IRS Notices

CP49 Refund Applied to Back Taxes: What It Means and What to Do in 2026

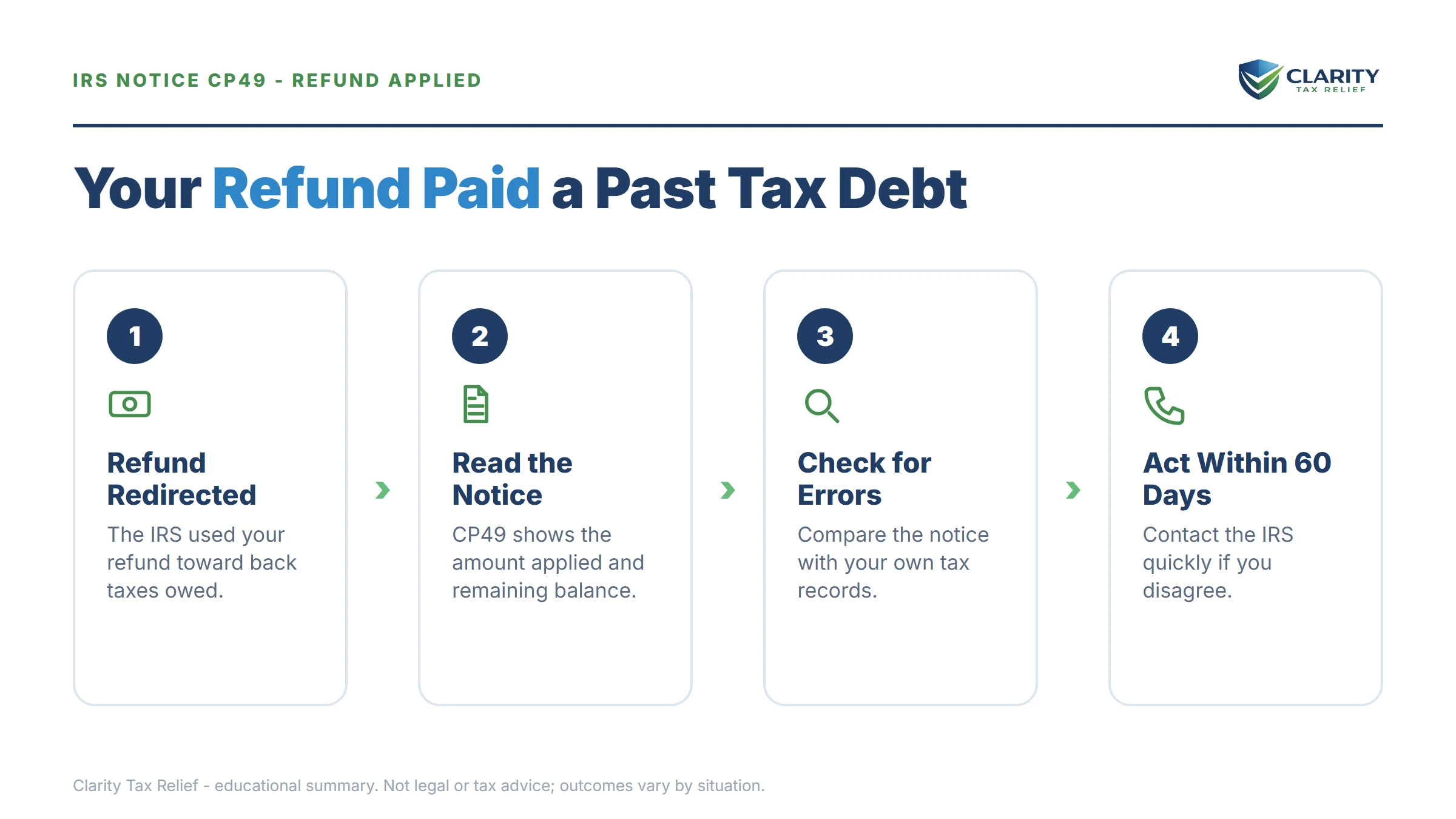

The short answer: a CP49 refund applied notice means the IRS kept all or part of your tax refund and used it to pay a federal tax balance you owe from a prior year. It is not a new bill or an audit — it's a receipt showing which year took the money and what balance, if any, remains.

