Tax Debt by Amount

Owe the IRS $25,000? Every Realistic Option in 2026

The short answer: if you owe the IRS $25,000, you can typically set up a payment plan online in about 15 minutes — roughly $348 per month over 72 months — with no financial disclosure required. Choose direct debit and you may also qualify to have a federal tax lien withdrawn. Interest and penalties keep accruing until it's paid.

You ran the numbers three times hoping the software was wrong, and it wasn't: between this year's balance and what's already sitting on prior years, you owe the IRS $25,000 on a regular W-2 paycheck. It feels like a number that shouldn't be possible when taxes come out of every check. It's fixable — and $25,000 is actually one of the easier balances to fix, because you sit exactly on the line where the IRS's friendliest rules still apply.

Three facts make this balance different from $20,000 or $30,000. First, $25,000 is the ceiling for a streamlined installment agreement without a direct-debit requirement. Second, it's the last balance at which a filed tax lien can be withdrawn through a direct-debit plan. Third, the minimum payment math still works on one income. This guide walks through all three.

⏱ The real clock: there's no single deadline on a $25,000 balance — but the failure-to-pay penalty adds 0.5% every month and interest compounds daily. On this balance that's roughly $111 in penalty alone each month before interest — 0.5% of the $22,200 in unpaid tax, since the penalty accrues on the tax itself — and each unanswered notice moves you one step closer to a levy.

Why you owe the IRS $25,000 — and why the number keeps moving

A $25,000 IRS balance is rarely one bad year — it's usually two or three moderate shortfalls stacked with penalties and interest. For W-2 employees, the most common engines are a second job that withheld as if it were your only income, a bonus or RSU vest withheld at a flat rate below your actual bracket, or an early 401(k) withdrawal that added tax and a 10% penalty the withholding never covered.

The number on your notice is also not the number you'll owe next month. Every 30 days, the failure-to-pay penalty adds another 0.5% and interest compounds on the whole pile — tax, penalties, and prior interest together. Your IRS online account shows the payoff figure by tax year, which matters because relief options like penalty abatement are applied year by year, not to the lump total.

Before choosing any option, confirm what portion of the $25,000 is penalty. On a balance built over two or three years, penalties commonly make up 10–20% of the total — and unlike tax and interest, penalties are frequently removable.

What $25,000 in IRS debt actually costs each month

An unresolved $25,000 balance grows by about $111 a month (0.5% of the $22,200 in unpaid tax — the penalty accrues on the tax itself, not on penalties or interest) in failure-to-pay penalty, plus daily-compounding interest at the federal short-term rate plus 3%. The penalty caps at 25% of the unpaid tax, but interest never caps — it runs until the balance is paid or the collection statute expires.

Two levers change that math immediately. Getting on an installment agreement cuts the monthly penalty rate in half, to 0.25%. And if you have any unfiled return in the mix, filing it stops the failure-to-file penalty — which at 5% per month is ten times the failure-to-pay penalty. You can estimate how much your specific balance is growing with our Penalty & Interest Calculator — it estimates accrual; only your IRS account shows the official figure.

