IRS Notices

IRS CP508C Notice: Passport Certification for Tax Debt — What to Do (2026)

The short answer: a CP508C notice means the IRS has certified your tax debt as "seriously delinquent" — $66,000 or more in 2026 — to the State Department, which can now deny your passport application or renewal. Paying the balance below $66,000 won't reverse it; paying in full or entering a qualifying payment arrangement will.

You're planning something that needs a passport — a trip, a contract abroad, family overseas — and instead of a renewal in the mail, the IRS just told the State Department to say no. That's what a CP508C does. It's jarring, but it's a status, not a sentence: certifications get reversed every day, and the fastest path off the list is more mechanical than most people expect.

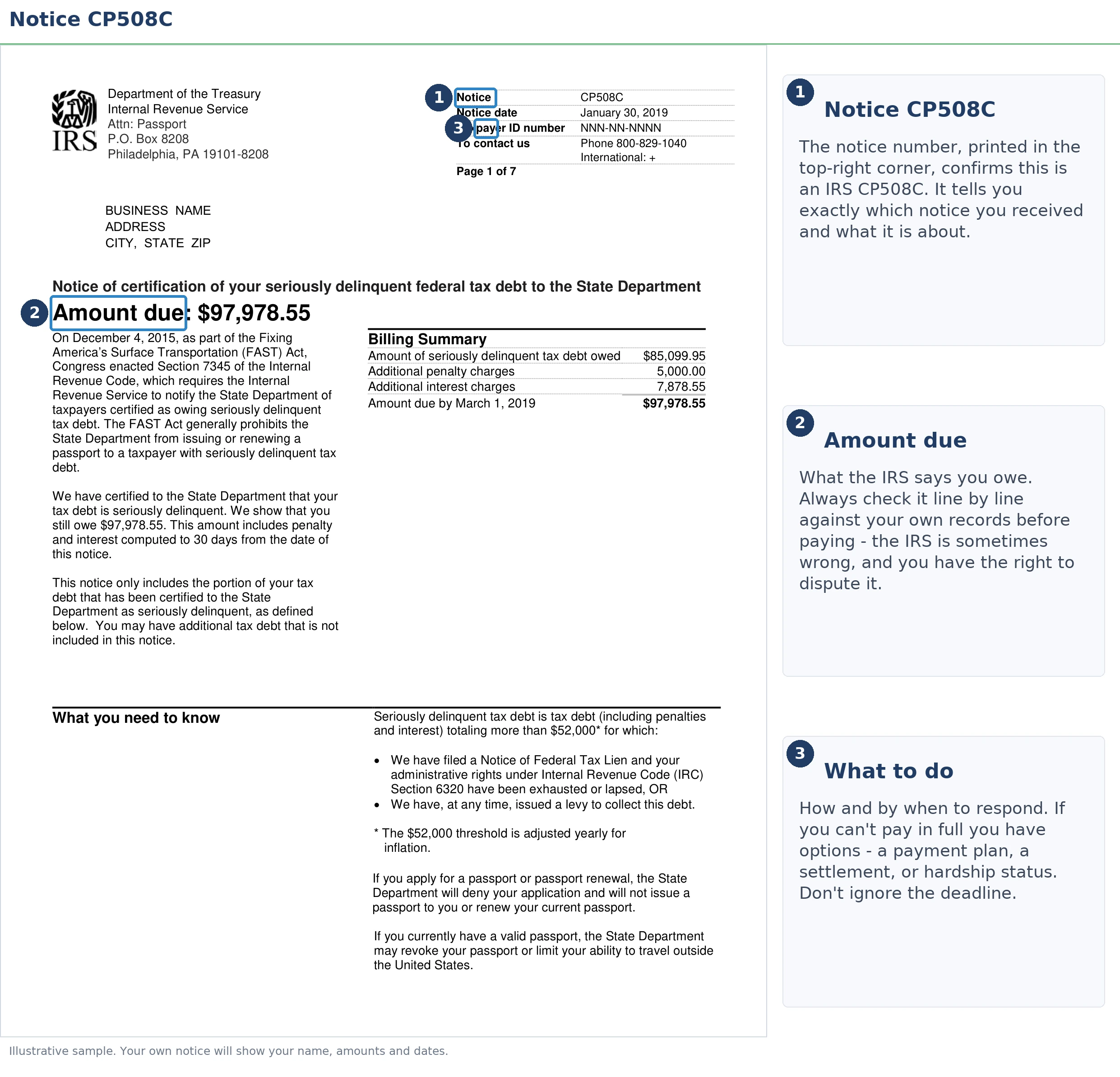

Two numbers on this notice matter more than everything else on it: the certified balance and the tax years it covers. The image below shows you exactly what a CP508C looks like and where to find both before you decide anything.

⏱ The clock that matters: if you already applied for a passport or renewal, the State Department typically holds your application open for 90 days after denial so you can resolve the certification — miss that window and you start the application over. No application pending? Your clock is the interest and the 0.5% monthly late-payment penalty growing the certified balance every month.

