IRS Notices

IRS CP297 Notice: Final Notice of Intent to Levy — Your 30-Day Rights (2026)

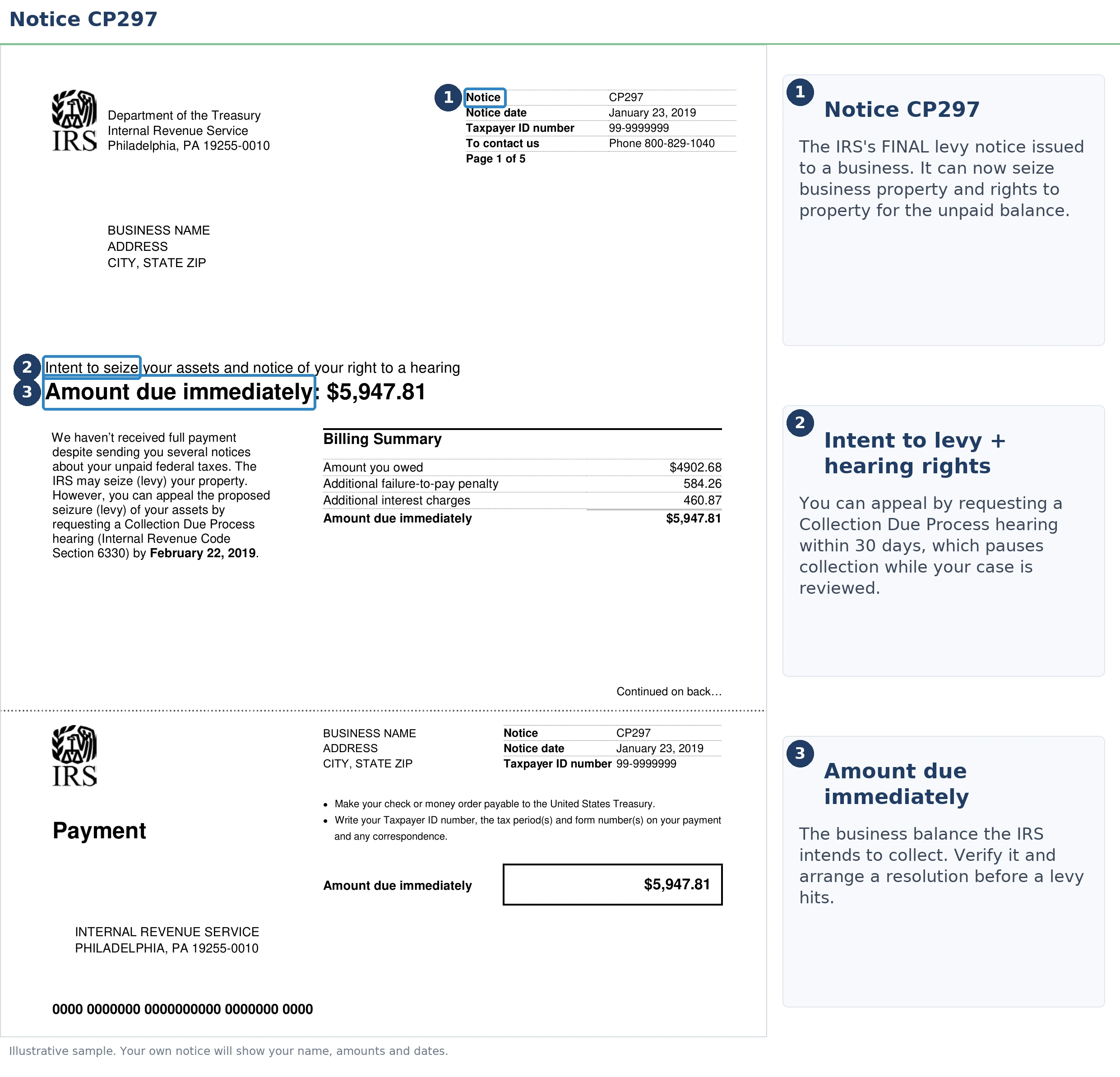

The short answer: a CP297 notice is the IRS's Final Notice of Intent to Levy and Notice of Your Right to a Hearing, most often sent for unpaid business taxes. You have 30 days from the notice date to request a Collection Due Process hearing on Form 12153 — after that window closes, the IRS can levy without further warning.

