IRS Notices

IRS CP521 Notice: Your Payment Plan Reminder, Explained (2026)

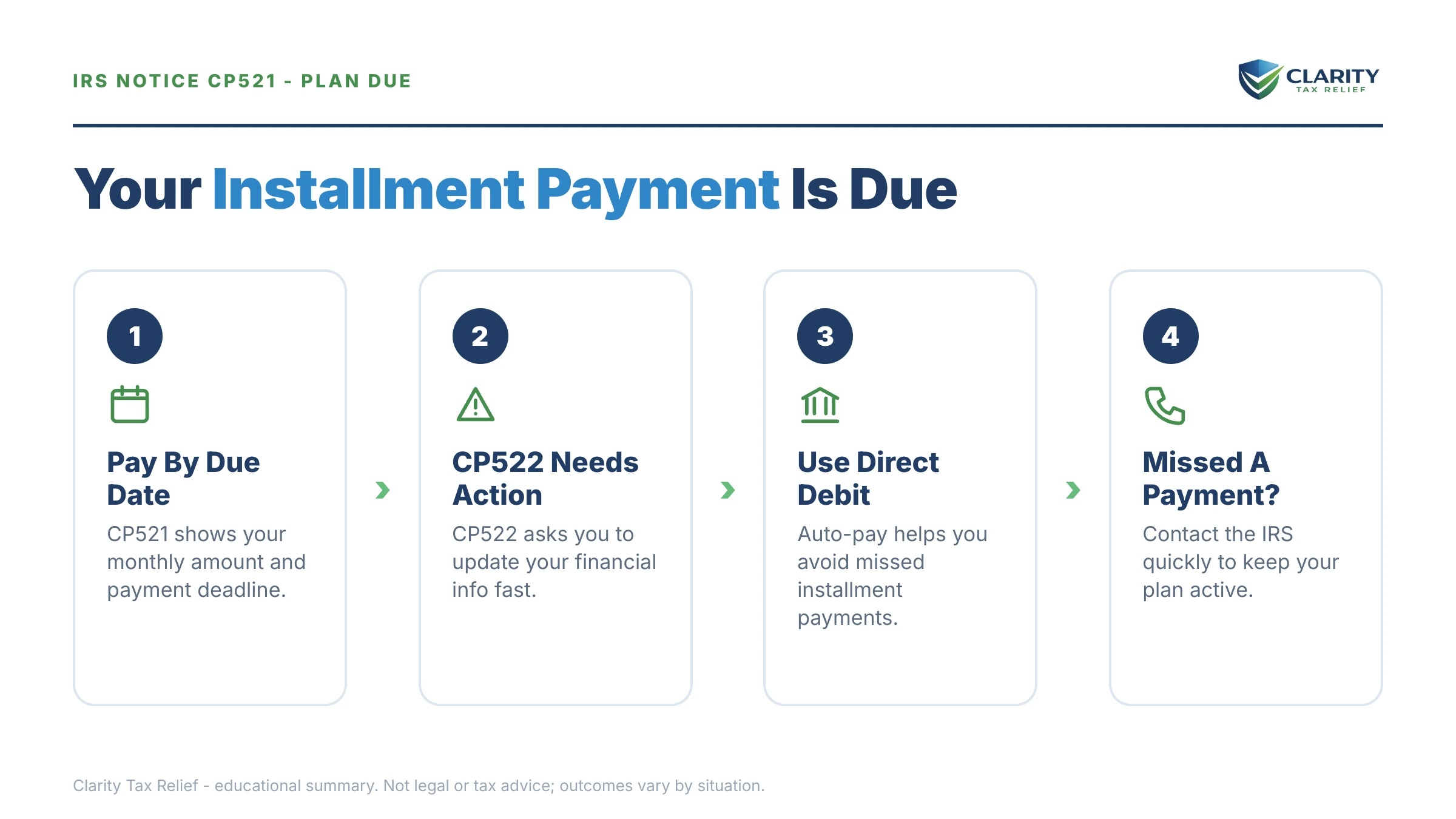

The short answer: a CP521 notice is the IRS's monthly reminder that a payment is due on your installment agreement. It is not a new debt and not a default — it means your payment plan is active. Pay the amount shown by the printed due date and nothing else happens.