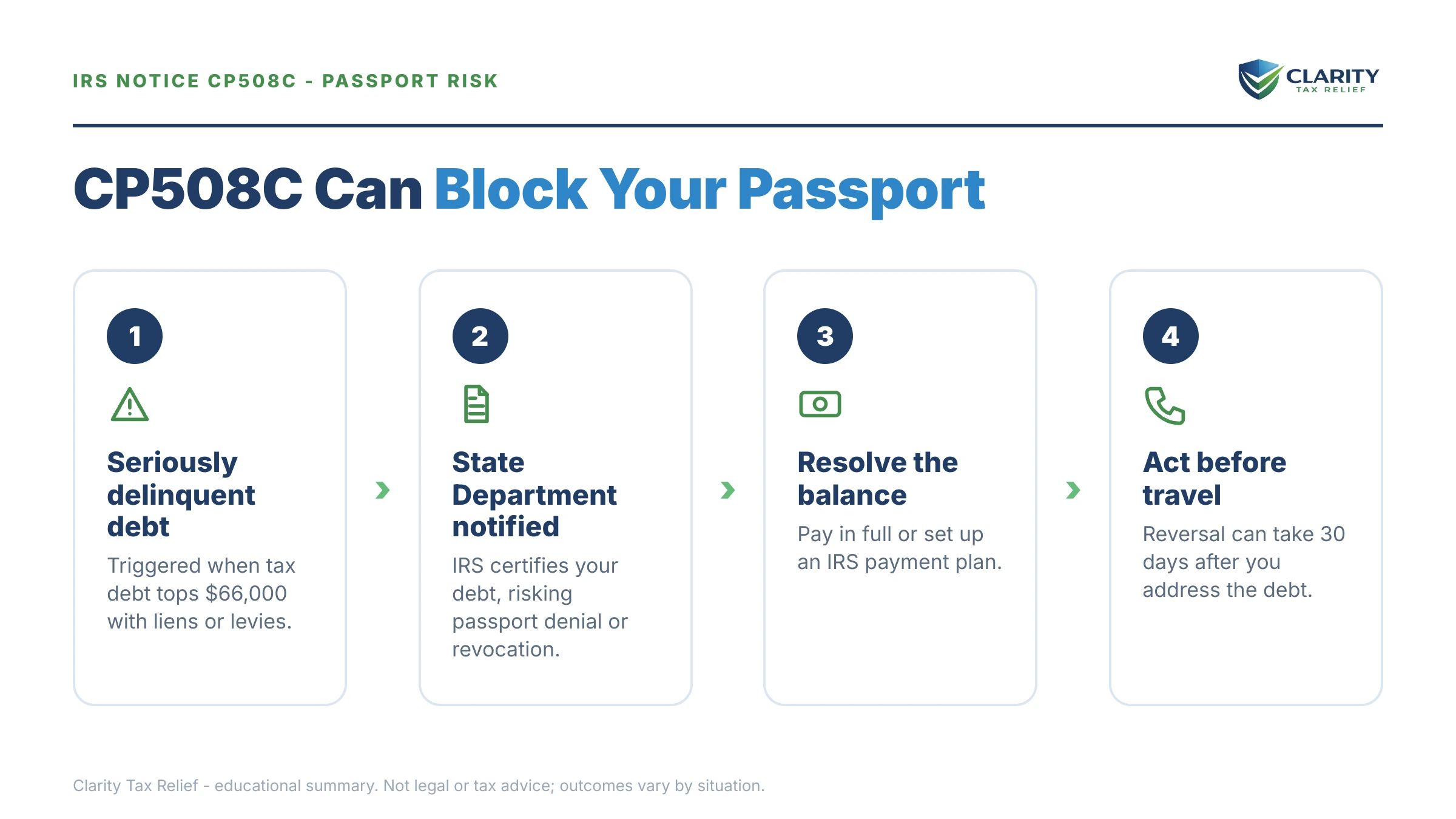

Why you got a CP508C

The IRS sends a CP508C only when two things are both true: your total unpaid, legally enforceable federal tax debt exceeds $66,000 (the 2026 inflation-adjusted threshold), and the IRS has already filed a Notice of Federal Tax Lien (with your appeal window lapsed) or issued a levy. Internal Revenue Code §7345 then requires the IRS to certify that debt to the State Department.

The threshold counts everything together — tax, penalties, and interest, across all your open years. That's how people who never owed $66,000 in any single year end up certified: three modest balances, compounding monthly, cross the line as a group. If you've been ignoring mail for a while, our guide to why did I get a letter from the IRS maps the whole system; this page covers only the passport certification.

Some debts never count toward the $66,000. FBAR penalties and child support aren't part of the calculation. And debt isn't "seriously delinquent" while you're paying timely under an installment agreement or accepted Offer in Compromise, while a timely Collection Due Process hearing or innocent spouse request is pending, during bankruptcy, in confirmed identity-theft cases, in hardship (Currently Not Collectible) status, or while you're in a federally declared disaster area or combat zone.

| Stage | Notice | What it means for you |

|---|---|---|

| First bill | CP14 | The IRS says you owe; typically about 21 days to pay before escalation begins. |

| Reminders | CP501 / CP503 | Still just bills, but penalties and interest grow the balance monthly. |

