IRS Notices

IRS CP90 Notice: Final Notice of Intent to Levy — What to Do in 2026

The short answer: a CP90 notice is the IRS's Final Notice of Intent to Levy — the last letter the law requires before the IRS can seize wages, bank accounts, and federal payments. You have 30 days from the notice date to file Form 12153 for a Collection Due Process hearing, which generally pauses levy action.

Maybe you were pulling together pay stubs and mortgage statements for a refinance when a certified IRS envelope landed on top of the pile — and this one doesn't say "reminder," it says the IRS intends to seize your assets. That jolt is real, and so is the deadline. But nothing has been taken yet, and the same 30 days the IRS gives itself before it can levy is 30 days of genuine leverage for you.

Unlike every bill and reminder that came before it, a CP90 carries a legal right no earlier notice did: the right to a Collection Due Process (CDP) hearing that freezes levy action while an independent appeals officer reviews your case. Use it or lose it — the window is exactly 30 days.

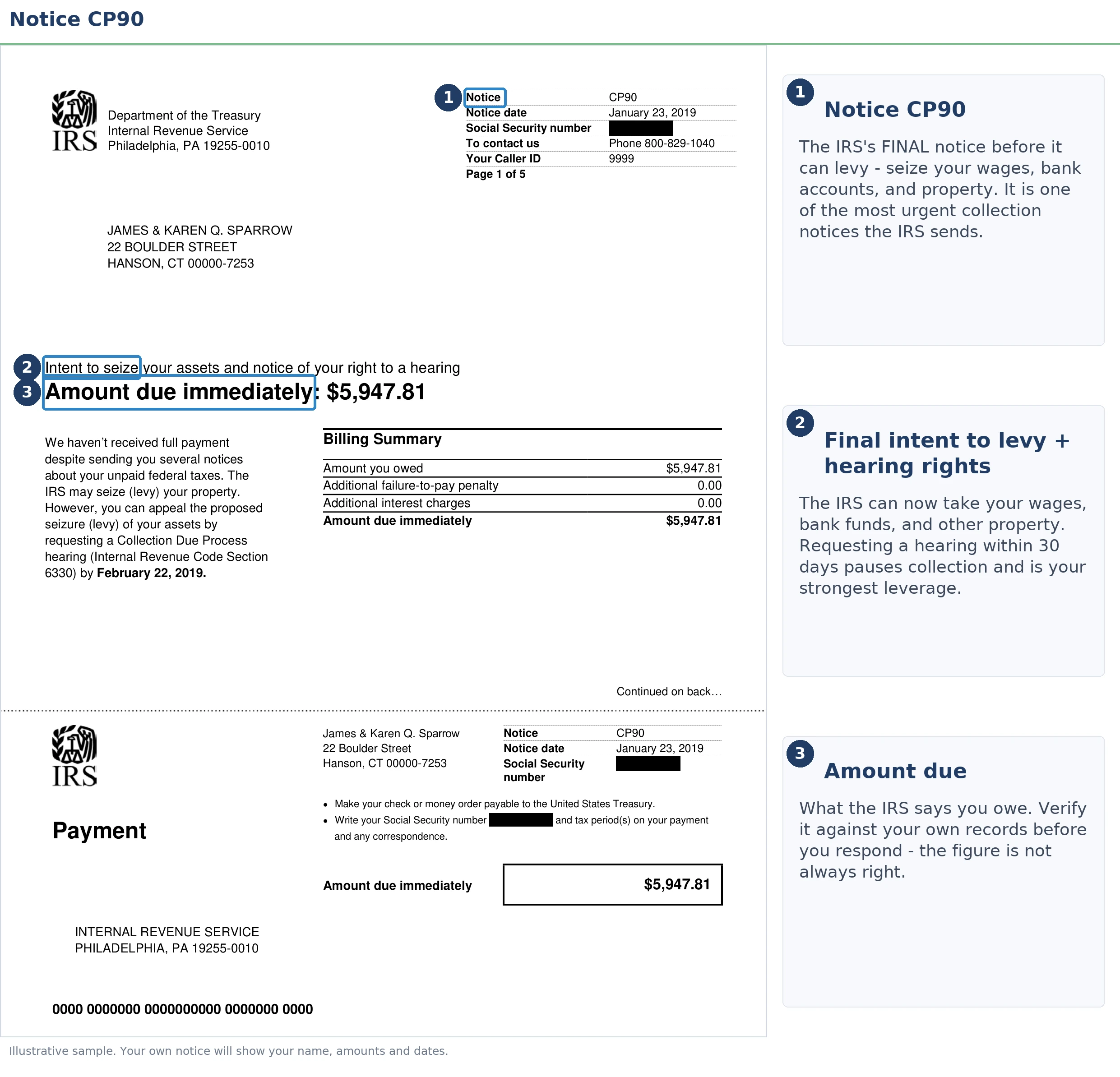

The image below shows exactly what a CP90 looks like and where to find the two lines that control everything: the notice date that starts your 30-day clock, and the total balance the IRS intends to collect.

⏱ Your deadline: you have 30 days from the date printed on your CP90 to request a Collection Due Process hearing on Form 12153. The clock runs from the notice date — not the day the letter arrived or the day you signed for it. After day 30, the IRS can levy without sending you anything else.

Why you got a CP90 notice

A CP90 means earlier IRS bills for a balance went unanswered, and the agency's automated system has now issued its last legally required warning before levy. Under IRC §6330, the IRS must give you notice and a hearing opportunity before seizing most assets — the CP90 is that notice for individual taxpayers, and it typically arrives by certified mail.

The balance behind it can come from several places: a return you filed but didn't fully pay, a return the IRS adjusted (a balance-due adjustment arrives as a CP11 notice; a refund-side adjustment as a CP12 notice), an audit assessment, or accumulated penalties and interest on a debt you thought was smaller. The CP90 itself lists the tax periods and the total for each — check every year listed, because a single wrong period changes your whole strategy.

If you're trying to piece together how the IRS got from "you owe" to "final notice," our guide to why you got a letter from the IRS maps the entire notice system in one place. The short version: you're at the end of the warning chain, not the middle.

CP90 vs. LT11, Letter 1058, and CP504: same law, different sender