You set the payment plan up months ago and thought the IRS letters were finally behind you — then another envelope shows up and your chest tightens before you even open it. Take a breath: a CP521 is the statement for the plan you already have, not the IRS coming back for more. The only thing it asks of you is the same monthly payment you already agreed to.

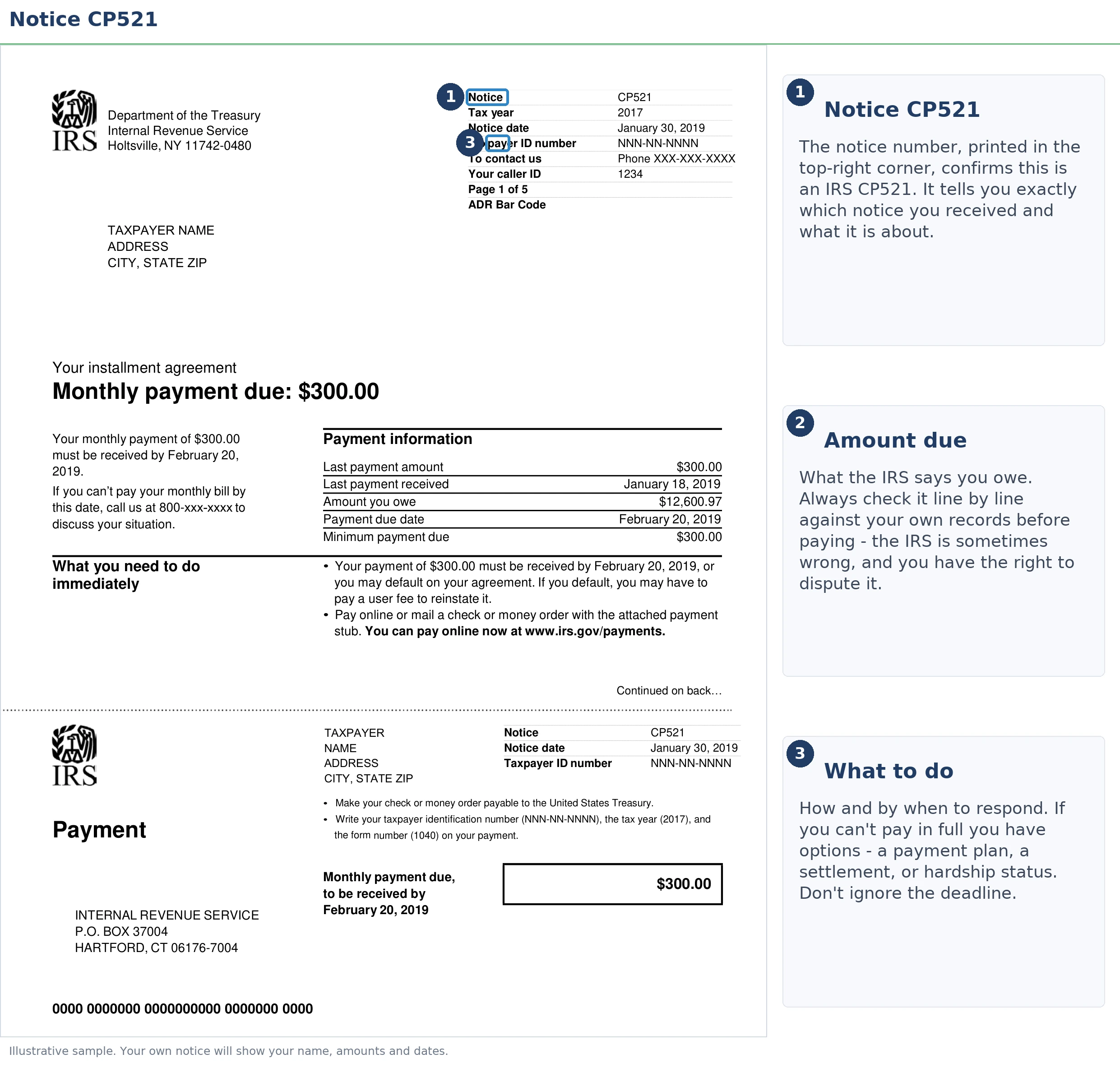

The image below shows exactly what a CP521 looks like and where to find the three numbers that matter — the amount due, the due date, and your remaining balance.

