Can't Pay the IRS

Medical Bills Mean You Can't Pay the IRS: Every Option in 2026

The short answer: if medical bills mean you can't pay the IRS, the IRS must count your documented out-of-pocket medical costs as necessary living expenses before it can demand payment or keep a levy in place. That documented hardship may qualify you for Currently Not Collectible status, a lower payment plan, penalty removal, or an Offer in Compromise.

The hospital's billing department calls one week, the IRS writes the next — and only one of them can reach into your paycheck without a judge's signature. If you're staring at treatment bills and an IRS notice at the same time, with rent due and no house to borrow against, the squeeze is real. It's also solvable: the tax code has specific, written rules that treat medical hardship as exactly that — hardship — and this page walks you through how to use every one of them.

⏱ Your real clocks: if a Final Notice of Intent to Levy (LT11 or Letter 1058) has arrived, you have 30 days from the date on that letter to request a Collection Due Process hearing on Form 12153 before the IRS can levy your pay or bank account. If a bank levy has already hit, the bank holds the funds 21 days before sending them to the IRS — hardship releases happen inside that window. No final notice yet? Then your clock is penalties and interest compounding every month.

Why medical bills and IRS debt collide

Medical hardship creates tax debt in predictable ways, and knowing which one hit you shapes the fix. The most common paths:

- You raided retirement savings to pay for treatment. An early withdrawal is taxed as ordinary income, usually plus a 10% penalty — a debt that shows up a year after the crisis. Our guide to the 401k withdrawal tax bill you can't pay covers that path in depth.

- You couldn't work, so withholding and estimated payments stopped — but freelance or severance income still landed, untaxed.

- You filed late, or not at all, while sick. The failure-to-file penalty runs 5% per month — ten times the failure-to-pay penalty — so a missed filing during treatment inflates the balance fast.

- You had the money for the tax bill until the deductible, the copays, and the uncovered charges took it. The debt is accurate; the cash is simply gone.

Whichever route brought you here, the leverage is the same: the IRS's own collection rules require it to leave you enough money for necessary health care before it takes anything else. Most people never invoke that rule because they never learn it exists.

What happens if you ignore the IRS while paying the hospital

IRS collection is an automated sequence, and it escalates on schedule whether or not a human ever reads your file. Even with the IRS workforce cut roughly 27% in 2025, the notice-and-levy machinery never paused. The stages, in order:

- CP14 — the first bill. No enforcement power yet, just the balance with penalties and interest attached. If this is where you are, read got a CP14 and can't pay — it's the cheapest stage to act.

- CP501 / CP503 — reminders. Still bills, but the balance grows monthly while they cycle.

- CP504 — intent to levy your state refund. The IRS can now take your state tax refund, and a federal tax lien becomes realistic.

- LT11 / Letter 1058 — the final notice. A 30-day clock starts. Miss it and the IRS can levy without further warning; use it and you get a Collection Due Process hearing where hardship arguments are heard before money moves.

- Levy. A bank levy freezes what's in the account, with a 21-day hold before the funds leave. A wage levy is continuous — it repeats every payday until released. Social Security can be levied up to 15% through the Federal Payment Levy Program.

Note the asymmetry with your medical creditors: a hospital or collection agency must sue you and win a judgment before touching your wages. The IRS skips court entirely. If you want to see what a wage levy would actually do to your paycheck, you can estimate it with our IRS Wage Garnishment Calculator.

Facing a levy while the medical bills keep coming?

Medical hardship is one of the strongest cases for stopping IRS collection — but only if it's documented and presented before the clock runs. Get your situation reviewed free: if a bank levy has hit, the 21-day hold is your window; if an LT11 arrived, the 30-day hearing deadline is.