Four different IRS letters carry the exact same legal weight as a final notice of intent to levy — the CP90 is simply the version generated by the IRS's automated campus systems. An LT11 notice comes from the Automated Collection System, and a Letter 1058 comes from an assigned revenue officer (which signals a human is now working your case). Businesses get the CP297 instead.

Don't confuse any of these with the CP504 notice that likely came before your CP90. A CP504 only authorizes seizure of your state tax refund. The CP90 is the notice that unlocks everything else — wages, bank accounts, Social Security — once its 30 days pass.

| Notice | What it means | What the IRS can do |

|---|---|---|

| CP14 | First bill, typically ~21 days to pay | Nothing yet — balance accrues |

| CP501 / CP503 | Automated reminders | Still no enforcement — balance grows |

| CP504 | Intent to levy state refund (IRC §6331(d)) | Seize your state tax refund only |

| CP90 / LT11 / Letter 1058 | Final notice + 30-day CDP rights | After 30 days: levy wages, bank accounts, federal payments |

| Levy notices (e.g., CP91) | A specific levy is executing | Money is actively being taken |

Your 30-day Collection Due Process window

Form 12153, filed within 30 days of your CP90's date, generally bars the IRS from levying the listed tax periods while an independent appeals officer hears your case. That hearing isn't just for disputing the debt — you can propose an installment agreement, an Offer in Compromise, hardship status, or challenge a lien filing, and the levy stays off while it's considered. Our Form 12153 CDP hearing guide walks through the form line by line.

A timely CDP request also preserves something you can't get back later: the right to take a disputed decision to U.S. Tax Court. Miss the 30 days and you can still get an "equivalent hearing" for up to one year — but it doesn't block levies and doesn't preserve court review.

One honest caveat: a pending CDP hearing pauses the 10-year collection statute (the CSED). Filing purely to run out the clock usually backfires — the clock stops while you wait. File because you have a dispute or an alternative to propose, not as a stall.

| When you act | What you can file | What it protects |

|---|---|---|

| Within 30 days of the notice date | Form 12153 (CDP hearing) | Levy generally barred while pending; Tax Court review preserved; CSED paused |

| Day 31 through 1 year | Form 12153 (equivalent hearing) | Appeals still hears you — but no levy bar and no Tax Court review |

| After a levy hits | Hardship release request; collection alternatives | Possible release of the levy — but seized funds may already be gone |

What the IRS can levy after a CP90

Once the CP90 window closes, the IRS can reach wages, bank accounts, Social Security, and most other income sources without sending another warning. Each levy type works differently, and the differences matter for planning:

- Bank accounts: the bank freezes the balance on the day the levy arrives, holds it for 21 days, then sends it to the IRS. Those 21 days are your release window — see the IRS bank levy 21-day rule.

