IRS Notices

IRS CP3219N Notice: The 90-Day Letter for Non-Filers — Deadline, Options, and What to Do (2026)

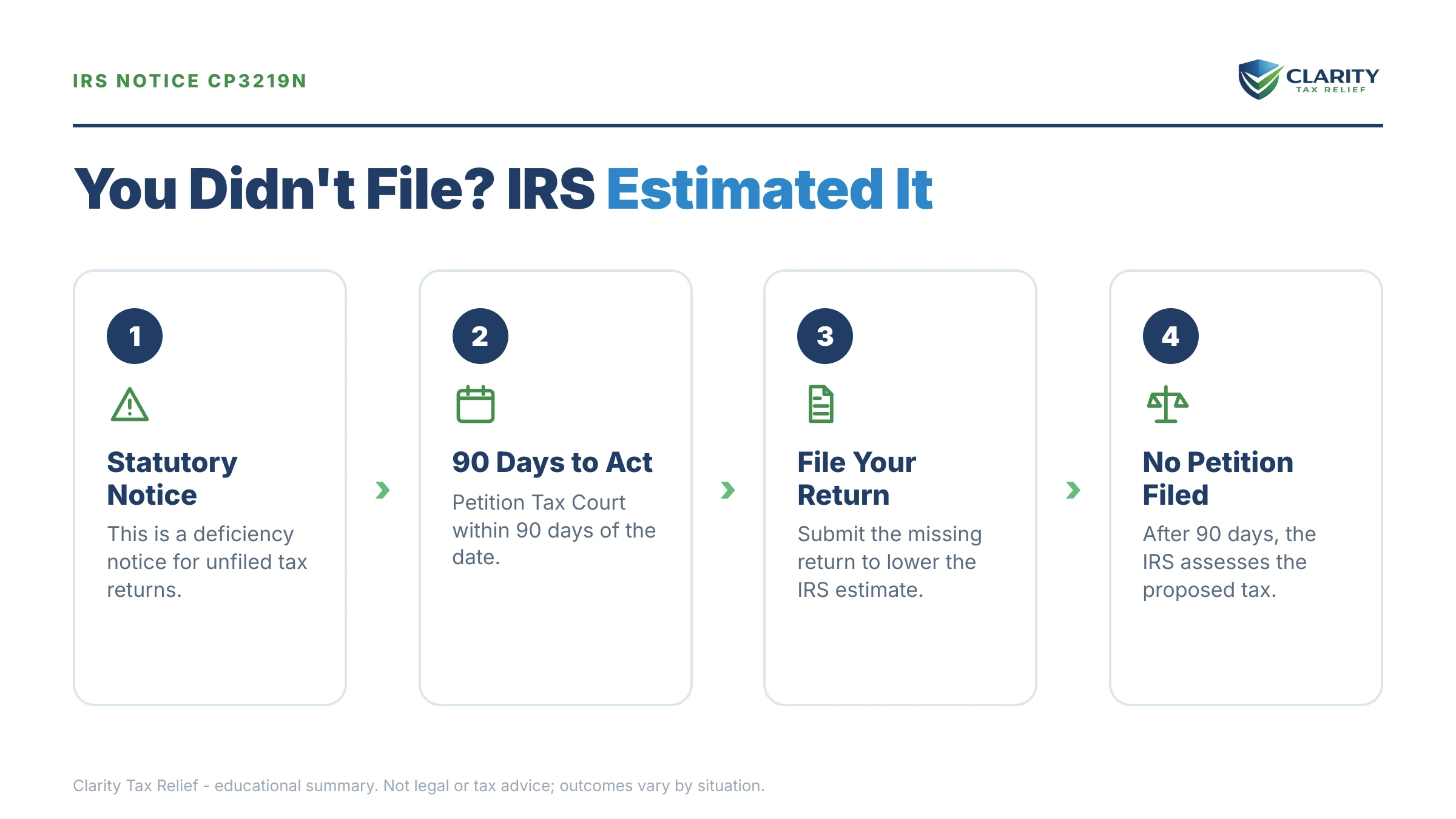

The short answer: a CP3219N notice is a statutory Notice of Deficiency the IRS sends when you didn't file a return, so it calculated your tax for you — usually far too high. You have 90 days from the date on the notice to file your actual return, agree to the amount, or petition the U.S. Tax Court. That deadline cannot be extended.

Maybe the year the divorce happened is the year the tax return never got done — and because you moved afterward, the IRS's earlier letters went to an address you don't live at anymore. Now a certified envelope has caught up with you, and it says the IRS has already decided what you owe. That number is almost never your real number, and the next 90 days are when you get to prove it.

