mark the 30-day Collection Due Process deadline — it is the one date in the sequence you cannot recover.

- Set up the resolution that fits before the next letter. A payment plan, hardship status, or offer started at any stage stops the escalation — and the earlier you start it, the fewer rights you have already spent.

- Keep every letter and send any response by certified mail. Your stack of notices is the record of where you stand in the sequence, and certified mail is your proof that you responded on time.

When you can handle the letters yourself

Most people at the front of the sequence don't need professional help. If you're holding a CP14, CP501, or CP503, you agree with the balance, and you can either pay within 180 days or afford a streamlined monthly payment, you can resolve this in an afternoon: verify the balance, then follow our walkthrough on how to set up an IRS payment plan online at the IRS payment plans page, or pay directly at IRS.gov/payments. Setting up any accepted arrangement pulls your account out of the notice stream — no phone hold times required.

Experienced help changes outcomes in specific situations: an LT11 or Letter 1058 has arrived and the 30-day window is running; a levy is already hitting your Social Security or bank account; you have unfiled returns (the IRS generally won't grant agreements until they're in); you dispute the balance itself; or the debt is large enough that the IRS wants full financial disclosure. In those cases the order you fix things in — returns, penalties, then the balance — materially changes what you pay, and a levy in motion has release paths that are time-sensitive. If a levy is causing genuine hardship and you can't get traction, the Taxpayer Advocate Service is a free, independent option as well.

Terms on your letters, decoded

- Levy — the actual seizure of money or property (wages, bank funds, Social Security) to pay the debt.

- Lien — the government's legal claim against everything you own; it secures the debt but takes nothing by itself.

- CDP hearing (Collection Due Process) — the formal appeal the final notice grants; requested on Form 12153 within 30 days, it generally pauses levy action while your case is heard.

- CSED (Collection Statute Expiration Date) — the day the 10-year clock on the debt runs out, though appeals, offers, and bankruptcy pause it along the way.

- ACS (Automated Collection System) — the computer-driven IRS collection operation behind the "LT" letters; your account sits in it until resolution or levy.

- FPLP (Federal Payment Levy Program) — the automated program that can take up to 15% of Social Security and other federal payments once the final-notice window closes.

Order of IRS collection letters: common questions

What is the exact order of IRS collection letters?

The core sequence is CP14 (the first bill), CP501 and CP503 (reminders), CP504 (intent to levy your state refund), and LT11 or Letter 1058 (the final notice of intent to levy). Some accounts skip CP501 or CP503, and Social Security recipients may see a CP90 as their final notice instead. The notice number in the top corner of each letter tells you exactly where you are.

How much time passes between IRS collection letters?