| Intent to levy | CP504 | The IRS can seize your state tax refund; a federal lien becomes likely. |

| Final notice | LT11 / Letter 1058 | A 30-day clock with Collection Due Process rights; levy authority follows. |

| Lien or levy | Letter 3172 / levy notices | The legal prerequisite for passport certification is now met. |

| Certification | CP508C | Debt over $66,000 is certified to the State Department; passports are denied. |

| Reversal | CP508R | Sent when the debt is resolved or in a qualifying arrangement — certification removed. |

What a CP508C actually does to your passport

A CP508C blocks new passports and renewals; it does not automatically cancel the passport in your drawer. The State Department's first action is denial: your pending or future application gets refused, held open for that 90-day resolution window, then closed if nothing changes.

A passport you already hold usually keeps working after certification — until it expires. Then you can't renew. The State Department also has the authority to revoke a certified taxpayer's passport outright or limit it to direct return travel to the United States, though revocation is discretionary rather than automatic. If you live overseas, that distinction is the whole ballgame — see our guide on owing the IRS and moving abroad for how certification plays out from outside the country.

One more thing the CP508C does not give you: Collection Due Process rights. Unlike an LT11 notice, there's no built-in hearing to request on the certification itself. Your remedies are fixing the underlying debt, asking the IRS to correct an erroneous certification, or — in genuine error cases — suing under §7345 in Tax Court or district court.