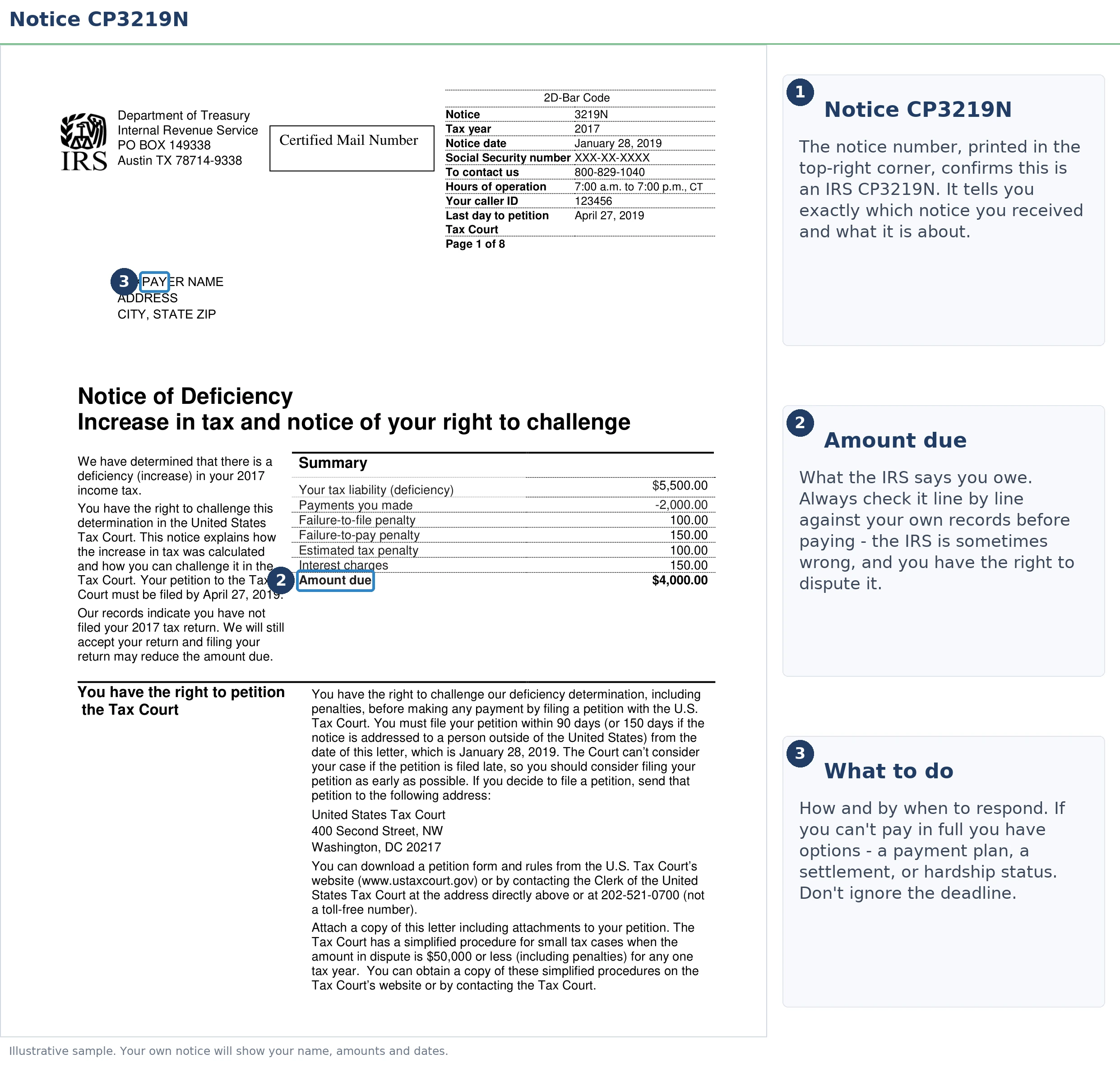

A CP3219N is different from every other IRS bill in one crucial way: the amount on it isn't based on a return you filed. It's based on a return the IRS built for you, using the harshest assumptions the law allows. The image below shows exactly what a CP3219N looks like and where to find the two things that matter most — the proposed deficiency and the last day to petition the Tax Court.

⏱ Your deadline: you have 90 days from the date printed on the CP3219N to respond — file your real return, sign the agreement form, or petition the U.S. Tax Court (150 days if the notice was addressed to you outside the United States). This window is set by statute. The IRS cannot extend it, and neither can you. The exact "last day to petition" date is printed on your notice — that date controls, not your mail delivery date.