You checked your deposit account for days, and instead of the refund you'd already assigned to rent and the credit card, a CP49 arrived saying the money went to a tax year you'd half forgotten. That sinking feeling is real — but so is the upside: your old debt just got smaller, and this letter hands you everything you need to finish the job on your terms.

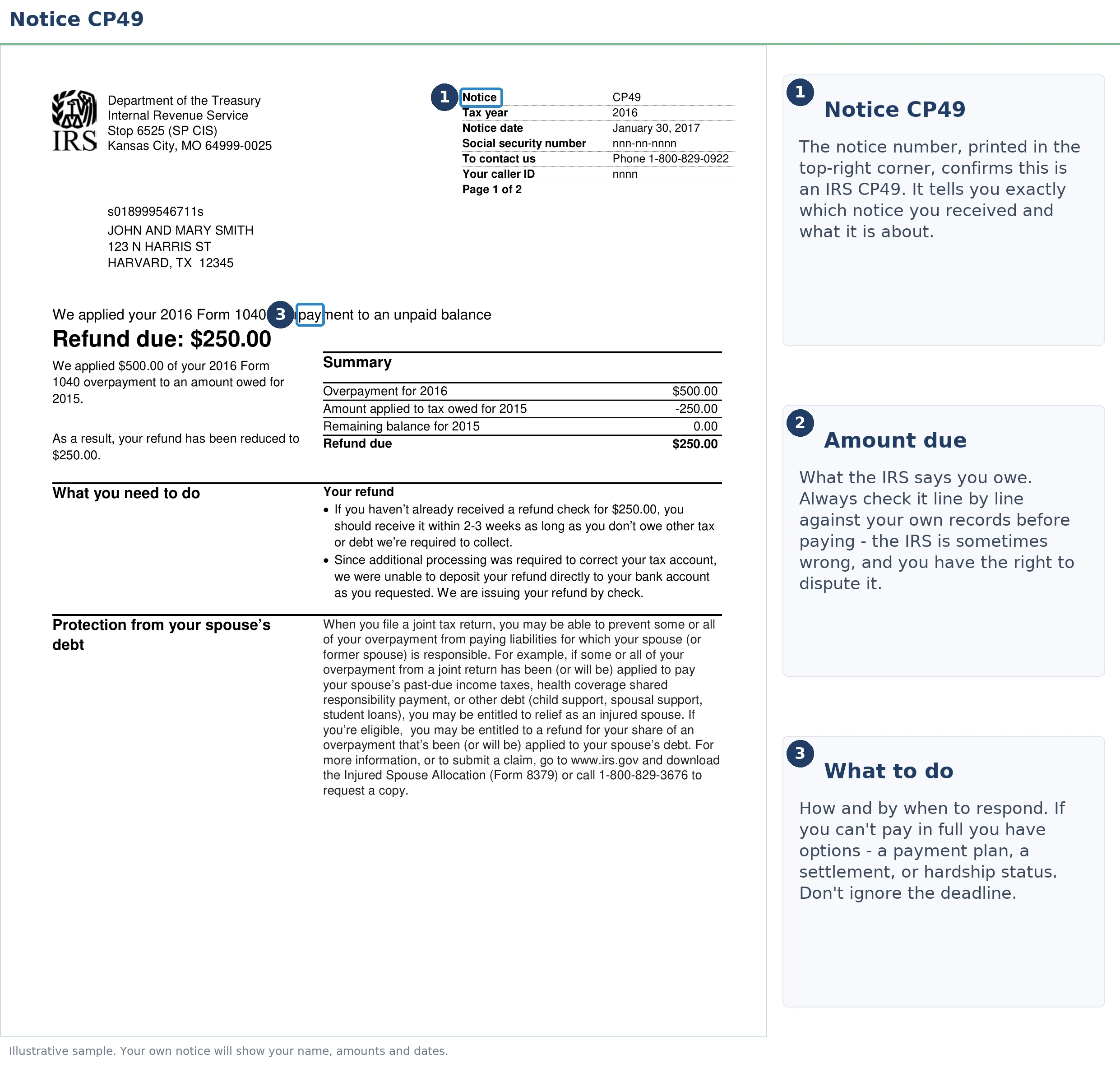

A CP49 asks nothing of you by a printed deadline, because the offset has already happened. Your job now is to verify the money landed on the right year, understand what's left, and stop the leftover balance from eating next year's refund too. The image below shows exactly what a CP49 looks like and where to find the three figures that drive every decision on this page.