What happens if you ignore a CP508C notice

Ignoring a CP508C keeps your passport blocked indefinitely — the certification has no expiration date and no automatic review. Here's the sequence if you do nothing:

- Applications and renewals denied. Any pending passport application is held about 90 days, then denied. Every future application meets the same wall until the IRS decertifies you.

- Letter 6152 may arrive. Before recommending that the State Department revoke a passport you already hold, the IRS generally sends Letter 6152 asking you to call and resolve the debt. Treat it as the last friendly touch.

- Revocation or limitation. The State Department can revoke your current passport or restrict it to return-only travel to the U.S. This is discretionary — but it's on the table for as long as you stay certified.

- Collection keeps running in parallel. The certification is an add-on, not a substitute. Wage and bank levies remain available, up to 15% of Social Security benefits can be taken through the Federal Payment Levy Program, and interest plus the monthly failure-to-pay penalty keep compounding the certified balance.

In 2026 there's no waiting this out. IRS staffing is down sharply, but certifications, liens, and levies come from automated systems that never got smaller — the debt grows and the block stays until something on your side changes.

Certified and need your passport back?

Get your CP508C reviewed free. An experienced tax professional will map the fastest qualifying arrangement for your numbers — and flag the imminent-travel expedite if you have a trip coming. The certification doesn't lift on its own, and interest grows the balance every month you wait.

How to reverse a CP508C certification: your real options

Once the IRS certifies your debt, only full payment, legal unenforceability, or a qualifying arrangement reverses a CP508C — paying the balance below $66,000 does not. That surprises almost everyone: the threshold controls who gets certified, not who gets decertified. A partial payment that drops you to $65,000 changes nothing; a modest monthly agreement changes everything.

| Option | What it takes | Effect on the certification |

|---|---|---|

| Pay in full | Full payment of every certified year — tax, penalties, and interest | Reversed, generally within 30 days; CP508R confirms it. |

| Installment agreement | Under $50,000: streamlined setup online, up to 72 months. Larger balances need financial disclosure | Debt is no longer "seriously delinquent" once the agreement is active; reversal generally within 30 days. |

| Offer in Compromise (accepted) | IRS accepts your offer based on what it can realistically collect — roughly 1 in 5 offers were accepted in FY2024 | Reversed once accepted, while you pay the offer terms on time. |

| Timely CDP hearing request | Form 12153 filed within the 30-day window printed on your levy notice, if it's still open | Reversed while the hearing is pending. |

| Innocent spouse relief | Form 8857 requesting relief on a joint-year liability | Reversed while the request is pending. |

| Hardship (CNC) status | Financial disclosure showing collection would prevent basic living expenses | Hardship accounts fall outside the "seriously delinquent" definition; confirm the IRS updates the certification. |

| CSED expiration | The 10-year collection statute runs out, making the debt legally unenforceable | Reversal required — but appeals, offers, and bankruptcy pause the clock. |

For most certified taxpayers, the installment agreement is the workhorse. A streamlined installment agreement covers balances up to $50,000 over as long as 72 months with no detailed financial disclosure — but a certified balance is by definition above $66,000, so you'll either need to reduce the assessed amount first (more on that in the example below) or set up a non-streamlined agreement with financials. Either way, interest and penalties keep accruing inside any plan; faster payoff is always cheaper.

An Offer in Compromise reverses the certification only after acceptance, not at filing — and the IRS runs the math on your assets and future income, not on how much you'd like to pay. Read how an offer in compromise works before betting your travel plans on one; the $205 application fee, and the 20% down payment on lump-sum offers, are both waived if your income is at or below 250% of the federal poverty level.

Two quieter paths deserve a look. If your levy notice arrived recently, a timely Form 12153 CDP hearing request triggers reversal while the hearing is pending. And if the debt is old, check the 10-year collection statute — debt past its CSED is legally unenforceable and must be decertified. You can estimate your own expiration dates with our CSED Calculator.