Why you got a CP3219N notice

A CP3219N means the IRS found income reported under your Social Security number for a year with no tax return on file — so it wrote the return for you. Employers, banks, brokerages, and retirement plans all send copies of W-2s and 1099s to the IRS. When those documents exist but a return doesn't, the IRS eventually prepares a substitute for return (SFR) and proposes to assess tax on it.

The CP3219N is rarely the first letter in this chain. It typically follows a CP59 ("we have no record of your return"), a CP518 final filing reminder, and a CP2566 laying out the proposed SFR numbers. If you moved — common after a divorce — those earlier notices may have gone to your old address. Legally, that doesn't matter: the IRS only has to mail the notice to your last known address, not prove you received it. The CP3219N you're holding is valid even if it's the first letter you've actually seen. (For the general anatomy of IRS mail, see why did I get a letter from the IRS.)

One reassurance up front: a CP3219N is not a criminal matter and not an accusation of fraud. It's the automated end of the non-filer pipeline — a proposal, not yet an assessment. Nothing can be levied at this stage. Your job is to answer it before the proposal hardens into a legal debt.

CP3219N vs. CP3219A: which 90-day letter do you have?

The letter after the number changes everything about how you respond. A CP3219A notice of deficiency comes after you filed a return and the IRS disagrees with it — usually following a CP2000 income mismatch. A CP3219N ("N" for non-filer) comes after you filed nothing, so there's no return to disagree with; the IRS invented the numbers from scratch.

Both letters start the identical 90-day Tax Court clock, but the winning move differs. With a CP3219A, you're arguing about specific line items. With a CP3219N, you usually don't need to argue at all — you need to file the real return, which replaces the IRS's assumptions wholesale. That's a much stronger position than most recipients realize.

Why the amount on a CP3219N is almost always too high

A substitute for return is built to protect the government, not to compute your correct tax. When the IRS prepares one, it systematically uses the worst-case assumption at every fork:

- Filing status: single, or married filing separately if you were still legally married on December 31 of that year — never head of household, never joint. For a divorced parent, losing head-of-household status alone inflates the tax meaningfully.

- Deductions: the standard deduction only. No itemizing, no dependents, no child tax credit, no education credits, no earned income credit.

- Investment sales: every 1099-B is counted at full gross proceeds with zero cost basis. Sell $60,000 of stock you bought for $55,000, and the SFR taxes $60,000 of "gain," not your real $5,000.

- Retirement money: distributions are taxed in full, and the 10% early-distribution addition is applied even when an exception (like a distribution paid to an ex-spouse under a QDRO) would eliminate it.

- Self-employment: 1099-NEC income is counted gross, with zero business expenses, plus self-employment tax on the whole amount.

On top of that inflated tax, the IRS stacks the failure-to-file penalty — 5% per month, capping at 25% of the tax — plus the 0.5%-per-month failure-to-pay penalty and compounding interest. Because the tax itself is overstated, every percentage-based penalty is overstated too. You can estimate how much of a proposed balance is penalties and interest with our IRS Penalty & Interest Calculator.

One more scenario worth naming: if the wage and income file includes a 1099 that isn't yours — an identity thief working under your SSN, or an ex's account still tied to your number — the deficiency is disputable on its face. That's a situation where the Tax Court petition, not just a late return, becomes the right tool.

What happens if you ignore a CP3219N

If day 90 passes with no response, the IRS assesses the full proposed amount and the balance becomes a legally collectible debt. From there the collection machine runs on its own — and in 2026, with IRS staffing down roughly 27%, the humans are harder to reach but the automated notices and levies never paused. The sequence looks like this:

- Day 91 — assessment. The proposed deficiency, penalties, and interest post to your account. Your Tax Court window is gone, and the 10-year collection statute starts running.

- CP14 — the first bill. Typically about 21 days to pay before the reminder cycle begins.

- CP501 / CP503 — reminders. Still just bills, but interest compounds monthly and a federal tax lien becomes increasingly likely.

- CP504 — intent to levy. The IRS can seize your state tax refund at this stage.

- LT11 / Letter 1058 — final notice. A 30-day clock to a wage garnishment or bank levy, with Collection Due Process rights you must actively invoke.

