IRS Payment Plans

Lower My IRS Monthly Payment: How to Reduce an Existing IRS Payment Plan (2026)

The short answer: yes — you can lower an existing IRS monthly payment. If you owe under $50,000 and the new amount still pays the balance within 72 months, you can change it yourself through the IRS Online Payment Agreement tool, usually with immediate approval. Bigger reductions require Form 433-F financial disclosure.

The direct debit hits your checking account this week, and for the first time it's going to hurt. You agreed to that number back when the budget looked different — and the IRS never calls to ask whether it still fits. If you've been searching "lower my IRS monthly payment," here's the honest map: what you can change yourself today, and where the IRS demands proof of your finances first.

⏱ The real clock: there's no application deadline to lower an IRS payment plan — but interest and a monthly late-payment penalty accrue on your balance the entire time, and one skipped payment can start the default sequence. Change the payment before you miss one, not after.

Why your IRS monthly payment is probably higher than it has to be

Most IRS payment plans are set at whatever number the taxpayer offered on the day they applied — the IRS accepts your figure if it clears the balance in time, and it never revisits that figure when your income drops.

Three things put people in this spot. First, you overcommitted at setup: scared, on the phone or the online tool, you picked an aggressive number to make the problem feel handled. Second, life changed — hours got cut, a second income stopped, rent or childcare went up. Third, the balance itself changed: penalties were abated, or a tax refund was applied to the debt, and the payment that made sense against the old balance now overshoots the new one.

Here's the number the IRS never volunteers: for balances up to $50,000, the practical minimum payment is roughly your total balance divided by 72 months, plus a cushion for accruing interest. Plenty of people are paying double or triple that floor without knowing a floor exists.

One more thing worth knowing in 2026: the IRS lost roughly 27% of its workforce in 2025. Nobody at the agency is reviewing accounts to suggest a lower payment — but the automated systems that flag missed payments and issue default notices are fully staffed. The change has to come from you.

What happens if you skip payments instead of lowering them

Skipping installment agreement payments doesn't lower them — it starts the default sequence that puts levies back on the table.

- A missed payment posts. Interest and the late-payment penalty keep accruing, and the automated system flags your account. One slip isn't always fatal — here's what actually happens after a missed IRS payment plan payment — but the flag is set.

- CP523 — Notice of Intent to Terminate. The IRS mails a CP523 notice stating your agreement will be terminated unless you cure the default within the window printed on the notice (typically about 30 days).

- The agreement terminates. The protection your plan gave you is gone. Getting it back means fees, a formal request, and possibly a fresh financial review — the full process to reinstate an IRS payment plan after default.

- Enforcement resumes. Once termination is final, the IRS can move toward wage garnishment and bank levies again — the exact machinery your plan existed to hold off. Defaulting to avoid a $300 payment can cost you an entire paycheck to a levy later.

Is next month's payment about to bounce?

Don't let one missed debit unravel your agreement. An experienced tax professional will review your plan free, run the numbers, and tell you exactly how low the IRS will realistically go — before the default sequence ever starts.