⏱ Your deadline: the payment due date printed on your CP521. There's no separate response window — this notice IS your bill. Miss that date and the default sequence can begin, while interest and a monthly late-payment penalty keep accruing on the unpaid balance either way.

Why you got a CP521 notice

A CP521 is the IRS's monthly billing statement for an active installment agreement — proof your payment plan is working, not a sign it's in trouble. The IRS sends one before each due date to taxpayers who pay by check, money order, or manual online payment.

The notice shows the tax years covered, this month's payment, the due date, and your remaining balance including penalties and interest accrued since the last statement. If you pay by direct debit, you generally won't receive monthly CP521s at all — the payments draft automatically, so getting one on a direct-debit plan is a flag worth checking (see the FAQ below).

If you're not on a payment plan and this letter makes no sense, someone may have set one up on a joint or business account — start with why you got a letter from the IRS to decode what's on file, then call the number printed on the notice.

CP521 vs. CP522 vs. CP523: know which letter you're holding

Three payment-plan notices look similar and mean very different things. A CP521 asks for money you already agreed to pay; a CP522 asks for paperwork; a CP523 threatens to end the agreement entirely.

| Notice | What it means | What to do |

|---|---|---|

| CP521 | Monthly reminder — a payment is due on your active installment agreement | Pay by the printed due date; no other response needed |

| CP522 | Request for updated financial information so the IRS can review your agreement's terms | Respond by the deadline — silence can default the plan even if you never miss a payment |

| CP523 | Notice of Intent to Terminate a defaulted installment agreement | Cure the default or appeal by the date printed on the notice |

| LT11 / Letter 1058 | Final notice of intent to levy — sent after an agreement is gone and the balance is back in collection | Act within 30 days to use your Collection Due Process rights before levy |

CP522s deserve special mention because they blindside people. If you're on a partial-pay installment agreement, the IRS periodically re-checks your finances — and the review can raise your payment if your income has grown. A CP522 is the one payment-plan letter that requires an actual written response, not just a check.