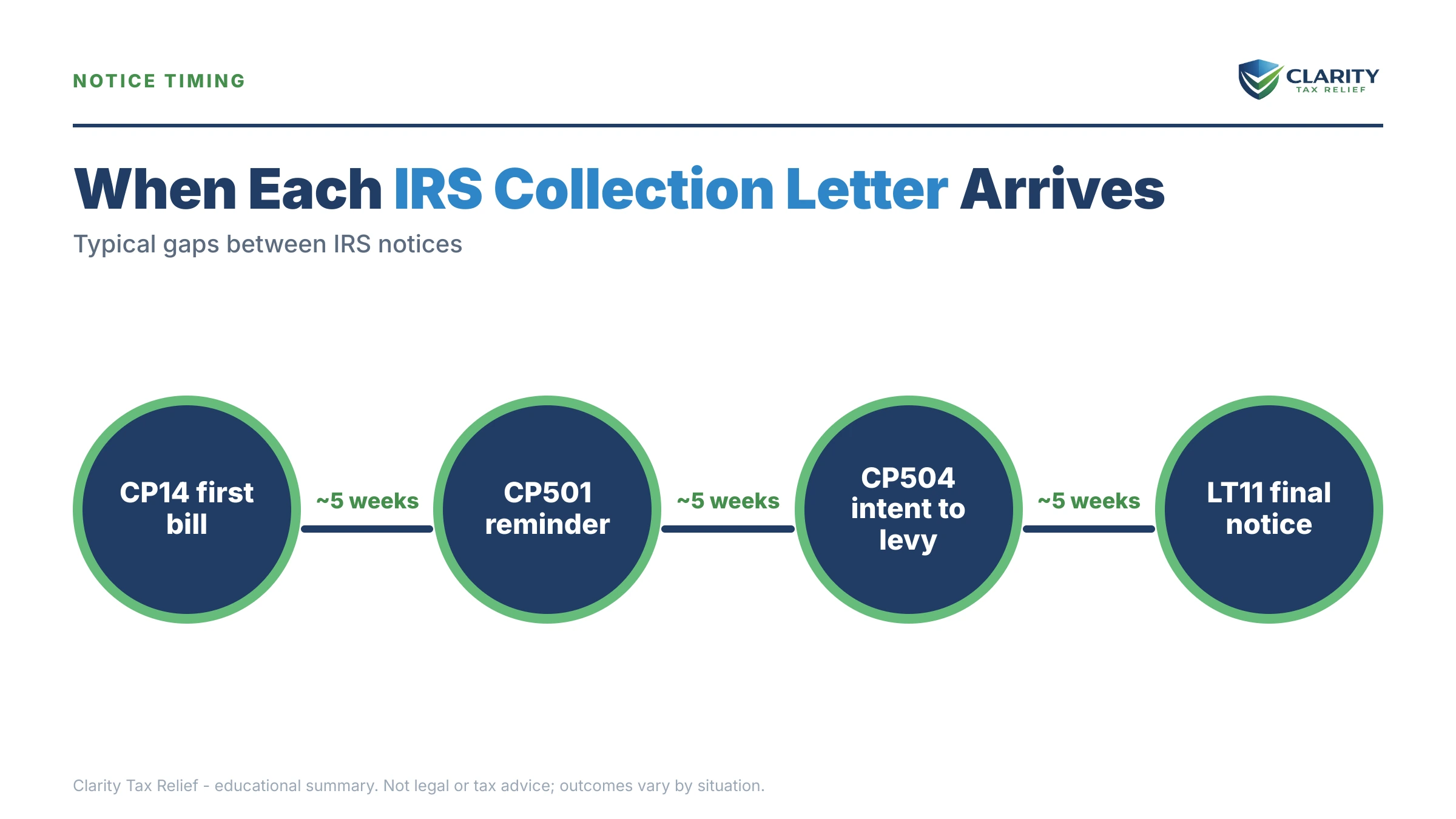

It varies — the IRS does not publish a fixed schedule, and gaps stretched after the 2025 staffing cuts. Letters typically arrive weeks apart, so a full run from CP14 to the final notice often takes several months. Never count on the gap, though: the only reliable deadline is the date printed on the letter in your hand.

Is the CP504 the final notice before the IRS can levy?

No — despite its alarming 'Notice of Intent to Levy' heading, a CP504 only lets the IRS seize your state tax refund. The true final notice is the LT11 or Letter 1058, which starts a 30-day clock and carries Collection Due Process appeal rights. That said, a CP504 means the final notice is next, so it is your last inexpensive moment to act.

Which IRS collection letters come by certified mail?

The CP504 and the final notice (LT11, Letter 1058, or CP90) are normally sent by certified mail, because the law requires proof the IRS attempted delivery before levying. Earlier bills like the CP14, CP501, and CP503 usually arrive by regular mail. A certified IRS envelope is a strong signal you have reached the enforcement end of the sequence — sign for it, because refusing delivery does not stop the clock.

Can the IRS skip the letters and levy me right away?

In almost all cases, no — the IRS must issue a final notice with 30-day appeal rights before levying wages or bank accounts. Narrow exceptions exist: state tax refunds can be taken after a CP504, and rare jeopardy levies skip notice when the IRS believes collection is at immediate risk. If money left your account and you never received a final notice, that is worth challenging.

What happens after the 30 days on an LT11 or Letter 1058 pass?

The IRS gains legal authority to levy. A bank levy freezes funds with a 21-day hold before the money is sent, a wage levy is continuous until released, and Social Security benefits can be reduced by up to 15% through the Federal Payment Levy Program. Requesting a Collection Due Process hearing within the 30 days generally pauses levy action while your case is heard.

Do the collection letters stop once I set up a payment plan?

Yes — an accepted installment agreement or short-term plan takes your account out of the collection-notice stream, and levy action stops while the agreement is in good standing. You will still get routine mail: annual balance reminders (CP71) and payment-plan statements, and the IRS will keep any tax refunds and apply them to the balance. Miss payments, and a CP523 default notice restarts the sequence.

Why is a private collection agency writing to me instead of the IRS?

The IRS assigns some older, inactive accounts to a small number of contracted private collection agencies, and it sends you a letter naming the agency before the agency ever contacts you. Private collectors cannot levy, file liens, or threaten arrest — they can only ask for payment, and payments still go to the U.S. Treasury, never to the agency. Anyone demanding gift cards or wire transfers is a scammer.

Your next 24 hours

- Sort your letters by date and read the notice number on the newest one — the code in the top corner (CP14 through LT11) tells you your stage, and the date printed beside it sets your deadline.

- Gather the full stack, your last filed tax return, and proof of your income — SSA-1099, pension statements, bank statements — so whichever option fits can be set up the same day.

- Get a free case review — use the 2-minute form or call (888) 825-7779. If the newest letter is an LT11 or Letter 1058, do this today: the 30-day hearing window is running, and it is the one deadline in the entire sequence you cannot get back.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.