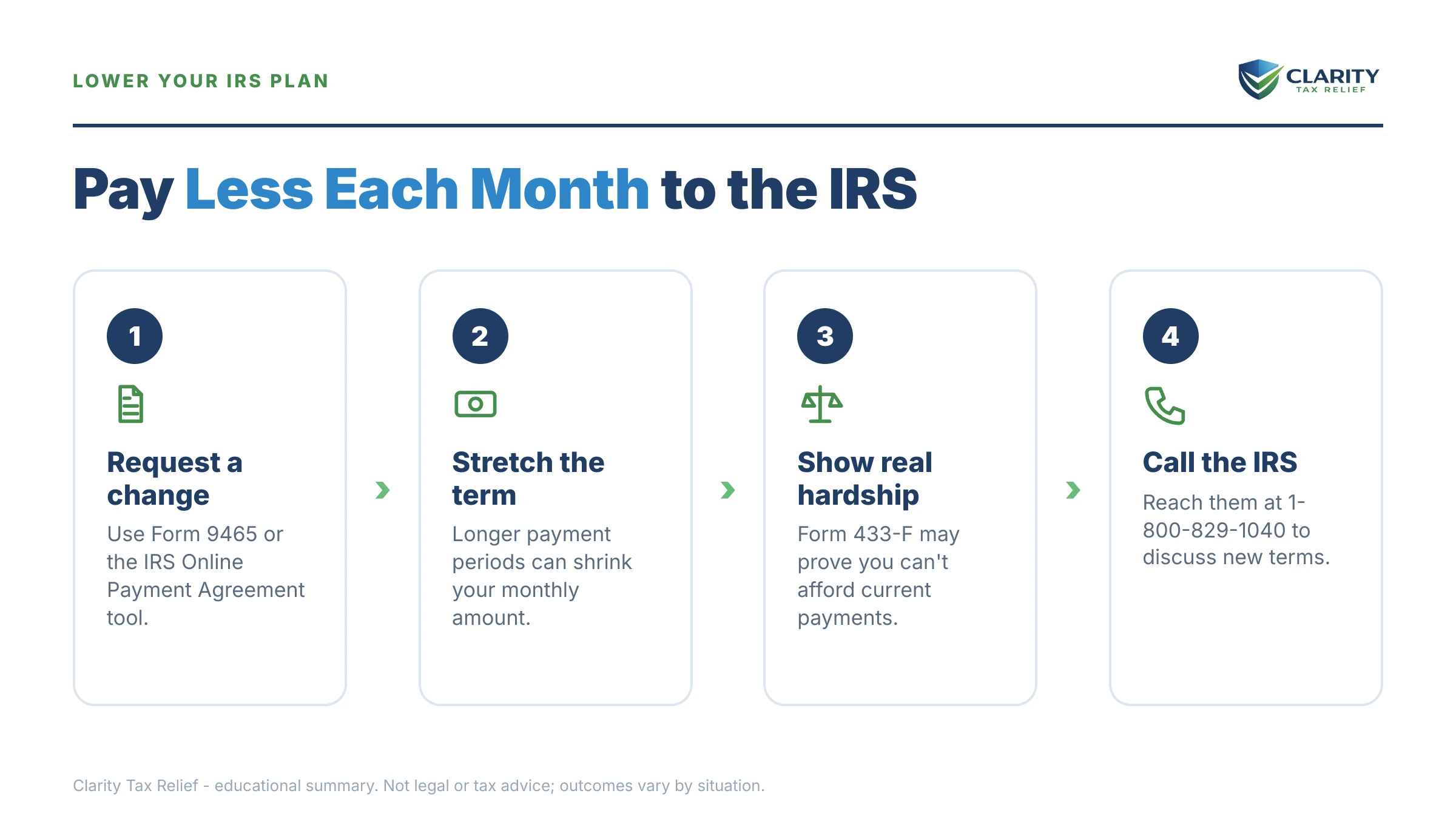

"Lower my IRS monthly payment": your five real options

There are five real ways to reduce an IRS monthly payment, and the first one takes about 15 minutes online. Which door you use depends on how much you owe and how far below the 72-month floor you need to go.

