IRS Notices

IRS CP503 Notice: What It Means, Your Deadline, and What to Do (2026)

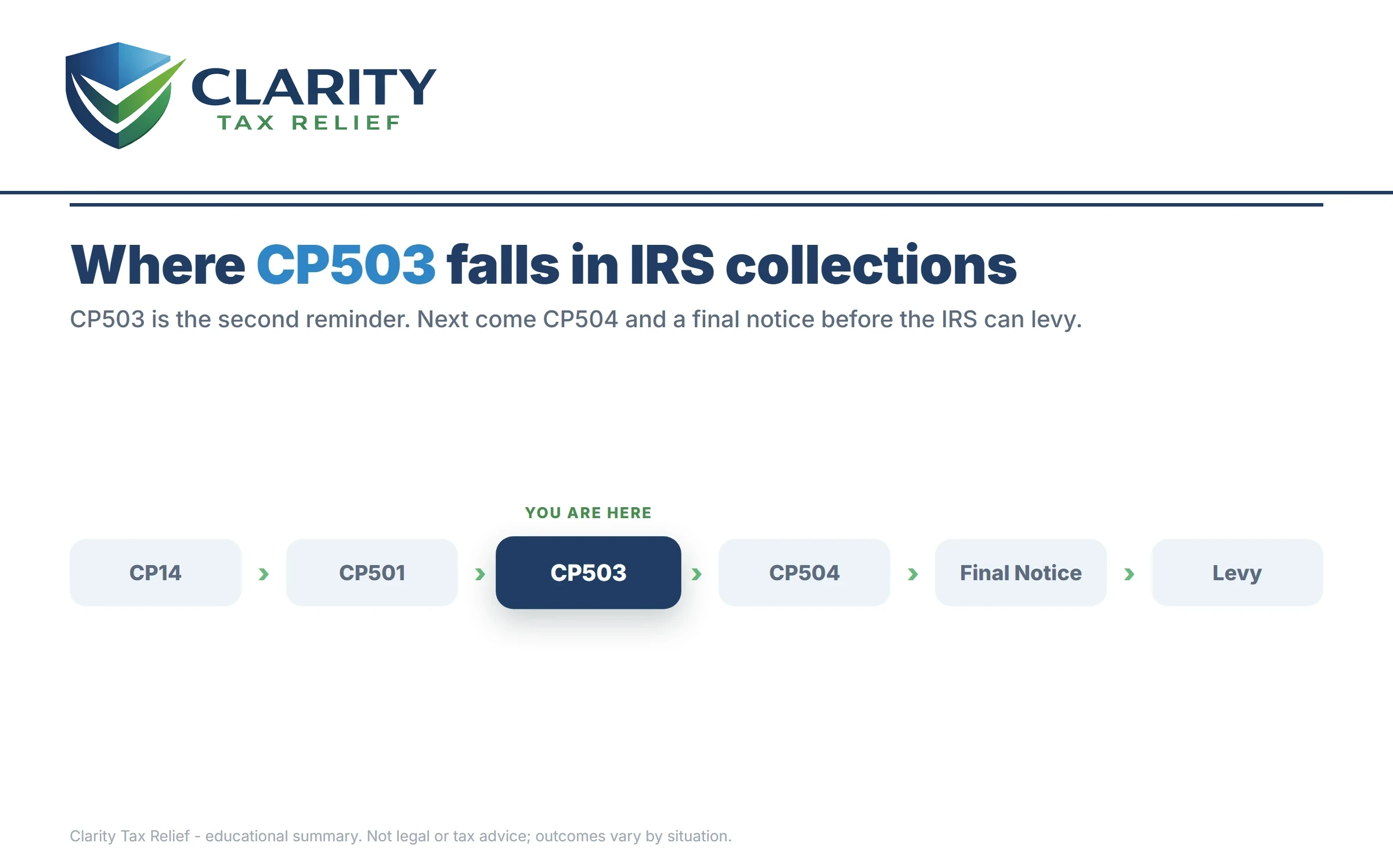

The short answer: a CP503 notice is the IRS's second reminder that you owe back taxes — usually the third letter about the same balance, after the CP14 bill and the CP501 reminder. No levy is coming yet, but only one notice (the CP504) stands between you and enforced collection.

