Can't Pay the IRS

Lost My Job and Can't Pay the IRS: Every Real Option in 2026

The short answer: if you lost your job and can't pay the IRS, you are not held to your old salary. With little or no income you may qualify for Currently Not Collectible status, a reduced payment plan, or an Offer in Compromise — but nothing pauses automatically. You must file every return and ask.

"I lost my job and can't pay the IRS" describes two problems stacked on top of each other: the income that was supposed to cover the bill is gone, and the bill doesn't know that. The IRS computer keeps mailing notices to the person who had a paycheck.

Here's the part almost nobody tells you: a layoff is one of the few events that can actually improve your standing with IRS collections — if you document it and act on it while your income is low. This guide walks through exactly how, using a hypothetical $54,600 balance so you can see the math.

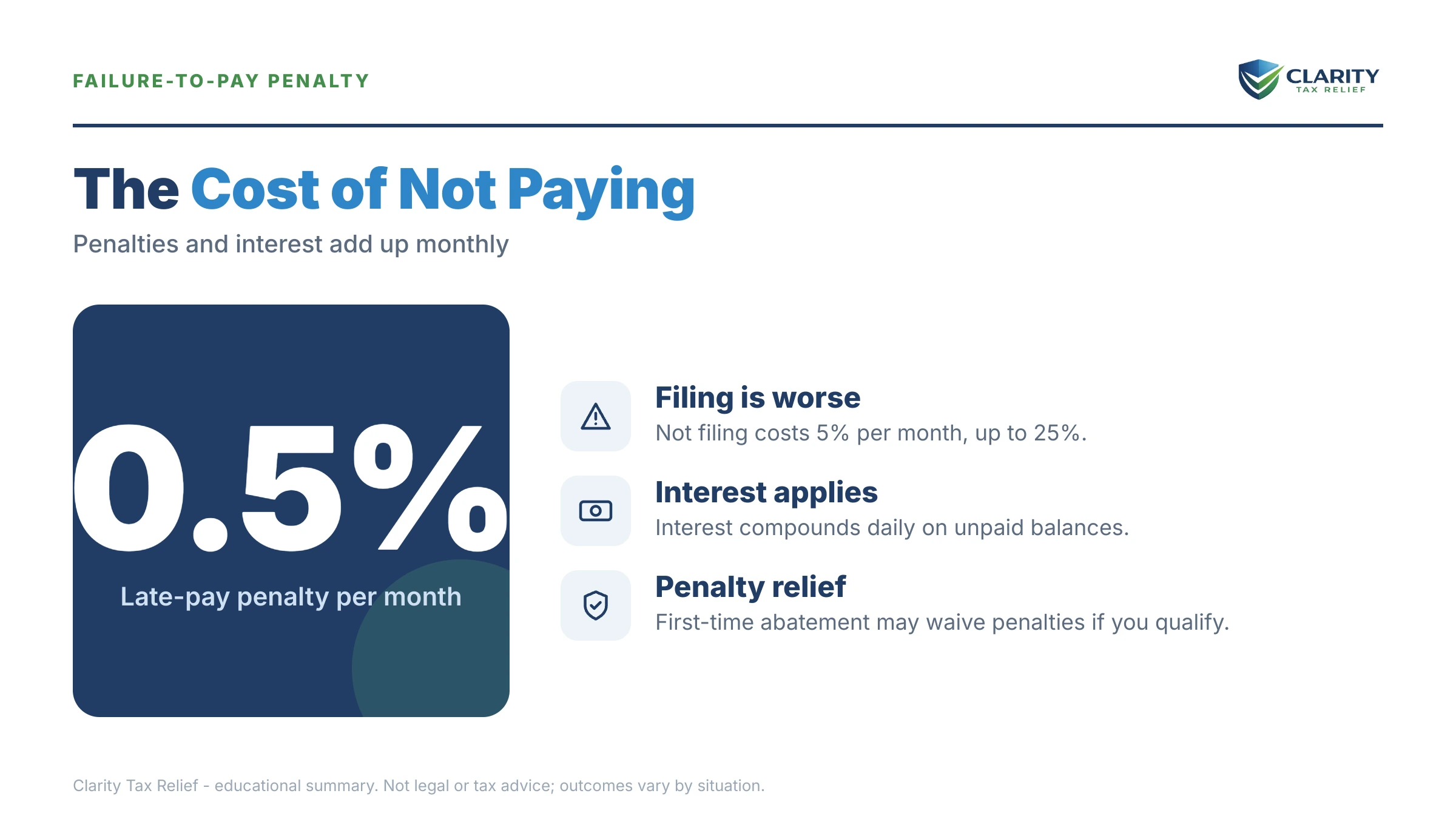

⏱ Your real clock: there is no single statutory deadline after a job loss — but the failure-to-pay penalty adds 0.5% of your balance every month, with interest compounding on top. And if an IRS notice is already in your mailbox, the response date printed on that notice is the deadline that controls.

Why losing your job changes your IRS options — in your favor

The IRS bases what you must pay on your current income and assets — not the salary you used to earn. Every hardship program in the collection system runs on a simple formula: your actual monthly income minus your necessary living expenses. When a layoff drives that number to zero or below, programs that were closed to you last year open up.

That's why timing matters. A person earning $95,000 with a $54,600 balance gets told to set up a full payment plan. The same person on unemployment, with the same balance, may qualify for paused collection or a settlement the IRS would never have considered before. Your window of strongest eligibility is while your income is down — which is exactly when most people freeze and do nothing.

The catch: none of it is automatic. The IRS doesn't know you were laid off until you show it — usually through your IRS online account, a phone call, or a Form 433-F walkthrough of your finances. Until then, the automated system treats you like someone who simply isn't paying.