The certified-mail slip had your business's name on it, and the letter you signed for says the IRS "intends to levy certain assets." That wording is deliberate: in 2026, a CP297 is the last legally required warning before the IRS can reach bank accounts, receivables, and other property. The same letter also hands you the strongest appeal right in the entire collection process — and the clock on that right starts on the notice date, not the day you opened the envelope.

If you're not sure which figures on the page control your response, the image below shows exactly what a CP297 looks like and where to find the two entries that matter most: the notice date and the total amount due.

⏱ Your deadline: you have 30 days from the date printed on your CP297 to request a Collection Due Process hearing using Form 12153. A timely request generally blocks levy action while IRS Appeals reviews your case. After day 30, the IRS can levy without sending another notice.

Why you got a CP297 notice

A CP297 means an unpaid tax balance — usually on a business account — has survived every earlier bill, and the IRS is now satisfying its legal duty to warn you before seizing assets. The debt is often unpaid Form 941 payroll tax, but 940, 1120, or civil-penalty balances travel the same road. (If you're still working out why the IRS is writing at all, start with why did I get a letter from the IRS.)

The CP297 sits in a family of final notices that all do the same legal job. A CP90 notice is the individual version, an LT11 notice comes from the IRS's Automated Collection System, and a CP297A notice means the IRS has already levied certain payments and is granting hearing rights after the fact. If your CP297 involves unpaid payroll quarters, the deeper problem — and its fixes — are covered in our guide to 941 back taxes.

Here is where the CP297 falls in the business collection sequence, so you can see exactly how much runway is left:

| Notice | What it says | Your window |

|---|---|---|

| CP161 | First bill: balance due on a business return | The pay-by date printed on the notice |

| CP504B | Intent to levy state refunds and certain property — urgent, but not the final notice | Pay-by date on the notice; typically about five weeks before the next step |

| CP297 (you are here) | Final Notice of Intent to Levy + right to a Collection Due Process hearing | 30 days to file Form 12153 before levy authority activates |

| CP297A | A levy on certain federal payments has already been issued; hearing rights granted after | Hearing window stated on the notice |

| Levy | Bank accounts, receivables, and other assets seized | No further warning required |