You've seen this letterhead before. The first bill came, then a reminder, and life — the shop, payroll, everything else — got in the way. Now the IRS is writing a third time about the same balance, and the tone has changed. Here's the good news: at the CP503 stage, nothing has been seized, no lien has been filed, and every fix is still on the table. This is the last quiet stop on the collection track, and this guide maps exactly what to do before the next stop.

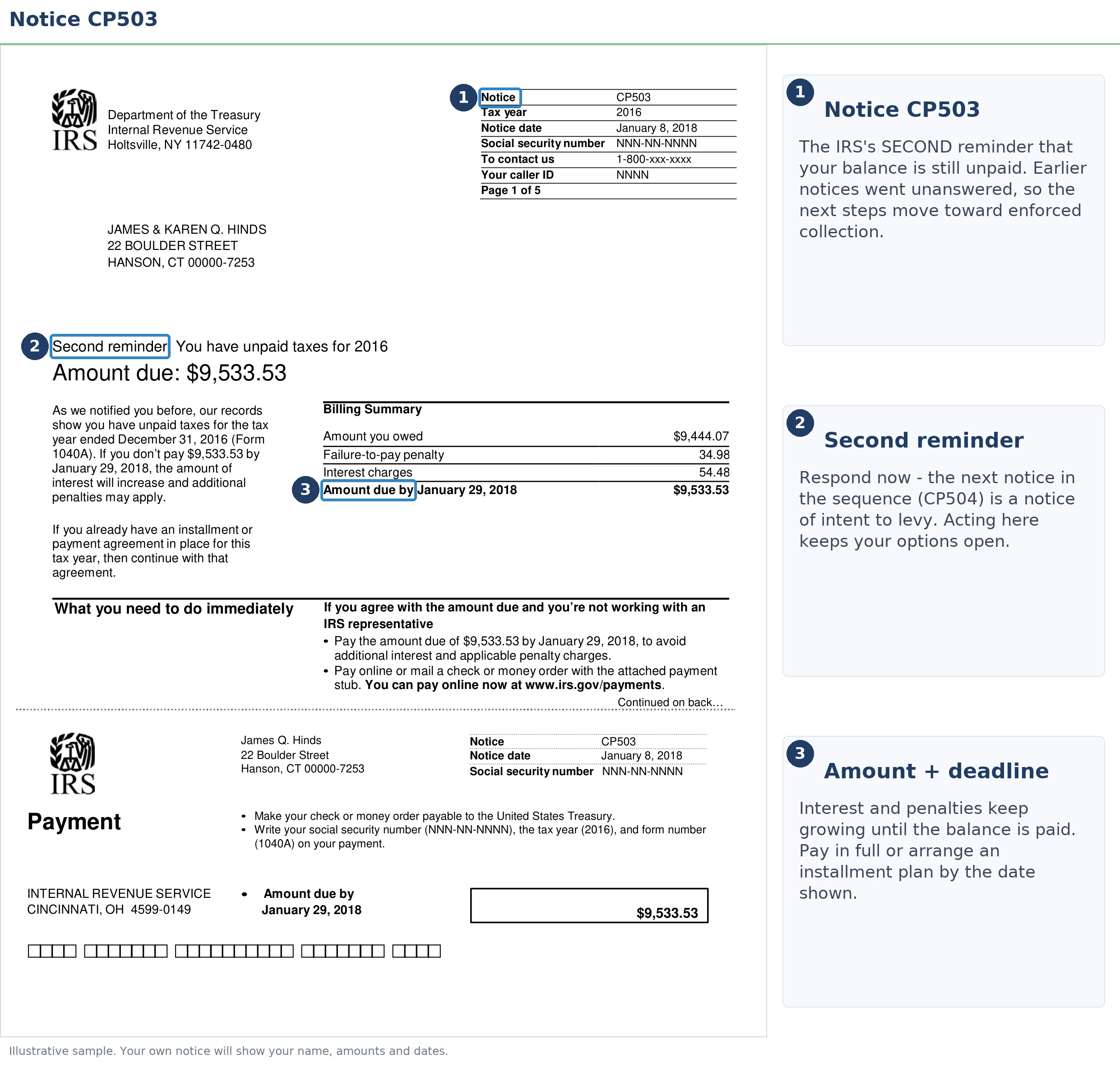

Two numbers on the notice decide everything: the due date and the total with penalties and interest. The image below shows exactly what a CP503 looks like and where to find both.