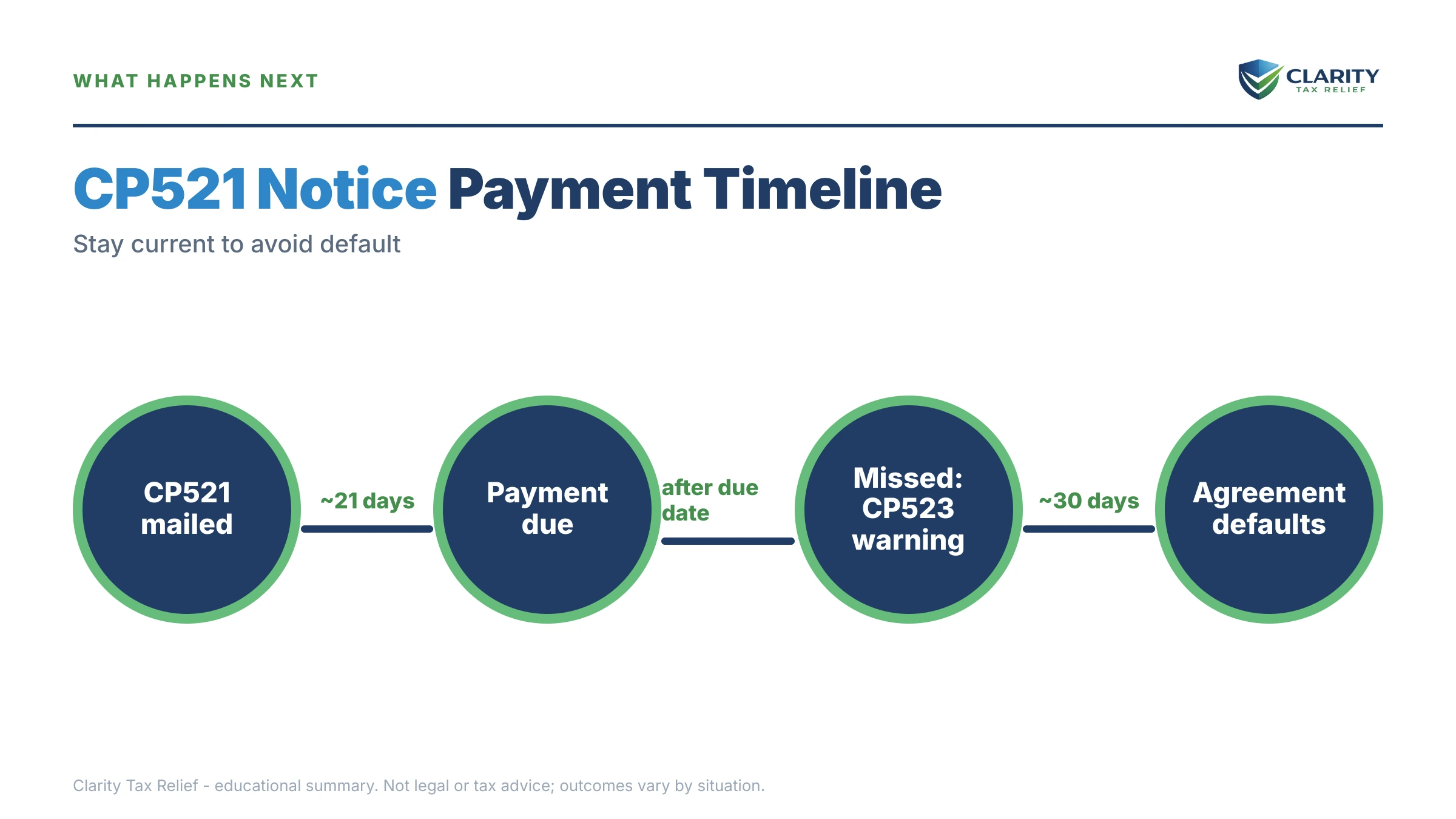

What happens if you stop paying (or ignore a CP521)

Ignoring a CP521 doesn't just cost a late fee — a missed installment payment starts a default sequence that can put your entire balance back into active collection. The sequence runs on the IRS's automated systems, which kept issuing defaults and levies right through the 2025 staffing cuts.

- Missed payment. The account is flagged. There's often a short informal window to catch up — here's what happens after a missed IRS payment plan payment — but interest never pauses.

- CP523 — Notice of Intent to Terminate. The IRS states it will end the agreement unless you cure the default by the deadline printed on the notice. You also get appeal rights at this stage. Full breakdown in our CP523 notice guide.

- Termination. The agreement is gone. The entire remaining balance — not just the missed months — is due and back in the collection stream. Getting it restarted means a reinstatement fee and, often, a new financial review; see how to reinstate an IRS payment plan.

- Enforcement. After the required final notices, the IRS can levy wages and bank accounts for the full balance. And if you owe more than $66,000 — the 2026 threshold — a terminated agreement removes the protection that kept your debt off the State Department's list; see passport revocation for tax debt.

Missed payments aren't the only trigger. An installment agreement also defaults if you file a new return with a balance you don't pay, skip filing a required return, or bounce a payment. For self-employed and gig readers, that's the trap: fall behind on quarterly estimated taxes, owe at filing, and the agreement you fought for defaults even though you never missed a monthly payment.

On a payment plan and something's off?

Maybe the CP521 balance won't move, the payment no longer fits your budget, or you've already missed one. Get your CP521 — and the agreement behind it — reviewed free before your next due date. An experienced tax professional will tell you whether restructuring, hardship status, or a settlement route fits your numbers.