Penalty relief won't decertify you by itself, but it shrinks what any of these options costs. First-time abatement can remove a year's penalties if your prior three years were clean — and starting summer 2026, the IRS's new Automatic Exemption from Penalty applies similar relief automatically, with no request needed.

A worked example: three unfiled years and a $71,400 certification

Say you're a gig worker who hasn't filed in three years. The platforms sent 1099s, so the IRS eventually filed a substitute return for each year — counting every dollar as profit, with no mileage, no fees, no expenses. Each year's assessment lands at $23,800 in tax, penalties, and interest. Total: 3 × $23,800 = $71,400. That's over $66,000, a lien is on file, and the CP508C follows.

The instinctive move — scraping together $6,000 to get the balance to $65,400 — accomplishes nothing. Once certified, dropping below the threshold doesn't trigger a reversal.

The right sequence: file the three real returns first. Substitute returns almost always overstate what a self-employed person owes, because they skip Schedule C expenses entirely. Say your actual returns — with mileage, platform fees, and supplies — bring the total assessed debt to $41,200. Now the balance is under $50,000, and a streamlined installment agreement is available online: $41,200 ÷ 72 months ≈ $572/month at the minimum (interest keeps accruing, so paying more shortens the pain). Once that agreement is active, the debt is no longer seriously delinquent, the IRS generally reverses the certification within 30 days, and the CP508R follows — even though you never paid the balance down first. If unfiled years are the root of your problem, start with our guide for people who haven't filed taxes in 3 years.

This is a hypothetical illustration — your assessed amounts, deductions, and plan terms will differ.

How to respond to a CP508C notice, step by step

- Pull your IRS account records. Log in to your IRS online account and confirm the certified balance, the tax years involved, and whether every required return has actually been filed.

- Fix the balance before you pay it. If any year is a substitute-for-return assessment, file the real return first — correcting an inflated balance is often the biggest single reduction available.

- Choose your qualifying arrangement. Pick full payment, an installment agreement, an Offer in Compromise, or hardship status based on what your income and assets genuinely support.

- Get the arrangement active before you travel. Set it up and confirm it is in force; the IRS generally reverses the certification within 30 days, and can typically expedite when you have imminent travel plans.

- Confirm the reversal with Notice CP508R. Watch for the CP508R confirming decertification, keep a copy, and bring proof of the reversal if you apply for a passport soon afterward.

When you can handle a CP508C yourself

You can often clear a CP508C on your own if your returns are all filed, the certified balance is accurate, and no travel is booked. In that case the job is a payment plan: set it up online or by phone, confirm it's active, and wait for the CP508R. No professional required.

Experienced help changes the outcome in four situations. First, imminent travel — the expedite process only helps if the arrangement, the IRS notification, and the State Department timing are coordinated correctly the first time. Second, unfiled years or substitute-return assessments, where the order of operations (file, then arrange) determines whether you're negotiating on $71,400 or $41,200. Third, Offer in Compromise math, where a miscalculated offer costs months and a rejection. Fourth, an erroneous certification — wrong taxpayer, excluded debt, or a balance the IRS mis-totaled — where the correction request or a §7345 suit needs to be built on documentation, not frustration. For deeper background on the passport program itself, see our guides on a passport revoked for tax debt and being denied a passport at the $66,000 tax debt threshold.

Terms on your CP508C, decoded

- Seriously delinquent tax debt: unpaid, legally enforceable federal tax debt over the inflation-adjusted threshold ($66,000 in 2026) where a lien has been filed or a levy issued.

- Certification: the IRS formally telling the State Department, under IRC §7345, that your debt meets that definition.

- CP508R: the notice you receive when the IRS reverses the certification and tells the State Department you're clear.

- Letter 6152: the IRS's heads-up letter, sent before it recommends the State Department revoke a passport you already hold.