⏱ Your deadline: the due date printed near the top of your CP503 — that exact date controls your account, not a standard window. If nothing changes by then, the automated system typically issues the CP504 intent-to-levy notice about five weeks later, and your state tax refund becomes seizable.

Why you got a CP503 notice

A CP503 notice means the IRS has now billed you at least twice for the same unpaid balance and recorded no response. The first bill was a CP14 notice; many accounts also get a CP501 notice in between, though some skip straight from CP14 to CP503. Either way, the CP503 is the second reminder — and the last plain bill before the notices with enforcement teeth.

The underlying balance usually comes from one of a few places: a return you filed with tax you couldn't fully pay (common for self-employed and business owners whose quarterly estimates ran short), a math-error adjustment like a CP11 notice that added tax you never addressed, or penalties and interest stacked on a balance you thought was closer to settled.

What a CP503 is not: an audit, a levy, or a lien. Nobody is questioning your return. It's a bill on its third mailing — and if you're not sure why the IRS started writing in the first place, our guide to why did I get a letter from the IRS decodes the whole notice system.

What happens if you ignore a CP503 notice

After a CP503, only one notice — the CP504 — stands between you and the IRS's enforcement powers. The sequence is automated: ignore each letter and the next one typically arrives about five weeks later, with a bigger balance and more legal weight behind it.

- CP14 — the first bill. Typically about 21 days to pay before the reminders begin.

- CP501 — first reminder. Still just a bill, but penalties and interest are compounding.

- CP503 — second reminder. You are here. The last notice with no enforcement attached.

- CP504 — Notice of Intent to Levy under IRC §6331(d). The IRS can seize your state tax refund, and a federal tax lien becomes a realistic next move.

- LT11 / Letter 1058 — Final Notice of Intent to Levy. This starts a 30-day clock and your Collection Due Process rights (requested on Form 12153). After it expires, wage garnishment and bank levies become legal.

- Levy — a bank levy freezes funds for 21 days before they're sent to the IRS; a wage levy is continuous until released.

One 2026 reality check: the IRS workforce shrank roughly 27% in 2025, so reaching a human is harder than ever — but the notice stream, liens, and levies run on automated systems that never took a furlough. The machine escalates on schedule whether or not anyone answers the phone. The full sequence, with day counts, is in our guide to the order of IRS collection letters.

| Notice | What it is | What changes / your window |

|---|---|---|

| CP14 | First bill for the balance | Typically about 21 days to pay; no enforcement yet |

| CP501 | First reminder | Due date printed on the notice; balance growing monthly |

| CP503 (you are here) | Second reminder — last plain bill | Due date printed on the notice; last stage with zero enforcement attached |

| CP504 | Notice of Intent to Levy (§6331(d)) | State tax refund becomes seizable; lien filing becomes realistic |

| LT11 / Letter 1058 | Final Notice of Intent to Levy | 30 days to request a CDP hearing (Form 12153) before wage and bank levies become legal |

Holding a CP503 right now?

Get it reviewed free before the due date printed on it passes. An experienced tax professional will confirm where you sit in the sequence, whether the penalties can come off, and which arrangement stops the CP504 from ever printing — no pressure, no obligation.

Your options if you can't pay the full CP503 balance

Every IRS resolution program is still fully available at the CP503 stage — nothing has been lost yet. The notice offers "pay now" as if it's the only choice; in reality the right fit depends on how much you owe and what your cash flow looks like:

- Pay in full — stops penalties, interest, and the notice sequence the day the payment posts. Cheapest by far if the cash exists.

- Short-term payment plan — up to 180 days to full-pay, $0 setup fee. Interest and the late-payment penalty keep running, but the CP504 never issues.

- Guaranteed installment agreement — for individuals only, with an income-tax balance of $10,000 or less (excluding penalties and interest). The IRS generally must accept a plan that full-pays within 3 years if all your returns are filed, you've filed and paid on time for the past 5 years, and you haven't had an installment agreement during that period.