Your options when medical bills mean you can't pay the IRS

Every IRS resolution program is means-tested, and documented medical expenses shift the means test in your favor. The general mechanics of each program live in our guide to how to settle tax debt yourself; here's how each one behaves when medical hardship is the driver:

| Option | Key threshold / requirement | How medical hardship changes it |

|---|---|---|

| Short-term payment plan | Full payment within 180 days; $0 setup fee | Buys time if insurance reimbursement or disability pay is coming |

| Installment agreement | Up to 72 months online for balances ≤ $50,000 | Documented medical costs justify a lower monthly payment |

| Partial-pay installment agreement | Financial disclosure (Form 433-F) showing you can't full-pay | Ongoing treatment costs cap the payment below full payoff |

| Currently Not Collectible (CNC) | Budget shows no money left after allowable expenses | Medical costs count toward that budget — often the deciding line |

| Offer in Compromise | $205 fee + 20% down (lump sum); waived if AGI ≤ 250% of poverty | Medical expenses shrink the "collectible" amount the offer is based on |

| Penalty abatement | Reasonable cause, or clean prior 3 years for first-time abatement | Serious illness is a textbook reasonable-cause ground |

| Hardship levy release (IRC §6343) | Levy prevents paying basic living or medical expenses | Built precisely for this situation — treatment costs are the evidence |

Two of these deserve their own sections, because they're the ones a renter facing a levy will most likely use: the hardship math behind CNC, and the emergency levy release.