| Option | Best when | What the IRS requires |

|---|---|---|

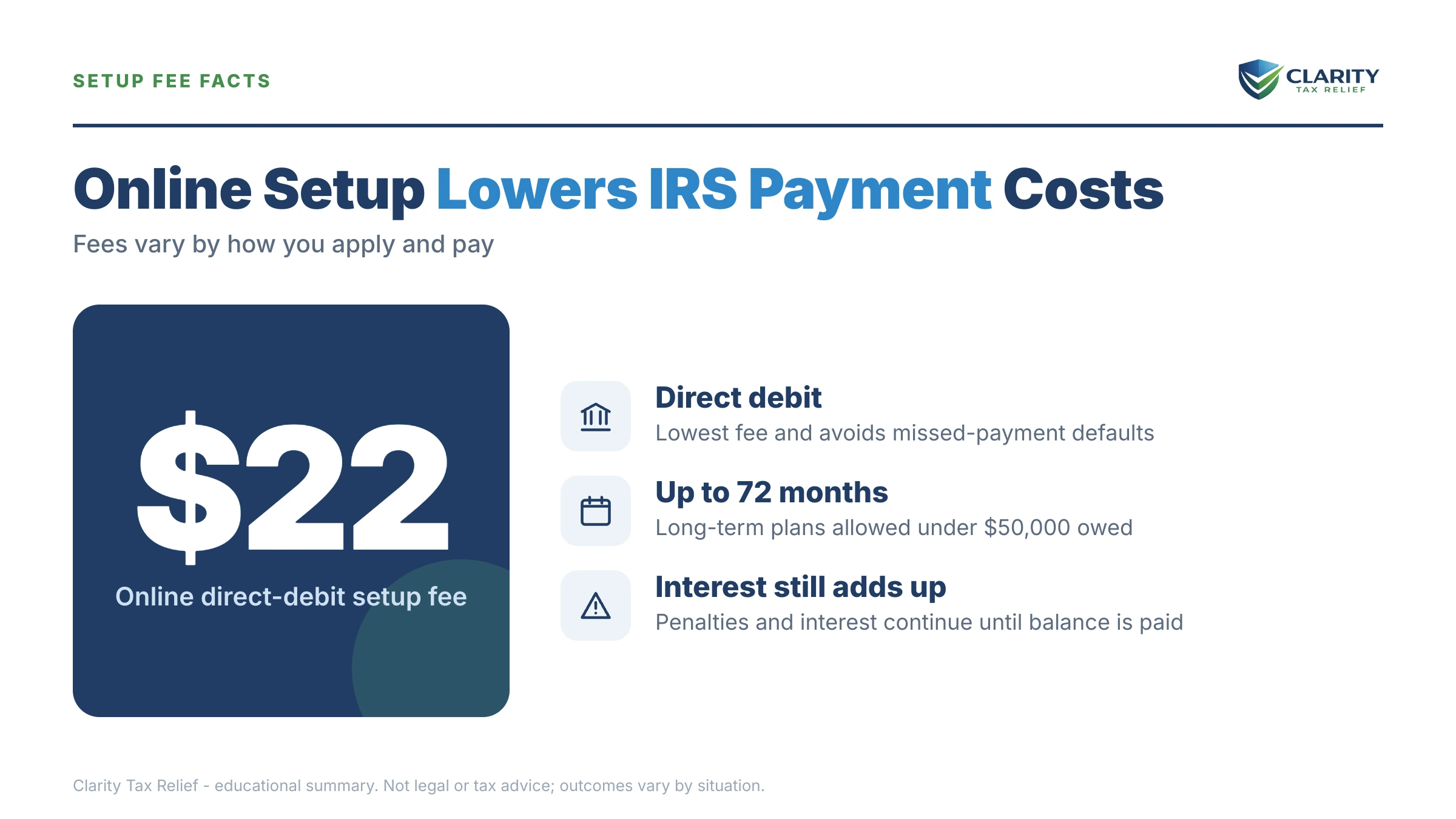

| Revise online (Online Payment Agreement) | Balance ≤ $50,000 and the new payment still clears it within 72 months | No financial forms; small revision fee; all returns filed |

| Restructure by phone with Form 433-F | The tool rejects your number, or you owe over $50,000 | Collection Information Statement (income, expenses, assets) |

| Partial-pay installment agreement (PPIA) | You can pay something, but not enough to ever pay in full before the 10-year statute expires | Full 433-F disclosure; periodic financial reviews |

| Currently Not Collectible (CNC) | Any payment would leave you unable to cover basic living expenses | Hardship-level financials; refunds still offset |

| Shrink the balance itself (penalty relief) | Clean compliance history or a reasonable-cause event behind the penalties | An abatement request — or nothing, once AEP is automatic |

1. Revise the payment yourself online

The Online Payment Agreement tool lets you change your monthly amount and your monthly due date on an existing plan. If your balance is $50,000 or less and the new amount full-pays within 72 months, approval is typically immediate — no human, no financial forms. This is the door most people should try first, and most never learn exists.

2. Restructure with Form 433-F financials

When your affordable number falls below the 72-month floor — or your balance is over $50,000 — the IRS wants proof before agreeing. That proof is a Collection Information Statement, usually Form 433-F. The IRS then sets the payment by formula: your monthly income minus its allowable living expense standards. How your expenses are documented drives the result, which is why this tier rewards preparation. Above the streamlined threshold the rules shift again — see IRS payment plans over $50,000.

3. Convert to a partial-pay installment agreement

A partial payment installment agreement is the option almost no notice mentions: a monthly payment based on what you can genuinely afford, even if it will never pay the debt in full before the 10-year collection statute runs out. Whatever remains uncollected when that statute expires generally falls away — though the IRS reviews PPIAs periodically and can raise the payment if your finances improve.

4. Switch to Currently Not Collectible status

If the honest answer is that you can't afford any payment, the goal isn't a lower payment — it's Currently Not Collectible status. Collection pauses entirely while you're in hardship. The debt remains, interest keeps accruing, and the IRS keeps your refunds, but no money leaves your account each month.