- Streamlined / online installment agreement — balances up to $50,000 can be set up online for up to 72 months, usually without submitting financial statements. Interest and penalties continue, though the late-payment penalty rate drops while a plan is in effect.

- Currently Not Collectible — if any payment would leave you unable to cover basic living or business-survival expenses, collection can be paused. The debt remains and interest accrues, but levies stop.

- Offer in Compromise — settling for less than the full balance when your income and assets genuinely can't cover it. It's real but means-tested: the IRS accepted roughly 1 in 5 offers in FY2024, and at smaller balances a payment plan usually beats the $205 application cost and months of review.

- Penalty relief — first-time penalty abatement can remove the failure-to-pay penalty if your prior three years were clean. And starting summer 2026, the IRS's new Automatic Exemption from Penalty (AEP) begins applying that relief automatically, with no request needed — so check whether penalties on your notice already qualify before paying them.

| Balance on the notice | Realistic options | What it takes |

|---|---|---|

| Under $10,000 | 180-day plan; guaranteed installment agreement (full-pay in 36 months) | Online setup; all returns filed; no financial disclosure |

| $10,000 – $25,000 | Streamlined installment agreement, up to 72 months | Online setup; no financial statements in most cases |

| $25,000 – $50,000 | Online agreement up to 72 months; direct debit typically required at the upper end | Online setup; direct-debit enrollment |

| Over $50,000 | Negotiated agreement, Currently Not Collectible, or Offer in Compromise | Financial disclosure (Form 433 series); professional help usually pays for itself here |

Say you owe $6,200 on a CP503: the math on each option

A hypothetical $6,200 CP503 balance grows by about $31 in failure-to-pay penalty every month it sits, before interest. Say you're a small-business owner whose quarterly estimates ran short and the CP14 arrived months ago. The failure-to-pay penalty runs 0.5% per month: $6,200 × 0.5% = $31/month, roughly $372 over a year — plus interest, which is set quarterly and compounds daily on top. You can rough out your own accrual with our Penalty & Interest Calculator.

Here's how the main options compare on that balance:

- 180-day short-term plan: roughly $6,200 ÷ 6 ≈ $1,034/month equivalent to be done in six months. $0 setup fee, and the smallest total accrual of any stretch-out.

- Guaranteed installment agreement: $6,200 ÷ 36 ≈ $172/month before accruals. Because a balance under $10,000 with clean recent compliance generally must be accepted, this is the lowest-friction monthly option — and while a plan is in effect, the late-payment penalty rate drops from 0.5% to 0.25% per month (about $15.50/month at the start, declining as you pay down).

- Offer in Compromise: almost never the answer at $6,200 if you can afford $172 a month — the IRS's own math would show it can collect in full, so the offer would fail. OICs earn their keep at balances your finances genuinely can't cover.

The takeaway: at this balance, the question isn't whether you can resolve it — it's only which payment shape fits your cash flow, and whether the ~$372/year in penalties can be abated on top.

Running payroll? Don't fix the 1040 by shorting your 941 deposits

The most expensive mistake a business owner can make with a personal CP503 is covering it with money withheld from employees' paychecks. Those withheld taxes are trust funds — fall behind on them and you trade a $6,200 bill with easy payment options for 941 back taxes, where the Trust Fund Recovery Penalty can make you personally liable and the IRS assigns humans, not just letters. Keep the payroll deposits sacred; put the 1040 balance on a plan instead.