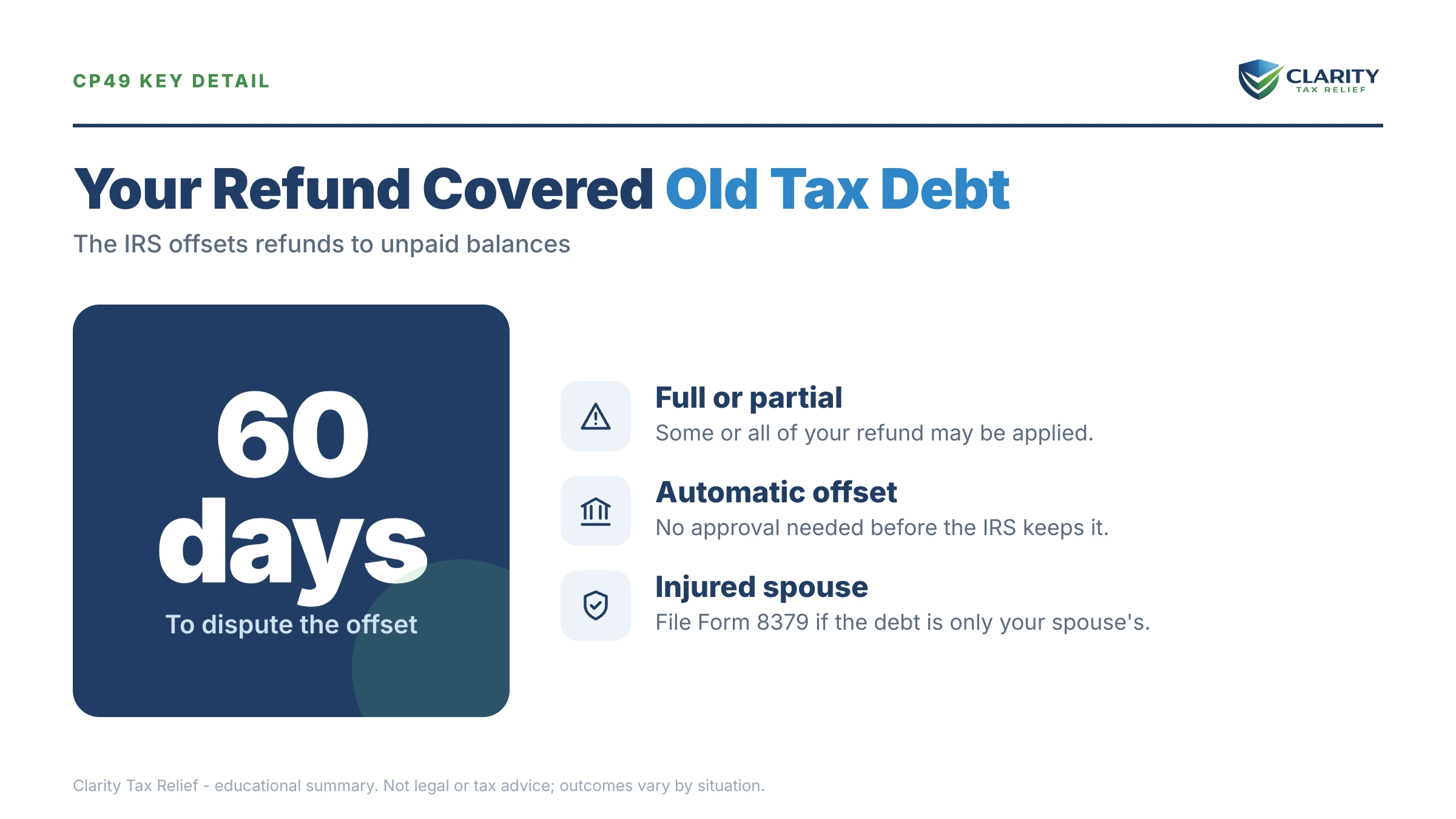

⏱ The real clock: a CP49 has no response deadline — the offset already posted. But the failure-to-pay penalty adds 0.5% of the remaining balance every month and interest compounds daily until what's left is resolved. If you believe the offset is wrong, call the number on the notice as soon as possible.