Ignoring a CP3219N also costs you things no later notice mentions. If the assessed balance exceeds $66,000 (the 2026 threshold) and goes unaddressed, it can be certified as seriously delinquent debt and block your passport. An SFR assessment generally doesn't count as a filed return for bankruptcy-discharge purposes, so the debt becomes harder to shed later. And if your real return would have shown a refund, the clock to claim it keeps running while you wait. The table below shows where the CP3219N sits in the full non-filer sequence.

| Stage | What it means | Your window |

|---|---|---|

| CP59 | First "no return on file" notice — a request, no proposed tax yet | File as soon as possible; no fixed clock |

| CP516 / CP518 | Second and final filing reminders | Last easy exits before the SFR machinery starts |

| CP2566 | Proposed SFR calculation — the draft of your CP3219N numbers | 30 days to respond, per the date on the notice |

| CP3219N (you are here) | Statutory Notice of Deficiency — last stop before assessment | 90 days, non-extendable (150 if addressed abroad) |

| Assessment | Proposed amount becomes a legal debt; Tax Court right expires | Day 91 onward |

| CP14 → CP504 → LT11 | Collection sequence: bill → intent to levy → final notice | Roughly 21 days on the CP14; 30 days on the LT11 before levy |

Holding a CP3219N with the clock already running?

The 90-day petition deadline on your notice is one of the few in the tax code that cannot be extended — and the right response usually cuts the proposed amount dramatically. Get your CP3219N reviewed free before the window narrows: an experienced tax professional will read the notice, pull your income records, and map the fastest path.

Your options: four ways to answer a CP3219N

Every CP3219N response falls into one of four lanes, and choosing the right one depends on whether the IRS's income data is right, whether its math is right, and how much of the 90 days you have left.

| Response | What happens | Best when |

|---|---|---|

| File your actual return | Your real filing status, dependents, basis, and deductions replace the SFR math; the IRS recomputes the balance | The income is yours but the IRS's assumptions inflate the tax — the majority of cases |

| Sign Form 5564 (agree) | You waive the Tax Court right; the IRS assesses immediately and you move straight to payment options | The proposed numbers are genuinely correct and you want to stop the escalation and start resolving |

| Petition the U.S. Tax Court | Assessment is blocked while the case is pending; most cases settle with IRS Appeals | You dispute the income itself (identity theft, a 1099 that isn't yours) or the deadline is too close to rely on return processing |

| Do nothing | Assessment of the full inflated amount on day 91, then the collection sequence | Never a strategy — even if you agree, signing the waiver gets you to a resolution faster and cleaner |

Filing the return is the most powerful option — but it does not stop the 90-day clock. Send the completed return with the response page from your notice to the address the notice specifies (not through your normal e-file software), by certified mail with tracking. Here's the trap experienced practitioners plan around: IRS processing in 2026 is slow, and your return may not be worked before day 90. If you're inside the final three to four weeks, the safe play is both — submit the return and file a protective Tax Court petition so the deadline can't expire on you while the return sits in a queue.

If the CP3219N covers a year where your real return shows a refund, know this: refunds are only payable within 3 years of the original due date. The IRS can propose tax on an old year forever; you can only collect a refund from it briefly. That asymmetry is a reason to file now, not later.

And if you have more than one unfiled year, expect more than one notice — each CP3219N carries its own independent 90-day deadline. Treat them separately and track each date. Multiple SFR years are also where the multi-year catch-up strategy matters, because the order you file in can change the total penalties.

A worked example: the $92,700 CP3219N after a divorce

Say your divorce finalized in 2023, that year's return never got filed, and a CP3219N arrives proposing $92,700 in tax, penalties, and interest. The IRS's wage and income file for the year shows three items: $88,000 in W-2 wages, a $46,000 401(k) distribution paid to you under the divorce's QDRO, and $61,000 in gross proceeds from brokerage sales made to split the accounts. This is a hypothetical, but the mechanics are exactly how SFRs work.

The SFR's math: you're treated as a single filer with only the standard deduction and no dependents. The entire $61,000 of stock proceeds is taxed as gain because the IRS has no cost-basis information. The $46,000 retirement distribution is taxed in full plus the 10% early-distribution addition — roughly $4,600 — because the SFR doesn't know about the QDRO exception. Then the failure-to-file penalty (capped at 25% of the tax), the failure-to-pay penalty, and interest are stacked on the inflated total. Result: $92,700 proposed.

The real return tells a different story. You had two kids and qualify for head of household. The stock you sold for $61,000 had a basis of $54,500 — the real capital gain is $6,500, not $61,000. The QDRO exception eliminates the $4,600 early-distribution addition entirely. Child tax credits apply. Recomputed, the tax plus correspondingly reduced penalties and interest lands at roughly $21,000 — meaning filing the actual return removes on the order of $71,700 from the proposed bill. No negotiation, no settlement program, no hardship application. Just the correct return, submitted inside the 90 days.