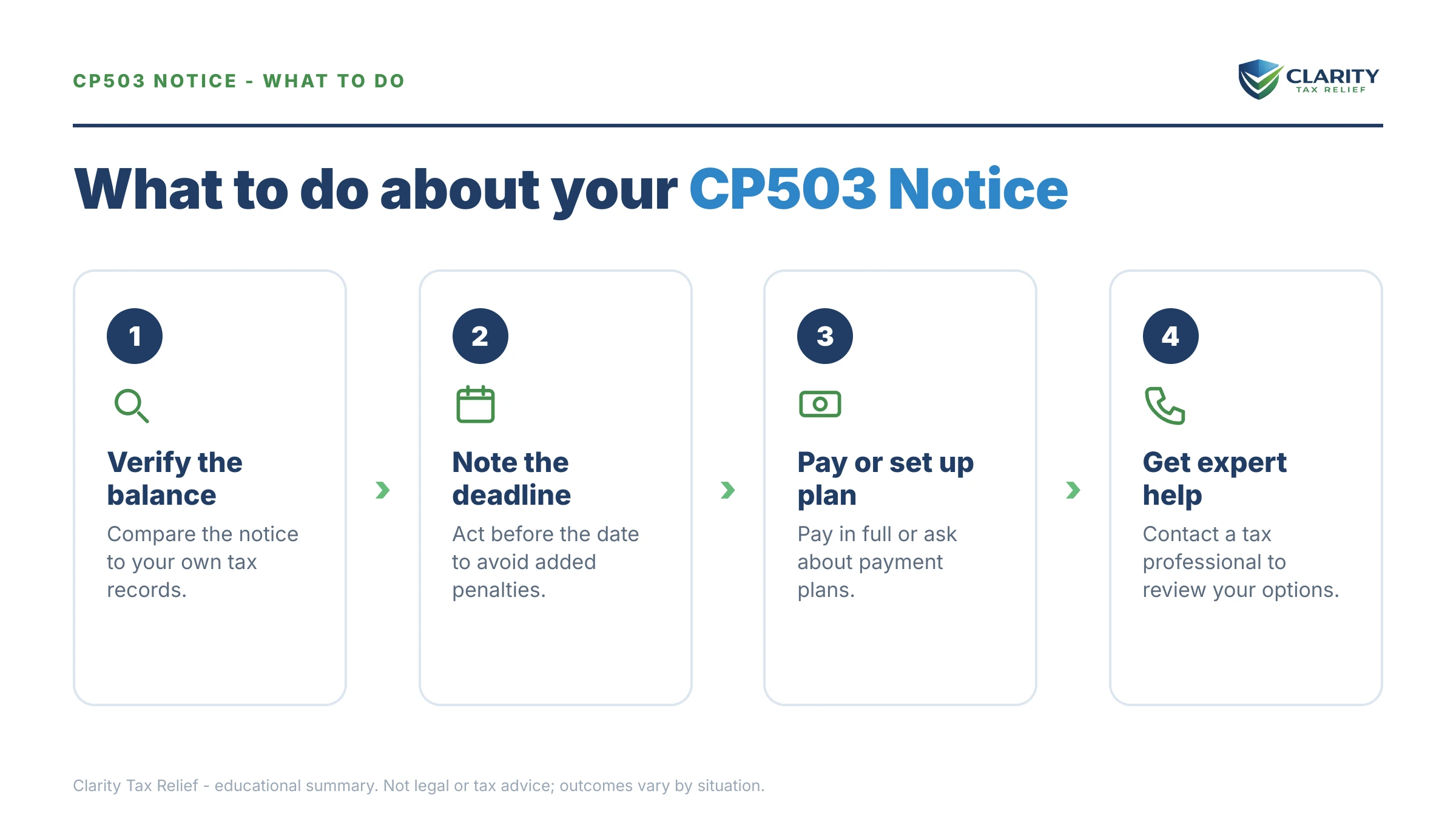

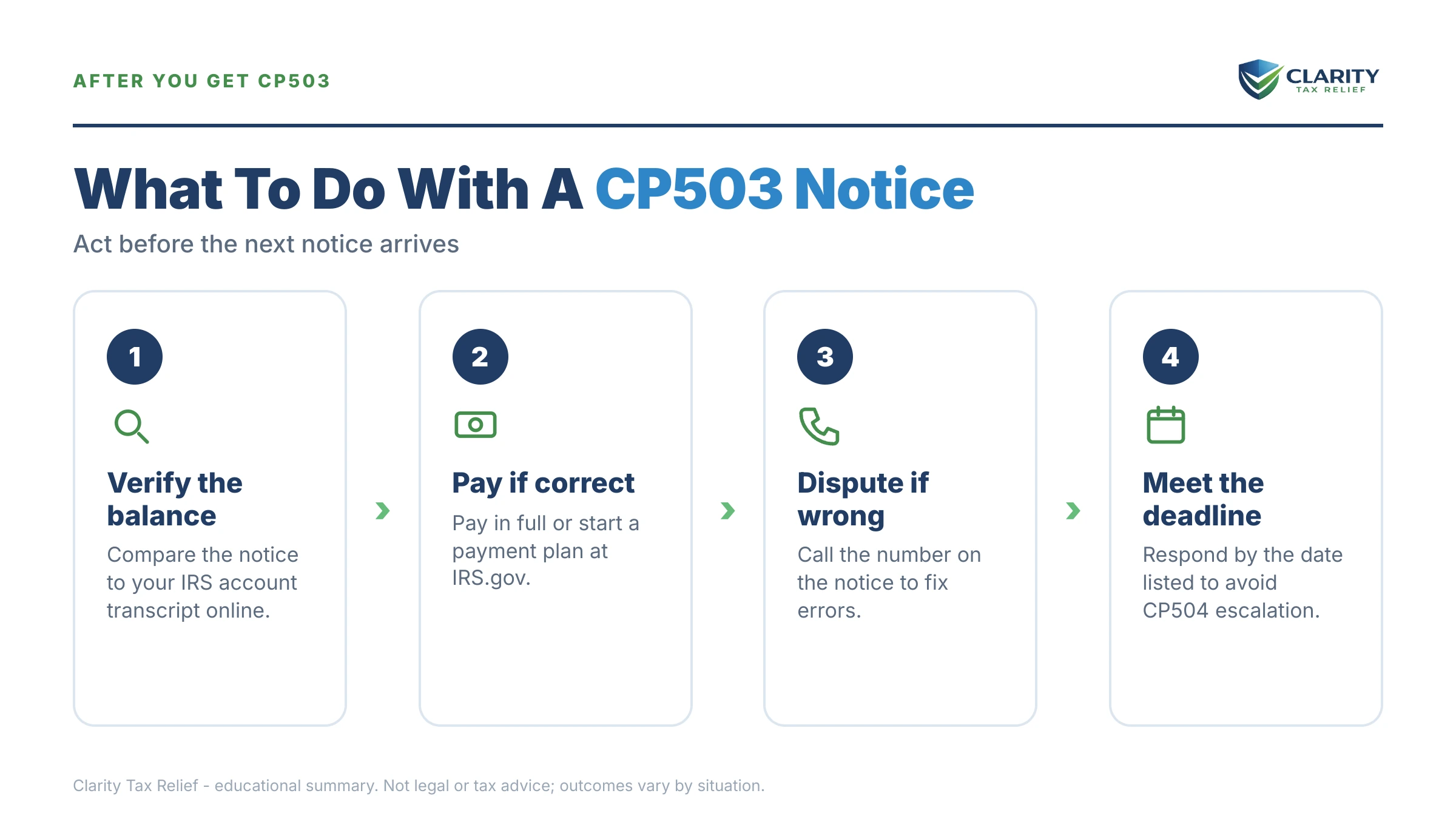

How to respond to a CP503, step by step

- Find the due date and the breakdown — the due date is printed near the top of the notice, and the balance is split into tax, penalties, and interest. Note all three; the penalty portion may be removable.

- Verify the balance — log into your IRS online account and confirm the amount matches. Payments made in the last few weeks may not appear on the notice.

- Pay in full if you can — pay by the due date at IRS.gov/payments. Full payment stops the penalty, the interest, and the notice sequence the day it posts.

- Set up an arrangement if you can't — a 180-day short-term plan or a monthly installment agreement, started before the due date, keeps the CP504 from issuing on this balance.

- Dispute in writing if the balance is wrong — respond with proof of payment or corrected figures using the address on the notice, and keep copies of everything you send.

When you can handle a CP503 yourself — and when help changes the outcome

Most single-year CP503 balances under $50,000 can be resolved without hiring anyone. If you agree with the amount, have all your returns filed, and just need time to pay, the online payment-plan setup on the IRS payment plans page takes minutes — and at $6,200, a guaranteed installment agreement is about as close to a sure thing as the IRS offers when you meet its conditions.

Experienced help earns its fee when the picture is more tangled: the balance covers multiple years or includes years you never filed, you dispute the amount, you're carrying business payroll debt alongside the personal balance, a CP504 or LT11 has already arrived for another year, or your finances point toward hardship status or an Offer in Compromise — where the disclosure forms and the math decide everything. In those cases, the order you fix things in (returns first, then penalties, then the balance) genuinely changes what you pay.