- Wages: a wage levy is continuous — it repeats every paycheck until released, leaving you only an exempt amount. You can estimate what a levy could reach with our IRS Wage Garnishment Calculator.

- Social Security: up to 15% of each monthly benefit through the Federal Payment Levy Program. If that levy executes, you'll typically see a CP91 notice.

- State refunds and federal payments: intercepted automatically once you're in levy status.

- Your home: seizing a principal residence requires federal court approval and is genuinely rare. For a homeowner, the practical threat is the federal tax lien — more on that below.

What happens if you ignore a CP90

Ignoring a CP90 moves you from the warning stage to the enforcement stage — after this notice, the next thing you receive may be your bank telling you the account is frozen. The sequence from here runs on automation, and with the IRS workforce down roughly 27% since 2025, the computers issuing levies are the one part of the agency still operating at full speed:

- Day 0: the CP90 is issued, usually by certified mail. The 30-day CDP clock starts from the printed date whether or not you pick up the letter.

- Day 30: your CDP rights expire. The levy bar and your Tax Court review right are gone.

- After day 30: systemic levies begin queuing — state refund intercepts, bank levies with their 21-day hold, continuous wage levies, and the 15% Social Security levy.

- Lien filing: if a federal tax lien hasn't already been filed, an unresolved final-notice balance makes one likely. The lien attaches to everything you own — including the home you're trying to refinance.

- Passport certification: once penalties and interest push the balance past $66,000 (the 2026 threshold), the IRS can certify the debt to the State Department, blocking passport issuance or renewal.

- The long tail: absent resolution, the account stays in enforced collection until the 10-year statute expires — accruing a 0.5% monthly failure-to-pay penalty plus compounding interest the entire time.

Holding a CP90 with the clock already running?

Get your CP90 reviewed free before the 30-day Collection Due Process window closes. An experienced tax professional will confirm your exact deadline, tell you whether Form 12153 makes sense in your case, and map the resolution that fits your numbers — no pressure, no obligation.

Your options after a CP90 (and what each costs)

An account in an approved arrangement is not an account the IRS levies — which is why setting up any legitimate resolution before day 30 defuses the CP90. Which one fits depends on your balance and your finances:

- Full payment stops penalty and interest accrual immediately and ends the collection sequence. If home equity or savings can cover it, this is often the cheapest path over time.

- Short-term payment plan — up to 180 days to pay in full, $0 setup fee. Interest and penalties continue, but levy action stops while you're in it.

- Streamlined installment agreement — balances of $50,000 or less can be set up online for up to 72 months without detailed financial disclosure. Above $50,000, you'll typically need Form 433-F financials or a paydown to get under the line — our guide to an IRS payment plan over $50,000 covers both routes.

- Currently Not Collectible status — if paying anything would prevent you from covering basic living expenses, collection can be paused. The debt remains and usually a lien is filed, but levies stop.

- Offer in Compromise — settling for less than the full balance when your income and assets genuinely can't cover the debt. It's real but means-tested: $205 application fee, 20% down on lump-sum offers (both waived with low-income certification), and the IRS accepted roughly 1 in 5 offers in FY2024.

- Penalty relief — first-time abatement can remove penalties if your prior three years were clean, and starting summer 2026 the new Automatic Exemption from Penalty (AEP) applies similar relief automatically, with no request needed. Reducing penalties shrinks the balance every other option has to solve.

| Option | Upfront cost | Timeline | The catch |

|---|---|---|---|

| Full payment | The balance itself | Immediate | None — accrual stops, sequence ends |

| Short-term plan | $0 setup fee | Up to 180 days | Interest and penalties keep accruing |

| Streamlined installment agreement | Setup fee (lower with direct debit; reduced for low income) | Up to 72 months | Balance must be $50,000 or less |

| Non-streamlined installment agreement | Setup fee + Form 433-F financials | Negotiated with the IRS | IRS reviews income, expenses, and equity |

| Currently Not Collectible | $0 (financial disclosure required) | Until finances improve | Lien likely; debt keeps growing |

| Offer in Compromise | $205 fee + 20% down (waived for low income) | Months to 2 years (auto-accepted if no decision in 2 years, with narrow exceptions - a returned or rejected offer stops the clock, and time during court disputes does not count) | Means-tested — roughly 1 in 5 accepted in FY2024 |

