Tax Deadlines & Payments

Pay IRS Before End of Year: What December 31 Actually Changes (2026)

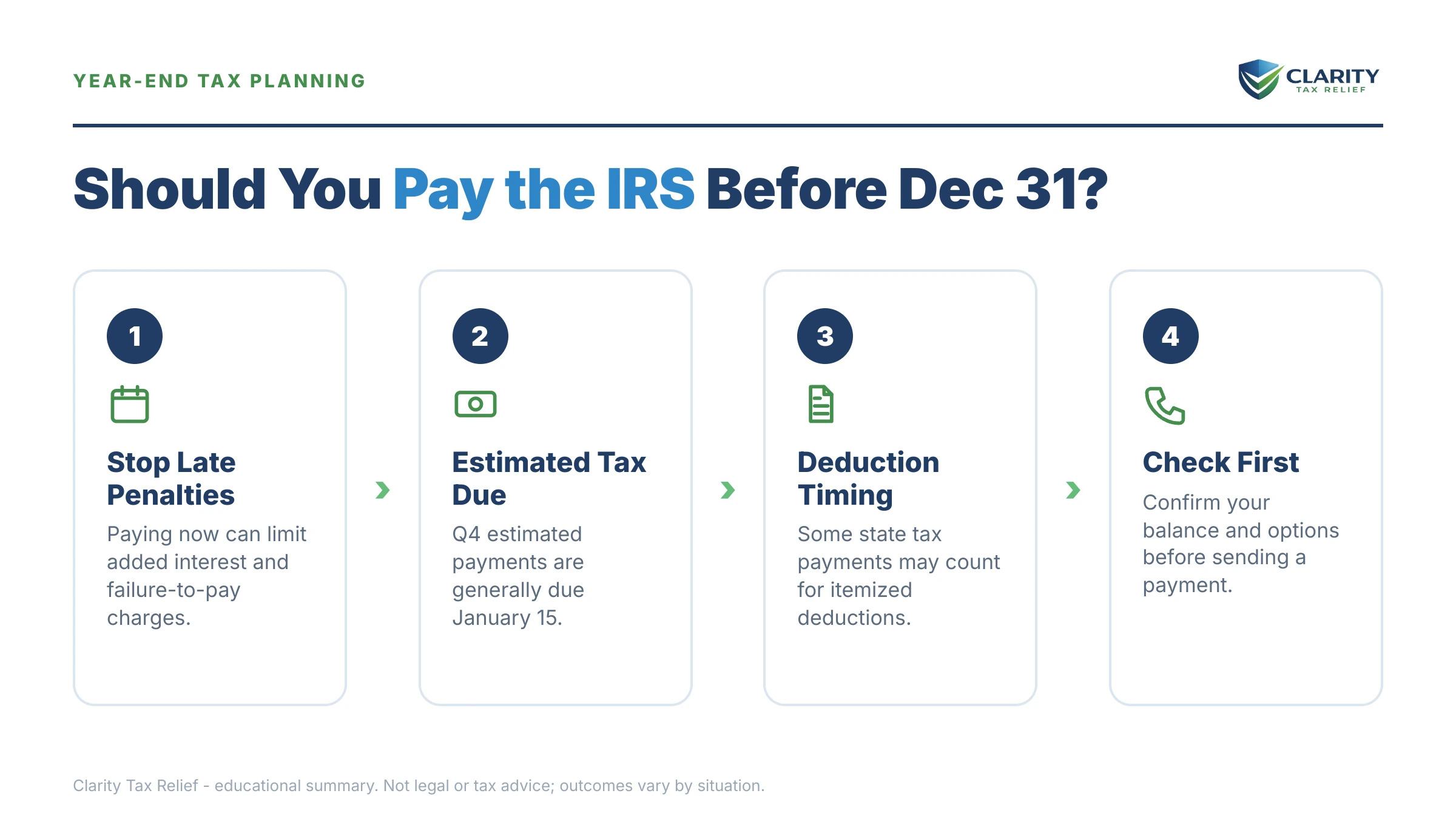

The short answer: usually, yes — pay the IRS before end of year if the balance is already assessed, because the 0.5%-per-month penalty and daily interest never pause. But your fourth-quarter estimated payment isn't due until January 15, and December 31 only controls withholding timing and state-tax deduction timing.

It's the last week of December. You and your spouse have run the rough numbers — one W-2 paycheck, a year of side income with no withholding — and you know money is going to the IRS one way or another. The only question is whether it leaves your account now or in April.