Terms on your CP503, decoded

- Notice date vs. due date: the notice date is when the letter was generated; the due date — usually near the top — is the one that controls your account.

- Second reminder: the IRS's own label for the CP503 — confirmation that at least two earlier bills exist for this balance.

- Failure-to-pay penalty: the 0.5%-per-month charge on unpaid tax, capped at 25% of the balance; it drops to 0.25%/month while an installment agreement is in effect.

- Lien vs. levy: a lien is a public legal claim against your property; a levy is the actual taking of money or assets. Neither has happened at the CP503 stage.

- Intent to levy: the language the next notice (CP504) will carry — the legal step that lets the IRS take your state tax refund.

- CSED: the Collection Statute Expiration Date — generally 10 years from assessment, though appeals, offers, and bankruptcy pause the clock.

The IRS's own summary of this notice is at Understanding your CP503 notice.

CP503 questions, answered

Is a CP503 notice serious?

Yes — more serious than the first bill, but no levy is happening yet. A CP503 means the IRS has billed you at least twice with no response it can see, and the next notice in the sequence, the CP504, carries real enforcement power. Nothing is being garnished at this stage, and every resolution option is still open. The mistake is treating it like the reminders that came before it.

How long do I have to respond to a CP503 notice?

Your deadline is the due date printed near the top of the notice — the IRS expects payment or a payment arrangement by that date. If nothing happens on the account, the automated system typically issues the next notice, the CP504 intent to levy, about five weeks later. Penalties and interest keep accruing the entire time, so acting before the printed date is always cheaper.

Can the IRS levy my bank account after a CP503?

Not based on the CP503 alone. Before levying wages or bank accounts, the IRS must first send a final notice of intent to levy — the LT11 or Letter 1058 — and then wait 30 days while you can request a Collection Due Process hearing with Form 12153. The CP503 is two steps before that. The exception is your state tax refund, which becomes seizable at the next notice, the CP504.

What is the difference between a CP501 and a CP503?

They carry the same legal weight — both are reminder bills — but the CP503 comes later in the sequence and signals the IRS's patience is running out. The CP501 is the first reminder after the CP14 bill; the CP503 is the second, and it is the last plain reminder before the CP504 intent-to-levy notice. Some accounts skip the CP501 entirely and go straight from CP14 to CP503.

What happens after a CP503 if I don't pay?

The CP504 Notice of Intent to Levy comes next, typically about five weeks later. At that point the IRS can seize your state tax refund and a federal tax lien becomes a realistic possibility. After the CP504 comes the LT11 final notice, which starts a 30-day clock before wage garnishment and bank levies become legal. The sequence is automated — it doesn't pause because IRS phone lines are busy.

Can I still set up a payment plan after receiving a CP503?

Yes — every payment option is still fully available at the CP503 stage. Balances of $50,000 or less can qualify for an online installment agreement of up to 72 months; under $10,000, you may qualify for a guaranteed installment agreement the IRS generally must accept if you meet the filing and payment conditions. Setting up any plan before the CP504 issues stops the escalation.

Why did I get a CP503 if I never saw a CP14 or CP501?

Usually because the earlier notices went to an old address or were lost — the IRS mails to your last known address from your most recent return, and it isn't required to prove you read them. The balance and the sequence are still valid. Update your address with Form 8822, then verify the balance in your IRS online account before paying anything.

Does a CP503 affect my credit score?

No — the CP503 itself is invisible to credit bureaus, and since 2018 the bureaus no longer include federal tax liens on credit reports at all. The real financial exposure comes later: a filed Notice of Federal Tax Lien is still a public record that lenders can find in searches, and it can complicate mortgages and business credit even though it no longer appears in your score.

Your next 24 hours

- Find the due date and the breakdown on the notice. Note the due date near the top and how the total splits into tax, penalties, and interest — the penalty slice is the part that may come off.

- Gather three things: the CP503 itself, the tax return for the year it covers, and a quick snapshot of your monthly income and expenses (business owners: include your payroll deposit status).

- Get a free case review before the printed due date passes — call (888) 825-7779 or use the 2-minute form. An experienced tax professional will confirm the balance, check your penalty-relief eligibility, and set up the arrangement that keeps the CP504 from ever printing.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.