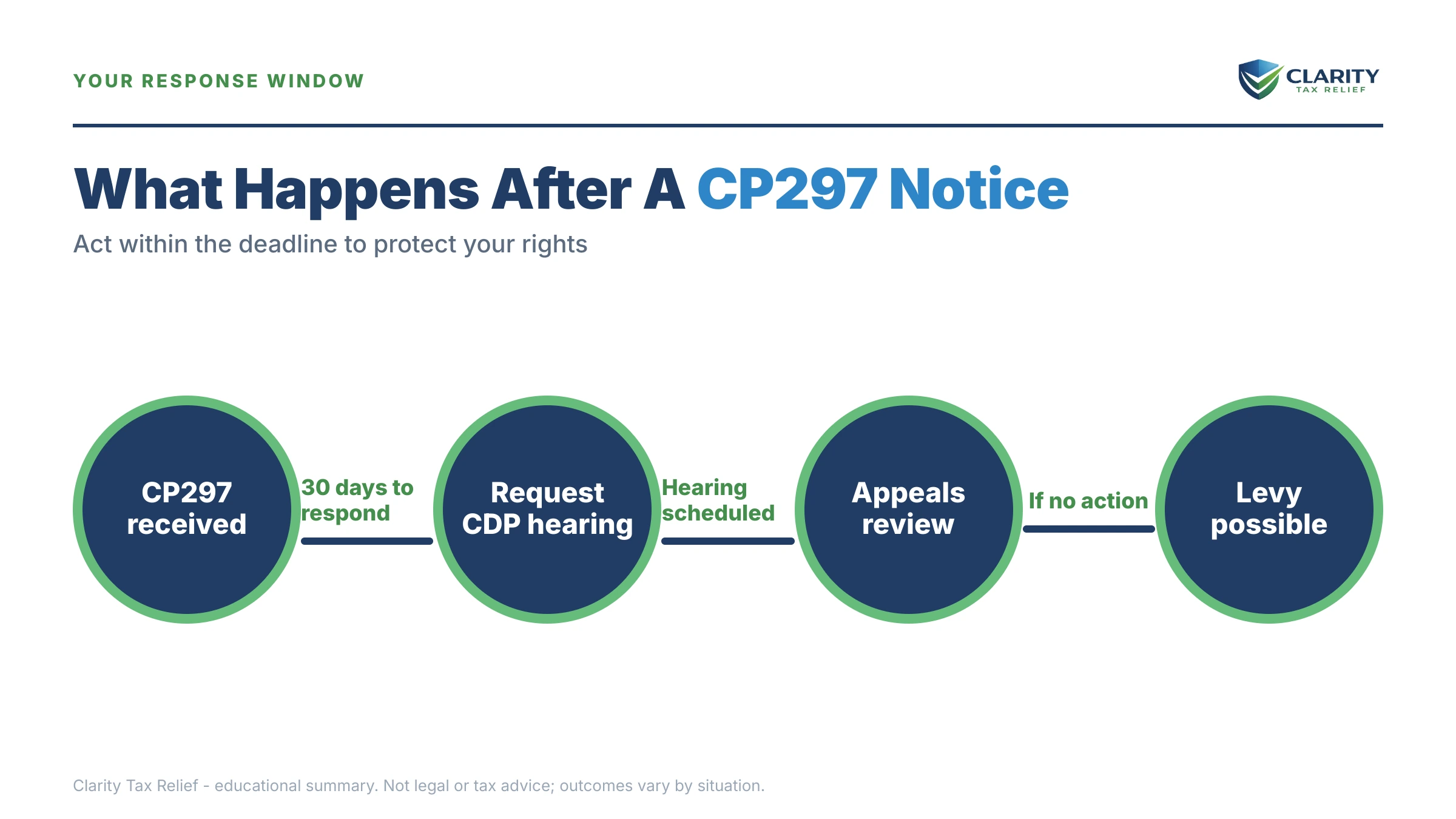

The 30-day CDP clock: what a CP297 lets you do

A timely Collection Due Process request is the only stage of IRS collection where you can get an independent Appeals review — with Tax Court backup — before money moves. You claim it by filing Form 12153, the CDP hearing request, within 30 days of the notice date. At the hearing you can dispute the amount (if you never had a prior chance to), ask for penalty relief, or propose a payment plan, hardship status, or offer instead of a levy.

Two honest trade-offs. First, a CDP appeal pauses the IRS's 10-year collection statute, so the debt stays collectible longer. Second, if you already agree with the balance and just need a payment plan, you can often set one up faster without a hearing. The table below shows what each window preserves — and what quietly expires if you wait.

| Window | Action available | What it preserves |

|---|---|---|

| Days 1–30 from notice date | Form 12153 — Collection Due Process hearing | Levy generally paused during review; Tax Court review of Appeals' decision |

| Day 31 to 1 year | Form 12153 — equivalent hearing | An Appeals hearing, but no Tax Court review, and levies aren't automatically paused |

| Any time | CAP appeal | Fast review of a specific levy or seizure action; no court review afterward |

| After a levy hits | Hardship release request | Release of a levy that prevents basic living or operating expenses — conditions apply |

What happens if you ignore a CP297

After the 30-day window on a CP297 closes, the IRS can levy bank accounts, accounts receivable, and other property without sending another warning. The sequence from there is automated and doesn't require a human to review your file first:

- Day 31 and beyond — levy authority is active. The IRS's systems can issue levies at any point; there is no second final notice.

- Bank levy — your bank freezes the balance and holds it for 21 days before sending it to the IRS. That hold is your last practical chance to negotiate a release.

- Receivables and payment processors — the IRS can order your customers or card processor to send your money to the Treasury instead of you, which chokes off business cash flow fast.

- Lien filing — a Notice of Federal Tax Lien (Letter 3172) can attach the government's claim to business and personal property, complicating credit and any sale.

- Personal assessment on payroll debt — for unpaid 941s, the IRS pursues the Trust Fund Recovery Penalty against owners and check-signers personally, proposed by Letter 1153 with a 60-day protest window. Once assessed, a wage levy against you is continuous until released — you can estimate what a paycheck levy would take with our IRS wage garnishment calculator.