What happens if you do nothing while unemployed

IRS collection is an automated sequence, and a layoff does not slow it down. If you ignore the balance, the stages arrive in this order, each with more power than the last:

- The bill (CP14). The first notice showing the balance, typically giving about 21 days before the sequence continues. If you're here, see got a CP14 and can't pay.

- Reminders (CP501, CP503). Still just bills — but the balance grows every month they sit unanswered.

- Intent to levy (CP504). The IRS can now seize your state tax refund, and a federal tax lien becomes a realistic next step.

- Final notice (LT11 / Letter 1058). This starts a 30-day clock and your Collection Due Process appeal rights. After the 30 days, enforcement is authorized.

- Levy. A bank levy comes with a 21-day hold before funds leave the account. A wage levy — the one that matters most when you eventually land a new job — is continuous until released.

Two more consequences run in the background. Any future tax refund gets offset against the debt automatically. And if the balance grows past $66,000 (the 2026 threshold), the IRS can certify it to the State Department, which can deny or revoke your passport. In 2026, with IRS staffing down roughly 27%, humans are harder to reach — but these steps are issued by computers that never stopped running.

Laid off and staring at a balance you can't touch?

Your low-income months are when your best IRS options are open — and penalties and interest are accruing monthly either way. Get a free, confidential review of which program your situation actually fits, before the notice sequence escalates.

Your options when you've lost your job and can't pay the IRS

Five programs cover nearly every job-loss situation, and which one fits depends on what's left after your necessary living expenses. (For the full do-it-yourself walkthrough of each program's paperwork, see how to settle tax debt yourself — this section focuses on how a layoff changes the math.)

| Option | Who typically qualifies | What it does while you're unemployed |

|---|---|---|

| Short-term payment plan | You can full-pay within 180 days (severance arriving, a job offer in hand) | Stops the notice sequence with $0 setup fee; interest and penalties continue |