Can't afford the payment on your CP521? Your real options

An installment agreement payment isn't fixed for life — the IRS can restructure, pause, or replace a plan that no longer matches your finances. Every one of these works better requested before a default than after one.

| Option | Who it fits | Trade-off |

|---|---|---|

| Lower your IRS monthly payment | Income dropped or necessary expenses rose since the plan was set; larger balances may require updated financials | Plan runs longer, so more total interest; a modification fee can apply |

| Switch to a direct debit installment agreement | Anyone with a bank account who keeps forgetting or mailing late | None meaningful — it ends the CP521s, cuts default risk, and carries lower fees |

| Partial-pay installment agreement | You can pay something monthly but can't full-pay before the 10-year collection statute runs out | Periodic financial reviews (CP522s), and a federal tax lien is likely |

| Currently Not Collectible status | Making any payment would leave you unable to cover basic living expenses per IRS standards | Collection pauses, but the debt, interest, and annual refund offsets continue |

| Offer in Compromise | Your assets and future income genuinely can't cover the debt — the IRS accepted roughly 1 in 5 offers in FY2024, so the math must actually work | $205 application fee (waived for low-income applicants), months of review, strict compliance terms afterward |

| Pay off the plan early | You got a windfall — a refund, a sale, an inheritance | None — there's no prepayment penalty, and interest stops the day the balance hits zero |

Why your CP521 balance barely moves: the math

Your CP521 balance keeps growing between payments because interest and a reduced failure-to-pay penalty accrue on the unpaid balance every month — and each payment covers that accrual before it touches principal. On a large balance, the early payments feel like running on a treadmill. You can estimate your own accrual with our Penalty & Interest Calculator.

Here's a clearly hypothetical example. Say you're a gig worker who just caught up three unfiled years and owes $92,700 combined. Because that's over $50,000, the IRS required financial disclosure — typically Form 433-F — and set your payment at $1,350 a month based on what your budget shows.

Using a 7% annual interest rate purely for illustration (the real rate adjusts quarterly), interest runs about $92,700 × 7% ÷ 12 ≈ $541 a month. The failure-to-pay penalty, which for most taxpayers drops to roughly 0.25% per month while an approved installment agreement is in effect, adds about $232. That's ~$773 of accrual — so of your $1,350 payment, only about $577 actually reduces the debt at first. Roughly 43 cents of every dollar hits principal.

Two things speed this up. First, extra payments in any amount go straight at the balance — even $200 more a month materially shortens the plan. Second, the IRS keeps your federal refund every year and applies it to the balance; it stings in April, but it's principal-only money. Details in will the IRS take my refund on a payment plan.