That's a real decision with real dollars attached, and the answer is different for each kind of balance you might be holding. Here's the map: which year-end dates actually matter, what waiting costs, and what to do if you can't pay at all.

⏱ Two real deadlines: December 31 is the last day a withholding change or a deductible state tax payment counts inside the 2026 tax year. January 15, 2027 is the due date for your fourth-quarter federal estimated payment. And on any balance the IRS has already billed you for, there is no future deadline — the failure-to-pay penalty and daily interest are accruing right now.

Should you pay the IRS before end of year?

Paying the IRS before end of year saves you money in exactly three situations: an assessed balance accruing penalties, a December withholding adjustment, and a state tax payment you plan to itemize. Everything else can wait for its actual deadline without costing you a dime extra.

Here's the part that surprises most people: December 31 is not the deadline for your fourth-quarter federal estimated payment — January 15 is. If you're a married couple squaring up self-employment or investment income for Q4, mailing the IRS money on December 29 instead of January 14 earns you nothing on the federal side.

What December 31 does control:

- Withholding timing. Tax withheld from a paycheck by December 31 counts for this tax year — and the IRS treats withholding as if it were paid evenly across all four quarters, no matter when it came out. A December W-4 change or bonus withholding can retroactively shrink penalties for earlier quarters.

- State deduction timing. If you itemize, a state income tax payment made by December 31 is deductible on this year's federal return (subject to the cap on state and local tax deductions). The same payment made January 2 slides into next year.

- The size of an assessed balance. If the IRS has already billed you for a prior year, every month you wait adds penalty and interest. There's no deadline to beat — the meter is simply running.

If you're comparing payment methods rather than payment timing — Direct Pay vs. debit vs. check — see the full breakdown of the best way to pay the IRS.

The three year-end clocks: December 31, January 15, April 15

Each year-end tax date controls a different balance, and mixing them up is how people either drain savings for nothing or eat a penalty they could have avoided. This table is the whole decision in one place:

| Date | What it controls | Who it matters to |

|---|---|---|

| December 31 | Last day withholding counts for the tax year; last day a state tax payment is deductible this year if you itemize | Anyone adjusting a W-4 or bonus withholding; itemizers making state estimated payments |

| January 15 | Fourth-quarter federal estimated payment due (Form 1040-ES) | Self-employed, 1099, and investment income without withholding |

| Late January | Filing season opens — any refund you're owed gets applied to an assessed back balance automatically | Anyone carrying an unpaid prior-year balance |

| April 15 | Return and full payment due; the 0.5%/month failure-to-pay penalty starts on any unpaid new-year balance | Everyone |

One more clock hides inside January 15: if you skip the Q4 estimate and settle up in April instead, the underpayment penalty on that quarter runs from January 15 to the day you actually pay. The full calendar is in our guide to the quarterly estimated tax deadlines for 2026.

What waiting until April actually costs

On an assessed IRS balance, waiting costs 0.5% of the balance every month in failure-to-pay penalty (capped at 25% total), plus interest that compounds daily on the whole amount — penalties included. The current rate resets quarterly; see the IRS interest rates for 2026.

And an assessed balance doesn't just cost money — it moves. The IRS collection system is automated, and in 2026 it's running with roughly 27% fewer employees than a year ago. Humans are harder to reach; the notice machine never slowed down. If you carry the balance into the new year, this is the sequence already queued up:

- The balance grows silently — penalty posts monthly, interest compounds daily, no letter required.

- Refund offset — when filing season opens in late January, any refund on your next joint return is applied to the old balance automatically. If you were counting on that refund, it's already spoken for — details in will the IRS take your refund every year.

- CP14 and reminder notices — the first bill gives you roughly 21 days before the sequence escalates (10 business days if the balance is $100,000 or more), followed by CP501 and CP503 reminders.

- CP504 — intent to levy your state tax refund, and a federal tax lien becomes a live possibility.

- LT11 / Letter 1058 — the final notice. After its 30-day window, the IRS can levy bank accounts and garnish wages.

Most December readers are at stage one or two — which is exactly the cheap stage. For the full picture of where the road ends, see what happens if you never pay the IRS.

The math on waiting: a married couple who owes $8,900

Say you and your spouse file jointly and owe $8,900. The math splits depending on whether that number is already assessed or still coming.