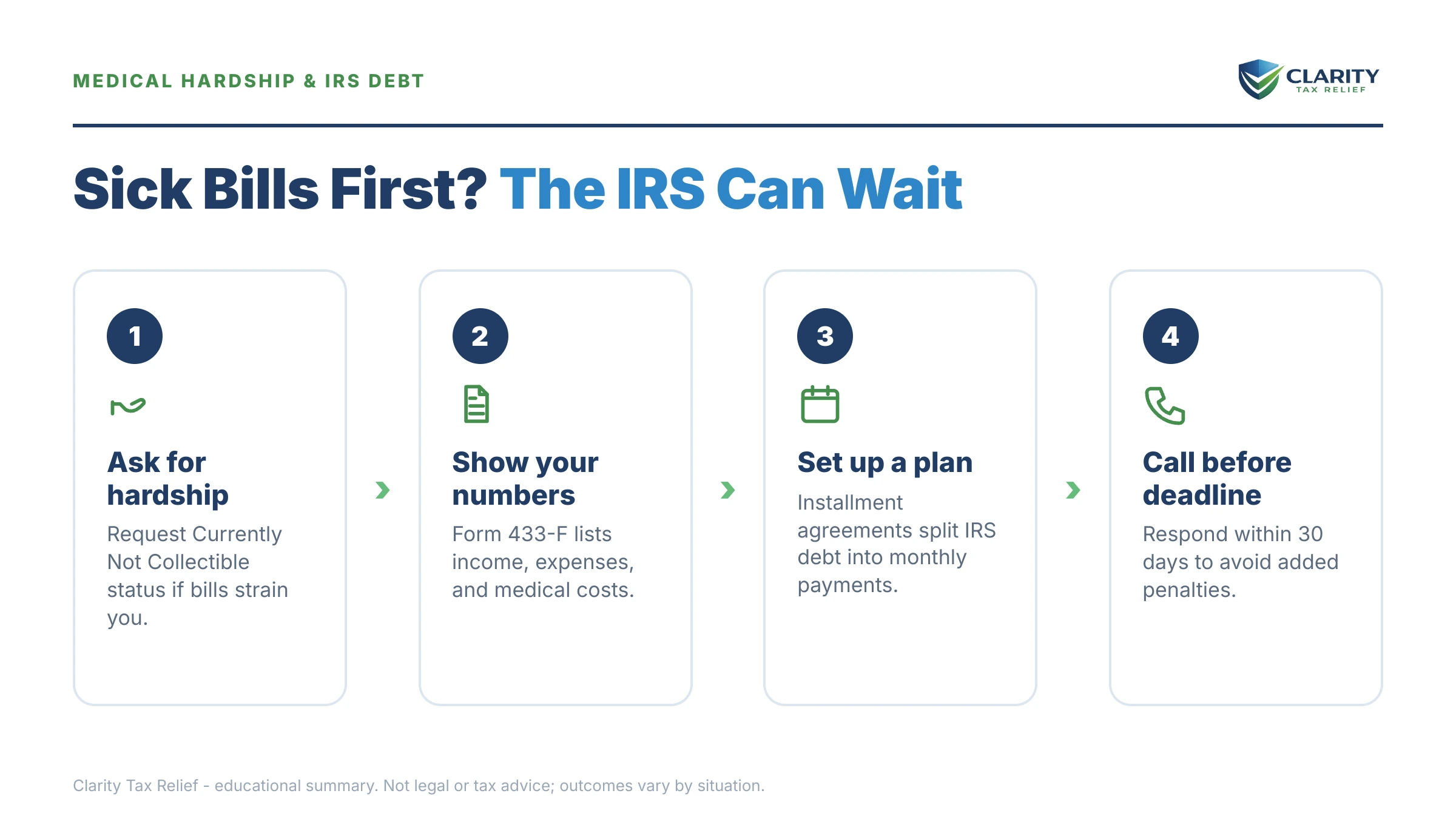

How medical expenses change the IRS's hardship math

The IRS decides what you can pay by subtracting "allowable living expenses" from your income — and out-of-pocket health care is an allowable category. You get a national standard amount for health costs automatically, and you can claim your actual, higher costs when you can document them: insurance premiums, copays, prescriptions, medical equipment, and travel to treatment. The full framework is in our guide to the IRS allowable living expenses standards, and the numbers get reported on Form 433-F.

Here's what that means in real numbers. This is a hypothetical example, not a client case.

Say you owe $41,800 after a year of treatment, you rent, and your take-home pay is $4,100 a month. On a standard 72-month streamlined plan, the minimum math is $41,800 ÷ 72 ≈ $581 a month — and because interest and the 0.5% monthly late-payment penalty keep accruing, the true payoff runs somewhat higher. Now run the hardship budget:

- Rent and utilities: $1,720

- Food, clothing, household (national standard): $850

- Car payment and operating costs: $1,050

- Health insurance premiums: $410

- Documented out-of-pocket treatment costs: $520

Total allowable expenses: $4,550 against $4,100 of income — you're $450 underwater every month. On those facts, the IRS's own formula says your ability to pay is zero: that's a Currently Not Collectible case, and any levy in motion should be released as a hardship. Strip out the two medical lines and the same budget shows $480 a month left over — enough for the IRS to demand a payment near that $581 figure. The medical documentation isn't a sympathy plea; it's the arithmetic difference between a $581-a-month demand and a $0 hardship status. See Currently Not Collectible status for how the status works and how long it holds.

The same math drives an Offer in Compromise. As a renter with no home equity, negative monthly cash flow, and — say — about $1,800 of reachable equity in a paid-down car, your "reasonable collection potential" is roughly that $1,800, not $41,800. An offer in that neighborhood is at least arithmetically defensible — but the IRS accepted roughly 1 in 5 offers in FY2024, verifies every number, and rejects offers whose math doesn't hold. If your AGI is at or below 250% of the federal poverty line, low-income certification waives the $205 fee, the 20% down payment, and payments while the offer is reviewed — details in our guide to the OIC low income certification.

Stopping a levy that's already in motion

IRC §6343 requires the IRS to release a levy that prevents you from meeting basic living expenses — and medical costs are basic living expenses. If a wage levy is shrinking paychecks you need for rent and treatment, or a bank levy froze the account your prescriptions come out of, you (or your representative) call the IRS, present the budget above, and request an economic-hardship release. The full playbook is in levy causing hardship.

Three timing facts matter. A bank levy's funds sit at the bank for 21 days before going to the IRS — a release obtained inside that window gets the money back before it leaves. A wage levy has no such buffer; it repeats every payday until released, so speed matters even more. And if the IRS is slow or unreachable — a real problem with 2026 staffing — the Taxpayer Advocate Service can force attention on a hardship case through Form 911.

Penalty relief when illness caused the debt

Serious illness is one of the clearest reasonable-cause grounds in the IRS's own penalty guidance. If you filed or paid late because you — or an immediate family member you cared for — were hospitalized or incapacitated, reasonable cause penalty abatement can remove the failure-to-file and failure-to-pay penalties for the affected period. The evidence is exactly what you already have: admission records, treatment dates, statements showing when the crisis began and ended.