One 2026 reality check: IRS staffing fell roughly 27% in 2025, so reaching a human takes longer — but levies are generated by automated systems that never stopped running. Understaffing delays your fix; it does not delay their enforcement.

Holding a CP297 right now?

Get it reviewed free before the 30-day hearing window closes. An experienced tax professional will confirm your exact deadline, whether Form 12153 makes sense for you, and which resolution fits the balance — no pressure, no obligation.

Your options for resolving the balance behind a CP297

Every resolution option is still on the table at the CP297 stage — the notice changes your deadline, not your eligibility. Which one fits depends on the size of the balance, whether it's a business or personal liability, and what your finances can honestly support:

| Option | Typical eligibility | Effect |

|---|---|---|

| Pay in full | Anyone; payment by the response date | Stops the notice sequence and further penalty accrual immediately |

| Business installment agreement | Payroll balances up to $25,000 can typically use an express agreement paid within 24 months by direct debit; larger balances require financials | Levy action generally stops while the agreement is in effect; interest and penalties continue |

| Individual installment agreement | Balances up to $50,000 (sole proprietors and personal liabilities) — up to 72 months, set up online | Same protection; direct debit lowers the setup fee and default risk |

| Currently Not Collectible | Financials show paying anything would prevent basic living or operating expenses | Collection pauses; debt and accruals remain, and the IRS reviews periodically |

| Offer in Compromise | $205 application fee; must show the offer equals the most the IRS could ever collect; the IRS accepted roughly 1 in 5 offers in FY2024 | Settles for less when accepted — rare for operating businesses with ongoing payroll |

| Penalty abatement | First-Time Abate with a clean prior 3 years; the new Automatic Exemption from Penalty (AEP) begins applying some relief automatically starting summer 2026 | Shrinks the balance; doesn't by itself stop the levy clock — pair it with an agreement |

A worked example: $13,600 behind a CP297

Say you and your spouse file a joint return and co-own a two-employee LLC that fell behind on payroll deposits during a slow winter. The CP297 arrives addressed to the business and shows $13,600 across two quarters of unpaid Form 941 taxes. This is a hypothetical, but the math is real:

- Express installment agreement: $13,600 ÷ 24 months ≈ $567 per month by direct debit. Interest and penalties keep accruing on the shrinking balance, so the total paid ends up somewhat higher — but levy action stops while the agreement holds.

- The trust-fund exposure: suppose roughly $8,200 of the $13,600 is withheld income tax plus the employees' share of FICA. That portion can be assessed personally — against either or both of you, depending on who controlled which bills got paid — and it follows you even if the LLC later closes. The remaining ~$5,400 (the employer's share and penalties) stays with the entity.

- The CDP angle: if you believe one of the two quarters was actually deposited, a Form 12153 filed inside the 30 days keeps that dispute in front of Appeals — with a levy pause and Tax Court review preserved — instead of arguing about it after your operating account is frozen.

- If the debt were personal instead: a $13,600 balance on your joint 1040 would fit a streamlined 72-month plan at roughly $189 per month ($13,600 ÷ 72), again plus accruals.