A roughly $21,000 remaining balance then fits a streamlined installment agreement — about $300 per month over 72 months at minimum, while interest continues to accrue — or a 180-day short-term plan with no setup fee if you can pull the money together. Which brings us to the step-by-step.

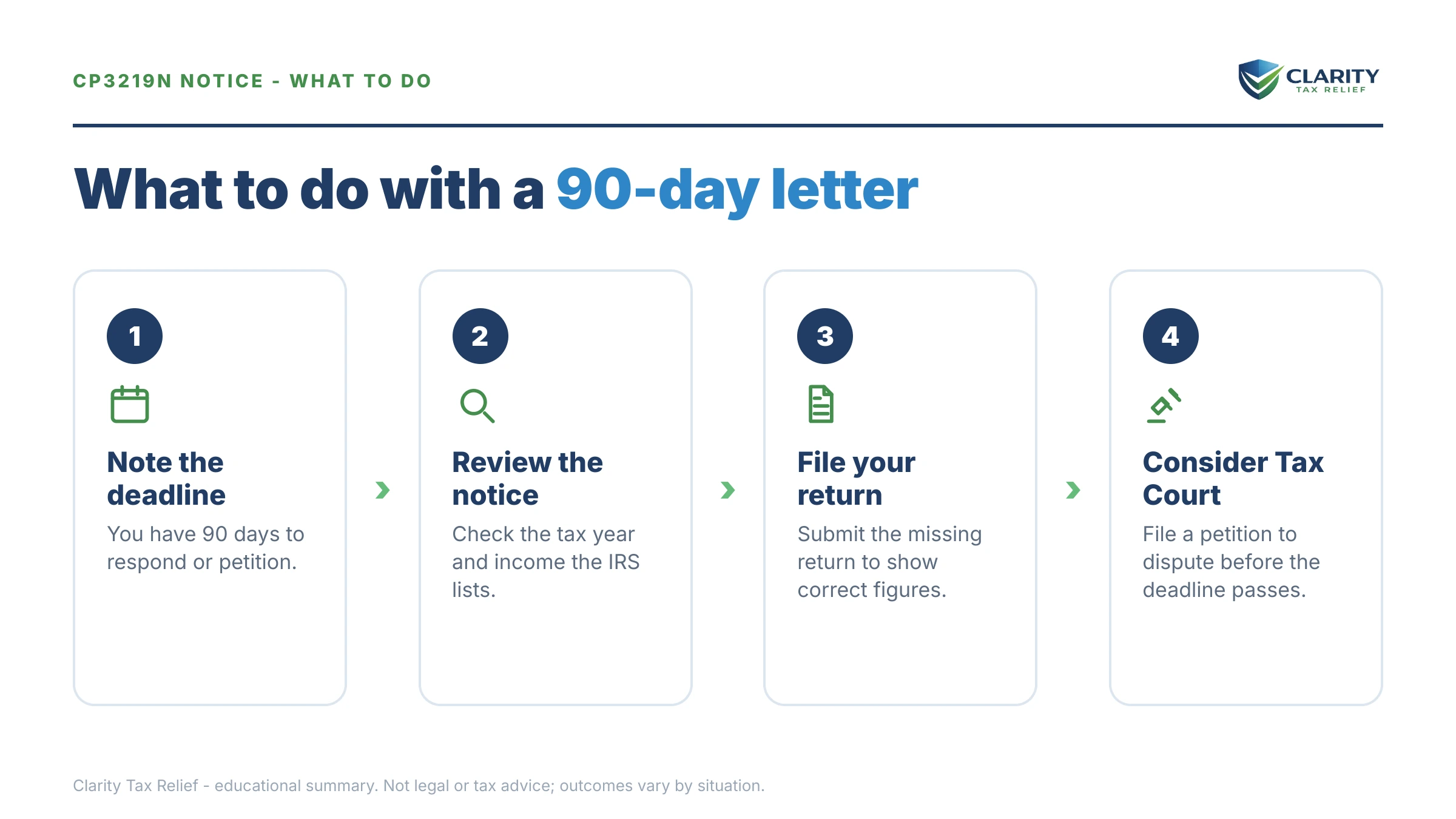

How to respond to a CP3219N, step by step

- Find your petition deadline. Locate the "last day to file a petition with the United States Tax Court" date printed on page one of your CP3219N and write it down — every other decision hangs on that date.