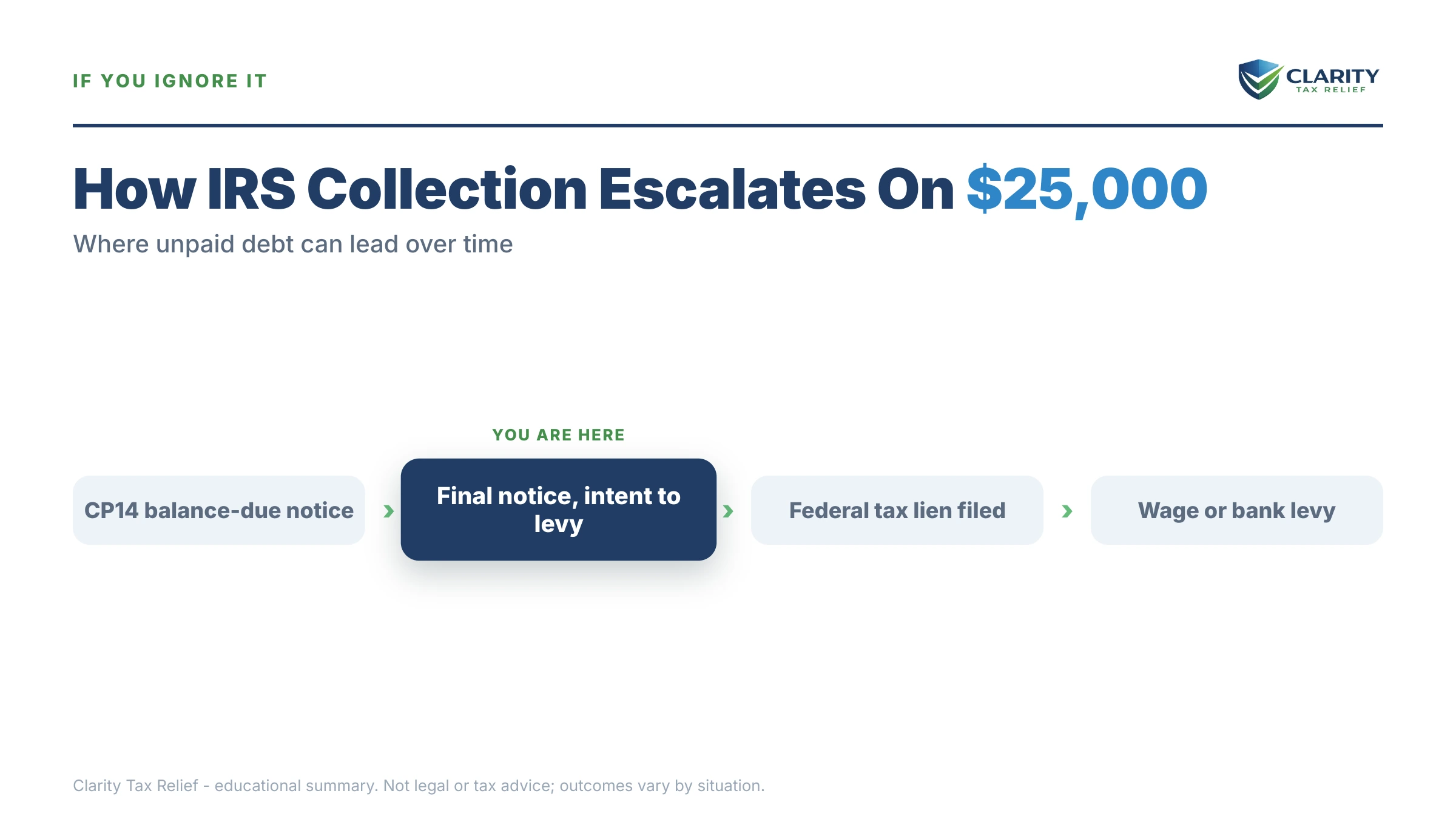

What happens if you ignore $25,000 in tax debt

A $25,000 balance moves through the IRS's automated collection sequence the same way a $2,500 balance does — the letters just carry bigger numbers and the lien question arrives sooner. The sequence runs in this order:

- CP14 — the first bill. You typically have about 21 days from the notice date before the reminder cycle starts (10 business days when the balance is $100,000 or more).

- CP501 / CP503 — automated reminders, each arriving with a larger balance. Still no enforcement, but the account is moving through the queue.

- CP504 — Notice of Intent to Levy. The IRS can now seize your state tax refund, and at $25,000 a Notice of Federal Tax Lien is a live possibility — the IRS routinely considers filing once a balance passes $10,000.

- LT11 or Letter 1058 — the final notice. It starts a 30-day clock and your Collection Due Process rights (requested on Form 12153). After 30 days, levies become legal.

- Levy — a bank levy freezes funds with a 21-day hold before the money leaves; a wage levy is continuous, hitting every paycheck until it's released.

Don't count on 2026 staffing problems to slow this down. The IRS workforce shrank roughly 27% in 2025, which makes it harder to reach a human — but the notice stream, lien filings, and levies are generated by automated systems that never stopped running.

Owe around $25,000 and not sure which option fits?