How to respond to a CP297, step by step

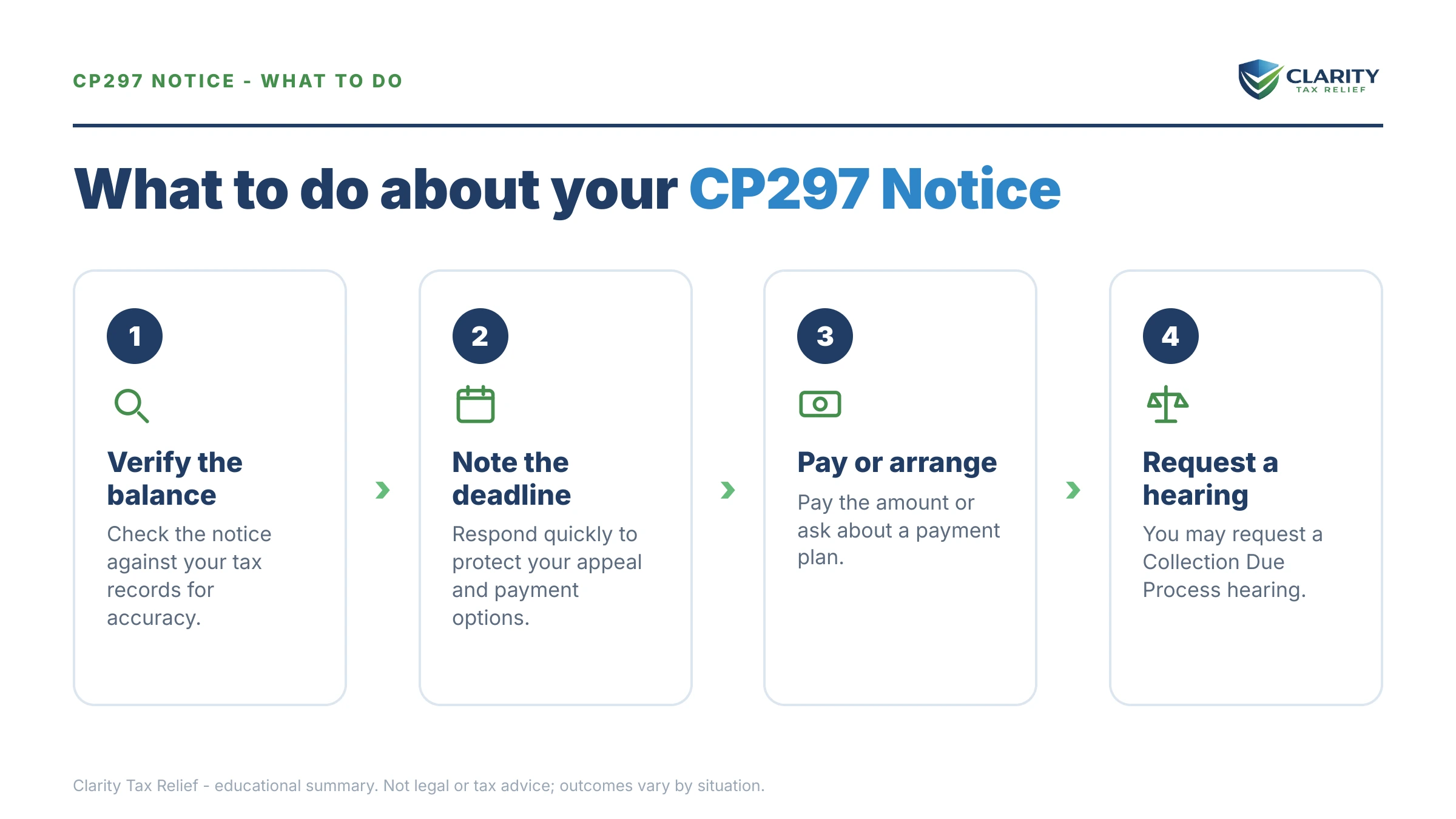

- Verify the notice against your records. Match the EIN or SSN, the tax periods, and the amount on the CP297 to your filed returns and your IRS account transcripts before you do anything else. The IRS's own explainer is at Understanding your CP297 notice.

- Calendar day 30. Count 30 days from the date printed at the top of the notice — that is your Collection Due Process deadline, not the day you opened the envelope.

- Decide whether to file Form 12153. File within the 30-day window if you dispute the balance or need a collection alternative reviewed by Appeals; a timely request generally pauses levy action. The official form and instructions are at IRS.gov's Form 12153 page.

- Get current on filings and deposits. File any missing returns and, for payroll debt, make the current quarter's federal tax deposits — the IRS won't approve an agreement while you're out of compliance.

- Lock in a resolution before the window closes. Set up a payment plan, request hardship status, or submit an offer — any approved arrangement takes levy action off the table while it's in effect. Payment and plan setup options live at IRS.gov/payments.

When you can handle a CP297 yourself

You likely don't need professional help if the balance is accurate, all your returns are filed, and the amount fits a plan you can set up directly — a personal balance under $50,000 you can pay monthly, or a business payroll balance under $25,000 you can clear within 24 months. In that case: confirm the numbers, set up the agreement before day 30, and keep every confirmation.