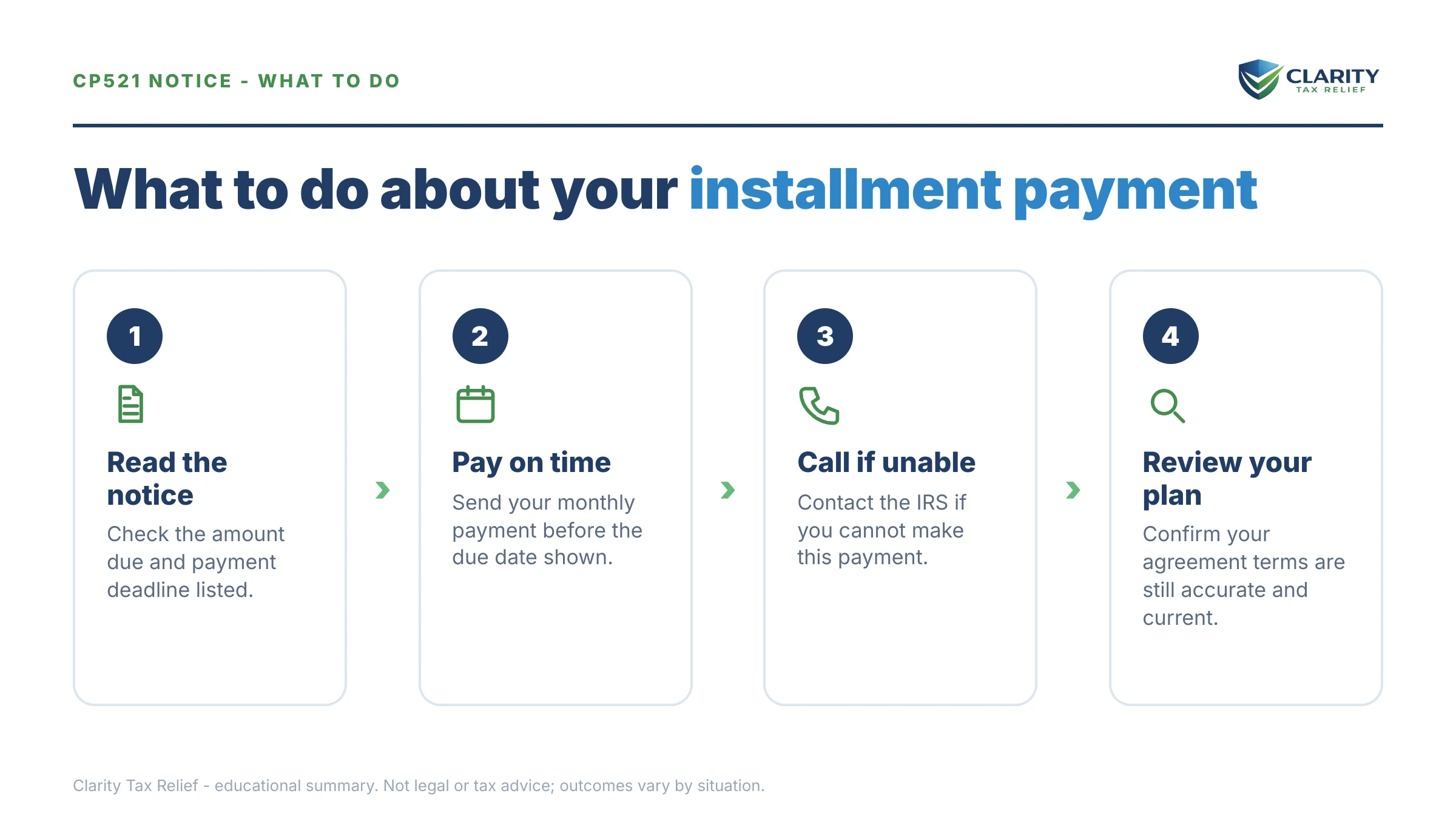

How to respond to a CP521, step by step

A CP521 needs five minutes, not a strategy session — as long as the numbers check out.

- Verify the notice matches your agreement — check the tax year, amount due, and remaining balance against your IRS online account and your Form 433-D or acceptance letter.

- Pay by the due date printed on the notice — pay online at IRS.gov/payments or mail the payment stub in the envelope provided — online posts faster and can't get lost.

- Compare the remaining balance to last month's — if it barely moved, that's interest and penalty accrual, not an error — the math section above shows exactly why.

- Switch to direct debit if you're mailing checks — automatic drafts remove the missed-payment and lost-mail risk that defaults agreements, and they end the monthly CP521s.

- Call before you miss a payment, never after — if the amount no longer fits your budget, restructuring an active agreement is far easier than reinstating a terminated one.

When you can handle a CP521 yourself

Most people can handle a routine CP521 with no professional help at all — it's a bill for a plan you already negotiated. If the numbers match your records and the payment fits your budget, pay it, consider switching to direct debit, and move on with your life.

Experienced help changes outcomes in a narrower set of situations: you've already received a CP523 or missed multiple payments; a new year's balance is about to default the agreement; the payment was set before your income dropped and you can't sustain it; or the balance is large enough — like the $92,700 example above — that a partial-pay agreement, hardship status, or an Offer in Compromise might resolve it for less than grinding out the full payoff. In those cases, the order and timing of the moves matter, and a review before your next due date costs nothing.