Why you got a CP49 refund applied notice

The IRS sends a CP49 when it applies some or all of your current-year refund to a federal tax balance from another year. Under IRC §6402(a), the IRS is allowed to keep an overpayment and apply it to your outstanding federal tax before refunding anything to you — and its computers do this automatically, before a refund ever leaves the building.

Three details on the notice tell the whole story: the tax year your refund came from, the year (or years) the money was applied to, and either the remaining refund being sent to you or the balance you still owe. The offset happens even if you're on an active payment plan — your refund is taken on top of your monthly payments, not instead of them, as we cover in will the IRS take my refund on a payment plan.

What a CP49 is not: an audit, a levy notice, or a new assessment. Nothing on it changes what you owed — it changes how much of it is already paid. If you're not sure why the IRS thinks you owed anything in the first place, start with why did I get a letter from the IRS and pull your account records before reacting to this one notice in isolation.

CP49 vs. the lookalike notices: which one do you actually have?

The IRS uses at least six different notices and codes when a refund shrinks or disappears, and each has a different fix. Match yours before doing anything else:

| Notice or code | What it means | What to do |

|---|---|---|

| CP49 | Your refund was applied to your own federal tax debt from another year | Verify the balance, then resolve what's left (this guide) |

| CP42 / CP39 | Your refund (or overpayment) went to your spouse's tax debt | Consider injured spouse relief to recover your share |

| CP44 | Refund delayed while the IRS decides whether to apply it to other tax | Wait or respond — the offset hasn't happened yet |

| Code 826 | Transcript entry showing the same offset a CP49 announces | Confirm date, amount, and receiving year |

| Code 898 | Refund taken for a non-IRS debt (child support, student loans, state tax) through the Treasury Offset Program | Dispute with the agency that got the money, not the IRS |

| CP12 | The IRS corrected a math error and changed your refund amount | Agree, or dispute the correction within the notice window |

| CP05 | Your refund is being held for review — not applied anywhere yet | Usually wait; respond only if the IRS asks for documents |

This distinction matters most for joint filers: if the debt that swallowed your refund belongs only to your spouse — from before your marriage, or from their separate filing — Form 8379 injured spouse can recover your portion of the refund. A CP49 for your own debt has no equivalent claw-back.

The three numbers to find on your CP49

Every decision you make next depends on three figures printed on the notice, and the image below shows you what a CP49 looks like and where to look. Find:

- The amount applied — and to which year. If the money landed on a year you already paid, or a year that isn't yours, that's a dispute, not a debt.

- Any remaining refund coming to you. If your refund was larger than the old balance, the leftover is still on its way — the CP49 tells you how much.

- The remaining balance you still owe. If the refund didn't cover everything, this number is what keeps accruing penalties and interest starting today.

Also note the notice date and the phone number in the top corner — you'll need both if anything doesn't match your records.

Say you owe $8,900: what a CP49 actually does to the math

A worked example makes the stakes concrete. Say you owe $8,900 from your 2023 return — a year your withholding fell short — and you rent, with no home equity or savings cushion. Your 2025 return shows a $3,150 refund. Instead of a deposit, you get a CP49: $3,150 applied to 2023, refund to you $0, remaining balance $5,750.

Here's what that $5,750 does if you leave it alone. The failure-to-pay penalty runs 0.5% per month — about $29 a month at this balance — and interest compounds daily on top. Do nothing for a year and the penalty alone adds roughly $345 before interest, and next spring's refund gets swept automatically too. You can estimate how fast your own balance grows with our IRS Penalty & Interest Calculator.

Now the fix: $5,750 is well inside the limits for an online payment plan. Simple division — $5,750 ÷ 48 months ≈ $120 per month before accruals — clears it in about four years; pay more and both the timeline and the interest shrink. For a renter, this matters doubly: the IRS can't take equity you don't have, so if collection escalates, it's your paycheck and bank account in the crosshairs. A modest monthly plan takes both off the table.