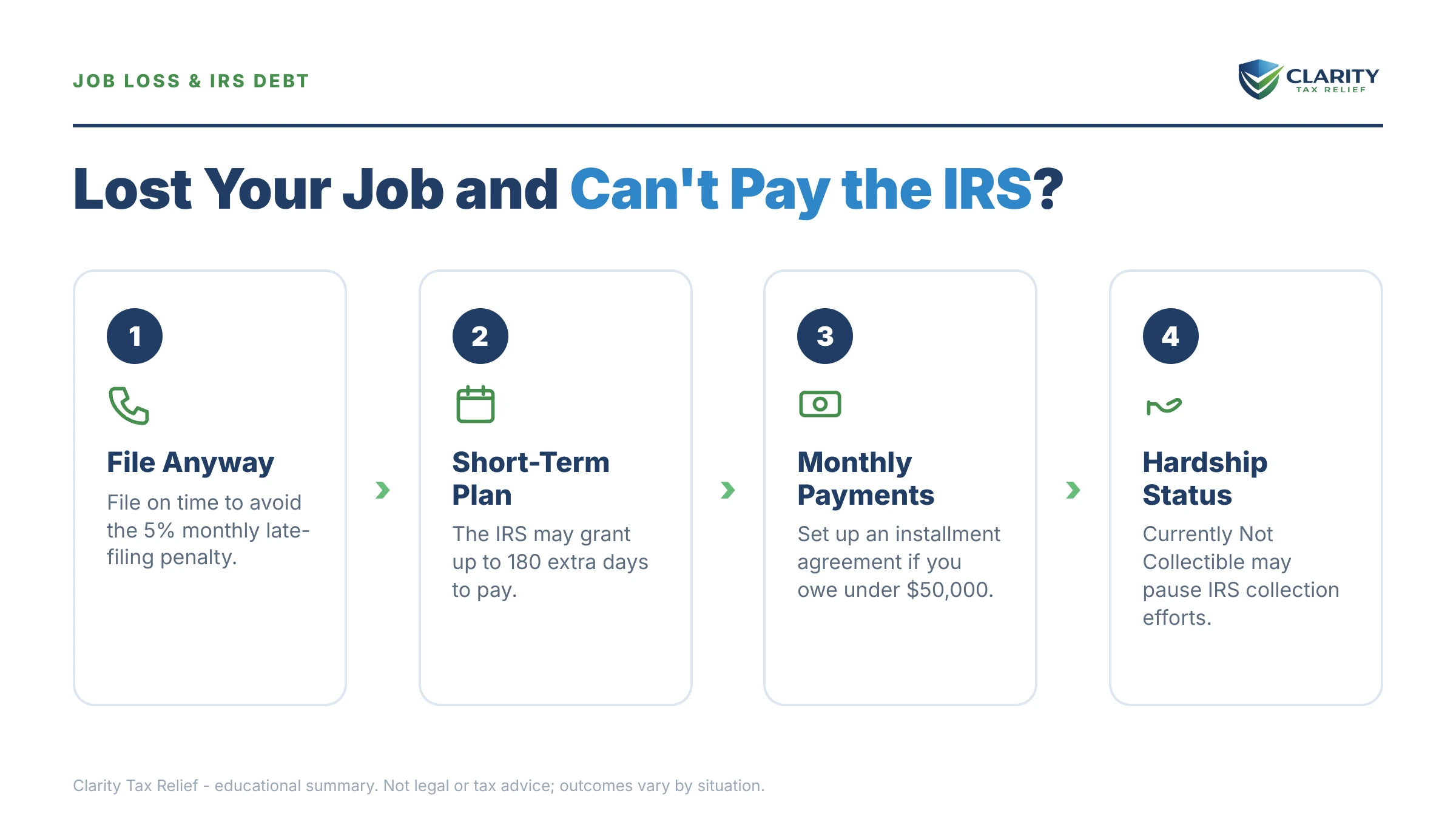

| Long-term installment agreement | Balance ≤ $50,000: set up online, up to 72 months. Above $50,000: financial disclosure (Form 433-F) required | Monthly payment sized to what you can actually afford; enforcement stops while it's active |

| Currently Not Collectible (CNC) | Income below the IRS's allowable living expense standards — common on unemployment alone | Levies and garnishment pause entirely; refunds still offset; balance keeps accruing |

| Offer in Compromise (OIC) | Assets plus realistic future income can't cover the balance before collection time runs out | Settles the debt for your Reasonable Collection Potential; means-tested, not automatic |

| Penalty relief (FTA / reasonable cause / AEP) | Clean prior 3 years, or documented hardship caused by the layoff | Removes qualifying penalties and shrinks the balance every other option is measured against |