Terms on your CP521, decoded

- Installment agreement: your formal monthly payment plan with the IRS — the contract this notice is billing against.

- Default: breaking the agreement's terms — a missed payment, a new unpaid balance, an unfiled return, or a bounced payment.

- Reinstatement: restarting a terminated agreement, which involves a fee and sometimes a fresh financial review.

- Direct debit installment agreement: a plan paid by automatic bank draft — no monthly CP521s and far less default risk.

- Refund offset: the IRS keeping your federal tax refund and applying it to your remaining balance, on top of your monthly payment.

- CSED: the Collection Statute Expiration Date — the end of the IRS's 10-year window to collect, which generally keeps running while you make plan payments.

For the official versions, see the IRS's own Understanding your CP521 notice page and its overview of payment plans and installment agreements.

CP521 questions, answered

Is a CP521 notice bad?

No — a CP521 is a routine monthly reminder that your installment agreement payment is due, and getting one means your payment plan is still active and in good standing. It becomes a problem only if you miss the due date printed on it. The notice to worry about is a CP523, which means the IRS intends to terminate your agreement.

Do I need to respond to a CP521 notice?

No written response is needed — you just make the payment shown by the due date printed on the notice. If the amount or tax year looks wrong, or a payment you already made isn't reflected, call the number on the notice with your confirmation in hand before the due date. Never skip the payment while you sort out a discrepancy.

Why did I get a CP521 if I'm on direct debit?

Taxpayers on direct debit installment agreements usually don't receive monthly CP521 reminders because payments draft automatically. If you got one anyway, check that your last draft actually went through — a returned or failed bank payment can knock an agreement off autopilot. Confirm your bank details in your IRS online account and call the number on the notice if a draft failed.

What happens if I miss the payment on my CP521?

One missed payment doesn't instantly terminate your agreement, but it starts the default process. The IRS typically sends a CP523 Notice of Intent to Terminate, and if you don't cure the missed payment by the deadline printed on it, the agreement terminates and the full balance returns to active collection. Reinstating after termination usually means a reinstatement fee and sometimes a fresh financial review.

Why is my CP521 balance barely going down?

Because interest and a reduced failure-to-pay penalty keep accruing on the unpaid balance while you're on the plan, and they're paid first. On a large balance, a big share of each monthly payment covers that month's accrual before touching principal. The fix is paying more than the minimum when you can — extra payments go straight at the balance and shorten the plan.

Can I lower the monthly payment on my CP521?

Yes — installment agreements can be restructured if your income drops or expenses rise. Depending on your balance, the IRS may ask for updated financials on Form 433-F to set the new amount, and a modification fee can apply. Ask before you miss a payment: lowering an active agreement is far simpler than reinstating a terminated one.

What is a CP522 notice?

A CP522 asks you to provide updated financial information so the IRS can review your installment agreement terms — it's common on partial-pay agreements, which get reviewed periodically. Unlike a CP521, a CP522 requires an actual response by its deadline. Ignore it and your agreement can default even if you never missed a payment; respond, and be aware the review can raise (or lower) your monthly amount.

Will the IRS keep my tax refund while I'm on a payment plan?

Yes. While an installment agreement is active, the IRS applies your federal tax refund to the remaining balance every year until it's paid off. The offset does not count as your monthly payment — you still owe that month's amount on schedule. Some taxpayers adjust withholding or estimates so less is refunded and more stays in their monthly budget.

Your next 24 hours

- Find the due date and amount due on your CP521 — they're in the box near the top — and put the date in your phone with a reminder three days ahead.

- Gather your agreement paperwork — the acceptance letter or Form 433-D, last month's CP521 if you have it, and your last few months of income if the payment no longer fits your budget.

- If the payment doesn't fit — or the balance never seems to shrink — get a free case review before your next due date at the 2-minute form or (888) 825-7779. Restructuring while your agreement is still in good standing keeps every option on the table; interest and penalties accrue either way, so waiting only costs you.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.