What happens if you ignore the balance left after a CP49

A CP49 reduces your debt, but it never pauses collection on what remains. The remaining balance moves through the IRS's automated sequence, each stage carrying more enforcement power than the last:

- CP49 — you are here. The offset posted. The leftover balance accrues penalty and interest from day one.

- Balance-due reminders. CP501 and CP503 notices if your account is in an active collection cycle; an annual CP71 reminder if it's dormant. Still just bills — but growing ones.

- CP504 — Notice of Intent to Levy. The IRS can now seize your state tax refund, and a federal tax lien becomes a live possibility.

- LT11 / Letter 1058 — Final Notice. This starts a 30-day clock and your Collection Due Process rights (requested on Form 12153). After it runs, the IRS can levy wages and bank accounts — the assets a renter actually has.

- Next filing season — the sweep repeats. Every future refund is applied to the balance year after year until it's gone.

One 2026 reality check: per TIGTA reports, IRS staffing fell sharply in 2025, so reaching a human is harder — but offsets, notices, and levies are issued by automated systems that never stopped running. The machine escalates on schedule whether or not anyone reviews your file.

One forward-looking exception worth knowing: if you expect next year's refund and losing it would leave you unable to cover essential living costs, an offset bypass refund for hardship can sometimes protect it — but it generally must be requested before the offset posts, often through the Taxpayer Advocate Service.

The IRS just kept your refund — don't let the rest of the balance ride

Send us your CP49. An experienced tax professional will verify the offset posted correctly, confirm what you actually still owe, and map the cheapest path to closing it out — free, confidential, before penalties and interest add another month's growth.

Your options for the balance that remains

The CP49 doesn't list your options, but the IRS has several — and which one fits depends on the size of what's left and what your budget can honestly carry:

| Option | Upfront cost | Timeline | The catch |

|---|---|---|---|

| Pay in full | $0 | Immediate | None — accruals stop the day the balance hits zero |

| Short-term payment plan | $0 setup | Up to 180 days | Penalties and interest continue until paid |

| Long-term installment agreement | Setup fee (reduced or waived for low income) | Up to 72 months online for balances ≤ $50,000 | Future refunds are still offset while you pay |

| Currently Not Collectible | $0 | Lasts while genuine hardship does | Balance and accruals remain; refunds still offset |

| Offer in Compromise | $205 fee (waived with low-income certification) | Months to a decision; auto-accepted if none within 2 years, with narrow exceptions — a returned or rejected offer stops the clock, and time during court disputes does not count | Means-tested — per IRS data, the IRS accepted roughly 1 in 5 offers in FY2024 |

| Penalty abatement | $0 | Weeks once requested | Removes qualifying penalties only; interest on tax remains |

Two notes at a typical post-CP49 balance. First, an Offer in Compromise is rarely the right tool for a few thousand dollars unless your finances genuinely show the IRS could never collect it — you may qualify only if your income and assets fall short of the full debt over the collection period. Second, penalty relief is worth checking even on small balances: first-time abatement applies if your prior three years were clean, and starting summer 2026 the new Automatic Exemption from Penalty (AEP) grants qualifying relief automatically, with no request needed.

How to respond to a CP49, step by step

- Verify where the money went. Log into your IRS online account and pull the account transcripts for both years — the code 826 entry should match the amount and year printed on the notice.

- Confirm the remaining balance. Compare the balance the CP49 shows with your online account, and note whether any other tax years also carry balances — they'll swallow future refunds too.

- Dispute it if anything is wrong. Call the number printed on the notice with proof of payment or the correct figures; joint filers protecting their share of the refund file Form 8379.

- Pick a plan for what's left. Pay in full, set up a short-term or monthly payment plan, or pursue hardship or settlement options — before the next collection notice arrives.

- Fix next year's withholding. Stop over-withholding so you aren't building another refund the IRS will keep; put that money toward the balance each month instead.

If you agree with the notice and can clear the rest, payment options are all in one place at IRS.gov/payments. The IRS's own summary of this notice is at Understanding your CP49 notice.

When you can handle a CP49 yourself

Most people who receive a CP49 don't need professional help. If the offset matches your records, the debt is genuinely yours, and the remaining balance is something you can pay within 180 days or through a simple online installment agreement, handle it yourself — the whole thing takes an evening.