Currently Not Collectible is the program built for exactly this moment. You show the IRS — usually on Form 433-F — that your unemployment income doesn't cover rent, utilities, food, health costs, and transportation under its national standards. If it doesn't, collection pauses. The debt isn't forgiven and interest keeps running, but no one touches your bank account or your eventual new paycheck while the status holds. The full mechanics are in our Currently Not Collectible status guide, and the same hardship framework applies whether the squeeze came from a layoff or from medical hardship and IRS debt.

The Offer in Compromise is where job loss gets complicated. The IRS decides offers on Reasonable Collection Potential (RCP): roughly your asset equity plus a multiple of your monthly disposable income. Unemployment can drive that disposable-income figure to zero — but the IRS may treat a recent layoff as temporary for someone with a strong work history and project the income it expects you to earn again. Two facts keep this honest: the IRS accepted roughly 1 in 5 offers in FY2024, and if your household income is low enough (AGI at or below 250% of the poverty level), low-income certification waives the $205 application fee, the 20% down payment, and payments during review. You can estimate your own numbers with our Offer in Compromise Calculator before anyone charges you a dime to "see if you qualify."

Penalty relief is the quiet win most people skip. If your prior three years were clean, first-time penalty abatement can remove the failure-to-pay penalty for one year — and starting summer 2026, the IRS's new Automatic Exemption from Penalty (AEP) applies similar relief automatically, with no request needed. A layoff that forced you to choose between housing and the tax bill can also support a reasonable-cause request, with documentation.

What each option costs and how long it takes

| Option | Upfront cost | Cost while unemployed | Typical time to set up |

|---|---|---|---|

| Short-term plan (180 days) | $0 setup fee | Interest + 0.5%/month penalty continue | Same day online |

| Long-term installment agreement | Setup fee varies; reduced or waived for low-income taxpayers | Monthly payment + accruals | Same day online if ≤ $50,000; longer if financials are required |

| Currently Not Collectible | $0 | $0 out of pocket; accruals continue on paper | Typically weeks, after the IRS reviews your financials |

| Offer in Compromise | $205 fee + 20% down on lump-sum offers — both waived with low-income certification | The offer amount, if accepted | Commonly many months; auto-accepted if the IRS doesn't decide within 2 years, with narrow exceptions — a returned or rejected offer stops the clock, and time during court disputes does not count |

| Penalty abatement / AEP | $0 | Removes qualifying penalties from the balance | Often resolved in weeks by phone or letter |

Say you owe $54,600 and just got laid off: the math

This is a hypothetical, but it's built the way the IRS actually builds these cases. Say you're a single W-2 employee who owed $54,600 across two tax years when the layoff hit. Unemployment pays you about $2,100 a month. Here's how each door looks:

- Do nothing: the failure-to-pay penalty alone is 0.5% × $54,600 = $273 a month, before interest. At that pace of accrual, the balance can cross the $66,000 passport-certification threshold in roughly two years if nothing changes.

- Online payment plan: not available yet — $54,600 sits above the $50,000 online ceiling. You'd either pay roughly $4,700 to get under $50,000 (unrealistic on unemployment) or submit Form 433-F. And even under the ceiling, $50,000 over 72 months is about $694 a month — a third of your unemployment income.

- Currently Not Collectible: your $2,100 income against IRS-standard expenses for rent, food, utilities, health insurance, and a car almost certainly nets negative. On these facts, CNC is the realistic near-term answer: collection pauses, and the 10-year collection clock keeps running against the IRS.

- Offer in Compromise: suppose your only assets are a financed car with $2,000 of equity and $1,200 in savings. On paper, RCP is tiny next to $54,600. The open question is future income — the IRS may project your return to work. Whether to file the offer now or bank CNC first and revisit is exactly the judgment call worth getting professional eyes on.