A free case review maps your exact balance — how much is removable penalty, whether the $348/month plan or something lower fits your budget, and how to protect your lien position — before another month of interest posts.

Your options when you owe the IRS $25,000

At $25,000, every major IRS resolution program is still on the table, and the streamlined rules mean most of them don't require handing over a financial statement. Here's how they compare at this exact balance:

| Option | Who it fits at $25,000 | What it costs |

|---|---|---|

| Pay in full | You have savings or can borrow at a lower rate than IRS interest | $0 setup; stops penalties and interest immediately |

| Short-term payment plan | You can clear $25,000 within 180 days | $0 setup; penalties and interest continue until paid |

| Streamlined installment agreement | Steady income; up to 72 months at roughly $348/month minimum, no financial disclosure | Setup fee (lower with direct debit, reduced or waived for low income); penalty rate drops to 0.25%/month |

| Partial-pay installment agreement | Your budget genuinely can't support $348/month | Requires Form 433-F financials; periodic IRS review; unpaid remainder can expire at the 10-year CSED |

| Currently Not Collectible | Paying anything would prevent basic living expenses | $0; collection pauses, but interest accrues and refunds are kept |

| Offer in Compromise | Income and assets genuinely can't cover $25,000 before the statute runs | $205 fee plus 20% down on lump-sum offers (both waived with low-income certification); roughly 1 in 5 accepted in FY2024 |

| Penalty abatement (FTA / AEP) | Clean compliance for the prior 3 years, or reasonable cause | Free to request; removes penalties and their interest, not the underlying tax |

These options aren't mutually exclusive — the strongest sequence for most people at this balance is penalty abatement first, then a direct-debit installment agreement on the reduced figure. For the full do-it-yourself playbook on each program, see our guide to how to settle tax debt yourself.

The $25,000 lien rule most people miss

$25,000 is the last balance at which a filed federal tax lien can be undone through a payment plan alone. If your assessed balance is $25,000 or less and you're on a direct-debit installment agreement, you can request lien withdrawal on Form 12277 after three consecutive direct-debit payments — erasing the public record, not just marking it paid. Above $25,000, that door closes, which is one reason to resolve this balance before another year's interest pushes you past the line.

The $25,000 payment plan, worked out

Here's a clearly hypothetical example with the arithmetic shown. Say you're a single W-2 employee whose second job under-withheld about $7,400 a year for three straight years: 3 × $7,400 = $22,200 in tax, plus roughly $2,800 in failure-to-pay penalties and compounded interest — a $25,000 balance.

- Minimum plan: $25,000 ÷ 72 months ≈ $348/month. Interest and the reduced 0.25% monthly penalty keep accruing, so the true payoff runs longer than the raw division suggests unless you pay above the minimum.

- Faster plan: at $600/month, the principal alone clears in about 42 months ($25,000 ÷ $600 ≈ 41.7) — cutting years of interest compared with the minimum.

- Penalty relief first: if the earliest of the three years follows a clean three-year compliance history, first-time abatement could remove that year's failure-to-pay penalty (and the interest charged on it) before you even start the plan. Later years need reasonable cause, since the prior years are no longer clean.

The order matters: abate penalties first, then set the plan on the smaller balance, so your $348 (or $600) works against tax instead of removable penalties.

Can you settle $25,000 with the IRS for less?

The IRS accepted roughly 1 in 5 Offers in Compromise in FY2024 — settlement is real, but it's means-tested math, not a discount program. The IRS computes your Reasonable Collection Potential: the equity in what you own plus a multiple of your monthly disposable income after allowed living expenses. It accepts an offer only when that figure comes out below $25,000.

Honest framing for a W-2 earner: steady paychecks usually produce a collection potential above $25,000, because the IRS counts years of future income it can reach through a plan or levy. An offer becomes realistic when income has genuinely dropped, expenses are high for allowable reasons, or assets are thin. If that describes you, the application runs through Form 656 with a $205 fee and a 20% down payment on lump-sum offers — all waived if your AGI is at or below 250% of the poverty level. Start with how an offer in compromise actually works before paying anyone to file one.

