Tax Debt by Amount

I Owe the IRS $20,000 — What Do I Do? Every Option for 2026

The short answer: owing the IRS $20,000 puts you under every major enforcement threshold. You can set up a 72-month payment plan online — no financial disclosure — for a minimum of about $278 a month. Your passport is safe (the 2026 threshold is $66,000), and a lien is usually avoidable if you act before the CP504 stage.

If you're thinking "I owe the IRS $20,000 and I have no idea what happens next," here's the part nobody tells you up front: $20,000 is the balance the IRS resolves most routinely. It's below the $25,000 streamlined cutoff, the $50,000 online-plan limit, and the $66,000 passport threshold — which means every door is still open, and most of them open from your phone.

Maybe the number came from a CP14 in the mail, a tax return you just filed, or years of 1099 income with nothing withheld. Either way, the two tables below show exactly what the IRS sends next if you wait — and why $20,000 is a meaningfully better position than $26,000.

⏱ The clock that's actually running: there's no single due date on a $20,000 balance — but the failure-to-pay penalty adds $100 every month (0.5% of $20,000), and interest compounds daily on top. Each collection notice that arrives starts a shorter clock and takes an option off the table.

Why you owe the IRS $20,000 — and why this band is different

A $20,000 IRS debt sits below every threshold that triggers heavier enforcement, so it's handled almost entirely by the IRS's automated collection system, not a human revenue officer. That cuts both ways: no agent is building a case against you, but no human is pausing the notice machine either.

Most $20,000 balances come from a handful of causes: a year of gig or 1099 income with no withholding (self-employment tax alone runs 15.3% before income tax), an early retirement withdrawal, a CP2000 income-matching adjustment, or two or three smaller years stacking up.

Where you sit matters more than how you got here. Here's how the IRS's own program thresholds treat different balances in 2026:

| Balance owed | What's available | What it means in practice |

|---|---|---|

| Under $10,000 | Guaranteed installment agreement | The IRS must accept a qualifying plan; almost no negotiation needed. |

| $10,000–$25,000 (you are here) | Streamlined agreement, online setup, up to 72 months | No financial disclosure. Direct debit generally keeps a lien off the record — and can support lien withdrawal if one was filed. |

| $25,001–$50,000 | Online plan still available, up to 72 months | Streamlined treatment generally requires direct debit at this level. |

| $50,001 and up | Payment plan with financial disclosure (Form 433 series) | The IRS reviews income, expenses, and assets before agreeing to terms. |

| $66,000 and up (2026) | Passport certification exposure begins | "Seriously delinquent" debt can block passport issuance or renewal. |

One caution before you relax into that middle row: penalties and interest compound. Neglected long enough, a $20,000 balance climbs toward the $25,000 line, where the rules tighten. If your balance is already near a boundary, the owe IRS $25,000 guide covers what changes above that line, and the owe IRS $15,000 guide covers the band below.

What happens if you ignore a $20,000 tax debt

An ignored $20,000 balance moves through five automated notice stages before the IRS can touch your wages or bank account. The sequence never skips you and never forgets you — it just escalates:

- CP14 — the first bill. No enforcement yet; the cheapest moment to fix anything. (Holding one now? See the CP14 notice guide.)

- CP501 / CP503 — reminder notices. Still just bills, but the balance grows every month they sit.

- CP504 — Notice of Intent to Levy under IRC §6331(d). The IRS can now seize your state tax refund, and a federal tax lien becomes realistic.

- LT11 / Letter 1058 — the final notice. A 30-day clock starts on your Collection Due Process appeal rights (requested with Form 12153).

- Levy — wages, bank accounts, and up to 15% of Social Security through the Federal Payment Levy Program.

Each stage carries a window — and a right you lose when it closes:

| Notice | Typical response window | What you lose if it passes |

|---|---|---|

| CP14 | About 21 days from the notice date | The lowest-cost resolution point; penalties keep stacking after it. |

| CP501 / CP503 | Date printed on each notice | The last low-stakes window to set up a plan before enforcement language starts. |

| CP504 | 30 days printed on the notice | Your state tax refund becomes seizable; lien filing becomes likely. |

| LT11 / Letter 1058 | 30 days | Your Collection Due Process hearing rights (Form 12153) — your strongest formal appeal. |

| Active levy | Bank levy: 21-day hold before funds leave | Prevention. A wage levy is continuous until released; recovering seized funds is far harder than stopping the levy beforehand. |

One 2026 reality worth naming: IRS staffing fell roughly 27% in 2025, so reaching a human is harder than ever — but the notices, liens, and levies are generated by automated systems that never got cut. Silence from the IRS is not the same as safety.