- Pull your wage and income transcripts. Download the wage and income transcript for the notice year from your IRS online account so you can see exactly which W-2s and 1099s the IRS counted — and spot anything that isn't yours.

- Prepare your actual return. Build the real Form 1040 for that year with your correct filing status, dependents, cost basis, deductions, and withholding — this is what replaces the IRS's inflated math.

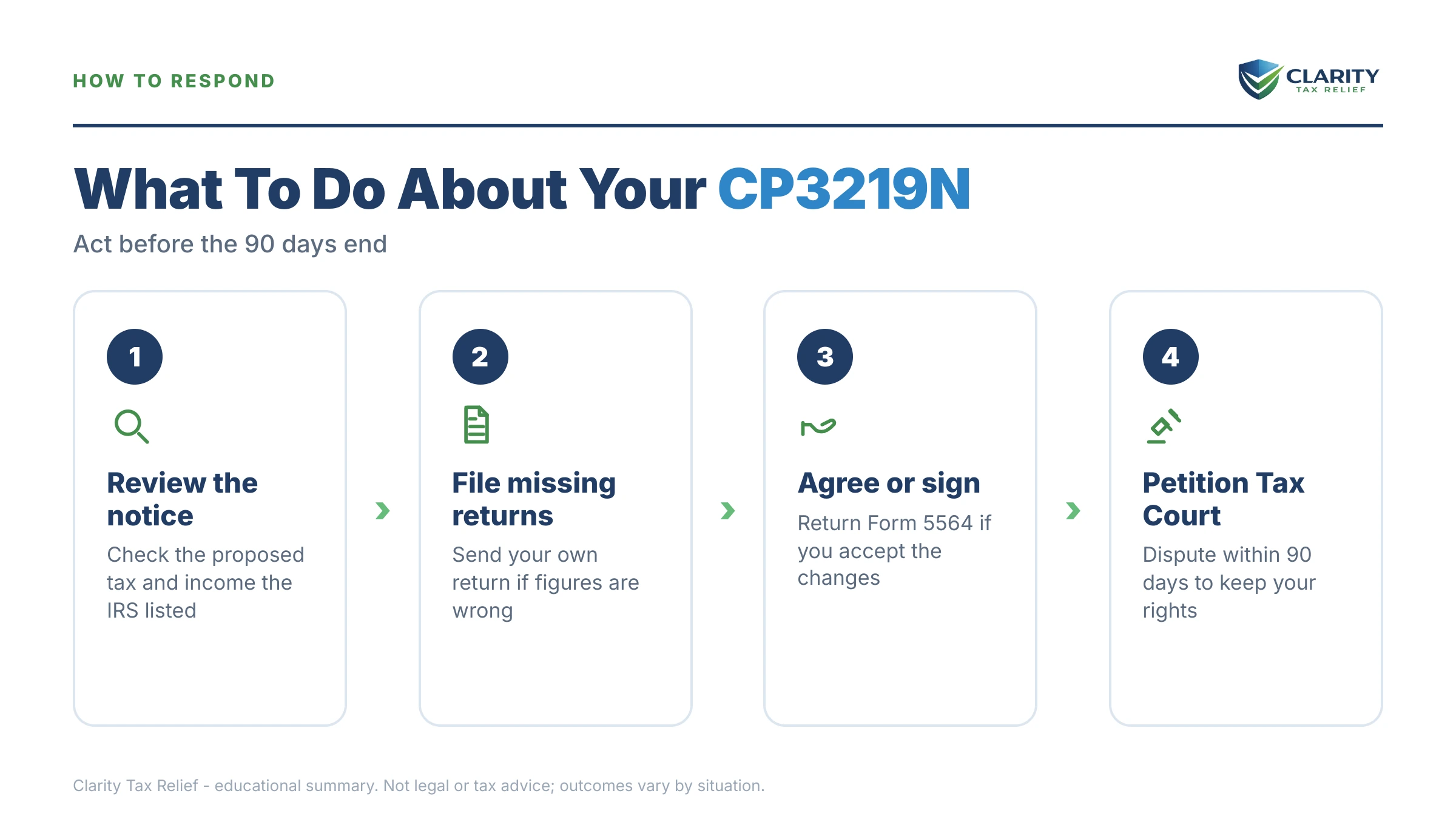

- Choose your response lane. File the return if the year just needs to be done right, sign Form 5564 if the IRS's numbers are actually correct, or petition the Tax Court if you dispute the income itself or the deadline is close.

- Send everything before day 90. Mail your return with the notice's response page by certified mail, and if you're petitioning, file with the Tax Court on or before the deadline date — the window cannot be extended.