Worked example: a $61,200 balance and a refinance in motion

Say you owe $61,200 across two tax years and a CP90 just arrived while you're preparing to refinance your home. Here's how the numbers actually play out — this is a hypothetical, not a client case:

- Doing nothing: the failure-to-pay penalty alone runs 0.5% a month — about $306 a month on $61,200 — plus compounding interest. You're currently $4,800 below the $66,000 passport certification threshold; on a do-nothing path, accrual alone can push you across it within roughly a year.

- The streamlined route: pay down $11,200 to bring the balance to $50,000, and you can set up a 72-month online agreement without handing over financials — roughly $695 a month ($50,000 ÷ 72) before the interest that continues to accrue.

- The full-balance route: keep the $61,200 intact and negotiate a non-streamlined agreement with Form 433-F financials. Spread over 72 months as an illustration, that's about $850 a month before accrual, though the actual terms depend on what your financials support.

- The refinance route: if your home has enough equity, a cash-out refinance that pays the IRS in full at closing often beats years of accrual — but only if the loan actually closes, which is exactly what an unresolved CP90 threatens.

Notice what the CDP window does in this scenario: a timely Form 12153 filing keeps a bank levy from landing mid-escrow while you finish underwriting. A frozen account during closing is the kind of surprise that kills loans.

Getting a CP90 while you're trying to refinance

A CP90 doesn't appear on your credit report or your title — the refinance-killer is the federal tax lien that frequently follows an unresolved final notice. Once filed, the lien attaches to your home, and most lenders won't close until it's addressed. You have three workable paths, in rough order of preference:

- Resolve before a lien is filed. Getting into an installment agreement now — before the IRS records a lien — is the cleanest outcome for underwriting. Timing is the whole game here.

- Pay the IRS from closing proceeds. If your cash-out covers the balance, the debt can be satisfied at the closing table, with the lien (if any) released after payment.

- Request lien subordination. If a lien is already recorded and the numbers work, Form 14134 lien subordination asks the IRS to let the new mortgage jump ahead of the lien so the loan can close — the IRS often agrees when the refinance improves its odds of getting paid. Our guide to refinancing with an IRS lien covers the lender side.

Whatever path you choose, tell your loan officer early. A tax balance discovered by the underwriter days before closing is far more damaging than one you disclosed with a resolution plan attached.