A worked example: how "about $20,000" became $36,900

This is hypothetical, but the math is real. Say you're a rideshare-and-delivery driver who hasn't filed taxes in 3 years — 2023, 2024, and 2025. Your back-of-envelope guess was "around $20,000." Then the returns get prepared, and the combined income and self-employment tax comes to $24,300 ($8,900 + $8,300 + $7,100). Here's what the IRS adds on top:

- Failure-to-file penalties: roughly $5,450. This penalty runs at 5% per month and maxes out fast — it's 10 times the failure-to-pay rate, though in months where both penalties apply the failure-to-file portion drops to 4.5% (5% combined), which is the rate used in this figure. It's why the failure to file penalty vs failure to pay distinction is the most expensive lesson in this scenario.

- Failure-to-pay penalties so far: roughly $2,600 — 0.5% per month per year, still running.

- Interest: roughly $4,550 — compounding daily on the tax and the penalties, still growing.

Total balance: about $36,900. The good news even here: that's still under $50,000, so the online 72-month plan remains available — at a minimum of about $513 a month ($36,900 ÷ 72) instead of the $278 a true $20,000 balance would cost. Filing those returns in year one would have avoided most of the single biggest line item. You can estimate your own penalty and interest buildup with our IRS Penalty & Interest Calculator.

Owe around $20,000 and not sure which option fits?

Penalties and interest are accruing either way — about $100 a month in late-payment penalty alone at this balance, before interest. An experienced tax professional will review your balance, your years, and your budget for free, and tell you exactly which path costs least.