- Arrange payment for what remains. Once the corrected balance is set, put a payment plan, hardship status, or settlement review in place so the account never reaches the levy stage.

If you still owe after filing your real return

Filing the correct return fixes the math; it doesn't make a genuine balance disappear. The good news is that the resolution options key off the corrected amount, which is usually a fraction of the CP3219N figure. Here's the realistic landscape by balance:

| Corrected balance | Realistic options | What to know |

|---|---|---|

| Under $10,000 | 180-day short-term plan ($0 setup) or a guaranteed installment agreement | No financial disclosure needed; interest and penalties keep accruing until paid |

| $10,000 – $25,000 | Streamlined installment agreement, set up online | Up to 72 months; no Form 433 financials required |

| $25,001 – $50,000 | Streamlined agreement with direct debit | Direct debit is generally required at the top of this band; still up to 72 months online |

| Over $50,000 | Non-streamlined agreement with financial disclosure, or pay down below $50,000 first | Expect Form 433 financials and closer scrutiny; a lien becomes more likely |

| Genuinely can't pay | Currently Not Collectible status or an Offer in Compromise review | Both are means-tested on your income, expenses, and assets — the IRS accepted roughly 1 in 5 offers in FY2024, so eligibility math comes first |

Penalty relief deserves its own look on any SFR year. If your compliance history was clean for the three years before the notice year, first-time abatement may remove the failure-to-file penalty — and starting summer 2026, the IRS's new Automatic Exemption from Penalty (AEP) applies some of this relief automatically, with no request needed. A divorce, serious illness, or other disruption during the filing year can also support reasonable-cause relief. On a five-figure balance, penalty relief alone can be worth thousands.

Petitioning the U.S. Tax Court: the short version

A Tax Court petition is the only response that legally freezes assessment while your dispute is heard. The filing fee is $60, the court can waive it for financial hardship, and you can file electronically through the court's DAWSON system at ustaxcourt.gov. Disputes of $50,000 or less per tax year qualify for simplified "small tax case" procedures built for people representing themselves.

Filing a petition doesn't mean a trial. In practice, most CP3219N petitions get routed to IRS Appeals, where your late-filed return becomes the settlement document and the case resolves on the corrected numbers. Think of the petition less as litigation and more as a deadline insurance policy that forces a human review. For the full mechanics — what goes in the petition, timing rules, what happens after docketing — see our guide to the 90-day letter and Tax Court petition.

Treat the deadline as absolute. Courts have repeatedly refused to hear deficiency petitions filed even one day late, and the timely-mailing rule only helps if the postmark is on or before the date printed on your notice.

What if you already missed the 90 days?

Missing the deadline closes the Tax Court door, but it does not lock in the SFR numbers forever. The main tool is audit reconsideration: you file the actual return after assessment and ask the IRS to adjust the account to the correct figures. The IRS grants these routinely on SFR years because the substitute numbers are so obviously provisional — but there's no deadline protection, so collection notices keep coming while it's reviewed. An Offer in Compromise based on doubt as to liability, or paying and filing a refund claim, are the backup routes.

The practical difference: before day 90, you control the timeline. After day 90, the IRS does, and you may be negotiating a corrected balance with a CP504 or levy notice already in the mail. If you're past the deadline, the move is the same — build the real return now — just with more urgency and, usually, a request to hold collection while reconsideration is pending.

When you can handle a CP3219N yourself

You likely don't need professional help if the notice year is simple: one W-2, income you recognize, and a return you can prepare accurately with time to spare. File the real return with the response page, confirm the recomputed balance, and set up a payment plan online if one is needed. If the IRS's numbers are actually right and the balance is small, signing Form 5564 and paying is a perfectly good outcome. If you're missing documents, our guide to filing back taxes without records covers reconstructing the year from transcripts.

Experienced help changes the outcome in specific situations: multiple unfiled years each running its own clock, a six-figure proposed deficiency, brokerage or crypto sales where basis reconstruction drives the whole number, self-employment income needing expense substantiation, income on the transcript that isn't yours, a divorce-year return where filing status and dependency are contested with an ex — or fewer than about 30 days left on the notice, where a protective petition needs to be drafted and filed correctly the first time. In those cases the cost of getting the response wrong is measured in tens of thousands, not hundreds.

If your CP3219N involves multiple years, disputed income, or an amount anywhere near six figures, have an experienced tax professional map the sequence before day 90 — start with a free case review or call (888) 825-7779.