Two other paths run alongside it. First-time abatement requires only a clean compliance record for the prior three years — no illness story needed. And starting summer 2026, the IRS's new Automatic Exemption from Penalty (AEP) begins applying some penalty relief automatically, with no request at all — so before you pay a penalty, check whether it's already been exempted. Interest on the tax itself generally survives abatement; interest on an abated penalty comes off with it.

What's realistic at your balance level

Medical hardship changes the analysis at every debt size, but the procedural doors differ by balance:

| Balance owed | Realistic options with documented medical costs | Watch out for |

|---|---|---|

| Under $10,000 | Guaranteed installment agreement with minimal review; penalty abatement may cut the balance meaningfully | Interest keeps accruing — pay it off early if reimbursement arrives |

| $10,000–$50,000 | Streamlined plan online up to 72 months (direct debit typically required above $25,000); CNC or an OIC if medical costs erase your disposable income | Defaulting a plan you couldn't afford restarts enforcement — set the payment on the hardship budget, not hope |

| $50,000–$100,000 | Full financial disclosure required; partial-pay agreements and CNC become the workhorses | Passport certification at $66,000 (2026 threshold) — the State Department can deny or revoke your passport |

| Over $100,000 | Likely a revenue officer, not the automated system; hardship documentation matters even more with a human reviewing it | 10-day response windows on some notices at this level; don't sit on mail |

If the medical crisis also cost you your income, the playbook shifts further toward hardship status — our companion guide lost my job and can't pay the IRS covers the no-income version of this problem. And whichever option you land on, choose the payment channel deliberately: the best way to pay the IRS varies by whether you're making one payment or seventy-two.