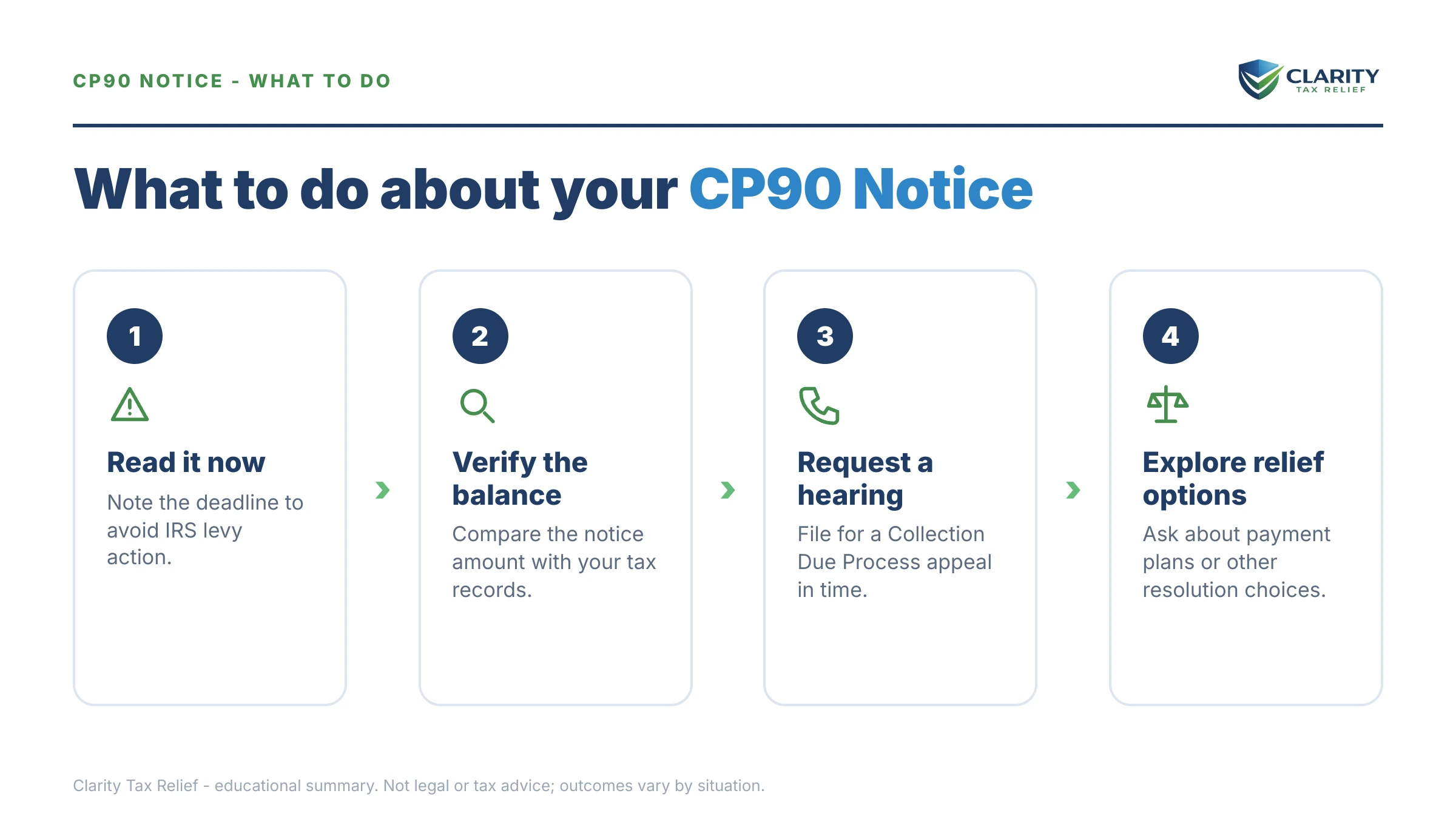

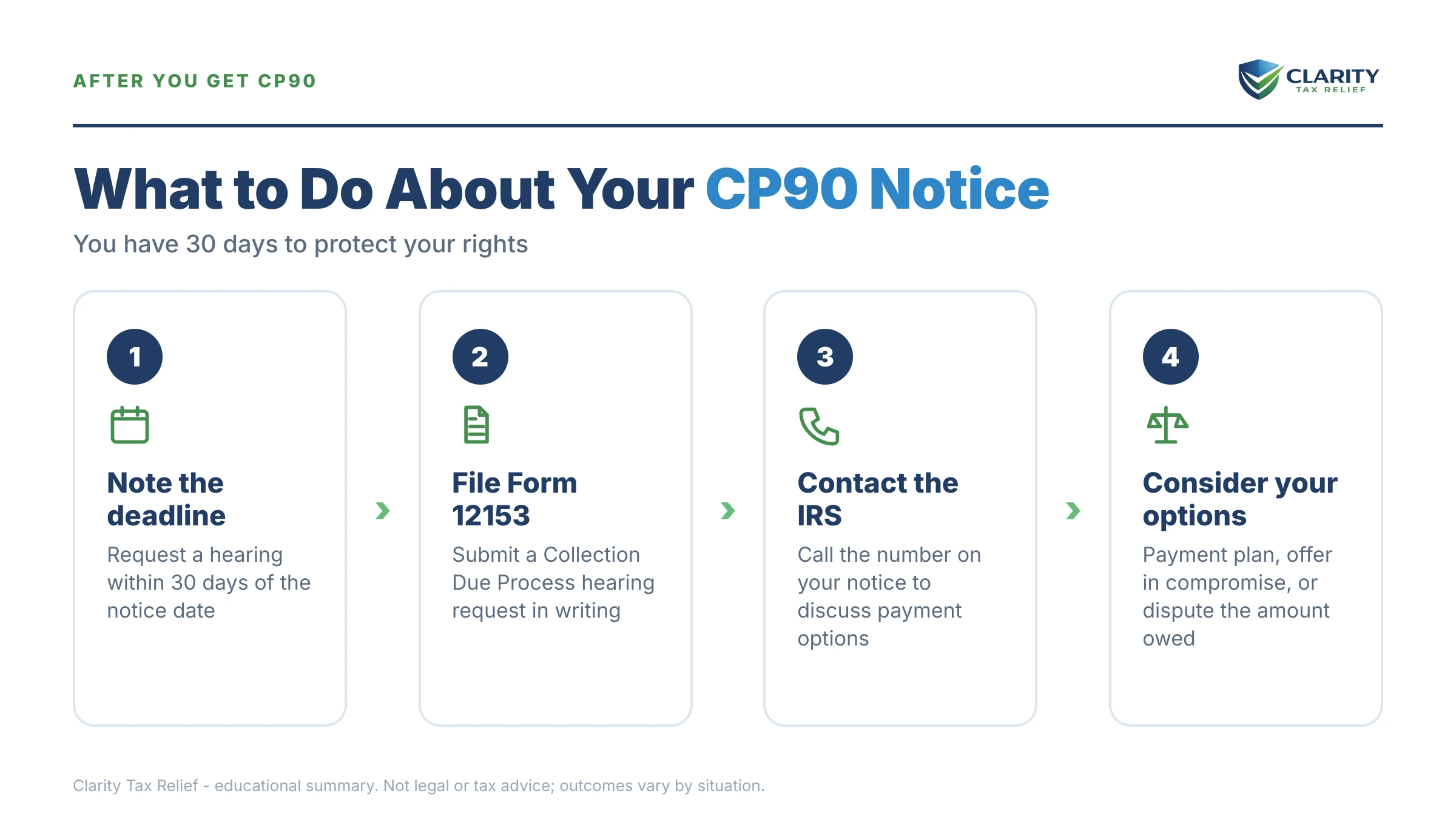

How to respond to a CP90, step by step

- Find your notice date and mark day 30. The date printed on the CP90 starts your 30-day Collection Due Process clock — not the day the letter arrived or the day you signed for it. Count 30 days forward and write that date down; every decision below has to happen before it.

- Verify the balance and the tax years. Log into your IRS online account and compare the balance and tax periods against the notice. Confirm every year listed is genuinely yours and that recent payments actually posted before you commit to a plan built on the wrong number.

- Decide whether to file Form 12153. If you dispute the debt, need levy action barred while you arrange financing, or want Appeals to consider a collection alternative, file Form 12153 before day 30. A timely filing preserves your Tax Court review rights and generally stops levy action while the hearing is pending.

- Set up your resolution before the window closes. Choose the option that fits your finances — full payment, a payment plan, Currently Not Collectible status, or an Offer in Compromise — and get it submitted or in place before the deadline passes. An account in an approved arrangement is not an account the IRS levies.

- Get experienced help for high-stakes situations. If the balance is over $50,000, a levy is imminent, you have unfiled years, or a refinance or sale is in motion, have an experienced tax professional review the notice before you commit to a path.

When you can handle a CP90 yourself

Plenty of CP90 situations don't need professional help, and it would be dishonest to pretend otherwise. You can likely handle this yourself if:

- You agree with the balance and can pay it in full, or within 180 days on a short-term plan.

- Your balance is under $50,000 and your only need is a streamlined online installment agreement — the IRS's payment plans page handles that in one sitting.

- The notice is simply wrong in a documentable way — a payment that didn't post — and you have the proof in hand.

Experienced help genuinely changes outcomes when the stakes go up: a balance over $50,000 where Form 433-F numbers get negotiated, a levy already in motion, multiple unfiled years that must be resolved first, Offer in Compromise math, or a refinance or sale that a lien could derail. In those cases, the difference between a well-argued CDP hearing and a missed one is often measured in tens of thousands of dollars. If cost is the barrier, the Taxpayer Advocate Service and Low Income Taxpayer Clinics exist for exactly that gap.

If your CP90 sits on top of a refinance, a levy threat, or a balance over $50,000, a free CP90 review at (888) 825-7779 — or the two-minute form — will map your options before the 30-day window decides them for you.

Terms on your CP90, decoded

- Levy: the actual seizure of money or property — a bank account, a paycheck, a federal payment.