5. Shrink the balance the payment is built on

A lower balance supports a lower payment. If penalties are inflating what you owe and your prior three years were clean, first-time penalty abatement can remove them — and starting summer 2026, the new Automatic Exemption from Penalty (AEP) grants that relief automatically for qualifying taxpayers, no request needed. Interest itself is harder to remove; here's the honest answer on whether IRS interest can be waived. And if what you really need is a full reset — settlement, hardship status, the whole menu — start with our guide to how to settle tax debt yourself, then come back here for the payment-plan mechanics.

| Method | Typical cost | Financial disclosure | Time to take effect |

|---|---|---|---|

| Online revision (OPA) | Small revision fee — lowest online, reduced or waived for low-income taxpayers | None | Often same day |

| Phone restructure with 433-F | Restructuring fee, plus long hold times in 2026 | Form 433-F | Days to weeks |

| Partial-pay agreement | Setup/restructure fee; payment reviewed periodically | Full 433-F, verified | Weeks |

| Currently Not Collectible | No fee; interest still accrues and refunds are kept | Hardship financials | Weeks |

| Penalty abatement / AEP | Free to request; reduces the balance itself | None (compliance history) | Weeks; AEP automatic from summer 2026 |

The 72-month math: lowering an $8,900 IRS payment plan

A worked example makes the floor concrete. Say you and your spouse file jointly and owe $8,900, and last spring — when both of you were working full hours — you set up a plan at $300 a month. Now one paycheck has shrunk and $300 doesn't fit.

Run the floor: $8,900 ÷ 72 = about $124 a month. Because interest keeps accruing during the plan (though the failure-to-pay penalty is cut in half, from 0.5% to 0.25% per month, while an installment agreement is in effect), you want headroom above the bare floor. Propose $150 a month: $150 × 72 = $10,800, which comfortably covers the $8,900 principal plus what accrues along the way. That's a change the online tool will typically approve on the spot — no financial forms, because the new amount still full-pays within 72 months.

Two nuances for a couple in exactly this position. First, because you owe under $10,000, you may have heard of the guaranteed installment agreement — but that program requires full payment within three years, which at $8,900 works out to roughly $247 a month. It's the streamlined 72-month track, not the guaranteed one, that lets you go low. Second, understand the trade: at $300 a month you'd have been done in roughly two and a half years; at $150 you'll be in the plan closer to five, paying meaningfully more interest overall. You can estimate the accrual at different payment levels with our IRS Penalty & Interest Calculator.

One place the lower payment works for you: mortgage underwriting. Lenders count your IRS payment in your debt-to-income ratio, so a $150 obligation reads very differently from a $300 one — details in our guide to buying a house while owing the IRS.

How to lower your IRS monthly payment, step by step

- Pull your current agreement terms. Log into your IRS online account or grab your latest CP521 statement. Confirm the exact balance, your current monthly amount, and how many months remain.

- Run the 72-month math. Divide your total balance by 72. If the payment you can actually afford is at or above that number — with a cushion for accruing interest — you can likely revise the plan online without financial forms.

- Revise the amount online. Use the IRS Online Payment Agreement tool to propose the new monthly amount, and a new due date if you need one. Approval is typically immediate when the math works.

- Prepare Form 433-F if the tool says no. If your number is below the streamlined floor or your balance is over $50,000, complete a Collection Information Statement listing income, expenses, and assets, then call the IRS to propose the restructured payment.

- Keep paying the old amount until the change is confirmed. A pending request is not an approved one. Keep your current payments going until the IRS confirms the new terms in writing, so you never trigger the default sequence.

When you can change your IRS payment plan yourself — and when help changes the outcome

You can lower your own IRS payment online, in one sitting, if you owe under $50,000 and your new amount still clears the balance within 72 months. That describes most people on this page, including the $8,900 couple above — no professional needed. The change happens at the IRS's Online Payment Agreement application, and the general rules live on the IRS payment plans page.

Experienced help earns its fee in the other situations: a CP523 already in hand (the cure window is short and the stakes are your levy protection); balances over $50,000, where the payment is set by expense documentation, not negotiation charm; partial-pay agreements, where the 433-F math determines whether part of the debt outlives the statute; business or payroll debt sitting behind the plan; and any unfiled years — the IRS won't restructure an agreement while returns are missing. One caution either way: know your rights before signing anything that extends the collection statute, because a longer statute means more years the IRS can collect.