Case 1 — it's an assessed back balance. The failure-to-pay penalty alone is 0.5% × $8,900 = $44.50 per month. Waiting from late December to mid-April is roughly four months: about $178 in penalty, plus daily-compounding interest on the full balance the entire time. Paying before December 31 doesn't erase what's already posted, but it stops every dollar of future accrual. You can run your own figures with our Penalty & Interest Calculator — it estimates, based on your balance and dates.

Case 2 — it's a projected shortfall on this year's return. Say one spouse's consulting income left your withholding $8,900 short for 2026. Three moves, three different outcomes:

- Pay it as a Q4 estimate by January 15. Timely for the fourth quarter, so no further penalty accrues on Q4 — but if the shortfall built up all year, penalties on the Q1–Q3 portions already ran from each quarter's due date. See the estimated-tax underpayment penalty for how each quarter is scored.

- Boost December withholding instead. If either spouse has a December bonus or can push a big W-4 adjustment through payroll, that withholding is treated as paid evenly all year — $8,900 withheld in December is credited as $2,225 per quarter back to April. Done fully, it can erase the underpayment penalty entirely. A January estimated payment can never do that.

- Do nothing until April 15. The underpayment penalty keeps running on every quarter's shortfall until the day you pay, at the IRS's quarterly interest rate. On $8,900 that's not ruinous — but it's a purely avoidable cost.

One check before you drain savings: the safe harbor. If your combined withholding and estimates already equal 100% of last year's total tax — 110% if your prior-year joint AGI was over $150,000 — you generally owe no underpayment penalty at all, and the remaining $8,900 can simply wait for April 15 with zero cost. That's the one scenario where not paying before year end is the mathematically correct move.

Deciding whether to send the IRS money before December 31?

Don't guess with your savings. An experienced tax professional will check your safe harbor, your assessed balances, and your penalty exposure — free — so you pay only what the calendar actually requires while interest and penalties are still small. Call (888) 825-7779 or use the 2-minute form.

Can't pay before year end? Your real options

An $8,900 balance you can't pay in full has more IRS-sanctioned exits than most people realize — including one the IRS is required by law to accept. Here's the menu with the eligibility lines that actually matter:

| Option | Who's eligible | Cost & catch |

|---|---|---|

| Short-term payment plan | You can pay everything within 180 days | $0 setup fee; penalties and interest keep accruing until paid |

| Guaranteed installment agreement | Owe $10,000 or less in tax, filed and paid on time the prior 5 years, can pay within 3 years | The IRS must accept it by statute; setup fee applies; interest continues |

| Streamlined / online installment agreement | Owe $50,000 or less | Up to 72 months; no detailed financial disclosure; direct debit lowers the fee |

| Currently Not Collectible | Paying anything would leave you unable to cover basic living expenses, shown with financials | Collection pauses; the debt and interest remain; the IRS revisits when income rises |

| Offer in Compromise | The IRS's own math shows it can't collect the full balance from your income and assets before the collection statute runs | $205 fee plus 20% down on lump-sum offers (both waived with low-income certification); roughly 1 in 5 offers accepted in FY2024 |

| Penalty relief (FTA / AEP) | Clean filing and payment history for the prior 3 years | Removes qualifying penalties — not the tax or interest; AEP becomes automatic starting summer 2026 |

For a couple owing $8,900, the standout is the guaranteed installment agreement: under $10,000 with a clean recent history, acceptance isn't discretionary. Spread over 36 months, $8,900 is roughly $247 a month before interest — and setting it up before the new year means no CP504, no lien talk, no offset surprise beyond the refund itself.

If the reason you can't pay is a job loss or a medical year rather than a cash-flow hiccup, the hardship paths work differently — start with lost my job and can't pay the IRS. And for the full self-service playbook on every program above, the hub guide is how to settle tax debt yourself.