Terms on your notice, decoded

- Statutory Notice of Deficiency — the formal legal proposal of tax you owe; it's what opens your one pre-payment path to court.

- Deficiency — the gap between the tax the IRS computed and the tax shown on a return (for a non-filer, that's the whole amount, since no return exists).

- Substitute for return (SFR) — the return the IRS prepared for you from third-party documents, using single/MFS status, the standard deduction, and no credits.

- Form 5564 — the waiver enclosed with your notice; signing it means you agree with the deficiency and let the IRS assess immediately.

- Last known address — the address on your most recent return or official update; mailing there makes the notice legally effective even if you never received it.

- Assessment — the moment the proposed amount posts as a legal debt; it also starts the 10-year collection statute (CSED), which can be paused by appeals, offers, and bankruptcy.

CP3219N questions, answered

What is a CP3219N notice from the IRS?

A CP3219N is a statutory Notice of Deficiency the IRS sends when its records show you earned income but never filed a return for that year. The IRS calculated the tax itself from W-2s and 1099s and is proposing to assess it. You have 90 days from the date on the notice to file your actual return, agree to the amount, or petition the U.S. Tax Court.

What is the difference between a CP3219A and a CP3219N?

A CP3219A follows a return you filed — it usually comes after a CP2000 when reported income didn't match your return. A CP3219N means you never filed at all, so the IRS built the numbers itself. Both start the same 90-day Tax Court clock, but with a CP3219N the most powerful response is usually filing your real return, which replaces the IRS's inflated figures.

Can I get an extension on the 90-day CP3219N deadline?

No. The 90-day window (150 days if the notice was addressed to you outside the United States) is set by statute, and the IRS has no authority to extend it. Filing your actual return during the window does not pause the clock either — if the deadline is near and you dispute the numbers, a Tax Court petition is the only thing that preserves your rights.

Should I just file my real tax return after getting a CP3219N?

For most people, yes — filing the actual return is the fastest way to replace the IRS's single-filer, zero-deduction math with your real filing status, dependents, and cost basis. Send it with the response form from your notice, not through normal e-file channels. But watch the calendar: the IRS may not process your return before day 90, so if the deadline is close, protect yourself with a petition too.

What happens if I ignore a CP3219N?

On day 91 the IRS assesses the full proposed amount, and the collection sequence begins: a CP14 bill, reminder notices, a CP504, then a final notice of intent to levy. You permanently lose the right to contest the amount in Tax Court before paying, the 10-year collection statute starts running, and a balance over $66,000 can trigger passport certification.

How much does it cost to petition the U.S. Tax Court?

The filing fee is $60, and the court can waive it if you can't afford it. You can file electronically through the court's DAWSON system, and disputes of $50,000 or less per year qualify for simplified small-case procedures designed for people without lawyers. Most deficiency cases settle with IRS Appeals before anyone sees a courtroom.

Why is the amount on my CP3219N so high?

Because a substitute-for-return calculation uses the worst possible assumptions: single or married-filing-separately status, only the standard deduction, no dependents or credits, no business expenses, and stock or crypto sales counted at full gross proceeds with zero cost basis. Then failure-to-file and failure-to-pay penalties and interest are stacked on top. Filing your real return corrects every one of those assumptions.

Will I get a refund if my real return shows one?

Only if you file within 3 years of the return's original due date. After that, the refund statute expires and the money is forfeited — even though the IRS can still assess and collect a balance for that same year. If your CP3219N year is approaching the 3-year mark and withholding may cover the tax, file immediately.

I missed the 90 days on my CP3219N — is it too late?

You've lost the Tax Court window, but not every path. You can still file your actual return and ask the IRS to adjust the assessment through audit reconsideration, pursue an Offer in Compromise based on doubt as to liability, or pay and file a refund claim. Collection continues while you do any of these, so move quickly.

Your next 24 hours

- Find the "last day to file a petition with the United States Tax Court" date on page one of your CP3219N and write it somewhere you'll see it daily. Every option you have runs through that date.

- Gather what the real return needs: your divorce decree or custody agreement if filing status or dependents changed that year, W-2s and 1099s (or your wage and income transcripts), brokerage statements showing what you paid for anything you sold, and proof of withholding.

- Get your CP3219N reviewed free before the 90-day window narrows — use the 2-minute form or call (888) 825-7779. An experienced tax professional will tell you in one conversation whether filing, agreeing, or petitioning is your fastest exit.

The IRS's own explainer for this notice is at Understanding your CP3219N notice, and once a corrected balance is set, every official payment route is at IRS.gov/payments.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.