How the rules change above and below $25,000

IRS payment-plan rules shift at specific dollar lines, and $25,000 is one of them. This is where your balance sits in the bigger picture:

| Balance | What changes | Guide |

|---|---|---|

| $10,000 or less | The guaranteed installment agreement — approval is required by law if you meet basic filing and payment conditions | I owe the IRS $10,000 |

| $10,001–$25,000 | Streamlined agreement with no financial disclosure and no direct-debit mandate; lien filing becomes a live consideration above $10,000 | I owe the IRS $20,000 |

| $25,001–$50,000 | Online plans remain available, but direct debit or payroll deduction is generally required — and the Form 12277 lien-withdrawal path ends | I owe the IRS $50,000 |

| $50,001+ | Financial disclosure (Form 433 series) generally required; the IRS reviews assets, equity, and monthly cash flow | I owe the IRS $100,000 |

| $66,000+ (2026) | Passport certification threshold — the State Department can deny or revoke a passport on a "seriously delinquent" debt | — |

The practical takeaway: at $25,000 you're one year of accrual away from losing the no-direct-debit option and the lien-withdrawal path. Acting this year preserves both.

How to respond when you owe the IRS $25,000, step by step

- Verify the balance. Log in to your IRS online account and confirm the $25,000 figure, which tax years it covers, and how much is penalty versus tax — the penalty portion may be removable.

- File any missing returns. The IRS won't approve a payment plan while required returns are unfiled, and the failure-to-file penalty is ten times the failure-to-pay penalty — filing stops the most expensive clock first.

- Choose your resolution. Pick full payment within 180 days, a 72-month installment agreement (about $348 per month minimum), a partial-pay agreement, or hardship status — based on what your budget genuinely supports.

- Set it up online with direct debit. Use the IRS Online Payment Agreement tool; direct debit lowers the setup fee, prevents missed-payment defaults, and protects your lien position at this exact balance.

- Request penalty relief. If you've been compliant for the prior three years, ask for first-time abatement on the failure-to-pay penalty — and starting summer 2026, the IRS's Automatic Exemption from Penalty may apply relief without a request.

When you can handle $25,000 yourself — and when help changes the outcome

Most people who owe exactly $25,000 can resolve it themselves in one online session. If you agree with the balance, every return is filed, and roughly $348 a month fits your budget, set up the plan directly through the IRS — no firm required. Add a first-time penalty abatement request by phone or letter and you've done what most professionals would do first.

Experienced help earns its fee in the harder versions of this balance: a levy notice already in motion, multiple unfiled years that have to be reconstructed and sequenced before any plan is possible, a lien already filed while you're trying to refinance or buy, a budget that can't support the streamlined minimum (where partial-pay and hardship math gets adversarial), or a genuine offer candidacy where one wrong figure on the financial statement sinks the application. In those cases, an experienced tax professional isn't buying convenience — they're changing which program you end up in.

What your transcript shows when you owe $25,000

Your IRS account transcript tells you where a $25,000 balance actually stands — what's been assessed, what's penalty, and whether enforcement markers have posted. These are the codes that matter at this balance:

| Code | What it means | What to do |

|---|---|---|

| 150 | Return filed and tax assessed — the starting balance for that year | Confirm the assessed amount matches the return you filed |

| 276 | Failure-to-pay penalty posted | Check first-time abatement eligibility — this penalty is often removable |

| 196 | Interest charged to the account | Interest itself is rarely waived, but it stops compounding on penalties once they're abated |

| 971 | A notice was issued | Match the date to the letter in your mailbox and note its response window |

| 582 | Federal tax lien indicator | At $25,000 or less, a direct-debit plan plus Form 12277 may support full withdrawal |

| 530 | Account placed in Currently Not Collectible | Collection is paused — expect periodic income reviews |

Terms you'll see at this balance, decoded

- Streamlined installment agreement: a payment plan approved without a financial statement — available at $25,000 with the fewest strings of any balance band.

- Direct-debit installment agreement (DDIA): a plan paid automatically from your bank account; at $25,000 it's the key to avoiding or withdrawing a lien.

- Notice of Federal Tax Lien: a public filing that attaches the government's claim to everything you own — different from a levy, which actually takes property.