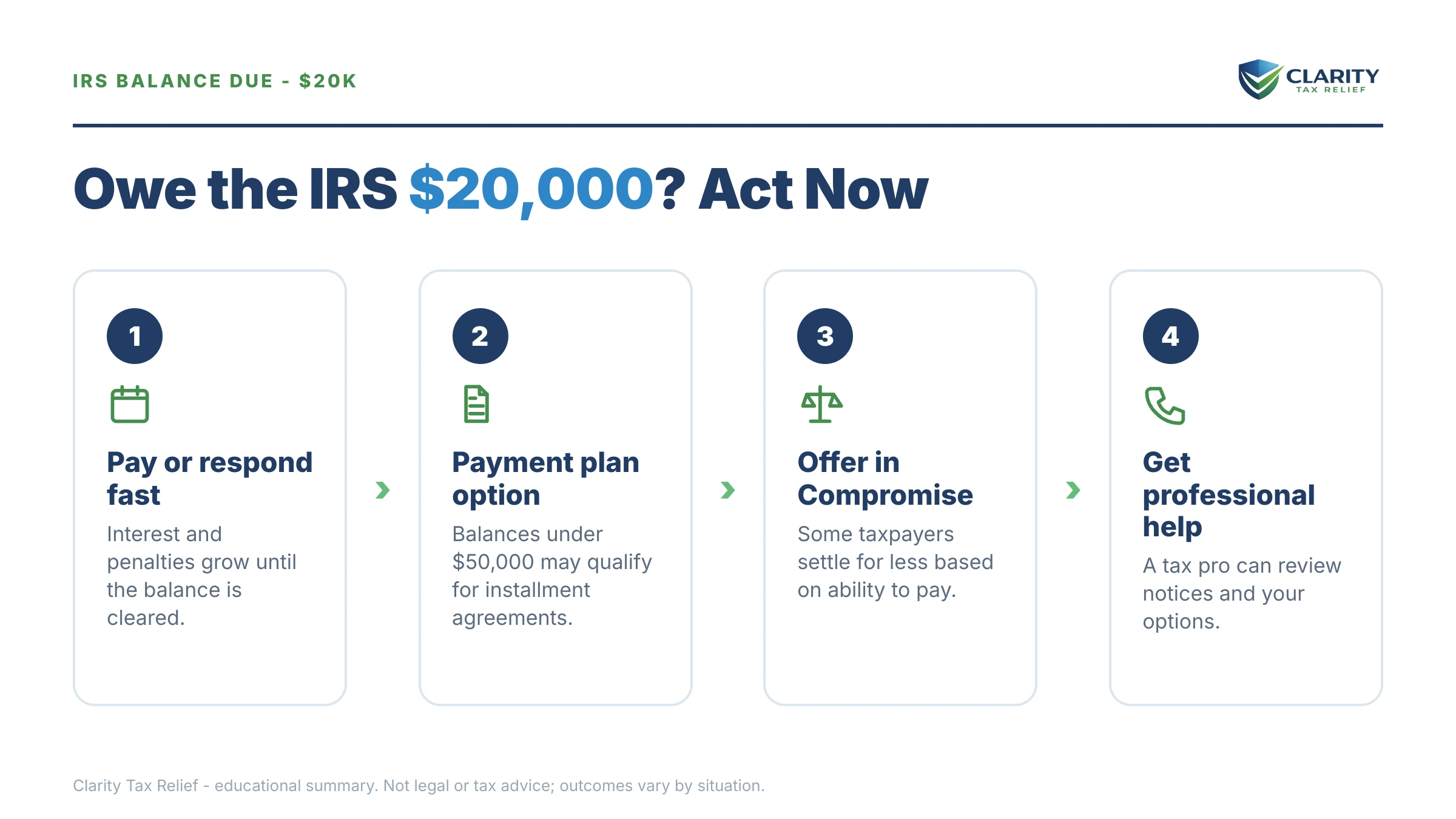

Your options when you owe the IRS $20,000

At $20,000 you have six realistic paths, and for most people the 72-month online payment plan is the default. (For the full DIY playbook on each program, see our guide to how to settle tax debt yourself — below is how each one behaves at exactly this balance.)

- Pay in full. Stops all penalties and interest immediately. Worth a hard look at savings or even a lower-interest personal loan, since IRS interest compounds daily and penalties stack on top of it.

- Short-term plan — up to 180 days. $0 setup fee. If a bonus, tax refund, or asset sale can clear $20,000 within six months, this is the cheapest structured option. Interest and the 0.5% monthly penalty continue until paid.

- Long-term installment agreement — the workhorse. Because $20,000 is under $25,000, you qualify for a streamlined installment agreement: up to 72 months, no financial disclosure, set up entirely online — balances up to $50,000 also qualify for online setup (direct debit is typically required above $25,000), and under the IRS's Simple Payment Plan, which replaced the streamlined agreement in 2025, payment terms can run up to the 10-year collection statute, not just 72 months. Minimum payment is about $278 a month; the failure-to-pay penalty drops to 0.25% monthly once the agreement is active, but interest continues — so paying $350–$400 a month finishes years earlier and costs meaningfully less. Walkthrough: how to set up an IRS payment plan online. Setup fees vary by method and are lowest with direct debit; low-income taxpayers may qualify for fee reduction or waiver.

- Currently Not Collectible (CNC). If paying anything would leave you unable to cover basic living expenses, IRS Currently Not Collectible status pauses levies and collection. The debt doesn't go away — penalties and interest still accrue, and refunds get kept — but it buys breathing room while the 10-year collection clock keeps running.

- Offer in Compromise (OIC). Settling for less than $20,000 is real but strictly means-tested: the IRS runs the math on your income and assets, and it accepted roughly 1 in 5 offers in FY2024. The $205 application fee and 20% down payment on lump-sum offers (both waived with low-income certification, AGI at or below 250% of the poverty level) make a bad application expensive. Blunt truth: if you can afford $278 a month, the IRS usually concludes a payment plan collects more than your offer would. See how does an offer in compromise work before spending anything on Form 656.

- Penalty relief. If your prior three years were clean, first-time penalty abatement can strip penalties from a year — often worth $1,000+ at this balance. And starting summer 2026, the IRS's Automatic Exemption from Penalty (AEP) begins applying some penalty relief automatically, with no request required. Interest on removed penalties comes off too.

How to resolve a $20,000 IRS debt, step by step

- Pull your real balance. Log into your IRS online account and confirm the exact balance, which tax years it covers, and whether any returns show as unfiled. The number in your head and the number the IRS is collecting are often different.

- File any missing returns immediately. The IRS will not approve a payment plan, hardship status, or an offer while required returns are unfiled — and the failure-to-file penalty runs at 10 times the failure-to-pay rate (though in months where both apply, the failure-to-file portion drops to 4.5 percent, for 5 percent combined), so filing is the single fastest way to stop the bleeding.

- Choose the option that fits your budget. If you can pay within 180 days, use the short-term plan with no setup fee. If not, a 72-month online agreement at roughly $278 or more per month is the default; hardship status or an Offer in Compromise apply only if your finances genuinely cannot support payments.

- Set the agreement up before the next notice. Apply through the IRS Online Payment Agreement tool or mail Form 9465. Choose direct debit — it lowers the setup fee, prevents accidental default, and is the key to avoiding a federal tax lien at this balance.

- Request penalty relief. If you have a clean compliance history for the prior three years, first-time abatement can remove penalties on the oldest year — and starting summer 2026, the IRS's Automatic Exemption from Penalty applies some relief automatically, with no request needed.

When you can handle $20,000 yourself — and when help changes the outcome

Most people with a single filed year, a balance they agree with, and room for $278+ a month can resolve a $20,000 debt themselves in about 20 minutes online. If that's you: set up the direct-debit plan, request first-time abatement, and be done. You don't need to pay anyone for that.

Experienced help earns its cost in specific situations:

- Multiple unfiled years. The order matters — returns first, then penalties, then the balance — and if the IRS filed substitute returns for you, they almost always overstate the tax because they include zero deductions. Correct returns can shrink the debt before you negotiate it.