Terms on your agreement, decoded

- Streamlined installment agreement — a plan of $50,000 or less that full-pays within 72 months, approved without detailed financial disclosure.

- Guaranteed installment agreement — the by-right plan for balances of $10,000 or less, which requires full payment within three years.

- Partial-pay installment agreement (PPIA) — a payment set by ability to pay that won't fully retire the debt before the collection statute expires.

- CSED — the Collection Statute Expiration Date: 10 years from assessment, after which the IRS generally can't collect (certain events pause the clock).

- Form 433-F — the Collection Information Statement the IRS uses to verify income, expenses, and assets before accepting a below-floor payment. (Form 9465 is its cousin — the form used to request a plan in the first place.)

- CP521 / CP523 — the CP521 is your routine monthly payment reminder; the CP523 is the intent-to-terminate notice that follows missed payments.

Lower-my-payment questions, answered

Can I lower my IRS installment agreement payment without calling the IRS?

Yes. If your balance is under $50,000 and your new amount still pays everything off within 72 months, you can change the payment yourself through the IRS Online Payment Agreement tool — no phone call, no financial forms. If the tool rejects your new amount, that's the signal the IRS wants Form 433-F financials before agreeing to go lower.

What is the minimum monthly payment the IRS will accept?

For balances up to $50,000, the practical floor is your balance divided by 72 months, plus enough to cover accruing interest and penalties. Below that number, the IRS requires financial disclosure and sets the payment based on your income minus allowable living expenses. Through a partial-pay agreement, the accepted payment can fall below what full payoff would require.

How much does it cost to change my IRS payment plan?

The IRS charges a modest fee to revise or restructure an existing installment agreement — lowest when you make the change online, and reduced or waived for low-income taxpayers. The bigger cost is time: a lower payment means more months of accruing interest, so you pay more in total before the balance clears.

Will lowering my payment extend how long I owe the IRS?

Yes — a lower payment stretches the payoff over more months, and interest plus a reduced late-payment penalty keep accruing the whole time. What does not change is the 10-year collection statute: the IRS still has the same window to collect, and lowering your payment doesn't restart it. Certain events like a pending offer in compromise or bankruptcy can pause that clock.

Can I lower my payment if I owe more than $50,000?

Yes, but not online. Above $50,000, the IRS requires a Collection Information Statement — usually Form 433-F, sometimes the longer Form 433-A — before changing your terms. The payment is then set by formula: your monthly income minus the IRS's allowable living expense standards. Experienced help matters most in exactly this range, because how your expenses are documented drives the number.

What if I can't afford any monthly payment at all?

Ask for Currently Not Collectible status instead of a lower payment. If your financials show that paying anything would leave you unable to cover basic living expenses, the IRS pauses collection entirely — no monthly payment, no levies. The debt remains and keeps growing with interest, and the IRS keeps any tax refunds, but you get breathing room until your situation improves.

What happens if I just stop paying instead of lowering the payment?

Your agreement heads toward default. The IRS typically sends a CP523 Notice of Intent to Terminate, and if you don't cure the missed payments within the window printed on that notice, the agreement ends and full enforcement — including wage and bank levies — comes back on the table. Lowering the payment first costs a small fee; defaulting costs your protection.

Can I change the date my IRS payment is due each month?

Yes. The Online Payment Agreement tool lets you change your monthly due date as well as the amount, which helps if your payment currently hits before your paycheck lands. If you pay by direct debit, allow time for the change to process before the next scheduled withdrawal, and keep the old payment funded until the IRS confirms the new terms.

Your next 24 hours

- Find your current terms. Pull your latest CP521 statement or log into your IRS online account and write down three numbers: total balance, monthly payment, and payment due date.

- Gather what a 433-F would ask. Two recent pay stubs for each spouse, a one-page list of monthly household expenses, and last year's return — even if you end up revising online, you'll know instantly whether your target number is realistic.

- Get the plan reviewed free. Interest accrues on your balance every month you overpay elsewhere and underpay here. Call (888) 825-7779 or use the 2-minute form, and an experienced tax professional will tell you the lowest payment the IRS will realistically accept — before your next debit hits.

If the IRS terminates an agreement in error or you're stuck in processing limbo, the independent Taxpayer Advocate Service can also intervene at no cost.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.