Notice what the example shows: with the same $54,600, the "right answer" isn't one program — it's a sequence. File everything, request penalty relief, land in CNC while income is down, and evaluate an offer with real numbers instead of hope.

Three situations that change the answer

Your spouse still works and you filed jointly. The debt is joint, and the IRS counts household income and expenses on Form 433-F. A working spouse's paycheck can close the door on CNC — but it usually supports a lower, survivable installment agreement instead. Don't assume hardship status is off the table until the household math is actually run.

You were already on a payment plan when the layoff hit. Do not just stop paying — a defaulted agreement triggers a CP523 and restarts enforcement. Contact the IRS before you miss payments to lower your IRS monthly payment or convert the agreement to CNC based on your new income. An arrangement modified in advance survives; one abandoned quietly does not.

The severance-year trap. If you got a severance package, it's fully taxable and often withheld at a flat supplemental rate that doesn't match your bracket — so the year you were laid off can itself produce a surprise balance due next April. High severance-year income can also disqualify you from low-income OIC certification even though you're broke today, which is another reason timing your applications matters.

Don't create next year's tax bill while unemployed

Unemployment benefits are taxable, and by default nothing is withheld from them. A full year of benefits with zero withholding is how people resolve one IRS debt and mail themselves another — file Form W-4V to have 10% withheld from each payment, and read owe taxes on unemployment if last year's benefits are already part of your balance.

Resist the urge to raid retirement money without running the numbers. If you're under 59½, a withdrawal is taxed as ordinary income plus a 10% early-withdrawal penalty — the exact trap covered in our guide to the 401(k) withdrawal tax bill you can't pay. There are cases where a partial withdrawal to get under the $50,000 online-plan line makes sense; there are more cases where it converts protected money into a second debt.

And when the new job comes, set your W-4 correctly on day one. Nothing undoes a year of careful resolution work faster than a new balance due.