- Collection Due Process (CDP): the formal hearing right attached to levy and lien notices — a timely request is itself a decertification trigger.

- CSED / legally unenforceable: the Collection Statute Expiration Date; debt the IRS can no longer legally collect must be decertified.

Primary sources: the IRS's official Understanding your CP508C notice page, its payment plans and installment agreements page, and the Taxpayer Advocate Service, which can intervene when a decertification stalls and travel or work depends on it.

CP508C questions, answered

What is a CP508C notice from the IRS?

A CP508C tells you the IRS has certified your tax debt to the State Department as seriously delinquent under Internal Revenue Code Section 7345. That certification lets the State Department deny your passport application or renewal, and in some cases revoke a passport you already hold. It only happens when your total debt exceeds the inflation-adjusted threshold — $66,000 in 2026 — and the IRS has already filed a lien or issued a levy.

Will my passport be revoked immediately because of a CP508C?

No. The immediate effect is that the State Department will deny new passport applications and renewals. Revocation of a passport you already hold is discretionary and less common, and the IRS generally sends Letter 6152 asking you to call before it recommends revocation. That gap is your window to get into a qualifying arrangement first.

How do I reverse a CP508C certification?

Get the debt out of seriously delinquent status: pay it in full, enter an installment agreement, get an Offer in Compromise accepted, make a timely Collection Due Process hearing request, or request innocent spouse relief. Once any of those happens, the IRS generally reverses the certification within 30 days and notifies the State Department. You'll receive Notice CP508R confirming the reversal.

If I pay my balance below $66,000, does the certification go away?

No — this is the most expensive misunderstanding about the CP508C. Once you're certified, paying the balance below the threshold does not by itself trigger a reversal. The IRS reverses only when the debt is fully paid, becomes legally unenforceable, or is no longer seriously delinquent because you entered a qualifying arrangement. A $600-a-month installment agreement can do what a $10,000 lump payment can't.

How fast can I get my passport back if I have travel planned?

Once your debt is resolved or in a qualifying arrangement, the IRS generally reverses the certification within 30 days and notifies the State Department. If you have imminent travel plans — generally within the next 45 days — tell the IRS when you set up your arrangement; it can typically expedite the reversal. Start before you book anything nonrefundable; nothing moves until an arrangement is actually in place.

Can I appeal or fight a CP508C certification?

There's no Collection Due Process hearing attached to a CP508C itself. If you believe the certification is erroneous — the debt isn't yours, it's below the threshold, or it falls into an excluded category — you can ask the IRS to correct it, and Section 7345 lets you sue in U.S. Tax Court or federal district court to have an erroneous certification reversed. For most people, though, fixing the underlying debt is faster than litigating the certification.

Does a CP508C affect a passport I already have?

Usually you can keep using a valid passport after certification — the State Department's first action is blocking new applications and renewals, not confiscating your current one. But the State Department has authority to revoke a certified taxpayer's passport or limit it to return travel to the United States. If your passport expires while you're certified, you won't be able to renew until the certification is reversed.

Are both spouses certified on a joint tax debt?

Certification is individual, but joint liability means each spouse is personally liable for the full balance — so both spouses can receive their own CP508C for the same debt. If the debt really traces to your spouse's income or actions, a request for innocent spouse relief is itself a reversal trigger while it's pending. Filing separately going forward doesn't undo certification on old joint years.

Your next 24 hours

- Find the certified balance and tax years on your CP508C. They're the two facts that determine whether you can reduce the debt before you arrange to pay it — and note whether any listed year is one you never actually filed.

- Gather your records: the notice itself, your last filed return, 1099s or income records for any unfiled years, and any upcoming travel dates. Those four things are the whole intake.

- Get a free case review. Call (888) 825-7779 or use the 2-minute form. The certification stays until a qualifying arrangement exists, and interest grows the balance monthly — the review tells you which arrangement gets your passport back fastest.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.