How to respond, step by step

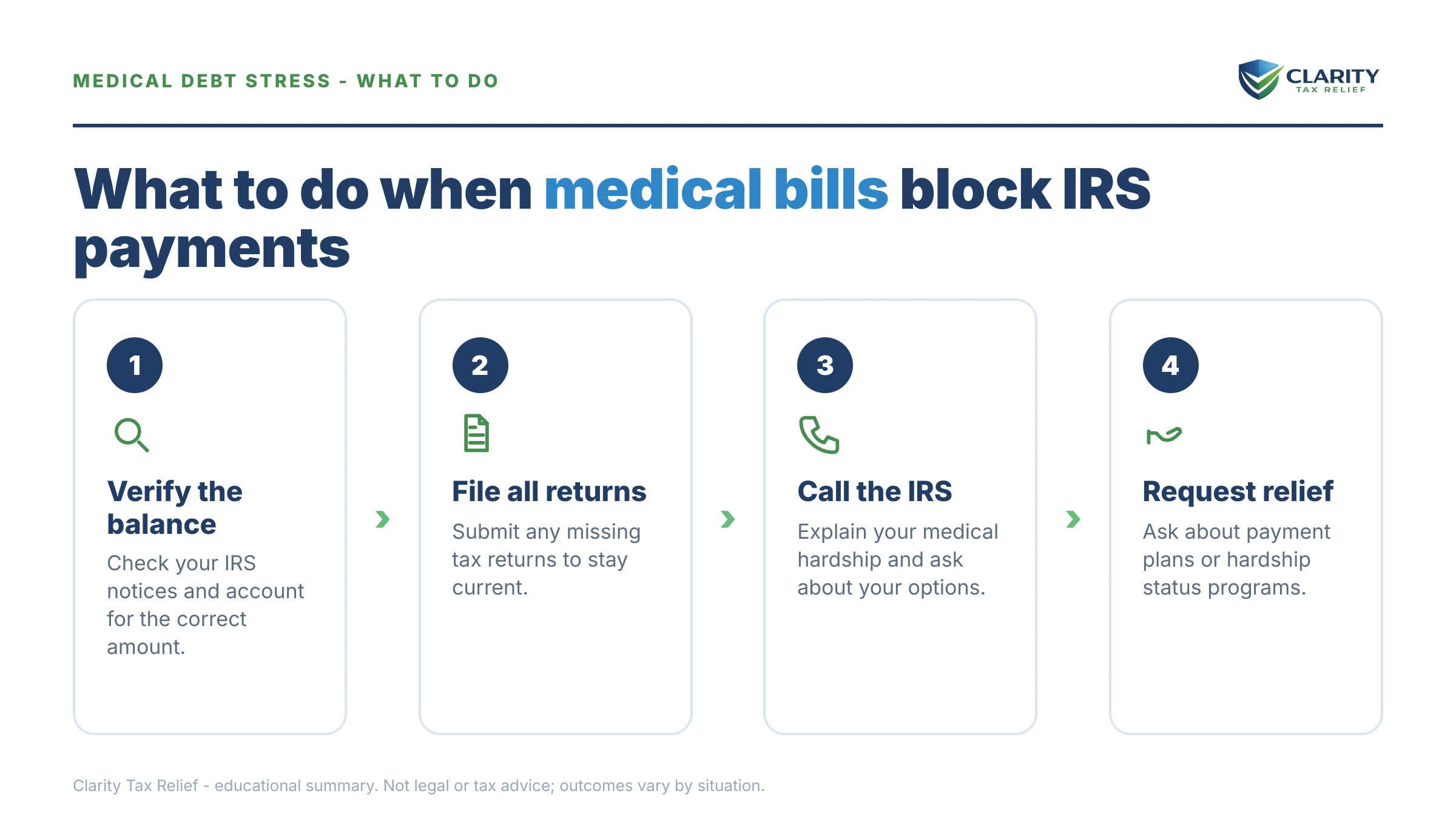

- Pull your IRS balance and latest notice. Log into your IRS online account, confirm the total owed for every year, and check which notice you're on (CP14, CP504, LT11) — that sets your real clock.

- Gather your medical-expense proof. Collect three months of medical bills, insurance premium statements, explanation-of-benefits forms, and prescription receipts, and total your true monthly out-of-pocket cost.

- Run your budget on Form 433-F terms. List monthly income, then subtract rent, utilities, food, transportation, insurance, and your documented medical costs — the remainder is what the IRS can realistically ask for.

- Request the option that matches the math. Ask for a payment plan if money is genuinely left over, Currently Not Collectible status if nothing is, or an Offer in Compromise if your income and assets can never cover the debt.

- Ask for penalty relief in the same contact. Request reasonable-cause abatement for the illness (or first-time abatement if your prior three years were clean) so the balance you resolve is the smallest legal number.

When you can handle this yourself — and when help changes the outcome

Plenty of medical-hardship cases don't need professional help. If your balance is under $10,000, no levy is in motion, and you agree with the amount, a guaranteed or streamlined installment agreement takes twenty minutes online. If reimbursement or disability back pay is arriving within six months, the 180-day short-term plan costs nothing to set up and stops the escalation.

Experienced help earns its cost in the harder configurations: a levy already hitting your pay or bank account, where every payday of delay is money gone; a CNC or offer case, where how the Form 433-F expenses are categorized and documented decides whether the hardship math holds; multiple unfiled years, where filing order affects penalties; or a rejection you need to appeal. The IRS applies its expense standards mechanically — a case presented in the IRS's own framework, with the medical documentation organized the way its examiners expect, gets a materially different reception than a plea for mercy.

Terms you'll see on your notices, decoded

- Levy: the actual seizure of money or property — wages, bank funds, state refunds. Different from a lien, which is a legal claim, not a taking.

- Currently Not Collectible (CNC): account status that pauses IRS collection because your budget shows nothing left after necessary expenses. The debt remains and interest accrues.

- Allowable living expenses: the IRS's expense standards — housing, food, transportation, and out-of-pocket health care — subtracted from income to compute what you can pay.

- Economic hardship (§6343): the legal standard requiring the IRS to release a levy that prevents you from meeting basic living and medical expenses.

- Reasonable cause: the standard for removing penalties when circumstances beyond your control — including serious illness — caused late filing or payment.