Experienced help changes outcomes in a narrower set of situations: a CP504 or LT11 has already arrived for the remaining balance and the levy clock is running; you have multiple years with balances or unfiled returns feeding the debt; the offset went to a spouse's separate liability and an injured spouse allocation needs to be built correctly; or paying anything would create genuine hardship, where the CNC and offer math has to be documented, not guessed. In those cases, sequencing — which year, which program, which form first — is what determines the final cost.

Terms on your CP49, decoded

- Refund offset: the IRS keeping your refund and applying it to a debt instead of sending it to you.

- Overpayment: the IRS's word for your refund — tax paid beyond what the year required.

- Code 826: the transcript entry recording an overpayment moved from one tax year to another.

- Injured spouse: a joint filer whose share of a refund was taken for the other spouse's separate debt — recoverable via Form 8379.

- Failure-to-pay penalty: the 0.5%-per-month charge that keeps growing on any balance the offset didn't cover.

- CSED: the Collection Statute Expiration Date — 10 years from assessment, after which the IRS generally can't collect, though appeals, offers, and bankruptcy pause the clock.

CP49 questions, answered

Why did the IRS take my refund and send me a CP49?

Because IRS records show you owe federal tax from a prior year, and the law lets the IRS apply any overpayment to that debt before sending you the rest. No human decided to take your money — the offset runs by computer, and it happens even if you're on a payment plan. Check your IRS online account to confirm the old balance is real before assuming the notice is right.

Can I get my refund back after a CP49 offset?

Usually only if the underlying debt is wrong. If you already paid the old balance, if the money posted to the wrong year, or if the debt belongs to your spouse alone, you can dispute it with proof and have the offset reversed or reapplied. Joint filers whose refund covered a spouse's separate debt can file Form 8379 to recover their share. Hardship reversals after the fact are rare — the offset bypass refund process generally has to happen before the refund is taken.

Will the IRS keep taking my refund every year?

Yes, until the balance is fully paid or otherwise resolved. Refund offsets repeat automatically each filing season, and they continue even while you're on an installment agreement — your refund is applied on top of your monthly payments, which shortens the payoff. Future offsets stop only when the debt is paid off, an offer in compromise is accepted, or the balance expires under the 10-year collection statute.

Is a CP49 the same as a Treasury Offset Program offset?

No. A CP49 means the IRS applied your refund to your own federal tax debt internally. The Treasury Offset Program takes refunds for other debts — child support, federal student loans, state income tax — and posts as code 898 on your transcript, usually with a letter from the Bureau of the Fiscal Service instead of a CP49. The dispute paths are completely different, so identifying which one hit you comes first.

Does a CP49 stop the IRS from levying me?

No. The offset is a collection action, not a pause in collection. If the remaining balance was already in the levy pipeline — you've received a CP504 or LT11 — those notices and their deadlines still stand, and an offset can sit right alongside an active wage or bank levy. Treat the CP49 as confirmation the balance is being actively collected, not as breathing room.

What does code 826 on my transcript mean?

Code 826 is the transcript entry for exactly what a CP49 announces: an overpayment from one tax year transferred to the balance on another year. The date and amount next to code 826 tell you when the offset posted and how much moved. If you see 826 but never received a CP49, the notice may have gone to an old address — update it with Form 8822 so you don't miss the next letter.

Is my CP49 real or a scam?

A real CP49 arrives by postal mail and never asks you to pay through gift cards, wire transfers, or payment apps. It also doesn't demand immediate payment — it reports an offset that already happened. You can verify it in minutes by logging into your IRS online account: the offset will show in your balance and on your transcript. Anyone calling or texting about a "refund seizure fee" is a scammer.

Your next 24 hours

- Find the three figures on your CP49: the amount applied and its receiving year, any remaining refund coming to you, and the balance you still owe. Circle them.

- Gather your records: the notice itself, your last two tax returns, and a recent pay stub or income snapshot — everything needed to verify the offset and price a payment plan.

- Get a free case review: submit the 2-minute form or call (888) 825-7779. The refund is gone, but the leftover balance is still compounding monthly — and it will take next year's refund too. Resolving it this week is the cheapest it will ever be.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.