How to pay the IRS before end of year, step by step

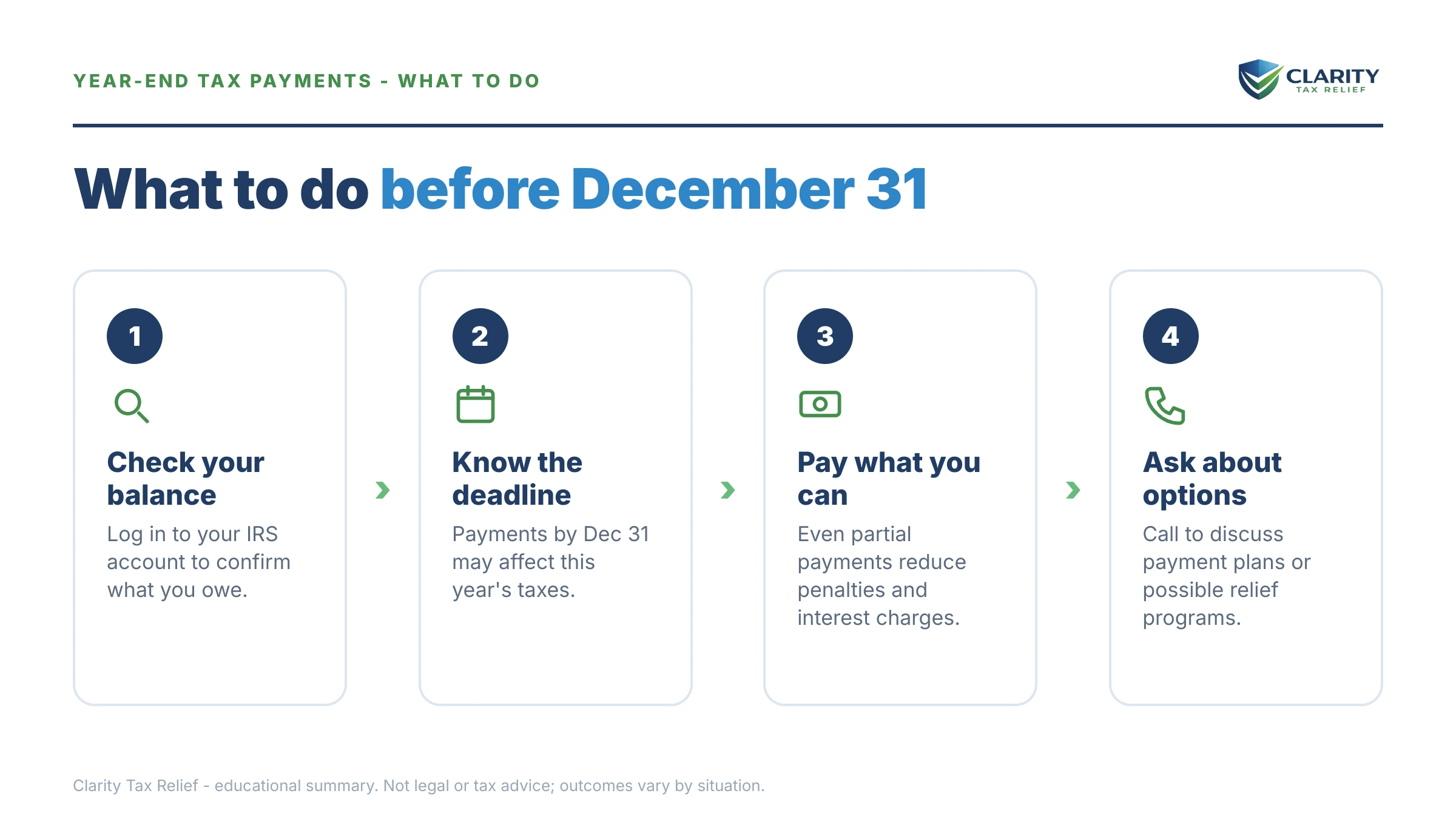

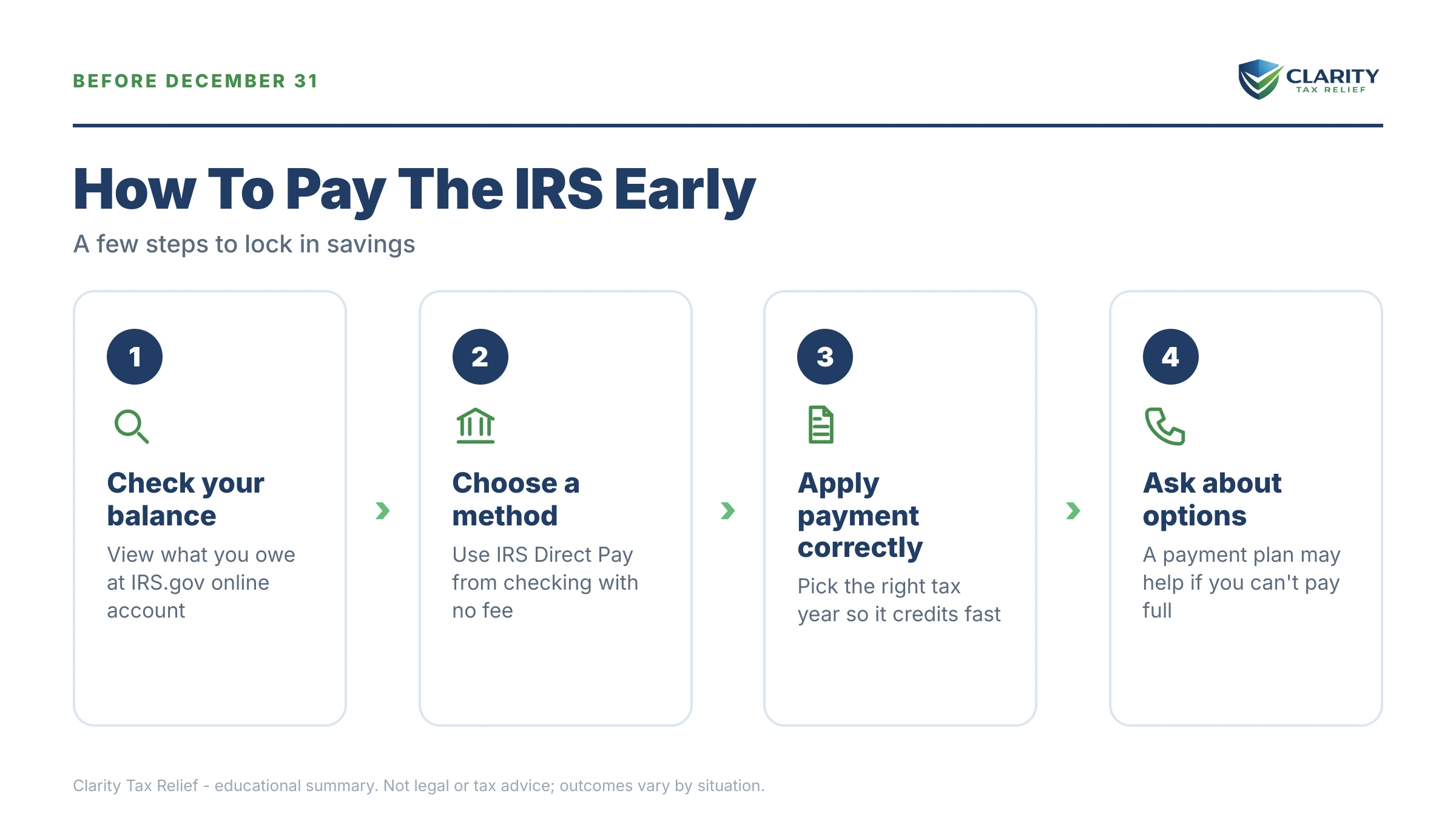

- Pin down the real number — log into your IRS online account to see any assessed balance, or project this year's shortfall from your year-to-date paystubs, 1099 income, and last year's return.

- Match each dollar to its deadline — assessed balances are accruing penalties now, so pay those first; withholding changes and deductible state payments must land by December 31; a federal Q4 estimate is timely through January 15.

- Check your safe harbor before overpaying — if your total withholding and estimates already reach 100% of last year's tax (110% if your prior-year AGI topped $150,000), you may owe no underpayment penalty — pay the rest in April instead of draining savings in December.

- Pay electronically so the date is locked in — use IRS Direct Pay or your online account and select the correct tax year and payment type (estimated tax vs. balance due). Save the confirmation number.

- Can't pay in full? Set up an agreement instead — apply online for a 180-day short-term plan or a monthly installment agreement before the notices escalate; an active agreement stops enforced collection while you pay.

The single most common year-end mistake is step 4: applying a payment to the wrong year. A December payment meant as a 2026 Q4 estimate but posted as a 2025 balance-due payment creates a phantom credit on one year and an untouched penalty clock on the other. Pick the year and type deliberately every time.

When you can handle this yourself — and when help changes the outcome

Most year-end IRS payments are a do-it-yourself job, and you shouldn't pay anyone to make one for you. Handle it solo if:

- You know your number and can pay it — Direct Pay takes ten minutes.

- Your balance is under $50,000 and you just need a monthly plan — the IRS payment plan online setup is genuinely straightforward.

- Your only issue is a Q4 estimate — pay it by January 15 and move on.