How to handle IRS debt after a job loss, step by step

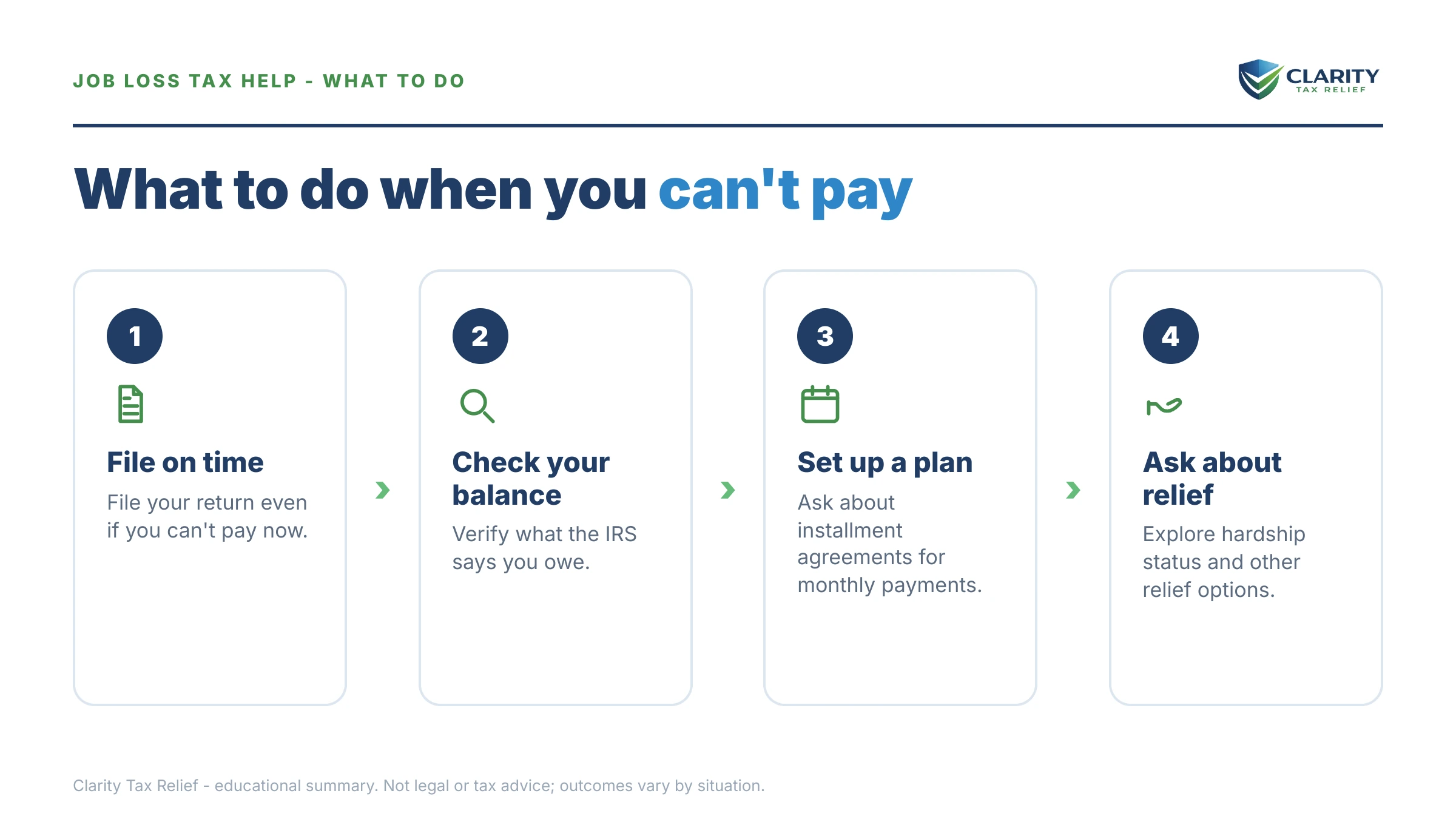

- Pull your exact balance. Log into your IRS online account and write down the total owed, the tax years involved, and any notices already issued. Every decision below depends on those numbers.

- File every unfiled return. File even with zero payment attached — the failure-to-file penalty is ten times the failure-to-pay penalty, and no relief program is available until your filings are current.

- Document your new financial reality. Gather your termination or layoff letter, your unemployment award letter, and your last three months of bank statements. This is exactly the evidence Form 433-F asks for.

- Match your finances to a program. No money left after necessary living expenses points to Currently Not Collectible. Some room in the budget points to an installment agreement. Assets plus future income that can never cover the debt points to an Offer in Compromise.

- Submit before enforcement starts. Set up a payment plan online, or send Form 433-F for hardship status. If a notice is already in hand, respond by the date printed on it — that date controls, not the calendar.

- Recheck the arrangement when you're re-employed. New income can end hardship status or make a low payment default. Update the IRS proactively so the arrangement adjusts instead of collapsing.

When you can handle this yourself — and when help changes the outcome

Plenty of job-loss cases don't need professional help. If your balance is modest, your returns are filed, and you expect income back within a few months, a $0-setup short-term plan or a simple online agreement is something you can do tonight — our comparison of the best way to pay the IRS covers the mechanics, and the reasons to file even if you can't pay apply to everyone.

Experienced help earns its cost when the stakes and the judgment calls get bigger: a balance over $50,000 that requires financial disclosure (where how expenses are presented decides between CNC and an unaffordable plan), multiple unfiled years, a final levy notice already in hand, or an Offer in Compromise where the future-income projection is genuinely arguable. In those cases, the difference between a well-built 433-F and a rushed one is measured in hundreds of dollars a month — every month.

Terms you'll run into, decoded

- Currently Not Collectible (CNC): an IRS status that pauses active collection because paying would leave you unable to meet basic living expenses.

- Allowable living expenses: the IRS's national and local standards for what housing, food, transportation, and health care "should" cost — the yardstick your budget is measured against.