- Gig or self-employment income. Reconstructing mileage, platform fees, and expenses across old years is where a $24,300 assessment becomes a much smaller one.

- A CP504 or LT11 already arrived. Deadlines with real teeth are now attached, and appeal rights expire on a fixed clock.

- You genuinely can't afford the streamlined payment. Negotiating CNC or a lower payment requires Form 433-F financial disclosure, and how expenses are presented against IRS allowable-living-expense standards changes the result.

- You're weighing an OIC. The eligibility math should be run — honestly — before any fee is paid, ours included.

If money is tight, know that free options exist too: the Taxpayer Advocate Service helps when IRS processes are causing hardship, and Low Income Taxpayer Clinics represent qualifying taxpayers at no charge.

Terms you'll keep seeing, decoded

- Streamlined installment agreement — a payment plan approved without financial disclosure because the balance is under the threshold; at $20,000, that's you.

- Failure-to-file vs. failure-to-pay — two separate penalties: 5% per month for not filing versus 0.5% per month for not paying, which is why you always file even when you can't pay.

- CSED — the Collection Statute Expiration Date: the IRS generally has 10 years to collect back taxes from assessment, though appeals, offers, and bankruptcy pause the clock.

- Currently Not Collectible (CNC) — an IRS status that pauses collection when paying would create genuine hardship; the debt and its interest remain.

- Notice of Federal Tax Lien — a public filing that attaches the government's claim to your property; at balances under $25,000 on direct debit, it's usually avoidable.

Owe the IRS $20,000? Your questions, answered

Can I set up a payment plan online if I owe the IRS $20,000?

Yes. Because $20,000 is under the $50,000 online threshold, you can set up a long-term payment plan of up to 72 months through your IRS online account, usually in under 20 minutes and without submitting any financial disclosure forms — balances up to $50,000 also qualify for online setup (direct debit is typically required above $25,000), and under the IRS's Simple Payment Plan, which replaced the streamlined agreement in 2025, payment terms can run up to the 10-year collection statute, not just 72 months. You need to be current on filing — the system rejects applications while required returns are missing, so file any overdue years first.

How much per month is a payment plan on $20,000 of IRS debt?

The minimum the IRS typically accepts on a 72-month plan is the balance divided by 72 — about $278 a month on $20,000. Interest and a reduced late-payment penalty keep accruing while you pay, so budgeting $350 to $400 a month pays the debt off faster and cuts the total cost. There is no prepayment penalty for paying it down early.

Will the IRS settle a $20,000 debt for less than I owe?

Only if your finances genuinely support it. An Offer in Compromise is accepted when $20,000 is more than the IRS could realistically collect from your income and assets before the collection statute expires — and the IRS accepted roughly 1 in 5 offers in FY2024. If you can afford about $278 a month, the IRS will usually see a payment plan as the answer instead.

Will the IRS file a lien on my house for $20,000?

It can, but at $20,000 it usually will not if you act. The IRS generally holds off on filing a Notice of Federal Tax Lien when a balance under $25,000 is being paid through a direct-debit installment agreement — and if a lien was already filed, you may qualify to request its withdrawal after several consecutive direct-debit payments. Ignoring the notice sequence is what makes a lien likely.

Can the IRS take my passport over $20,000?

No. Passport certification under the seriously delinquent tax debt rules applies at $66,000 or more for 2026, and it also requires that a lien has been filed or a levy issued. A $20,000 balance is well below the threshold — though penalties and interest can push a neglected balance toward it over several years.

Will the IRS garnish my wages for a $20,000 balance?

Not without warning. The IRS must send a final notice of intent to levy — the LT11 or Letter 1058 — and give you 30 days to respond before garnishing wages, and that notice comes after the CP14, CP501, CP503, and CP504 stages. Entering a payment plan at any point before the levy starts stops the sequence. Once a wage levy begins, it is continuous until released.

Does a $20,000 IRS debt expire after 10 years?

Generally yes — the IRS has 10 years from the date the tax was assessed to collect (the CSED), after which the remaining balance is written off. But the clock pauses during an Offer in Compromise, bankruptcy, certain appeals, and time spent abroad, so 10 calendar years often stretches longer. Waiting out a $20,000 debt also means a decade of notices, refund offsets, and levy exposure.

Your next 24 hours

- Pull the real number. Log into your IRS online account and write down the exact balance, the tax years it covers, and whether any return shows as unfiled. If it's correct and affordable, you can even start a plan today at IRS.gov/payments.

- Gather three things: your last filed return, every IRS notice you've received, and this year's income documents (1099s, W-2s) — everything any resolution path will need, in one folder.

- Get the free case review. Call (888) 825-7779 or use the 2-minute form. An experienced tax professional will map your $20,000 balance against every program above — remember, penalties and interest accrue until a resolution is actually in place.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.