- Lien: a recorded legal claim against everything you own; it doesn't take anything, but it clouds your title and complicates sales and refinances.

- Collection Due Process (CDP): your statutory right to an independent Appeals review before levy — the right this notice exists to give you.

- Form 12153: the one-page form that requests a CDP hearing; timely filing is what pauses levy action.

- Equivalent hearing: the consolation version available for up to a year after the deadline — Appeals listens, but levies aren't barred and Tax Court review is off the table.

- CSED: the Collection Statute Expiration Date — 10 years from assessment, paused by CDP hearings, Offers in Compromise, and bankruptcy.

The IRS's own summary of this notice is at Understanding your CP90 notice — worth reading alongside this guide, since it's the exact language Appeals will use.

CP90 notice questions, answered

Is a CP90 the same as an LT11 or Letter 1058?

Legally, yes — all three are final notices of intent to levy that carry the same 30-day Collection Due Process rights. The difference is who sent it: a CP90 comes from the IRS's automated campus systems, an LT11 from the Automated Collection System, and a Letter 1058 from an assigned revenue officer. Your deadline and your options are identical for all three.

How long after a CP90 can the IRS levy?

The IRS can levy any time after the 30-day window on your CP90 expires. That doesn't mean a levy hits on day 31 — automated levies queue up on their own schedule — but the legal barrier is gone. A Form 12153 filed within the window generally blocks levy on those tax periods while your hearing is pending.

Does filing Form 12153 stop an IRS levy?

A Form 12153 filed within the 30-day window generally prevents the IRS from levying the tax periods listed on your CP90 while your Collection Due Process hearing is pending, and it preserves your right to take a disputed decision to Tax Court. Know the trade-off: the 10-year collection statute pauses while the hearing is open, so use the time to line up a real resolution, not just to delay.

What if I missed the 30-day deadline on my CP90?

You can still request an equivalent hearing by filing Form 12153 within one year of the CP90 date. Appeals will hear the same issues, but an equivalent hearing does not bar the IRS from levying while it's pending and does not preserve Tax Court review. If a levy has already hit, hardship releases and collection alternatives can still get it lifted.

Can the IRS take my house after a CP90?

It's legally possible but genuinely rare — seizing a principal residence requires federal court approval and is reserved for the most serious cases. The realistic threats after a CP90 are wage levies, bank levies, and a federal tax lien against your home's title. The lien is what damages homeowners in practice, because it can stall a sale or refinance until it's addressed.

Can the IRS levy my Social Security after a CP90?

Yes. Once the CP90 window closes, the IRS can take up to 15% of your Social Security benefits through the Federal Payment Levy Program, and the levy repeats every month until the debt is resolved or the levy is released. If that 15% would leave you unable to cover basic living expenses, you can pursue a hardship release or Currently Not Collectible status.

Can I still refinance my home after getting a CP90?

Often yes, but timing is everything. A CP90 itself doesn't appear on your title — the danger is the federal tax lien that frequently follows an unresolved final notice, which most lenders require you to address before closing. Options include paying the IRS from closing proceeds, requesting lien subordination on Form 14134, or getting into an installment agreement before a lien is filed.

Why did I get a CP90 instead of a call from the IRS?

Because IRS collections run on automation, not people. The IRS workforce shrank roughly 27% in 2025, but the notice and levy systems are computerized and never stopped. A CP90 is generated automatically when earlier notices go unanswered — no employee reviewed your file, and none will unless you, or a levy, force the issue.

Does a CP90 put my passport at risk?

Not by itself, but the balance behind it might. The IRS certifies seriously delinquent tax debt to the State Department at $66,000 for 2026, which can block passport issuance or renewal. A balance below that line keeps growing through penalties and interest, so a debt in the low $60,000s can cross the threshold within months of inaction.

Your next 24 hours

- Find the notice date on your CP90 and count 30 days forward. Write that date somewhere you'll see it — it's your Form 12153 deadline, and it's the only date on the letter that matters.

- Gather three things: the CP90 itself, your most recent tax return, and proof of your current income — plus your refinance or loan paperwork if one is in motion.

- Get a free CP90 case review before the 30-day window closes — the 2-minute form or (888) 825-7779. Thirty days is enough time to do this right; it is not enough time to wait and see.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.