- CSED: the collection statute expiration date — the IRS generally has 10 years from assessment to collect, though appeals, offers, and bankruptcy pause the clock.

- Failure-to-pay penalty: 0.5% of unpaid tax per month (0.25% on an installment agreement), capped at 25%.

- Reasonable Collection Potential: the IRS's calculation of everything it could collect from you — the number an Offer in Compromise must clear.

Owe the IRS $25,000: your questions answered

Can I set up a payment plan online if I owe the IRS $25,000?

Yes. Balances up to $50,000 in combined tax, penalties, and interest qualify for a long-term payment plan through the IRS Online Payment Agreement tool, with up to 72 months to pay. At $25,000 the minimum works out to roughly $348 per month. You'll need every required return filed first — the IRS won't approve a plan while returns are missing.

Will the IRS file a tax lien if I owe $25,000?

It can — the IRS routinely considers filing a Notice of Federal Tax Lien once a balance passes $10,000. But at $25,000 you have unusual leverage: set up a direct-debit installment agreement and you can generally avoid a new lien filing, and if one has already been filed, you may request withdrawal on Form 12277 after three consecutive direct-debit payments. That withdrawal option disappears once your assessed balance climbs above $25,000.

Can I settle $25,000 in IRS debt for less than I owe?

Only if the IRS's own math shows it could never collect the full $25,000 from your income and assets before the collection statute runs out. An Offer in Compromise carries a $205 application fee and, for lump-sum offers, a 20% down payment — both waived with low-income certification. The IRS accepted roughly 1 in 5 offers in FY2024, so treat any promise of easy settlement as a red flag.

How fast do penalties and interest grow on $25,000?

The failure-to-pay penalty adds 0.5% per month — about $111 a month (0.5% of the $22,200 in unpaid tax — the penalty accrues on the tax itself, not on penalties or interest) — up to a 25% cap, and interest compounds daily at the federal short-term rate plus 3%. Setting up an installment agreement cuts the monthly penalty rate in half, to 0.25%. If you also have an unfiled return, the failure-to-file penalty is ten times larger, so file first.

Can the IRS take my passport over $25,000?

No — passport certification requires a 'seriously delinquent' balance of $66,000 or more in 2026, and $25,000 is well under that line. The catch is that penalties and interest keep compounding, and adding another unpaid year can move you toward the threshold faster than you'd expect. Resolving the balance now keeps the passport question permanently off the table.

Can the IRS garnish my wages if I owe $25,000?

Yes, but not without warning. The IRS must first send a final notice of intent to levy — usually an LT11 or Letter 1058 — and give you 30 days to respond or request a Collection Due Process hearing. Once a wage levy starts, it's continuous until the debt is resolved or the levy is released, which is why acting during the notice stage matters so much.

Does owing the IRS $25,000 hurt my credit score?

Not directly — the three credit bureaus stopped reporting federal tax liens in 2018, so an IRS balance never appears on your credit report. But a filed lien is still a public record that mortgage and business lenders can find, and many loan applications ask about tax debt outright. A direct-debit payment plan at this balance is the cleanest way to keep a lien from being filed at all.

What if I can't afford $348 a month on $25,000?

You have two real paths. A partial-pay installment agreement lets you pay what your budget actually supports after the IRS reviews a financial statement, with the rest potentially expiring at the 10-year collection deadline. If paying anything would leave you unable to cover basic living expenses, Currently Not Collectible status pauses collection entirely — though interest keeps accruing and the IRS reviews your income periodically.

Your next 24 hours

- Pull the official number. Log in to your IRS online account and write down the balance by tax year — and how much of each year is penalty versus tax.

- Gather three things: your most recent tax return, your last two pay stubs, and a rough list of monthly expenses. That's everything needed to know which option fits.

- Get the free case review. Call (888) 825-7779 or use the 2-minute form — a review of your $25,000 balance costs nothing, and every month you wait adds roughly $111 in penalty plus compounding interest.

Primary sources if you want to go straight to the IRS: the official IRS payment plans and installment agreements page, the IRS payments portal, and — if collection action is causing hardship the normal channels won't fix — the Taxpayer Advocate Service.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.