Experienced help changes outcomes in four situations: a levy is already in motion or your receivables are exposed; the IRS has started a Trust Fund Recovery Penalty investigation (a Letter 1153 or an interview request means personal liability is being built right now); you have multiple unfiled 941 quarters that must be sequenced before any agreement will stick; or you're disputing the underlying liability at a CDP hearing, where the record you build determines what a court can later review. Those aren't paperwork problems — they're strategy problems with 30-day fuses.

Terms on your CP297, decoded

- Levy — the actual seizure of money or property (a bank account, receivables, a paycheck); this is what the CP297 is warning about.

- Lien — a public legal claim against your property that secures the debt; it takes nothing by itself but clouds credit and sales.

- Collection Due Process (CDP) — your right to an independent IRS Appeals review before levy, requested on Form 12153 within 30 days, with Tax Court review preserved.

- Equivalent hearing — the late version of a CDP hearing, available up to one year out; you get Appeals, but no court backup and no automatic levy pause.

- Trust fund taxes — the payroll money withheld from employees' checks; the IRS treats it as employees' money you held in trust, which is why it can become personal debt.

- CSED — the Collection Statute Expiration Date, generally 10 years from assessment; appeals, offers, and bankruptcy pause it. If a levy has caused genuine hardship, the Taxpayer Advocate Service can also intervene.

CP297 questions, answered

Is a CP297 the same as an LT11 or CP90?

They carry the same legal weight — all three are final notices of intent to levy that start a 30-day Collection Due Process clock. The difference is who receives them: CP90 goes to individuals, LT11 comes from the IRS Automated Collection System, and CP297 is typically issued on business tax accounts. Your response rights under Form 12153 are identical for each.

How long after a CP297 can the IRS levy?

The IRS can levy any time after the 30-day window on your CP297 expires — no further warning is required. If a bank account is levied, the bank holds the funds for 21 days before sending them to the IRS, which is your last chance to negotiate a release. A wage levy, by contrast, is continuous until the IRS formally releases it.

Should I file Form 12153 after getting a CP297?

File it if you dispute the balance, want penalty relief considered, or need a payment alternative reviewed before levy action starts — a timely CDP request generally pauses levies while your hearing is pending. Be aware the appeal also pauses the IRS's 10-year collection clock, so it extends how long the debt stays collectible. If you agree with the balance and can set up a payment plan quickly, you may not need the hearing at all.

Can the IRS take my personal bank account over a business CP297?

It depends on how your business is structured. If you operate as a sole proprietor or a single-member LLC taxed on your personal return, the business tax debt is your personal debt and personal accounts are reachable. If the debt belongs to a corporation or multi-member LLC, the levy targets the entity's assets — but the trust-fund share of unpaid payroll taxes can be assessed against you personally through the Trust Fund Recovery Penalty.

Can I still get a payment plan after receiving a CP297?

Yes — an installment agreement remains available at this stage, and getting one in place generally stops levy action while you make the payments. You'll need to be current on all required filings and, for a business, current on federal tax deposits before the IRS will approve it. Smaller business balances can often be set up on an express agreement without a full financial disclosure package.

What happens if I missed the 30-day deadline on my CP297?

You lose the right to Tax Court review, but not every option. Within one year of the notice date you can still request an equivalent hearing using the same Form 12153, which gets your case in front of IRS Appeals — though levies are not automatically paused while it's pending. You can also set up a payment plan or hardship status at any time, and a CAP appeal can challenge a specific levy action quickly.

Does a CP297 mean the IRS has filed a tax lien?

Not automatically — a levy notice and a lien filing are separate actions. A CP297 warns that the IRS intends to seize assets; a Notice of Federal Tax Lien (Letter 3172) is a public filing that attaches the government's claim to what you own. In practice they often arrive at the same stage of collection, so check your notice and your IRS account to see whether a lien has already been filed.

Your next 24 hours

- Find the notice date printed at the top of your CP297, count 30 days forward, and write that date somewhere you'll see it — that is your Collection Due Process deadline.

- Gather your file: the notice itself, the returns for the tax periods it lists, proof of any payments or deposits you've made, and your last three months of bank statements.

- Get the notice reviewed free before the 30-day window closes — call (888) 825-7779 or use the 2-minute form, and an experienced tax professional will map your fastest path away from a levy.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.