Experienced help earns its cost in a narrower set of situations: multiple unfiled years behind the balance (the order you fix things changes the total), a CP504 or LT11 already in hand (rights and deadlines are now in play), business or payroll tax mixed in, a disputed amount, or finances tight enough that hardship status or an Offer in Compromise is realistic — those are financial-disclosure exercises where the math has to be right the first time. If penalties are a big slice of what you owe, check whether first-time penalty abatement applies before you pay them.

Everything you'd do yourself runs through two official pages: IRS.gov/payments for making a payment and the IRS payment plans page for agreements. If a payment you made isn't posting correctly and you can't get it fixed, the Taxpayer Advocate Service exists for exactly that.

Year-end payment terms, decoded

- Estimated tax: quarterly prepayments (Form 1040-ES) on income with no withholding — the fourth installment is due January 15, not December 31.

- Safe harbor: the prepayment level (90% of this year's tax, or 100%/110% of last year's) that shields you from the underpayment penalty even if you still owe in April.

- Underpayment penalty: an interest-style charge, figured on Form 2210, on each quarter you paid in less than required — it runs until the day you pay.

- Failure-to-pay penalty: 0.5% of an unpaid assessed balance per month, up to 25% — separate from, and on top of, interest.

- Refund offset: the automatic application of your next refund to an existing IRS balance the moment your new return processes.

Pay IRS before end of year: your questions, answered

Does paying the IRS before December 31 lower my tax bill?

Not your federal bill — federal income tax payments are never deductible, so paying in December instead of April doesn't reduce the tax itself. What it reduces is the cost of carrying the balance: the 0.5%-per-month failure-to-pay penalty and daily interest stop accruing on whatever you pay. The exception is state income tax: a state payment made by December 31 can be deducted this year if you itemize, subject to the SALT cap.

Should I pay the IRS before December 31 or wait until January 15?

It depends on which balance you're paying. A fourth-quarter estimated payment is timely any time through January 15, so there's no federal penalty benefit to sending it in December. But if the balance is already assessed — the IRS has billed you — every day you wait adds interest, so pay it now. And a state estimated payment must land by December 31 to be deductible this year for itemizers.

Does increasing my December withholding erase estimated-tax penalties?

It can shrink or even erase them, because the IRS treats withholding as paid evenly across all four quarters no matter when it actually comes out of your paycheck. A large December withholding boost — from a bonus, an RSU vest, or a revised W-4 — gets credited back to April, unlike an estimated payment, which only counts from the date you send it. This is the single most powerful year-end move for a couple with one W-2 income and one 1099 income.

Will the IRS take our refund next spring if we still owe at year end?

Yes. Once a balance is assessed, the IRS automatically applies your next refund to it — no levy notice required. If you and your spouse over-withheld and expect a joint refund in the spring, an unpaid prior-year balance will absorb it before you see a dime. If only one spouse owes the underlying debt, the other may be able to recover their share of the refund with an injured spouse claim on Form 8379.

Does paying before year end stop penalties and interest completely?

It stops future accrual on whatever you pay, but it doesn't erase what has already been charged. Interest and the failure-to-pay penalty that posted before your payment remain part of the balance until paid. If penalties make up a meaningful chunk of what you owe, ask about first-time abatement — if your prior three years are clean, the IRS can remove qualifying penalties, and starting in summer 2026 an automatic version called AEP applies without any request.

What if we can't pay anything before the end of the year?

File every required return on time anyway — the failure-to-file penalty is 5% per month, ten times the 0.5% failure-to-pay penalty, so filing without paying protects you from the expensive one. Then set up a payment arrangement: a short-term plan gives you up to 180 days with no setup fee, and balances of $50,000 or less can go on a monthly plan online for up to 72 months. Collection notices stop escalating once an agreement is in place.

Do year-end IRS payments count on the date I send them?

Electronic payments through IRS Direct Pay, your IRS online account, or EFTPS are credited as of the day you submit them, which makes them the safe choice in the last week of December. A mailed check depends on postmark and processing, and a late-December mailing can post in January. If a December 31 date matters to you — for state deduction timing or year-end withholding — pay electronically and save the confirmation.

Your next 24 hours

- Find your real number. Log into your IRS online account and note any assessed balance and its tax year — that's the balance accruing 0.5% a month right now, and it comes before any December strategy.

- Gather three documents: last year's tax return (for the safe-harbor line), both spouses' most recent paystubs, and a running total of this year's 1099 or side income.

- Get a free case review. An experienced tax professional will tell you which dollars need to move by December 31, which can wait until January 15 or April, and whether a plan or penalty relief fits — before another month of interest posts. Call (888) 825-7779 or use the form.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.