- Form 433-F: the Collection Information Statement — the financial snapshot the IRS uses to decide hardship status and payment amounts.

- Reasonable Collection Potential (RCP): the IRS's calculation of the most it could ever collect from you; the floor for any Offer in Compromise.

- Levy: the actual seizure of money or property — a bank account, a paycheck, a state refund — as opposed to a lien, which is a claim recorded against what you own.

- CSED: the Collection Statute Expiration Date — generally 10 years from assessment, after which the IRS can no longer collect (certain events pause the clock).

Lost-my-job IRS questions, answered

Will the IRS stop collecting if I lost my job?

Not automatically — you have to ask. If your unemployment income can't cover the IRS's allowable living expense standards, you can request Currently Not Collectible status, usually by submitting Form 433-F with proof of your new income. Once granted, levies and garnishments stop, but penalties and interest keep accruing and the IRS re-checks your income in future years.

Do I have to pay taxes on unemployment benefits?

Yes — unemployment compensation is taxable income on your federal return. Nothing is withheld unless you request it, which is why many people who collect benefits all year owe again the next April. Filing Form W-4V has 10% withheld from each payment, so this year's hardship doesn't become next year's second tax debt.

Can the IRS levy my unemployment check?

Unemployment benefits are generally exempt from IRS levy under federal law, so the IRS can't intercept the benefit payment itself. But that protection doesn't follow the money into your bank account — funds sitting in a checking account can still be reached by a bank levy once the debt hits final-notice stage. Don't treat the exemption as a reason to ignore IRS mail.

Should I cash out my 401(k) to pay the IRS?

Usually not without running the math first. If you're under 59½, an early withdrawal is taxed as ordinary income plus a 10% penalty, which often creates a new tax bill the following year — trading one IRS debt for another. Compare that cost against a payment plan or hardship status, which may cost far less while your income is down.

Should I still file my tax return if I can't pay anything?

Yes — always file, even with a zero payment. The failure-to-file penalty runs 5% of the unpaid tax per month, ten times the 0.5% failure-to-pay penalty, so skipping the return multiplies the damage. Filing on time also preserves your eligibility for payment plans and settlement programs, all of which require you to be current on filings.

Does losing my job qualify me for an Offer in Compromise?

Job loss strengthens an offer but doesn't qualify you by itself. The IRS calculates what it could realistically collect from your assets and future income, and it may treat unemployment as temporary for someone with a recent work history — projecting the income it expects you to earn again. The IRS accepted roughly 1 in 5 offers in FY2024, so have the math checked before you pay anyone to file one.

Will the IRS garnish my paycheck when I start a new job?

It can, if your debt has already passed the final-notice stage and you never responded. A wage levy is continuous — it stays on every paycheck until the debt is paid or the levy is released. Getting into a payment plan or hardship status before you're re-employed is the cleanest way to make sure your first new paycheck arrives whole.

Can IRS penalties be removed because I lost my job?

Sometimes. Job loss alone isn't automatic reasonable cause, but if it caused genuine hardship — you had to choose between rent and the tax bill — a reasonable-cause request can succeed with documentation. If your prior three years are clean, first-time penalty abatement is a simpler path, and starting summer 2026 the IRS's new Automatic Exemption from Penalty applies to qualifying taxpayers with no request needed.

Your next 24 hours

- Find your number. Log into your IRS online account tonight and write down the total balance, the tax years it covers, and the most recent notice on the account.

- Gather your proof. Pull your last filed return, any IRS letters, your layoff or termination letter, your unemployment award letter, and three months of bank statements — the complete file every option below runs on.

- Get the free case review. Call (888) 825-7779 or use the 2-minute form. An experienced tax professional will match your post-layoff finances to the right program while your eligibility is at its strongest — the balance is accruing penalties and interest every month it waits.

The primary sources, if you want to go straight to the government: the IRS's payment plans and installment agreements page, its Offer in Compromise page, and the independent Taxpayer Advocate Service for cases the normal channels are mishandling.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.