- CSED: the Collection Statute Expiration Date — generally 10 years from assessment, after which the IRS can no longer collect; certain events (appeals, offers, bankruptcy) pause the clock.

Medical bills and IRS debt: your questions, answered

Will the IRS forgive tax debt because of medical bills?

Not automatically — there is no medical-forgiveness program. But medical hardship feeds every real relief path: documented medical costs lower what the IRS says you can pay, which can qualify you for Currently Not Collectible status or an Offer in Compromise. The IRS accepted roughly 1 in 5 offers in FY2024, and eligibility is means-tested — the math, not the diagnosis, decides.

Do medical bills count as expenses when the IRS decides what I can pay?

Yes. Out-of-pocket health care is one of the IRS's allowable living expense categories. You get a national standard amount automatically, and you can claim your actual, higher costs — premiums, copays, prescriptions, treatment travel — if you document them. Those expenses come off your income before the IRS calculates any payment plan, hardship status, or offer amount.

Can the IRS levy my bank account if the money is earmarked for medical bills?

Yes — a levy grabs whatever is in the account the day it hits, regardless of what the money was for. The bank then holds the funds for 21 days before sending them to the IRS, and that window is your chance to request a release. If losing the money prevents you from paying basic living or medical expenses, the IRS can release the levy for economic hardship under IRC §6343.

Will the IRS remove penalties if I was seriously ill?

Often, yes. Serious illness — yours or an immediate family member's — is one of the clearest grounds for reasonable-cause penalty abatement, especially when hospital records show why you couldn't file or pay on time. First-time abatement is a separate path if your prior three years were clean, and starting summer 2026 the IRS's Automatic Exemption from Penalty (AEP) applies some relief with no request needed. Interest on the tax itself generally stays.

Should I pay the hospital or the IRS first?

Prioritize the IRS for one structural reason: it can levy your paycheck and bank account without suing you, while a hospital or medical collector must win a court judgment first. That said, don't stop essential current care to pay old taxes — the IRS's own expense standards allow ongoing health costs, and hardship rules exist precisely so treatment continues.

Does Currently Not Collectible status erase my tax debt?

No. CNC pauses collection — no levies, no demanded payments — but the balance remains and interest keeps accruing. The 10-year collection statute (CSED) keeps running while you're in CNC, so if your finances never recover, part or all of the debt can expire before the IRS collects it. The IRS reviews CNC accounts periodically and can reactivate collection if your income rises.

Can I get an Offer in Compromise because of medical hardship?

You may qualify if your income and assets genuinely can't cover the debt — medical expenses shrink both sides of that math. The application costs $205 with 20% down on lump-sum offers, but low-income certification (AGI at or below 250% of the poverty line) waives the fee, the down payment, and payments during review. A rarer effective tax administration offer exists for cases where illness makes full collection unfair even when assets could technically cover it.

I emptied my 401(k) to pay for treatment — is that why I owe?

Very likely. Early retirement withdrawals are taxed as ordinary income and usually add a 10% penalty, so a $40,000 medical withdrawal can create a five-figure tax bill by itself. The debt is real, but the same hardship that forced the withdrawal supports penalty abatement and hardship-based collection options. See our guide to the 401(k) withdrawal tax bill you can't pay for the specifics.

Your next 24 hours

- Find your most recent IRS notice and check the code in the corner and the date at the top. A CP14 means you're early; a CP504 or LT11 means a levy clock is running — the LT11's 30-day hearing deadline is the one you cannot get back.

- Gather your proof: last year's return, the notice, two recent pay stubs, your lease, and three months of medical bills and insurance statements. That stack is your entire hardship case.

- Get a free case review — the form takes 2 minutes, or call (888) 825-7779. An experienced tax professional will run your medical-hardship math the way the IRS runs it and tell you which option the numbers actually support, before the next payday or the 21-day bank hold decides for you.

For the primary sources behind this guide, see the IRS's official pages on payment plans and installment agreements and the Offer in Compromise program, and the Taxpayer Advocate Service for hardship cases the normal channels won't move.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.